| NEWS RELEASE __________ |

|

|||

| 820 First Street, NE Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 [email protected] www.cbpp.org Robert

Greenstein Iris J. Lav Board of Directors John R. Kramer, Chair Henry J. Aaron Ken Apfel Barbara B. Blum David de Ferranti Marian Wright Edelman James O. Gibson Beatrix Hamburg, M.D. Frank Mankiewicz Richard P. Nathan Marion Pines Sol Price Robert D. Reischauer Audrey Rowe Susan Sechler Juan Sepulveda, Jr. William Julius Wilson |

STATE TAX SYSTEMS ARE BECOMING INCREASINGLY INEQUITABLE

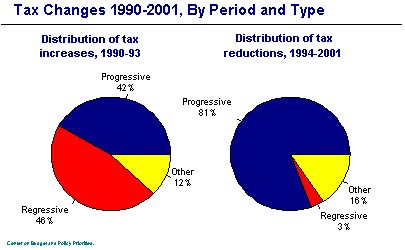

Many state tax systems have become more regressive over the past decade, according to a new study by the Center on Budget and Policy Priorities. State tax hikes during the recession of the early 1990s hit lower-income families hard, but state tax relief during the prosperous period from 1994 to early 2001 was targeted primarily on upper-income families. "Now that we’re once again in a recession and states are facing budget problems, there’s a real danger the cycle will begin to repeat itself," said Nick Johnson, lead author of the report, entitled The Rising Regressivity of State Taxes. "State policymakers need to understand that there are ways they can raise revenue without forcing poor families to bear most of the burden." The report provides examples of ways in which states have made their tax systems less progressive in recent years. It also describes how a few states have made modest efforts to moderate the trend toward rising regressivity. Income Taxes Down, but Not Sales and Excise Taxes The tax systems of most states already are significantly regressive — that is, they take a larger proportion of the income of lower-income families than the income of more affluent families. This is largely because states derive about half of their revenues from general sales taxes and excise taxes on items such as gasoline and tobacco products. These consumption taxes impose a disproportionate burden on lower-income families, who must consume (rather than save or invest) a larger share of their income than higher-income families. Since the early 1990s, every state has changed its tax code in some fashion, typically by raising taxes in response to tight fiscal conditions in the early 1990s and then cutting taxes in the middle and late 1990s and into 2000 and early 2001. The new report finds that those changes have generally failed to reduce the burden of regressive taxes, and in some states have increased that burden. For instance, during the economic expansion from 1994-2001, states did very little to reduce these regressive taxes. Out of approximately $35 billion in state tax cuts, only about 3 percent were net reductions in sales and excise taxes. Instead, states focused tax relief on higher-income families. Some 81 percent of states’ tax cuts during this period were reductions in progressive taxes such as personal income taxes, corporate income taxes, and estate taxes, which are more burdensome to higher-income families. The different treatment of progressive and regressive taxes during the tax-cutting period of 1994 to 2001 stands in sharp contrast to the tax increases of the early 1990s, the report finds. In the early 1990s, states generally increased regressive taxes more than they raised progressive taxes.

"In the recession of the early 1990s, the added burdens of new taxes were shared across the income spectrum. But in the economic expansion, the benefits of tax cuts accrued largely to higher-income taxpayers, at the expense of those with lower incomes," said Daniel Tenny, co-author of the report. The report identifies several states that contributed to this trend toward greater tax regressivity. Examples include Arkansas and Iowa, both of which raised revenue in the early 1990s primarily with sales and excise tax increases but more recently have cut progressive taxes like the income tax; Massachusetts, which raised both progressive and regressive taxes in the early 1990s but later just cut progressive income and estate taxes; and Tennessee, where the only significant tax change during the study period was a large sales tax increase in the early 1990s. In those states and others, the tax burdens on low-income families likely have risen while those on higher-income families likely have declined, according to the report. The report also identifies some specific actions that states have taken to moderate the trend toward regressivity, such as repeal of the sales tax on food in Georgia and Missouri and enactment and/or expansion of low-income tax credits and sales tax rebates in states like Kansas and Oklahoma. State Tax Regressivity Need Not Worsen During Current Recession Early indications in the current recession are that low- and moderate-income families again may be expected to take on an increased tax burden as states balance their budgets. Given the trend toward greater regressivity in state tax systems, states need to consider other ways to raise revenue, the report concluded. "If policymakers recognize that the benefits of the tax cuts in the last eight years have largely flowed to higher-income families, they may look first to these better-off families to help balance state budgets," said Johnson. Furthermore, noted Center Deputy Director Iris Lav, "Increasing the tax burdens of low-income families undermines the efforts states have been making to help low-income families become less dependent on state assistance such as welfare." Instead of increasing sales and excise taxes, states can raise revenue from sources such as the personal income tax, corporate taxes, and inheritance and estate taxes. They also can freeze or reverse previously enacted cuts in those taxes. Few States Assess Impact of Tax Changes on In a companion study, the Center found that only a handful of states systematically assess the impact of tax changes on families at different income levels. Such assessments of tax legislation, known as "tax incidence analyses," are often performed at the federal level. But only three states (Maine, Minnesota, and Texas) now require such analyses of major state tax legislation by either the legislative or executive branch. Many states, however, already possess some or all of the essential building blocks necessary to construct a computer model that could provide this information. "Understanding who wins and who loses when taxes are increased or reduced is essential to holding policymakers accountable for their decisions," said Michael Mazerov, author of the companion report, entitled Developing the Capacity to Analyze the Distributional Impact of State and Local Taxes: Issues and Options for States. The Center on Budget and Policy Priorities is a nonpartisan research organization and policy institute that conducts research and analysis on a range of government policies and programs, with an emphasis on those affecting low- and middle-income people. It is supported primarily by foundation grants. State Group Contact List

|