Commentary: Even As Insurance Market Improves, GOP’s ACA Repeal Would Kill It

One of the most harmful effects of repealing the Affordable Care Act (ACA) is that it would begin immediately to unravel states’ individual health insurance markets. Congressional Republicans bent on repeal have tried to dismiss this danger, in part by disingenuously claiming that these markets are already near collapse, or even in a “death spiral.”[1] They’d rather blame the law, not their own actions, for the damage they’re about to cause.

The evidence shows that the individual market is becoming more stable, not less. In contrast, repeal would set up the perfect conditions for a death spiral.The evidence shows that the individual market is becoming more stable, not less. In contrast, repeal would set up the perfect conditions for a death spiral.

The main symptom of a death spiral is rapidly falling enrollment. A death spiral occurs when healthier people leave the pool with health coverage, pushing up premiums for remaining enrollees, who cost more to cover. The higher premiums then cause more people to leave the pool, raising premiums still higher. This cycle can continue until few people are left and the market is near collapse.

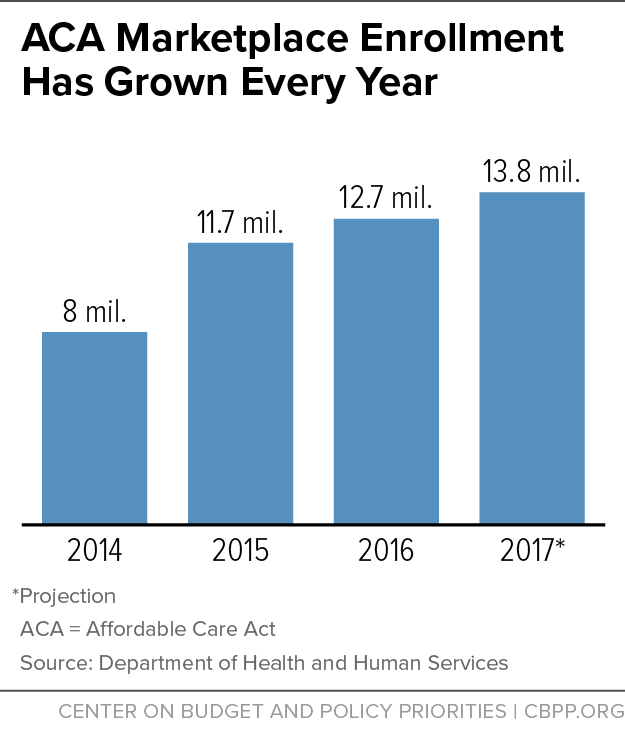

But enrollment in the individual market (which includes plans inside and outside the ACA marketplaces) has grown each year since the ACA’s major coverage expansions and reforms took full effect in 2014, from about 11 million people in 2013 to about 18 million as of early 2016. For the 2017 plan year, where open enrollment continues through January, marketplace enrollment is tracking higher than last year.[2] While that’s not a complete picture of the whole market, it’s an encouraging sign. (See Figure 1.)

Dramatic premium increases could also signal a death spiral, but only if they cause people — specifically, healthier people — not to enroll. That doesn’t appear to be happening in the marketplaces. States with larger premium increases in 2015 had similar enrollment growth as states with smaller increases, a new report by the White House Council of Economic Advisers (CEA) finds.[3] Nor is there evidence that premium increases caused healthier people to leave the individual market during this period. The report found that states with larger premium increases had slower growth in the insurer-reported costs of covering ACA plan enrollees, which suggests that the pool of people with coverage in these states is getting healthier, not sicker.

Initial data on 2016 and 2017 market conditions also show no sign of a death spiral. The CEA examined whether county-level premium changes affected marketplace enrollment and found no sign of an unraveling market from 2015 to 2016. In 2017, average premiums for marketplace plans rose by an estimated 22 percent nationwide, which is significant. But there was “essentially no relationship” between the change in the premium for “benchmark” plans in a state and the change in how many people selected plans from 2016 to 2017, the CEA found.

Even in states with some of the largest premium increases, enrollment appears to be on track. For example, Arizona had by far the highest benchmark premium increase in 2017 but has seen plan selections rise by about 8 percent as of late December, compared to the same point last year. Oklahoma, too, had significant premium increases but plan selections are up about 9 percent so far.

ACA premium credits protect against a death spiral in the marketplaces by capping the premiums modest-income people pay at a set percentage of their income, insulating them from premium increases. The credit grows with the cost of the benchmark plan, which not only helps people afford coverage but also holds premiums down for healthier people who may not use much medical care, making it more likely they will enroll.

Premium increases are concerning, particularly because they make coverage less affordable for people who don’t get subsidies, which can affect the risk pool over time. But there’s growing evidence that premium increases in 2017 were a “one-time pricing correction,” as a report from Standard & Poor’s Global Ratings recently put it[4] — not the sign of a doomed market. Many insurers in the individual market simply priced too low in the initial years after the ACA took effect. Some did so inadvertently, because they couldn’t be sure who would sign up for their plans and how much they would cost to cover. Other insurers set prices low deliberately, to attract new customers. Since then, many insurers have needed to raise premiums significantly to cover their costs and also to address the phase-out of the ACA’s temporary reinsurance program.[5] Standard & Poor’s predicts the individual insurance market will be closer to break-even results overall this year, with more insurers making a profit.

So, the individual market under the ACA is moving in the right direction and showing growing signs of long-term sustainability. The problem, of course, is that congressional Republicans intend to repeal much of the law — including the marketplace subsidies and individual mandate, which are critical to the stability of the individual market.

As the Urban Institute noted, repeal would begin to immediately unravel the individual market.[6] Eliminating the individual mandate would cause 4.3 million people to drop their coverage in 2017, and many of them would be healthier. That would cause significant financial losses for insurers which would lead them to either pull out of the market for the following year or raise premiums significantly. By 2019, when the subsidies would disappear under the two-year delay the analysis assumed, Urban projects the market would virtually collapse, with enrollment falling to a mere 1.6 million enrollees, a reduction of 92 percent.

A new report from the Congressional Budget Office (CBO) paints a similarly dire picture, estimating that in the first full year after repeal’s enactment, enrollment in the individual market would drop by 10 million people, premiums would jump 20 to 25 percent, and roughly 10 percent of the population would live in an area with no individual-market insurers. The situation would worsen over time, CBO estimates, with enrollment falling and premiums climbing. By 2026, premiums would double, 75 percent of the population would live in an area with no individual-market insurers, and fewer than 2 million enrollees would be left in the individual market.[7]

Now that’s a death spiral.

End Notes

[1] “Ryan: Obamacare is in ‘death spiral,’” Washington Post, January 5, 2017, https://www.washingtonpost.com/video/national/ryan-obamacare-is-in-death-spiral/2017/01/05/375a49da-d366-11e6-9651-54a0154cf5b3_video.html.

[2] Virgil Dickson, “ACA signups continue to outpace last year, hitting 11.5 million,” Modern Healthcare, January 10, 2017, http://www.modernhealthcare.com/article/20170110/NEWS/170119983.

[3] “Understanding Recent Developments in the Individual Health Insurance Market,” Council of Economic Advisers Issue Brief, January 2017, https://www.whitehouse.gov/sites/default/files/page/files/201701_individual_health_insurance_market_cea_issue_brief.pdf.

[4] Deep Banerjee, “The ACA Individual Market: 2016 Will Be Better Than 2015, But Achieving Target Profitability Will Take Longer,” S&P Global Ratings, December 22, 2016, https://morningconsult.com/wp-content/uploads/2016/12/12-22-16-The-ACA-Individual-Market-2016-Will-Be-Better-Than-2015-But-Achieving-Target-Profitability-Will-Take-Longer.pdf.

[5] Cynthia Cox, et al., “Explaining Health Care Reform: Risk Adjustment, Reinsurance, and Risk Corridors,” The Henry J. Kaiser Family Foundation, August 17, 2016, http://kff.org/health-reform/issue-brief/explaining-health-care-reform-risk-adjustment-reinsurance-and-risk-corridors/.

[6] Linda J. Blumberg, Matthew Buettgens, and John Holahan, “Implications of Partial Repeal of the ACA through Reconciliation,” Urban Institute, December 2016, http://www.urban.org/sites/default/files/publication/86236/2001013-the-implications-of-partial-repeal-of-the-aca-through-reconciliation_0.pdf.

[7] “How Repealing Portions of the Affordable Care Act would Affect Health Insurance Coverage and Premiums,” Congressional Budget Office, January 2017,

More from the Authors