Increasing the D.C. EITC to 25

Percent of the Federal EITC Would Help Working Families Escape Poverty and Address

Continuing Inequities in the D.C. Tax System

by Ed Lazere, Iris Lav, and Bob Zahradnik

Summary

| View PDF version If you cannot access the file through the link, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

In 2000, the District adopted a new Earned Income Tax Credit equal to 10 percent of the federal EITC. Earned Income Tax Credits provide tax refunds to working poor and near-poor families with children and boost the incomes of families seeking to work their way out of poverty. In addition, the new D.C. EITC addresses some long-standing inequities in the D.C. tax system. In adopting the credit, D.C. joined 14 other states, including Maryland, that have a state Earned Income Tax Credit. (Montgomery County, Maryland also enacted an EITC in 2000 to augment the state's EITC.)

Over 50,000 District households are eligible and could benefit from the D.C. EITC as they file tax returns this year, receiving up to $300 in tax refunds as a result. Available data suggests that there are likely to be a substantial number of D.C. EITC recipients in most wards of the city.

The D.C. EITC accomplishes several positive goals. It provides low-income District residents with relief from the high tax burdens they face, provides an income boost that helps lift working families out of poverty, and supports efforts to move families from welfare to work. The D.C. EITC builds on the strengths of the federal EITC, which is now the most effective program for lifting working families out of poverty. By making work pay better, the EITC has been shown to encourage low-income parents to enter the work force.

On January 23, 2001, a bill was introduced to raise the D.C. EITC to 25 percent of the federal EITC. The bill, which was co-sponsored by all 13 members of the D.C. Council, would cost roughly $11 million per year.

Increasing the D.C. EITC to 25 percent of the federal credit would further address the goals of the D.C. EITC enacted last year in several important ways.

Before 2000, for example, the income tax burden on low-and moderate-income families in the District was among the highest in the country. Moreover, the income tax structure resulted in a substantial "cliff" for some families, where a single additional dollar of income triggered a large increase in tax liability. The $288 million tax cut in the District's Tax Parity Act of 1999 did little to address either of these problems. The D.C. EITC enacted in 2000 (described in this report as the "10 percent D.C. EITC") made significant progress in eroding the cliff and reducing the tax burden on near-poor families, but it did not eliminate these problems. A larger D.C. EITC would resolve these problems in the D.C. income tax for most families with children.

- A 25 percent D.C. EITC would reduce the high tax burden on near-poor families. If the Tax Parity Act's lower rates had been fully implemented in 2000, a two-parent family of four with income of $22,002, or 125 percent of the federal poverty line, would have owed D.C. income tax of approximately $671 without the 10 percent EITC. That would be the fourth highest income tax burden at that level in the nation. The 10 percent D.C. EITC reduces that tax burden to $479, still higher than all but seven states. A D.C. EITC set at 25 percent of the federal credit would reduce such a family's burden to $190, which would put D.C.'s tax on the family approximately in the middle of all states that have an income tax.

- A 25 percent D.C. EITC would eliminate the income tax "cliff" for most families. The District's income tax has a low-income credit that offsets 100 percent of the taxes owed by families with incomes at or below roughly the poverty line. Families just above the ceiling, however, are not eligible for the low-income credit. This creates an income tax "cliff" where a single additional dollar of income can increase a family's tax from zero to a very substantial level. The 10 percent D.C. EITC greatly reduced the cliff, but did not eliminate it for all families. For example, a family of four could see its income tax burden jump from zero to $316 just by having an additional dollar of income. A D.C. EITC set at 25 percent of the federal credit would eliminate the tax cliff for nearly all families.

- A 25 percent D.C. EITC would ensure that all families benefit from recent tax relief efforts. Some families received no benefit from either the Tax Parity Act or the 10 percent D.C. EITC. Families that claim the D.C. EITC cannot claim the low-income credit. Yet for some families — such as families of four with incomes between $15,700 and $18,555 — the 10 percent D.C. EITC provides less relief than the low-income credit. Thus, these families cannot take advantage of the D.C. EITC (and instead continue to claim the low-income credit). While these families owe no income tax, they pay a substantial amount of their income in sales, excise, and property taxes. A 25 percent D.C. EITC would ensure tax relief for nearly all working families with children and incomes below $25,000.

Beyond addressing problems in the District's income tax, a larger D.C. EITC would provide a greater income supplement to families that work but remain low-income. Increasing the D.C. EITC from 10 percent to 25 percent of the federal credit would raise the maximum refund working District families of three or four could receive from $299 to $860. This would further help lift the incomes of poor families closer to, or above the poverty line. The need to help working families in D.C. escape poverty remains high.

- Over one-third of D.C. children are poor, and the overall District poverty rate is 20 percent. Yet most poor families are working families. Nearly 60 percent of the District's poor families with children include at least one working adult. On average those adults work 37 weeks out of the year.

- A family of four with a parent who works full-time at $7.50 an hour would remain poor even when the federal EITC and 10 percent D.C. EITC are considered. A 25 percent D.C. EITC would give this family a refund of $474 and would lift its income above the poverty line.

- About 17,000 families in D.C. receive welfare assistance, and as many as 5,000 will reach time limits by the end of 2002. State EITCs help make welfare reform more successful by boosting the incomes of families that move from welfare to low-wage work. Recent academic research shows that the federal EITC has positive effects in encouraging parents to enter the labor force. Moreover, recent evaluations have found that when welfare reform policies go beyond increasing employment and also increase income through public wage supplements, they lead to better school outcomes for the children of affected families.

The Impact of the Current 10 percent D.C. EITC

The

D.C. EITC enacted in 2000 provides low- and moderate-income District households a tax

credit equal to 10 percent of the federal EITC for which they qualify. To understand the

impact of the new D.C. EITC, it is useful to understand the federal credit upon which it

is based. The federal EITC is a refundable tax credit for low- and moderate-income

workers, primarily those with children, designed to offset the burden of federal payroll

taxes and to supplement earnings of low-income working families. The EITC has become a

central element of federal efforts to boost income from work and lessen poverty among

families with children, often called the "make work pay" strategy. The federal

EITC lifts nearly five million people out of poverty, making it the most effective program

for lifting working families out of poverty, and research indicates that the EITC

encourages work among low-income parents. (See Appendix.)

The

D.C. EITC enacted in 2000 provides low- and moderate-income District households a tax

credit equal to 10 percent of the federal EITC for which they qualify. To understand the

impact of the new D.C. EITC, it is useful to understand the federal credit upon which it

is based. The federal EITC is a refundable tax credit for low- and moderate-income

workers, primarily those with children, designed to offset the burden of federal payroll

taxes and to supplement earnings of low-income working families. The EITC has become a

central element of federal efforts to boost income from work and lessen poverty among

families with children, often called the "make work pay" strategy. The federal

EITC lifts nearly five million people out of poverty, making it the most effective program

for lifting working families out of poverty, and research indicates that the EITC

encourages work among low-income parents. (See Appendix.)

D.C.

Income Tax in 2000 for a |

||

| Income | Without D.C. EITC | With Current D.C. EITC (10% of Federal) |

| $5,000 | $0 | -$200 |

| $10,000 | $0 | -$263 |

| $15,000 | $376 | $36 |

| $20,000 | $689 | $454 |

| $25,000 | $1,064 | $934 |

For families with very low earnings, the value of the EITC increases as earnings rise. (See Figure 1.) Families with two or more children receive an EITC equal to 40 cents for each dollar up to $9,720 earned in 2000, for a maximum benefit of $3,888. Families with one child receive an EITC equal to 34 cents for each dollar earned up to $6,920 of earnings, for a maximum benefit of $2,353. Both types of families continue to be eligible for the maximum credit until income reaches $12,690. For families with incomes above $12,690, the EITC phases out as earnings rise. Families with two or more children are eligible for some EITC benefit until income exceeds $31,152, while families with one child remain eligible for some EITC benefit until income exceeds $27,413. Workers without children also are eligible for the EITC, but at much lower level. The maximum credit for individuals and couples without children is $353 in 2000.

Like the federal EITC, the D.C. EITC is a refundable credit. Families compute their D.C. EITC as 10 percent of their federal EITC and then apply the credit amount to their tax liability. If the credit amount exceeds their liability, the D.C. EITC results in a refund. D.C. EITC refunds help offset the burden of other taxes paid by low-income families, such as the sales tax — which represents the largest component of the tax burden of low-income District households. D.C. EITC refunds also help lift working families closer to or above the poverty line.

- A single-parent who has two children and earns $10,000 would owe no D.C. income tax without the EITC. With the 10 percent D.C. EITC, the family receives a refund of $263.

- A similar family with $15,000 in income has its income tax burden almost entirely eliminated by the new EITC. The EITC reduces the family's income tax from $376 to $36.

- For a family earning $25,000, the new D.C. EITC provides a modest reduction in income taxes, from $1,064 to $934.

EITC Recipients Live Throughout the District

There is no information yet available on families receiving the D.C. EITC, since families are just now beginning to claim the credit as they file their 2000 tax returns. Because D.C. EITC recipients must claim the federal EITC, however, information on federal EITC recipients provides a good indication of both the number of families that are likely to claim the D.C. EITC and where they live. Table 2 present District families that received the federal EITC for Tax Year 1998 by zip code.

| Zip Code (Ward) | EITC Recipients | Percent of Total |

| 20019 (Ward 7) | 7,102 | 14% |

| 20020 (Wards 6,7,8) | 7,031 | 14% |

| 20011 (Ward 4) | 5,684 | 11% |

| 20002 (Wards 5,6) | 5,581 | 11% |

| 20032 (Ward 8) | 5,073 | 10% |

| 20009 (Wards 1,2) | 3,739 | 7% |

| 20001 (Ward 2) | 3,646 | 7% |

| 20010 (Ward 1) | 3,629 | 7% |

| 20003 (Ward 6) | 1,482 | 3% |

| 20018 (Ward 5) | 1,432 | 3% |

| 20017 (Ward 5) | 1,219 | 2% |

| 20024 (Ward 2) | 854 | 2% |

| 20012 (Ward 4) | 717 | 1% |

| 20005 (Ward 2) | 714 | 1% |

| All other | 2,289 | 5% |

| Total | 50,192 | |

| Source: IRS data. | ||

- Over 19,000 EITC recipients — 38 percent of all District recipients of the federal EITC — live east of the Anacostia River, in the 20019, 20020, and 20032 zip codes.

- Nearly 5,700 EITC recipients live in the 20011 zip code, in the lower portion of Ward 4. An additional 700 EITC recipients live in the 20012 zip code, the other major zip code for Ward 4.

- The 20002 zip code is the fifth largest in terms of EITC recipients, with 5,100 households receiving the credit. This zip code covers Ward 5 and Ward 6.

- Three zip codes in the central portion of the city — 20001, 20009, and 20010 — each include nearly 4,000 EITC recipients. These zip codes are primarily in Ward 1 and Ward 2.

The Impact of Raising the D.C. EITC to 25 Percent of the Federal Credit

The bill to increase the D.C. EITC to 25 percent of the federal credit would increase tax relief for low-income families, particularly those with children, a group that did not benefit significantly from the 1999 Tax Parity Act. As shown in Table 3, a 25 percent D.C. EITC would greatly increase the refunds some families would receive, result in new refunds for families that currently do not get one, and reduce taxes substantially for other low-income families.

Comparison of D.C. Tax Liability, 2000 |

|||

Gross Earnings |

D.C. Tax Liability With a 10% D.C. EITC (current law) |

D.C. Tax

Liability With a 25% D.C. EITC |

|

Family of four with two children |

|||

| No earnings | $0 |

$0 |

$0 |

| Half-time minimum wage | $6,396 |

($256) |

($640) |

| Full-time minimum wage | $12,792 |

($121) |

($701) |

| Wages equal federal poverty line | $17,601 |

$0 |

($204) |

| Wages equal 125% of poverty line | $22,002 |

$646 |

$357 |

Family of three with two children |

|||

| No earnings | $0 |

$0 |

$0 |

| Half-time minimum wage | $6,396 |

($256) |

($640) |

| Full-time minimum wage | $12,792 |

($121) |

($701) |

| Wages equal federal poverty line | $13,737 |

($54) |

($604) |

| Wages equal 125% of poverty line | $17,171 |

$190 |

($252) |

| Wages equal 200% of poverty line | $27,474 |

$1,172 |

$1,052 |

- For example, a single parent with two children and full-time minimum wage earnings (around $13,000) is eligible for a $121 income tax refund for tax year 2000 as a result of the 10 percent D.C. EITC. A 25 percent D.C. EITC, however, would provide the same family a $701 refund.

- A two-parent family of four with poverty-level earnings ($17,600) currently owes no D.C. income taxes. A 25 percent D.C. EITC would have provided a $204 refund for this family for tax year 2000.

- A two-parent family of four with $22,002 in income — 125 percent of the poverty line — would have had its tax year 2000 income tax burden reduced from $646 to $357 if there had been a 25 percent D.C. EITC.

Raising the D.C. EITC to 25 Percent of the Federal Credit Would Address Problems That Remain in the District's Income Tax

The D.C. EITC helps address two problems in the income tax as it affects low-income families — the high income tax burden on families with incomes modestly above the poverty line and a substantial income tax "cliff." While the 10 percent D.C. EITC significantly ameliorates these problems, it does not eliminate them. Moreover, some families received no benefit from the 10 percent D.C. EITC or from the 1999 Tax Parity Act. Raising the D.C. EITC to 25 percent of the federal credit would make much more progress in addressing these needs, as described below in more detail.

Reducing High Tax Burdens On Near-Poor Families

Prior to 2000, the income tax burden on District families with incomes slightly above the poverty line pay was among the highest in the country. The provisions of the Tax Parity Act reduced this tax burden only modestly. The D.C. EITC enacted in 2000, on the other hand, significantly addresses this problem, although it does not eliminate it.

- Without the 10 percent D.C. EITC, a two-parent family of four with income of $22,002 — 25 percent above the poverty line, would have owed $839 in income taxes in 2000, more than a similar family in any other state with an income tax except Kentucky. The D.C. EITC reduced that tax burden to $646.

- If the Tax Parity Act had been fully implemented in 2000, the income tax burden on such a family after the 10 percent D.C. EITC would have been $479. While this is substantially less than what a near-poor family would owe without the EITC and Tax Parity Act, it is higher than the tax burden on near-poor families in all but seven states.

- By contrast, a D.C. EITC set at 25 percent of the federal credit, combined with the fully-implemented provisions of the Tax Parity Act, would have resulted in an income tax liability of $190 for a family of four with income of $22,002 in 2000. At this level, near-poor families in the District would have a lower income tax burden than near-poor families in 21 of the 41 other states with an income tax.

- For a single-parent family of three with income at 125 percent of the poverty line — $17,171 — the current 10 percent D.C. EITC combined with the fully-implemented tax rates in the Tax Parity Act would have resulted in an income tax liability of $93 in 2000. This is lower than 19 of the 41 other states with an income tax. With an EITC set at 25 percent of the federal credit, however, a near-poor family of three would receive a refund of $348. Only four states would provide a larger income tax refund (all through state EITCs) to such a family.

The Income Tax "Cliff"

The District's low-income tax credit offsets 100 percent of District income taxes for individuals and families up to a certain income. This level may be described as a "no-tax floor." In tax year 2000, the no-tax floor is set at $18,554 for a family of four.(1) Thus a family with poverty-level income — $17,029 in 2000 for a family of four — owed no income tax because its income was below the "no-tax floor." Once family income rises above the "no-tax floor" however, the family is not eligible for any portion of the low-income credit, and thus must pay the full amount of the D.C. income tax.

The D.C. low-income credit targets all of its benefits to families with incomes below or very close to poverty. If a family works its way out of poverty and loses the advantage of the low-income credit, however, it can find itself faced with an income tax "cliff" where a single additional dollar of income triggers a large amount of tax. In 2000, for example, a two-parent family of four with income of $18,554 would have its $581 tax liability fully offset by the low-income credit. If such a family earned $18,555, however, it was no longer eligible for the tax credit and thus its tax liability before considering the EITC would be $581.

2000

D.C. Tax Liability For A |

||

Income |

Tax Liability Before D.C. EITC |

Tax Liability After 10% D.C. EITC |

$18,554 |

$0 |

$0 |

$18,555 |

$581 |

$316 |

The 10 percent D.C. EITC helps erode this cliff, but only partially.

- The two-parent family of four with income of $18,555 described above would receive a D.C. EITC worth $265, reducing its tax liability to $316.

- This means that even with the new 10 percent D.C. EITC, a family could see its tax liability jump from zero to $316 if its income rises just one dollar.

For some types of families, the current 10 percent D.C. EITC eliminates entirely the tax cliff. In particular, there is no income tax cliff for a single parent family with two children. For these families, the net effect of the 0 percent D.C. EITC and the lower rates of the Tax Parity Act is to create a fairly smooth and gradual increase in tax liability as income increases.

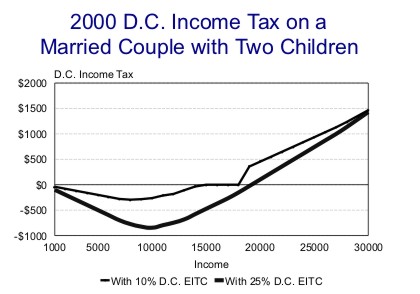

Increasing the D.C. EITC to 25 percent of the federal EITC would eliminate the cliff entirely for a two-parent family of four and would substantially reduce the cliff for larger families. (See Figure 2)

Families that Do Not Benefit from the 10 percent D.C. EITC

While the D.C. EITC

enacted in 2000 provides tax relief and refunds to thousands of low-income working

households, there are some low-income households that did not benefit from the new credit.

These are families that also received no benefit from the Tax Parity Act. Expanding the

D.C. EITC to 25 percent of the federal EITC would provide relief to the families that have

been left out.

While the D.C. EITC

enacted in 2000 provides tax relief and refunds to thousands of low-income working

households, there are some low-income households that did not benefit from the new credit.

These are families that also received no benefit from the Tax Parity Act. Expanding the

D.C. EITC to 25 percent of the federal EITC would provide relief to the families that have

been left out.

The reason some families have not benefitted from the 10 percent D.C. EITC reflects the interaction of the new credit with the prior low-income credit. Families that claim the D.C. EITC cannot claim the low-income credit. If a family's D.C. EITC amount is less than the benefit they would receive from the low-income credit, the family does not claim the EITC and instead continues using the low-income credit.

- Two-parent families of four with incomes between $15,700 and $18,555 receive less benefit from the 10 percent D.C. EITC than from the low-income credit. Because they can use only one of these tax relief provisions, they claim the low-income credit.

- Two-parent families of five with incomes between $16,600 and $21,400 also receive no benefit from the 10 percent D.C. EITC.

Because these families claim the low-income credit, they owe no income tax, but they still pay a substantial amount of income in D.C. taxes, particularly sales and excise taxes. According to Citizens for Tax Justice the lowest income D.C. households spend seven percent of their income on District taxes other than the income tax. Because the sales tax is a regressive tax, which means it consumes a larger share of the income of lower-income households than of higher income households, the overall tax burden of low-income District residents is higher than the tax burden on the highest income residents.(2)

In short, there are some low-income District households that have sizable D.C. tax burdens but got no tax relief from either the Tax Parity Act or the 10 percent D.C. EITC. Expanding the D.C. EITC to 25 percent of the federal credit would bring benefits to nearly all of the families that do not currently benefit.(3) For example, a two-parent family of four with income of $16,000 would have received a $457 refund in 2000 if the D.C. EITC were set at 25 percent of the federal credit and the Tax Parity Act were fully in effect.

A D.C. EITC Equal to 25 Percent of The Federal Credit Would Reduce Poverty and Complement Welfare Reform

Increasing the D.C. EITC would do more than address lingering problems in the District's income tax. By boosting the incomes of low-income working families, it also would help reduce D.C.'s high rate of poverty and it would complement welfare reform efforts.

Consider a family of four with one parent who works full-time earning $7.50 an hour, or $15,000 per year. After subtracting federal payroll taxes and adding a federal EITC of $3,402 the family's cash income would be $17,254, or about $350 below the poverty line for a family of four in 2000. (The family would owe no D.C. income taxes but would not get a refund from the 10 percent D.C. EITC.) Increasing the D.C. EITC to 25 percent of the federal credit would result in a D.C. income tax refund of $474, increasing the family's total income to $17,728, or slightly above the poverty line.

Raising the incomes of low-income working families in the District is particularly important for several reasons.

- Poverty in the city remains high. In the late 1990s, some 36 percent of D.C. children — and 20 percent of all D.C. residents — were poor.

- Over half (58 percent) of poor families with children include one or more working adults who are employed an average of 37 weeks of the year. In other words, poverty remains high despite a substantial work effort among low-income families.

- Roughly 17,000 D.C. families receive welfare benefits. The District's five-year time limit will be reached by some families beginning in March 2002, and as many as 5,000 are expected to reach the limit by the end of 2002. An expanded D.C. EITC could help families make the transition from welfare to work. In addition, EITCs help meet the ongoing expenses associated with working, such as transportation and child care, and may allow families to cope with unforeseen costs that otherwise might drive them onto public assistance.

Recent research has shown that poverty can have a substantial effect on child and adolescent well-being, even when all other factors associated with poverty are controlled for. Children who grow up in families with incomes below the poverty line have poorer health, higher rates of learning disabilities and developmental delays, and poorer school achievement. They are far more likely to be unemployed as adults than children who were not poor. Research also suggests that efforts to lift children out of poverty can have positive effects. For example, research released in early 2001 found that welfare programs that resulted in both greater employment and greater incomes led to improved school performance for children, while welfare programs that increased employment but not incomes had no effect on school performance. The report noted that:

Welfare reforms and antipoverty programs can have a positive impact on children's development if they increase employment and income, but increasing employment alone does not appear sufficient to foster the healthy development of children. Children living in poverty are at risk of low achievement, behavior problems, and health problems, so it is critical that policies affecting their families enhance children's well-being rather than leaving them at the same level of deprivation and risk that they experienced under the former welfare system.(4)

Cost of a D.C. EITC

The projected cost of a 25 percent refundable D.C. EITC in fiscal year 2001 is roughly $11 million. This estimate is based on two sets of data. The first set is Internal Revenue Service data on the amount of federal EITC claims filed by residents of each state. The second data source is the U.S. Department of Treasury's projections of the cost of the federal EITC in future years. Based on this data, the estimated cost of the federal EITC going to District residents in FY 2002 is $84 million.

If all D.C. residents who claim the federal credit also claim the D.C. credit, the cost of the expansion would equal 15 percent — the difference between the current 10 percent and 25 percent — of the $84 million in federal EITC benefits they will receive, or $12.6 million. Other states that have enacted EITCs, including New York, Wisconsin, and Vermont, have found that the participation rate for a state EITC in the second year after enactment was 85 to 93 percent of participation in the federal credit by state residents.(5) If it is assumed that 90 percent of federal EITC recipients would claim the D.C. EITC, the cost of the credit for tax year 2001 would be $11.3 million.

APPENDIX

Research Findings on the Effectiveness of the EITC

Several recent academic studies indicate that the EITC has positive effects in inducing more single parents to go to work, reducing welfare receipt, and moderating the growing income gaps between rich and poor Americans.

Harvard economist Jeffrey Liebman, who has conducted a series of studies on the EITC, has noted that workforce participation among single women with children has risen dramatically since the mid-1980s.(6) In 1984, some 72.7 percent of single women with children worked during the year. In 1996, some 82.1 percent did. The increase has been most pronounced among women with less than high school education. During this same period there was no increase in work effort among single women without children.

A number of researchers have found that the large expansions of the EITC since the mid-1980s have been a major factor behind the trend toward greater workforce participation. Studies by Liebman and University of California economist Nada Eissa find a sizable EITC effect in inducing more single women with children to work.(7) In addition, a recent study by Northwestern University economists Bruce Meyer and Dan Rosenbaum finds that a large share of the increase in employment of single mothers in recent years can be attributed to expansions of the EITC. They find that the EITC expansions explain more than half of the increase in employment among single mothers over the 1984-1996 period.(8)

These findings are consistent with an earlier study by Stacy Dickert, Scott Hauser, and John Karl Scholz of the University of Wisconsin, which projected that the EITC expansions in the 1993 budget law would generate a reduction in welfare receipt. Dickert, Hauser, and Scholz estimated that the 1993 EITC expansions would induce approximately 500,000 families to move from welfare to the workforce.(9)

Finally, Liebman also has found that the EITC moderates the gap between rich and poor. During the past 20 years, the share of national income received by the poorest fifth of households with children has declined, while the share of income received by the top fifth has risen sharply. Liebman found that the EITC offsets between one-fourth and one-third of the decline that occurred during this period in the share of income the poorest fifth of households with children receive.

Notes

1. The D.C. no-tax floor is set at the level below which a family would owe no federal tax, not including the federal EITC.

2. Citizens for Tax Justice and the Institute on Taxation and Economic Policy, Who Pays? A Distributional Analysis of the Tax Systems in All 50 States, June 1996.

3. There are some rare exceptions. For example, two-parent families with three children and incomes between $21,100 and $21,400 would not see any change in income tax liability if the D.C. EITC were expanded to 25 percent of the federal EITC.

4. Manpower Demonstration Research Project, How Welfare and Work Policies Affect Children: A Synthesis of Research (Executive Summary), January 2001<http://www.mdrc.org/Reports2001/NGChildSynth/ng-childsynEX.htm>

5. If the D.C. EITC is expanded to 25 percent of the federal EITC for tax year 2001, this would represent the second year of a D.C. EITC, since the 10 percent D.C. EITC went into effect in tax year 2000. For more general information on state EITC cost estimates, see Nicholas Johnson, A Hand Up: How State Earned Income Tax Credits Help Working Families Escape Poverty, 2000 Edition, Center on Budget and Policy Priorities, November, 2000. <https://www.cbpp.org/11-2-00sfp.htm>

6. Jeffrey B. Liebman, "The Impact of the Earned Income Tax Credit on Incentives and Income Distribution," in James M. Poterba, ed., Tax Policy and the Economy, Vol. 12, MIT Press, 1998.

7. See for example, Nada Eissa and Jeffrey B. Liebman, "Labor Supply Response to the Earned Income Tax Credit," Quarterly Journal of Economics, May 1996, 112(2), pp. 605-637.

8. Bruce D. Meyer and Dan T. Rosenbaum, "Welfare, The Earned Income Tax Credit, and the Labor Supply of Single Mothers," March 7, 1998.

9. Stacy Dickert, Scott Hauser, and John Karl Scholz, "The Earned Income Tax Credit and Transfer Programs: A Study of Labor Market and Program Participation," in James M. Poterba, ed., Tax Policy and the Economy, Vol. 9., MIT Press, 1995.