|

January 29, 2006

NEW CBO DATA INDICATE GROWTH IN LONG-TERM

INCOME INEQUALITY CONTINUES

by Isaac Shapiro and Joel Friedman

The Congressional Budget Office recently released extensive data on household incomes and tax liabilities for 2003.[1] CBO issues the most comprehensive data available on changes in incomes and taxes for different income groups, capturing trends at the very top of the income scale that are not shown, for example, in Census data.

The new CBO report highlights the degree to which income gains have become increasingly concentrated at the top of the income scale over the past two and a half decades. Over this period, income gains among high-income households have dwarfed those of middle- and low-income households.

The new CBO data also show that the income gap widened significantly between 2002 and 2003. The income gap had narrowed somewhat in 2001 and 2002, due in part to the sharp decline in the stock market after its peak in 2000. The data for 2003, however, show a return to the long-term trend of increasing income inequality. Further, other available evidence from the Census Bureau and from surveys of executive pay indicate that income inequality has continued to grow in the years since 2003.

Income Inequality at Historically High Levels

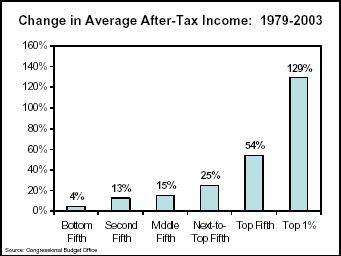

The CBO data show that between 1979 (the first year the CBO report covers) and 2003:

- The average after-tax income of the top one percent of the population more than doubled, rising from $305,800 to $701,500, for a total increase of $395,700, or 129 percent. (CBO adjusted these figures for inflation and expressed them in 2003 dollars.)

- By contrast, the average after-tax income of the middle fifth of the population rose a relatively modest 15 percent, or $5,900, reaching $44,800 in 2003.

- The average after-tax income of the poorest fifth of the population rose just 4 percent, or $600, over the past 24 years.

- Because incomes grew fastest among the most affluent, this group’s share of the total national income grew as well.

- In contrast, the shares of national income received by various groups of low- and middle-income people all fell. The middle fifth of the population received 16.5 percent of the national after-tax income in 1979, but only 15.5 percent in 2003. The bottom fifth received 6.8 percent of such income in 1979, but just 5.0 percent in 2003.

Income is now more concentrated at the very top of the income spectrum than in all but five years since the mid-1930s. This conclusion is reached by examining the CBO data in conjunction with data from a ground-breaking historical analysis of income distribution trends published in a leading economics journal in 2003.[2] When viewed together, the studies indicate that the richest one percent of households now receive a larger share of the national income than at any time since 1937, except for the period from 1997 to 2001.[3]

|

Average After-Tax Income by Income Group

(in 2003 dollars) |

|

Income Category |

1979 |

2003 |

Percent Change

1979-2003 |

Dollar Change

1979-2003 |

| Lowest fifth |

$13,500 |

$14,100 |

4.4% |

$600 |

| Second fifth |

$27,300 |

$30,800 |

12.8% |

$3,500 |

| Middle fifth |

$38,900 |

$44,800 |

15.2% |

$5,900 |

| Fourth fifth |

$50,900 |

$63,600 |

25.0% |

$12,700 |

| Top fifth |

$89,700 |

$138,500 |

54.4% |

$48,800 |

| Top 1 Percent |

$305,800 |

$701,500 |

129.4% |

$395,700 |

| Source: Congressional Budget Office, Effective Federal Tax Rates: 1979-2003, December 2005 |

New Data Highlight Continuation of Long-Term Trends in Income Inequality

The CBO data show that long-term trends in income inequality returned in 2003. Income concentration grew steadily during the latter half of the 1990s, and then peaked in 2000, the year the stock market hit a record high. From 2000 to 2002, income became less concentrated at the very top, partially due to the drop in the stock market. The after-tax incomes of most groups fell from 2000 to 2002, but fell more sharply for the top one percent. In 2003, however, those with the highest incomes experienced far more rapid growth in after-tax income than other income groups. For instance, between 2002 and 2003, the average after-tax income for the 20 percent of the population with the lowest incomes fell by $200 or 1.4 percent in inflation-adjusted terms, and those with slightly higher incomes experienced modest increases of less than one percent. In contrast, households in the top one percent of the income spectrum saw their after-tax incomes jump by 8.2 percent, or $53,300.

|

Change in Average After-Tax Income, 2002 to 2003

(in 2003 dollars) |

Income

Category |

Dollar

Change |

Percent

Change |

| Lowest fifth |

-200 |

-1.4% |

| Second fifth |

100 |

0.3% |

| Middle fifth |

300 |

0.7% |

| Fourth fifth |

1,000 |

1.6% |

| Top fifth |

5,200 |

3.9% |

| Top 1 percent |

53,300 |

8.2% |

| Source: Congressional Budget Office, Effective Federal Tax Rates: 1979-2003, December 2005. |

The CBO data also indicate that the growth in income disparities since 1979 largely reflect changes in before-tax income. That is, most of the divergence in income patterns among various income groups reflects diverging outcomes in the income they received before taking changes in federal tax policies into account.

Changes in federal taxes, however, have had some influence over these patterns. The direction of that influence depends upon the time period examined. Changes in federal taxes exacerbated the growth in income disparities during the 1980s, but mitigated the growth in income disparities during the 1990s. The new CBO data for 2003 show that the significant tax cuts taking effect in that year benefited those at the top of the income spectrum the most, and thus exacerbated the underlying growth in before-tax income inequality in 2003.

Income Gap Likely To Grow After 2003

Available evidence indicates that since 2003, income gains at the top may have continued to outpace the gains across the rest of the income spectrum. Consider:

- Census data show that the top five percent of households experienced income gains from 2003 to 2004 while other households did not. Most other households, in fact, saw their incomes decline from 2003 to 2004.[4] These Census data, moreover, are likely to understate divergence in incomes in 2004. The Census data do not break out trends among the top one percent of households, where income gains may have been especially concentrated. In addition, the Census data do not include significant amounts of income received by high-income households; for instance, the Census data ignored earnings above $1 million. If an individual makes $10 million a year, the Census records those earnings as $1 million. (This is done for confidentiality reasons.)

- During the current economic recovery, wages and salaries have grown less than half as fast as their average rate of growth during other post-World War II recoveries. Meanwhile, corporate profits have grown much faster than in other recoveries.[5] The ultimate beneficiaries of these large gains in corporate profits are primarily high-income households, since they own the lion’s share of the stocks of corporations.

- After adjusting for inflation, wages among low- and middle-income workers have fallen since 2003.

- In contrast, separate surveys of pay trends by Business Week and Forbes magazines both found extremely large increases in the compensation of chief executive officers (CEOs) in 2004. The Business Week article observed that from 2003 to 2004, “CEO raises and total pay once again dwarfed those of the average worker.”[6] The Forbes report found that the CEOs of the nation’s 500 largest companies received an “aggregate 54 percent pay raise last year…. That easily outpaced 2003’s eight percent raise.”[7] (The income gains among highly-paid CEOs are not captured by the Census data.)

- The rise in federal tax revenues in 2005 also appears to stem in part from a continued growth in income inequality. In May 2005, CBO said that one possible reason that revenues were coming in faster in 2005 than it had forecast earlier this year was that increases in income may have been more concentrated among high-income taxpayers than it had anticipated.[8] High-income taxpayers pay taxes at higher rates, so an increasing concentration of income results in a higher level of revenue. In an August report, CBO stressed that much of the recent growth of revenues has occurred because of a boom in corporate tax receipts rather than in taxes on wages and salaries.[9] This development also is consistent with the notion of increased income inequality.

- An even more recent report by CBO estimates that capital gains realizations jumped by 48 percent from 2003 to 2004, which is larger than the substantial 20 percent increase that occurred from 2002 to 2003.[10] CBO also estimates that capital gains income will rise by another 13 percent from 2004 to 2005. Increases in capital gains income lead to more income inequality as capital gains income is heavily concentrated among high-income households.

|

New Study Shows Economic Mobility Decreased

as Income Inequality Increased |

|

Some have argued that increases in income inequality are unimportant because of economic mobility. In particular, they argue that, while the incomes of the lowest-income 20 percent of the population have stagnated or grown very slowly since the late 1970s, few families remain in the bottom 20 percent of the income distribution over time.

A new study by two economists at the Federal Reserve Bank of Chicago, however, shows that over the same period of time in which income inequality increased, economic mobility decreased. Reviewing Census data from 1940-2000, the authors find, “economic mobility fell sharply during the 1980s and failed to revert, perhaps even continued to decline, in the 1990s.” *

Thus, far from compensating for the increase in income inequality since 1979, changes in economic mobility over the same time period may have heightened its effects.

* Daniel Aaronson and Bhashkar Mazumder, “Intergenerational Economic Mobility in the U.S., 1940 to 2000,” Federal Reserve Bank of Chicago, Working Paper 2005-12, November, 2005, http://www.chicagofed.org/publications/workingpapers/wp2005_12.pdf. |

In testimony before Congress, former Federal Reserve Board Chairman Alan Greenspan also reiterated his conclusion that income is becoming more concentrated. In response to a question, he said there is a “really serious problem here, as I’ve mentioned many times before this [House] committee, in the consequent concentration of income that is rising.”[11]

Federal Policies Are Exacerbating Income Disparities

The major pieces of tax legislation that have been enacted since 2001 have served to concentrate income further at the top of the income spectrum. These tax cuts have helped high-income households far more than other households. This can be seen by examining information on the combined effect of the tax-cut bills adopted in 2001, 2002, and 2003. The Urban Institute-Brookings Institution Tax Policy Center estimates that:

- In 2005, the bottom fifth of households received an average combined tax cut of $18 from these bills, raising their after-tax income by 0.3 percent.

- The middle fifth of households received an average tax reduction of $742, increasing their after-tax income by 2.6 percent.

- The top one percent of households, however, received an average tax reduction in 2005 of $34,900, leading to a jump in their after-tax income of 4.6 percent.

- Finally, households with incomes exceeding $1 million received an average tax cut of $103,000 — an increase of 5.4 percent in their after-tax income, or more than double the percentage increase received by the middle fifth.

Furthermore, some of the tax cuts that were enacted in 2001 are still being phased in. These tax cuts are heavily tilted to those at the top of the income scale. These tax cuts include the elimination of the tax on the nation’s largest estates, as well as two tax cuts that started to take effect on January 1, 2006 and will go almost entirely to high-income households. The Tax Policy Center reports that 97 percent of the tax cuts from these two measures will go to people with incomes above $200,000.[12] As a result, the tax cuts ultimately will be even more skewed toward high-income households than they were in 2005.

To date, the President and Congress have taken little heed of the trend toward increasing income concentration and have not shown concern about the degree to which the tax cuts are exacerbating income disparities. To the contrary, Congress (with the President’s support) is on track to pass “reconciliation” legislation that would cut programs assisting low- and middle-income households at the same time that it extends tax cuts — such as the reduction in taxes on capital gains and dividend income — that are of primary benefit to high-income households. Such legislation would continue the pattern of recent years, under which actions by federal policymakers have contributed to a further widening of income disparities between the most affluent households and other Americans.

End Notes:

[1] Congressional Budget Office, Historical Effective Federal Tax Rates: 1979 to 2003, December 2005.

[2] Thomas Pickety and Emmanuel Saez, “Income Inequality in the United States, 1913-1998,” Quarterly Journal of Economics, 118, 2003. Their tables have been updated through 2002 at http://emlab.berkeley.edu/users/saez/

[3] Data for 1986 are ignored in this comparison. Incomes at the top were distorted that year because high-income taxpayers made temporary adjustments to their incomes in response to the passage of the 1986 Tax Reform Bill.

[4] Between 2003 and 2004, the average income of the top five percent of households rose by an average of $4,340, or 1.7 percent, after adjusting for inflation. By contrast, for example, the average income of the middle fifth of households fell by $300, or 0.7 percent.

[5] Isaac Shapiro, Richard Kogan, Aviva Aron-Dine, “How Does This Recovery Measure Up,” Center on Budget and Policy Priorities, revised January 6, 2006.

[6] Louis Lavelle, “A Payday For Performance,” Business Week online, April 18, 2005.

[7] Scott DeCarlo, “CEO Compensation,” Forbes, April 21, 2005.

[8] Congressional Budget Office, Monthly Budget Review, May 5, 2005.

[9] Congressional Budget Office, The Budget and Economic Outlook: An Update, August 2005.

[10] Congressional Budget Office, The Budget and Economic Outlook: Fiscal Years 2007 to 2016, January 2006, pages 87 and 92.

[11] Federal Reserve Board Chairman Alan Greenspan, Testimony before the House Financial Services Committee, July 20, 2005.

[12] Robert Greenstein, Joel Friedman, and Isaac Shapiro, “Two Tax Cuts Primarily Benefiting Millionaires Will Start Taking Effect January 1,” Center on Budget and Policy Priorities, December 28, 2005. |