This report was commissioned by the Center on Budget and Policy Priorities’ Full Employment Project. Views expressed within the report do not necessarily reflect the views of the Center.

Introduction

The Federal Reserve, the monetary authority of the United States, is mandated by Congress to pursue price stability and maximum employment through its monetary policy. The structure of the Fed was designed to ensure that it has political independence and a high degree of discretion in its pursuit of these goals. The Fed is free to interpret the goals and prioritize them as it sees fit, and it is not required to conduct monetary policy according to any explicit rule. Discretion gives policymakers the flexibility to react to unusual circumstances and allows them to take the complexities of the economy into account in their decision making.

The Fed has not always had the discretion it exercises today. The international gold standard constricted monetary policy during the Fed’s early years. Though that rule was abandoned in the Great Depression, proposals to limit the discretion of monetary policymakers through rules or targets abound.

A rule, or operational mandate, provides a specific formula or prescription for how monetary policy will respond to economic conditions; the best-known is the Taylor rule. A target is a single, explicitly defined goal for monetary policy; an example is inflation targeting, which has been adopted by many countries since the 1990s. Monetary policymakers can decide how to use policy to achieve the target, but they cannot reinterpret the target or prioritize other goals above it.

When monetary policymakers exercise discretion, their decisions reflect their preferences. This is sometimes cited as a downside of discretion, but it must be recognized that any type of rule or target also embeds a set of preferences and priorities and may thus serve some groups better than others.[3]

This report provides an overview of the discretionary policy pursued by the Fed and of several rules and targets that have been suggested as alternatives. We evaluate each alternative with a particular focus on its ability to promote full employment — namely, the strong and sustained labor market conditions that boost living standards and career trajectories across the income distribution and contribute to broad prosperity. A summary of historical and proposed rules and targets appears in Table 1. We suggest that neither the discretionary policy as currently implemented by the Fed, nor the Taylor rule, nor inflation targeting is likely optimal for securing full employment. Alternatives including price-level targeting, nominal income targeting, and nominal wage targeting, though untried, hold potential, and nominal income and wage targeting especially merit further research.

| TABLE 1 | ||||

|---|---|---|---|---|

| Summary of Monetary Policy Rules and Targets and Their Full Employment Impacts | ||||

| Rule/Target | Targeted Variables | Discretion | Empirical Use | Potential Effectiveness for Full Employment |

| Gold standard | Convertibility of currency to gold | Low | Most of world before WWII | Low |

| Dual mandate with discretion | Inflation and employment | High | In use in U.S. | Medium |

| Taylor rule | Interest rate as function of inflation and output gap | Low | Not tried* | Low |

| Inflation targeting | Inflation | Medium | In use in 26 countries | Low |

| Price-level targeting | Price-level trajectory | Medium | Not tried** | Medium |

| Nominal income (NGDP) targeting | NGDP (growth rate or trajectory) | Medium | Not tried | High |

| Nominal wage targeting | Wage rate or quantity of wages paid | Medium | Not tried | High |

I. A Brief History of Rules

When the Federal Reserve Act of 1913 established the Federal Reserve System, the United States and many other countries were on the gold standard. Central banks in gold standard economies follow a classic version of rule-based monetary policy: they maintain the convertibility of their country’s currency to gold at a fixed rate. This commitment to convertibility precludes a central bank from freely using monetary policy to pursue other objectives, including domestic macroeconomic stability and full employment.[4]

The limits of this rule-based regime became most apparent in the Great Depression, when the gold standard helped propagate the crisis around the world.[5] More than a dozen countries abandoned the gold standard in 1931,[6] though the United States did not follow suit until 1933, when the unemployment rate was 25 percent. The collapse of the international gold standard opened new possibilities for the goals and conduct of monetary policy. After World War II, the Full Employment Act of 1946 formalized full employment as a responsibility of the federal government, including the Federal Reserve,[7] and approximately two decades of relatively stable growth and low inflation followed.[8] During this time, the Fed did not follow an explicit rule for monetary policy, but instead used discretion to pursue macroeconomic and price stability.

The question of whether to continue with discretionary monetary policy or to return to a rule-based system was, and remains, one of the most debated issues in monetary policy.[9] This debate is closely linked to the dilemma of central bank independence. To achieve long-term success, central bankers require some degree of removal from direct political interference.[10] But a politically independent central bank must still be held accountable to elected officials and the public for the policies it pursues. Typically, the balance between independence and accountability is determined by a government’s mandate for the central bank, which falls into one of two broad categories. The more restrictive approach is an operational mandate or instrument rule, which stipulates an explicit intermediate goal for the bank. The gold standard falls into this category. Famously, Milton Friedman (1960) advocated for an operational mandate for the Fed in the form of a “k-percent rule” for monetary policy, under which the Federal Reserve would increase the stock of money “at a fixed rate year-in and year-out without any variation in the rate of increase to meet cyclical needs.”[11] Though the rule was not implemented, proponents valued its simplicity and argued that it would promote price stability.

A less restrictive approach than an operational mandate is a goal mandate, which stipulates the economic goals for the bank but lets the bank determine how to pursue these goals.[12] The Fed’s dual mandate of maximum employment and price stability is an example of a flexible goal mandate because it gives the Fed independence in interpreting and prioritizing these two goals. An example of a less-flexible goal mandate is inflation targeting. The “Great Inflation” of the 1970s convinced many governments to officially prioritize low inflation as the primary goal of monetary policy. Beginning with New Zealand in 1990, a large number of countries have adopted inflation targeting, which bears some resemblance to the gold standard in that it specifies a single, explicit target for the central bank.

The United States, though influenced by aspects of inflation targeting, continues to maintain discretion in interpreting and pursuing its dual mandate. However, numerous changes to the Fed’s mandate have been proposed for macroeconomic and political reasons, reflecting desires from both sides of the political spectrum to alter the Fed’s priorities and limit or redirect its power.[13] Alternatives include the introduction of an operational mandate or changes to the goal mandate that provide a single explicit target for monetary policy, thereby removing some of the Fed’s discretion to weigh its own priorities. The next section provides an overview of the Fed’s current practice, and subsequent sections consider several rules and targets that have been suggested as alternatives.

II. The Dual Mandate and Discretionary Policy

Congress amended the Federal Reserve Act in 1977 to state that the Federal Reserve Board of Governors and the Federal Open Market Committee (FOMC) should “promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates.” Maximum employment and stable prices are referred to as the dual mandate,[14] and the Fed independently decides how to interpret and achieve these goals.

a) Interpreting the Dual Mandate

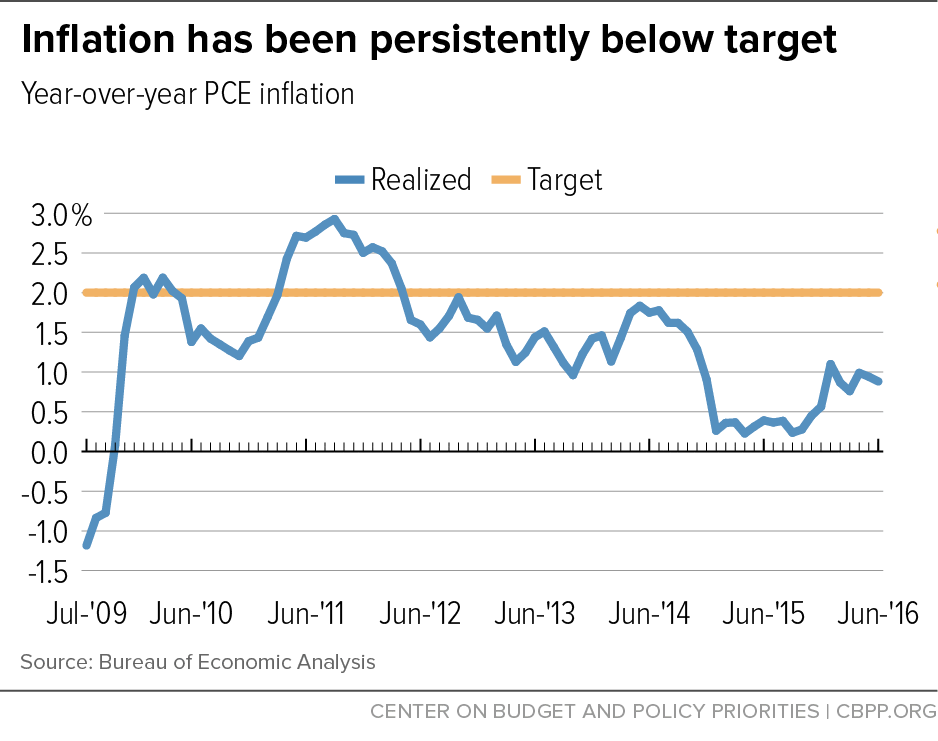

In January 2012, the FOMC announced that 2 percent inflation, as measured by the annual rate of change of the personal consumption expenditures (PCE) price index,[15] is the rate most consistent with its price stability mandate.[16] This announcement was intended to help “anchor” inflation expectations[17] around the inflation target. In October 2014, the FOMC clarified that the “Committee would be concerned if inflation were running persistently above or below” its 2 percent objective.[18] Nonetheless, inflation has been below target since the 2012 announcement. (See Figure 1.) This trend may reflect the difficulty of achieving the target given weak demand, falling commodity prices, and a lower neutral real interest rate. Consistent undershooting of the target may also reflect policymakers’ aversion to the possibility of above-target inflation. For example, the FOMC raised interest rates preemptively in December 2015 despite below-target inflation and below-full employment. Subsequently, the FOMC members have put off further rate hikes as inflation and inflation expectations have remained low, but they have continued, as former Treasury Secretary Larry Summers put it, “holding out the prospect of future rate increases and then find[ing] themselves unable to deliver.”[19]

Of course, moderate and stable inflation prevents the problems associated with both deflation and very high inflation.[20] But in recent years, inflation stabilization has received high — perhaps too high — priority. Empirical studies find that only very high values of inflation are harmful to economic growth and to the well-being of the poor.[21] Somewhat higher inflation could even help lower-income households by reducing the real value of their debts.[22] Social Security and some other benefits are indexed to inflation, which protects recipients from the loss of purchasing power.[23] Meanwhile, the benefits of ultra-low inflation accrue mostly to creditors, including banks and other financial institutions.

As for the employment part of the dual mandate, the FOMC does not have an explicit definition of “maximum employment.” According to the website of the Board of Governors, [24] “[t]he maximum level of employment is largely determined by nonmonetary factors that affect the structure and dynamics of the job market. These factors may change over time and may not be directly measurable. As a result, the FOMC does not specify a fixed goal for maximum employment…. In the FOMC’s June 2016 Summary of Economic Projections, Committee participants’ estimates of the longer-run normal rate of unemployment ranged from 4.6 to 5.0 percent and had a median value of 4.8 percent.”[25]

The Fed decides not only how to interpret maximum employment and stable prices, but also the relative emphasis to place on each in cases of tradeoffs. Allowing inflation to fluctuate somewhat more in order to achieve more stable output and employment could be a wise tradeoff. Only with maintained full employment can workers across the income distribution, especially at the middle and lower ends, gain the bargaining power needed to raise their real wages.[26] Historically, inequality has rarely declined with high unemployment.[27] Periods of below-full employment can do lasting damage if long-term unemployed workers lose skills or leave the labor market altogether.[28] As Baker and Bernstein argue, “not taking action against slack job markets does permanent damage to the rate of economic growth, the rate of job growth, federal and state budgets, career trajectories, and living standards, particularly of the least advantaged.”[29]

b) Discretion in Practice

The Fed’s primary policy tool in normal times is the federal funds rate, the rate at which banks lend to and borrow from each other overnight. In deciding how to adjust this policy rate target, the FOMC uses a variety of models that produce rate recommendations. Policymakers are not bound to follow the models’ recommendations, and always have room to use their own judgment.[30]

The Fed derives one federal funds rate benchmark by using optimal control (OC) techniques. The OC method entails building a model of how many different economic variables affect each other over time and combining it with a “loss function,” which quantifies how much policymakers dislike different macroeconomic outcomes. The method produces recommendations for the policy rate that would be “optimal” under those particular modeling assumptions and description of policymakers’ preferences. Note that there is no single policy that is objectively optimal; it is conditional on the selection of the loss function, which is a value judgment. But even if everyone could agree on the most appropriate loss function to use, uncertainty and instability in macroeconomic relationships would still make it difficult to agree on an optimal policy. Still, OC techniques provide guidance on the range of policy choices that are reasonable.

A challenge for monetary policy is that the response of some macroeconomic variables to monetary policy is slow; controlling the economy is like steering a ship when there are long lags between moving the rudder and the ship responding.[31] Given this situation, OC theory prescribes small and cautious policy movements to avoid overshooting.[32] However, in exigent circumstances, such as the start of a financial crisis, policymakers can take more aggressive action so long as they maintain discretion.[33]

Other challenges with monetary policy based on OC and discretion have to do with transparency, predictability, and accountability. Because of their complexity, monetary policy decisions are difficult to communicate to the public and difficult to predict, which can raise public uncertainty.[34] Even if the Fed makes great efforts to communicate its goals and plans, citizens may have difficulty verifying that the Fed is acting in their best interests without undue influence from financial or other interest groups.

Many of the rules and targets that have been proposed are purported to improve transparency, predictability, and accountability. Whether they would do so effectively, while producing favorable macroeconomic and employment outcomes, is the subject of ongoing debate, which we attempt to outline below.

III. The Taylor Rule

In a 1993 study, John Taylor[35] maintained that the Fed’s behavior from the mid-1980s to 1993 was well described by an equation relating the federal funds rate to the output gap and inflation:

federal funds rate = 0.5 * output gap + 1.5 * inflation + 1

where the output gap is the percent deviation of real GDP from its potential. Since then, a Taylor rule has come to refer to an operational mandate in which the central bank sets its policy rate according to a formula that may include inflation, output, or other economic variables. Some versions of the Taylor rule use the deviation of unemployment from its “natural rate” in place of the output gap. Under a Taylor rule, then, the Fed tends to raise the federal funds rate when inflation and output and employment are high and to lower the fed funds rate when they are low.

The Fed uses rules like the above as guidance for how to set policy rates, but it is not required to follow the recommendation of any particular rule. Taylor and others have argued that legislation should require the Fed to choose and disclose a rule.[36] This argument is based on both political/ ideological and macroeconomic grounds. On the ideological side, limiting the Fed’s instrument independence via an operational mandate appeals to those who dislike the power and discretion exercised by unelected officials. On the macroeconomic side, requiring the Fed to adhere to a rule appeals to those who see adverse consequences from discretionary policies that they perceive are often too loose or too tight. For instance, Taylor points to the economic stability of the years 1985 to 2003,[37] when the federal funds rate closely followed the recommendations of the Taylor rule (economist Allan Meltzer characterizes these years as the “rules-based era” of monetary policy[38]). Taylor argues that Fed policy in 2003–2005 was looser than prescribed by the Taylor rule, contributing to the housing bubble. Former Fed Chair Ben Bernanke, however, calculates[39] that Fed policy has actually followed a version of the Taylor rule consistently, even since 2003, so neither the bubble nor the slow recovery can be attributed to deviations from the rule’s recommendations.

Requiring the Fed to follow a Taylor rule would likely be detrimental to the full employment goal. As Chairwoman Janet Yellen[40] notes, “the simple rules that perform well under ordinary circumstances just won't perform well with persistently strong headwinds restraining recovery and with the federal funds rate constrained by the zero bound.” Following the Great Recession, for example, the original form of the Taylor rule would have directed the Fed to raise interest rates above zero in 2011,[41] years before the labor market recovery was near completion, which would have slowed the recovery even further. In several other historical episodes, the economy has benefited from the Fed’s discretion and flexibility, including in reaction to the Russian debt default in 1998 and to the bursting of the tech bubble in 2001; in both cases the easing was faster and larger than would have been suggested by Taylor-type rules.[42]

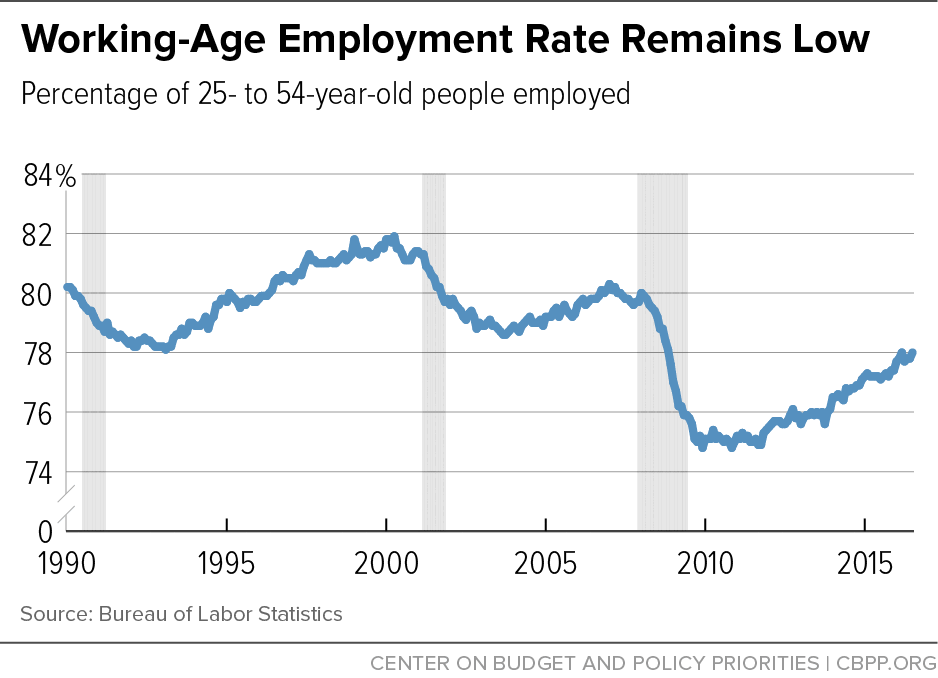

The Taylor rule also poses several implementation difficulties that could risk harming the prospects for full employment. First, several of the variables are difficult to measure.[43] Potential GDP and the natural rate of unemployment vary over time and cannot be observed, but must be estimated. And the estimates can be noisy,[44] leading to policy that is either too tight or too loose. A related downside is that the Taylor rule uses a single measure — the output gap, or unemployment — as an indicator of real economic activity, which may not fully capture how far the economy is from full employment. Today, wage growth at the bottom and middle of the income distribution remains low even as unemployment has fallen. The employment rate of the working-age population remains low as well.[45] (See Figure 2.)

Bernanke suggests[46] that the optimal weights on the output gap and inflation in the Taylor rule vary over time with changes in the structure of the economy; the implication is that disclosing a specific rule to Congress would make it more difficult for the Fed to adapt to these changes.[47] Bernanke’s point underscores a fundamental limitation of rule-based policymaking that can have negative implications for achieving full employment. The structure of key economic relationships is constantly changing, underscoring the critical role for both flexibility and adaptability.

IV. Inflation Targeting

Unlike the Taylor rule, which would require the central bank to set its policy interest rate according to a specific formula, inflation targeting specifies the central bank’s goal, but not how it should set its policy rate. An inflation-targeting (IT) central bank chooses an explicit number for the inflation rate — the percent change in the price index — as its sole objective, and it can set interest rates as it sees fit to achieve that objective. New Zealand became the first country to officially implement IT in 1990, and since the switch inflation has been lower and output growth higher than before. Around 26 high- and low-income countries now use IT, including Canada, the United Kingdom, Sweden, Australia, and Brazil.[48] Bernanke explains that “the Federal Reserve, though rejecting the inflation-targeting label, has greatly increased its credibility for maintaining low and stable inflation, has become more proactive in heading off inflationary pressures, and has worked hard to improve the transparency of its policymaking process — all hallmarks of the inflation-targeting approach.”[49]

A benefit of IT is that it provides a high degree of transparency and accountability. With a single, quantitative objective, it is easy to judge whether the central bank has achieved its goal. The choice of this transparent mechanism can also lend credibility to the central bank’s commitment to price stability and contribute to improved macroeconomic outcomes. Before the 2008 financial crisis, there was a growing consensus that inflation targeting was the best practice for monetary policy, responsible for low and stable inflation, well-anchored expectations, and a more favorable tradeoff between inflation and output volatility.[50] However, these benefits are not universally acknowledged. Laurence Ball and Niamh Sheridan, for example, note that, although countries that adopted IT experienced macroeconomic improvements, countries that did not adopt IT experienced similar improvements around the same time.[51]

The largest downside to IT is that it severely limits a central bank’s ability to aggressively pursue full employment. Most inflation-targeting central banks have adopted a flexible form of IT that focuses on achieving the target in the medium term (around two or three years) and allows some room for smoothing output over the shorter term, within limits. Flexible IT thus combines aspects of discretionary monetary policy with aspects of rules-based policy.[52] But when the price stability and employment objectives come into conflict, IT central banks ultimately prioritize price stability.[53]

Even though IT is not an ideal monetary policy regime for promoting full employment, its prospects could be improved by moderately raising the inflation target. The typical target of 2 percent was chosen to help alleviate problems associated with “wage stickiness.” Workers tend to strongly dislike nominal wage cuts, so if inflation is near zero and a company or industry is hit by a negative shock, it may choose to lay off workers rather than cut nominal wages. Slightly higher inflation can make it easier for employers to respond to negative shocks by giving smaller nominal wage increases or none at all, rather than reducing employment. The 2 percent target is intended to be high enough to give wages room to adjust, while avoiding the downsides of higher inflation.[54]

Ball makes the case for an inflation target of 4 percent rather than 2 percent.[55] “The primary reason to raise inflation targets,” he writes, “is to ease the zero-bound problem, the constraint on monetary policy arising from the fact that nominal interest rates cannot be negative. A higher inflation target raises the long-run levels of nominal rates, allowing larger decreases in rates before the zero bound becomes binding. This flexibility makes it easier for a central bank to restore full employment when an economic slump occurs.” In several countries, nominal interest rates have in fact become slightly negative recently, demonstrating that the zero lower bound is not a firm constraint. Still, there are limits to how negative rates can go before investors prefer to hold cash. A higher inflation target would give central banks more room to maneuver in a downturn.

V. Price-Level Targeting

Under price-level targeting, the central bank selects an optimal path for the growth of the price level over time. As with inflation targeting, the central bank adjusts the short-term interest rate to keep the economy on target.[56] However, unlike inflation targeting, price-level targeting requires any gains in inflation to be offset by reductions in inflation of equal magnitude, keeping the economy on the designated price-level path.[57] Under inflation targeting, shocks to inflation create permanent shifts in the price-level path, but under price-level targeting that path is fixed.73

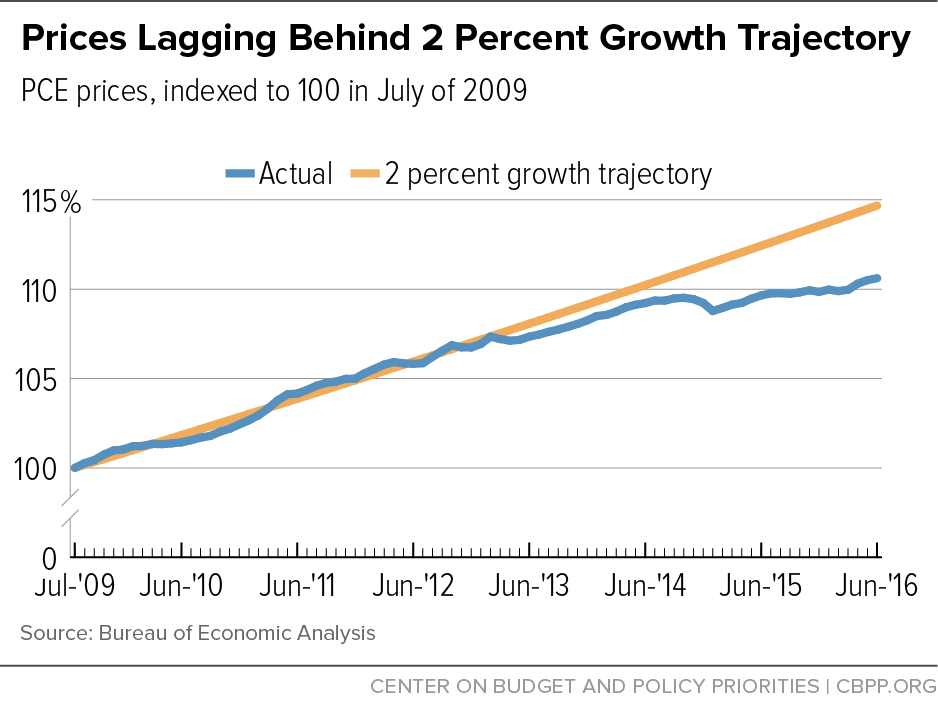

In the U.S. economy, inflation has averaged below 2 percent over the past five years. (See Figure 3.) If the Federal Reserve were to adopt a price-level target, it would be required to balance below-target inflation with above-target inflation, a mandate that could counteract its recent tendency to undershoot its inflation target.[58] This would remove any uncertainty about whether the target is symmetric or a “ceiling.”

In terms of reaching full employment, price-level targeting may be more effective than inflation targeting. In response to a demand shock that lowered both output growth and inflation, a central bank using price-level targeting would reduce the output gap more aggressively than a bank using inflation targeting,[59] thus keeping employment more stable.[60] Stability benefits could also come through expectations.[61] Any negative demand shock resulting in below-target prices and low output will result in an expectation of higher future inflation, which will lower the real interest rate (since the real interest rate is the nominal interest rate minus expected inflation), in turn stimulating the economy and offsetting the negative shock. In theory, this policy also reduces the constraints of the zero lower bound.[62] With stable expectations of future prices, consumers and firms may feel more confident engaging in long-term contracts,[63] thereby increasing investment and producing more jobs.

While the benefits of price-level targeting are clear when the economy is hit by demand shocks, supply shocks are less straightforward. Consider an adverse supply shock that lowers output growth and raises inflation. Strict adherence to a price-level target would require monetary policymakers to tighten policy to offset the rising prices, exacerbating the unfavorable output and unemployment outcome. To address this issue, Hall (1984) suggests an “elastic” variant of price-level targeting in which deviations from the price-level target are allowed to depend on the unemployment rate: when unemployment is especially high, the price level is allowed to temporarily go above target.[64] This is also called an output-gap-adjusted price-level target, and in theory could be particularly useful in minimizing the distortions created by the zero lower bound on nominal interest rates.[65] Ball et al. (2005) find that such a policy is superior to inflation targeting.[66]

Although the Bank of Canada has studied the efficacy of a price-level target, no central bank has ever actually instituted a price-level-targeting rule.[67] In part, this could reflect a path dependency: since the Bank of New Zealand first adopted inflation targeting, other central banks have followed suit and are now reluctant to change course. The FOMC, for instance, at its November 2011 meeting, noted that “price-level targeting where the central bank maintained flexibility to stabilize economic activity over the short term could generate economic outcomes that would be more consistent with the dual mandate,” but that “a number of participants expressed concern that switching to a new policy framework could heighten uncertainty about future monetary policy.”[68] But it could be argued that the benefits of switching to a more effective framework are likely to offset any temporary increase in uncertainty that might occur.

VI. Nominal Income (or NGDP) Targeting

The nominal gross domestic product (NGDP), or nominal income, is the sum of all spending or all income in the U.S. economy, not adjusted for inflation. Under nominal income targeting, a central bank would choose and announce either a target growth rate for NGDP or a target path for NGDP and adjust its policy rate to help achieve the target in the medium run; the bank would lower rates if NGDP were below target and raise them if NGDP were above target. For many of the same reasons that price-level targeting would improve upon inflation targeting, targeting the level of NGDP is preferable to targeting the growth rate for NGDP.[69] Since NGDP growth is the sum of real GDP growth and inflation, an NGDP target would incorporate both real economic conditions and inflation, consistent with the Fed’s dual mandate, and would provide a well-defined way for the Fed to decide whether conditions were too tight or too loose.

Nominal income targeting has been discussed since at least the 1970s,[70] though it has received more attention since the Great Recession. In fact, the FOMC discussed the possibility of NGDP targeting at its November 2011 meeting, and considered simulations that suggested NGDP targeting could promote a stronger economic recovery while maintaining price stability.[71] However, the minutes note that “Several participants observed that the efficacy of nominal GDP targeting depended crucially on … the premise that the Committee could make a credible commitment to maintaining such a strategy over a long time horizon and that policymakers would continue adhering to that strategy even in the face of a significant increase in inflation. In addition, some participants noted that such an approach would involve substantial operational hurdles, including the difficulty of specifying an appropriate target level.”[72]

The FOMC members’ qualms about NGDP targeting are surmountable. First, credibility is essential no matter what policy strategy the Fed chooses, and can be established by demonstrating and communicating commitment to the target consistently. The transparency of an NGDP target facilitates the communication and accountability that improve credibility. In addition, economist Scott Sumner argues that the politics of NGDP targeting may be better than those of inflation targeting. If a central bank needs to lower interest rates, explaining that it intends to raise nominal income may be more popular than explaining that it needs to raise inflation.[73]

Second, specifying an appropriate target level is feasible. Christina Romer, a monetary economist and former chair of the Council of Economic Advisers, suggests that, if normal output growth for the United States is about 2.5 percent a year and the Fed believes that 2 percent inflation is appropriate,[74] the target path for NGDP should be growth of 4.5 percent per year, i.e., the sum of the two. If the potential output growth rate were to change substantially, as it has in the past,[75] then the normal level of inflation acceptable under NGDP targeting would change. For example, if output growth averages only 1% per year, then inflation would average 3.5 percent per year (the difference between the nominal growth rate and the real growth rate). But this is not likely to be a large problem, because under any reasonable potential growth rate inflation would average below 5 percent, far from a harmful level.

NGDP targeting could potentially be quite effective from the perspective of full employment. Advocates of NGDP targeting note that an NGDP target would have required the Fed to act more aggressively earlier in 2008, since NGDP growth was negative in the third quarter of 2008 while core inflation was still positive.[76] Others argue that the Fed’s failure to act more aggressively was due not to its policy framework but to its forecast—it did not expect the recession to be as severe as it was.[77] Still, between 2007 and 2009 NGDP growth averaged 1.38 percent, which would have signaled the need for easier monetary policy that could have reduced the severity of the recession. From 2010 to 2016, NGDP growth has averaged 3.77 percent, with a range from 2.51 percent to 4.82 percent,[78] and so this target would have implied the need for easier monetary policy in the recovery period as well. It is thus reasonable to suppose that NGDP targeting would have resulted in more favorable employment outcomes. Another reason that NGDP targeting could more effectively promote full employment is that people’s ability to repay debt depends on nominal income,[79] so nominal income stability should also promote financial stability. This is important since financial instability can lead to deeper recessions with more job loss.

Since NGDP responds slowly to monetary policy, Sumner proposes a futures contract approach that would allow monetary policy to respond to expected future NGDP instead of current NGDP.[80] The Fed would set up a futures market in which participants would bet as to whether the future NGDP growth rate would exceed or fall short of the Fed’s target. The Fed would then adjust the monetary base, just as it does today, according to the bets. So, if traders on this NGDP prediction market thought nominal growth would exceed the Fed’s target, the Fed would reduce the base, and vice versa.[81]

This approach is based on the notion that the market is an efficient forecaster, but it could be problematic for a number of reasons. For instance, the futures market could be subject to manipulation by large speculators,[82] or trading volume could be too low. More broadly, the futures-market approach would drastically limit the Fed’s discretion; the Fed would play a passive role. We think it would be more effective for the Fed to commit to pursuing the NGDP target in the medium run, taking into account the Fed’s own forecasts of future NGDP in its policy decisions.

VII. Nominal Wage Targeting

Nominal wage targeting can refer to targeting the wage rate (the price of labor) or targeting the quantity of wages paid (total nominal labor compensation, or the average hourly wage times the total number of hours worked). The former can be thought of as a special type of inflation targeting, since wages themselves are a price and wage growth is a type of inflation. Inflation-targeting central banks choose which specific price index to use for their inflation target; nominal wage targeting entails choosing a price index with 100 percent weight on wages. Mankiw and Reis (2003) find that “a central bank that wants to achieve maximum stability of economic activity should use a price index that gives substantial weight to the level of nominal wages.”[83]

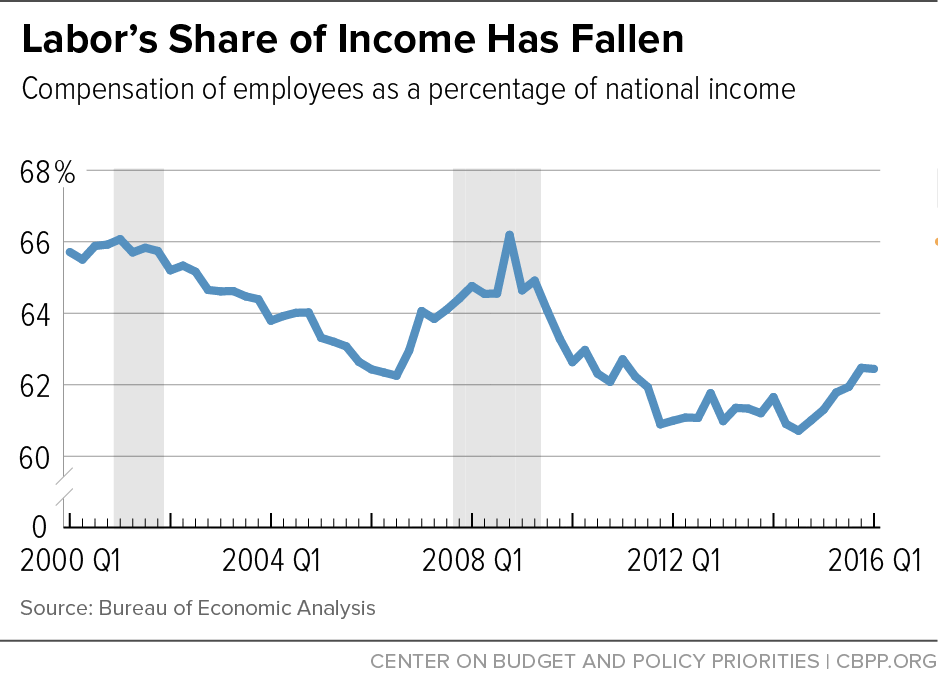

When workers become more productive, the economy grows faster. When real wages grow at the same pace as productivity (or equivalently, when nominal wages grow at the rate of productivity plus inflation), this growth potentially leads to shared prosperity. Thus, Josh Bivens suggests that the target growth rate of nominal wages should be around 3.5 percent, reflecting the sum of 2 percent inflation and 1.5 percent productivity growth.[84] This would keep labor’s share of income stable. In the United States, real wages have not kept pace with productivity growth since the 1970s,[85] so labor’s share of GDP has declined from 65 percent in 2001 to just 60 percent in 2014. (See Figure 4.)

The promise of nominal wage targeting stems from the fact that strong wage growth is the clearest indicator of full employment. When the economy is at full employment, it becomes easier for workers to bargain for higher wages, so employers who wish to retain and hire workers must pay them more.[86] Slow nominal wage growth signals a need for looser monetary policy to restore full employment. If the central bank were to commit to a set rate of wage growth or a path of nominal wages, it would also be committing to maintaining labor market conditions sufficiently strong to give workers enough bargaining power to reap the gains of productivity growth. Price inflation, in contrast, is not as clear an indicator of employment conditions.[87] In fact, the link between price inflation and wage inflation appears to have weakened.[88]

Nominal wage targeting has never been attempted, and its implementation could entail several challenges. First, there is no single wage rate. Policymakers would need to choose whether to target mean or median wages or some other measure. Second, nominal wages tend to respond to monetary policy with a lag. It may thus be preferable to target either expected future wages or total nominal labor compensation, which reacts more quickly.

Targeting total nominal labor compensation, or the quantity of wages, would bear strong similarities to nominal income targeting, since the largest component of national income is wages, the income that accrues to labor. Stabilizing nominal wage growth would tend to stabilize NGDP growth, and vice versa. Nominal wage targeting would imply somewhat larger monetary responses to supply shocks, since an adverse supply shock typically reduces the share of labor in national income. Thus, nominal wage targeting could help reduce unemployment that occurs in response to adverse supply shocks.[89] In fact, Sumner, one of the biggest proponents of NGDP targeting, has suggested that nominal labor compensation targeting (or nominal labor compensation per capita targeting) could be preferable to NGDP targeting, since it would minimize employment fluctuations while maintaining low inflation on average.[90]

VIII. Conclusions

Monetary policy rules can provide a number of important benefits. A simple and precise rule improves predictability, reduces uncertainty about the motives for policymakers’ actions, facilitates accountability,[91] and reduces political interference. Commitment to a monetary rule can also reduce the “time-inconsistency problem” that arises when policymakers have incentives to pursue short-run objectives even if the result is poor long-run outcomes.[92] Traditionally, the time-inconsistency problem is thought to lead to overly high inflation. This was a large concern in the 1970s, but today the concern is less-than-full employment, often accompanied by excessively low inflation.

Strict rules are too mechanical and inflexible under unforeseeable circumstances or when financial and technical changes alter monetary and macroeconomic relationships.[93] In these situations, expert judgment, or discretion, is valuable. The best compromise between strict rules and full discretion may come from a targeting rule. Unlike an instrument rule, which dictates how the central bank should set its monetary instrument (like its policy rate), a monetary target provides a defined goal for monetary policy but allows policymakers some discretion in how to attain the goal in the medium run.[94] A target is easier to communicate and provides more accountability than full discretion. Inflation targeting is the most widely implemented targeting rule, but it is not likely optimal with regard to full employment.

Central banks are understandably reluctant to make drastic changes to their monetary policy frameworks. Changes produce unknowns, and frequent changes risk generating unnecessary uncertainty and eroding the central bank’s credibility. But these are not sufficient reasons for central banks to never change the policy framework. Just as the departure from the gold standard was ultimately worthwhile, the adoption of a new target for monetary policy, if carefully considered and communicated, could reap major long-term benefits. Price-level targeting would be the easiest change to implement, especially for central banks that currently practice inflation targeting, because of the similarities between the two. Price-level targeting would improve on inflation targeting by mitigating the tendency for the inflation target to be treated more like a ceiling than a symmetric target. Nominal income or nominal wage targets, though untested, hold even more promise, at least in theory.

End Notes

[1] Carola Binder is an assistant professor at Haverford College in the Department of Economics.

[2] Alex Rodrigue is a math and economics major at Haverford College.

[3] For further discussion of monetary policy, political influences, and inequality, see Carola Binder, “Rewriting the Rules of the Federal Reserve for Broad and Stable Growth,” Roosevelt Institute, December 14, 2015, http://rooseveltinstitute.org/rewriting-rules-federal-reserve-broad-stable-growth/.

[4] Michael Bordo, “Monetary Policy Regimes, the Gold Standard, and the Great Depression,” National Bureau of Economic Research, 1999, http://www.nber.org/reporter/fall99/bordo.html.

[5] The Federal Reserve raised interest rates, tightening monetary conditions, in 1928, in an effort to curb stock market speculation and to avoid losing gold to the French. To avoid large gold outflows, other countries on the gold standard also raised interest rates, leading to deflation and depression. See Barry Eichengreen, Golden Fetters and the Great Depression, 1919-1939 (New York: Oxford University Press, 1992).

[6] Ben Bernanke and Harold James, “The Gold Standard, Deflation, and Financial Crisis in the Great Depression: An International Comparison,” in R. Glenn Hubbard, ed., Financial Markets and Financial Crisis (Chicago: University of Chicago Press, 1991), pp. 33-68.

[7] Aaron Steelman, “Employment Act of 1946,” Federal Reserve History (Richmond, Va.: Federal Reserve Bank of Richmond, 2013), http://www.federalreservehistory.org/Events/DetailView/15.

[8] Christina D. Romer and David H. Romer, “A Rehabilitation of Monetary Policy in the 1950s,” Monetary Policy Rules and Practice 92, no. 2 (2002), pp. 121-27.

[9] Laurence Meyer, “Rules and Discretion,” remarks at the Owen Graduate School of Management, Vanderbilt University, Nashville, Tenn., 2002, http://www.federalreserve.gov/boarddocs/speeches/2002/200201162/default.htm.

[10] If the central bank lacks political independence, the government may be tempted to pursue overly expansionary monetary policy — for example, before an election — undermining economic stability and fueling inflation. See John C. Williams, “Monetary Policy and the Independence Dilemma,” Federal Reserve Bank of San Francisco, 2015, http://www.frbsf.org/our-district/press/presidents-speeches/williams-speeches/2015/may/monetary-policy-independence-dilemma/.

[11] Milton Friedman, A Program for Monetary Stability (New York: Fordham University Press, 1960).

[12] Williams, “Monetary Policy and the Independence Dilemma.”

[13] See Pedro Da Costa, “House Republicans Want Fed to Adopt Policy-Making Rules,” Wall Street Journal, July 9, 2014, http://blogs.wsj.com/economics/2014/07/09/republicans-want-fed-to-report-to-congress-on-monetary-policy/. Recent legislative initiatives include the Centennial Monetary Commission Act of 2015, the Sound Dollar Act of 2015, and the Fed Oversight Reform and Modernization Act of 2015. Also see Thomas Gaudett, “The Politics of the Federal Reserve,” Harvard Political Review, May 24, 2011.

[14] Federal Reserve Bank of Chicago, “The Federal Reserve’s Dual Mandate,” revised August 5, 2016, https://www.chicagofed.org/publications/speeches/our-dual-mandate.

[15] Although the Fed’s official target is overall, or headline, PCE inflation, it often focuses on core PCE inflation, which excludes volatile prices like energy and food. See James Bullard, “Measuring Inflation: The Core Is Rotten,” speech at the Money Marketeers of New York University, May 18, 2011.

[16] Board of Governors of the Federal Reserve System, press release, January 25, 2012, https://www.federalreserve.gov/newsevents/press/monetary/20120125c.htm.

[17] Anchored expectations refers to inflation expectations that are “relatively insensitive to incoming data” and remain stable in response to shocks; Ben Bernanke, “Inflation Expectations and Inflation Forecasting,” speech to the Monetary Economics Workshop for the National Bureau of Economic Research Summer Institute, Cambridge, Mass., June 10, 2007, https://www.federalreserve.gov/newsevents/speech/bernanke20070710a.htm.

[18] Board of Governors of the Federal Reserve System, press release, January 27, 2016, https://www.federalreserve.gov/newsevents/press/monetary/20160127b.htm.

[19] Lawrence Summers, “The Fed Is Making the Same Mistakes Over and Over Again,” Washington Post, June 14, 2016, https://www.washingtonpost.com/news/wonk/wp/2016/06/14/larry-summers-the-fed-is-making-the-same-mistakes-over-and-over-again/.

[20] Federal Reserve Bank of San Francisco, “What Are the Costs of Deflation?” Dr. Econ, February 2006, http://www.frbsf.org/education/publications/doctor-econ/2006/february/deflation-costs.

[21] William Easterly and Stanley Fischer, “Inflation and the Poor,” Journal of Money, Credit and Banking 33, no. 2 (2001), pp. 160-78; Robert Pollin and Andong Zhu, “Inflation and Economic Growth: A Cross-Country Non-Linear Analysis,” Political Economy Research Institute, 2005; Michael Bruno and William Easterly, “Inflation Crises and Long-Run Growth,” Journal of Monetary Economics 41 (1998), pp. 3–26.

[22] Matthias Doepke and Martin Schneider, “Inflation and the Redistribution of Nominal Wealth,” Journal of Political Economy 114, no. 6 (2006), pp. 1069-97.

[23] Andres Erosa and Gustavo Ventura, “On Inflation as a Regressive Consumption Tax,” Journal of Monetary Economics 49, no. 4 (2002), pp. 761-95.

[24] Board of Governors of the Federal Reserve System, “What Are the Federal Reserve’s Objectives in Conducting Monetary Policy?” Current FAQs, https://www.federalreserve.gov/faqs/money_12848.htm.

[25] The 4.8 percent estimate is in line with the U.S. Congressional Budget Office’s current estimate of the nonaccelerating inflation rate of unemployment, or NAIRU.

[26] Dean Baker and Jared Bernstein, “Getting Back to Full Employment,” Center for Economic and Policy Research, 2013, http://www.cepr.net/documents/Getting-Back-to-Full-Employment_20131118.pdf.

[27] Alan Blinder, “Petrified Paychecks,” Washington Monthly, November-December 2014, http://www.washingtonmonthly.com/magazine/novemberdecember_2014/features/petrified_paychecks052713.php?page=all.

[28] This concept is known as hysteresis; see Lawrence Ball, “Hysteresis in Unemployment: Old and New Evidence,” National Bureau of Economic Research, March 2009, http://www.nber.org/papers/w14818.

[29] Baker and Bernstein, “Getting Back to Full Employment.”

[30] Flint Brayton, Thomas Laubach, and David Reifschneider, “Optimal-Control Monetary Policy in the FRB/US Model,” FEDS Notes, November 24, 2014, http://www.federalreserve.gov/econresdata/notes/feds-notes/2014/optimal-control-monetary-policy-in-frbus-20141121.html#.

[31] Robert E. Hall and N. Gregory Mankiw, “Nominal Income Targeting,” in N. Gregory Mankiw, ed., Monetary Policy (Chicago: University of Chicago Press, 1994).

[32] If monetary policymakers respond to forecasts, not just contemporary realizations, they can help mitigate this issue. See Robert J. Gordon, “The Conduct of Domestic Monetary Policy,” in Albert Ando, Hidekazu Eguchi, Roger Farmer, and Yoshio Suzuki, eds., Monetary Policy in Our Times (Cambridge, Mass.: MIT Press, 1985), pp. 45-81. Also see Robert E. Hall, “Monetary Strategy With an Elastic Price Standard,” paper presented at the symposium, “Price Stability and Public Policy,” Federal Reserve Bank of Kansas City, 1985.

[33] David Wheelock, “Lessons Learned? Comparing the Federal Reserve’s Responses to the Crises of 1929-1933 and 2007-2009,” Federal Reserve Bank of St. Louis Review 92, no. 2 (March/April 2010), pp. 89-107.

[34] Janet L. Yellen, “Revolution and Evolution in Central Bank Communications,” speech at the Haas School of Business, University of California, Berkeley, November 13, 2012, http://www.federalreserve.gov/newsevents/speech/yellen20121113a.htm.

[35] John Taylor, “Discretion Versus Policy Rules in Practice,” Carnegie-Rochester Conference Series on Public Policy 39 (1993), pp. 195-214.

[36] An example of such proposed legislation is the Federal Reserve Accountability and Transparency Act of 2014.

[37] John Taylor, “Monetary Policy Rules Work and Discretion Doesn’t: A Tale of Two Eras,” Journal of Money, Credit, and Banking 44, no. 6 (2012), pp. 1017–32.

[38] Allan H. Meltzer, “Federal Reserve Policy in the Great Recession,” remarks presented at

Cato Institute Monetary Conference, November 2011.

[39] Ben S. Bernanke, “The Taylor Rule: A Benchmark for Monetary Policy?” Brookings Institution, April 28, 2015, http://www.brookings.edu/blogs/ben-bernanke/posts/2015/04/28-taylor-rule-monetary-policy.

[40] Yellen, “Revolution and Evolution in Central Bank Communications.”

[41] This calculation is from Bernanke, “The Taylor Rule.”

[42] Donald L. Kohn, “Comment on Goodfriend: ‘Inflation Targeting in the United States?’” speech at the National Bureau of Economic Research Conference on Inflation Targeting, Bal Harbour, Florida, January 25, 2003.

[43] Bernanke notes that “The Taylor rule also assumes that the equilibrium federal funds rate (the rate when inflation is at target and the output gap is zero) is fixed, at 2 percent in real terms…. Both FOMC participants and the markets apparently see the equilibrium funds rate as lower than standard Taylor rules assume. But again, there is plenty of disagreement, and forcing the FOMC to agree on one value would risk closing off important debates” (Bernanke, “The Taylor Rule”).

[44] D. Staiger, J.H. Stock, and M.W. Watson, “The NAIRU, Unemployment, and Monetary Policy,” Journal of Economic Perspectives 11, no. 1 (1997), pp. 33-49.

[45] This issue could be partially addressed by modifying the Taylor rule to incorporate more indicators of labor market health on the right-hand side.

[46] Bernanke, “The Taylor Rule.”

[47] Taylor recommends that “The Fed could change its strategy or deviate from it if circumstances called for a change, but the Fed would have to explain why.” See John B. Taylor, “A Monetary Policy for the Future,” Economics One (A blog by John B. Taylor), April 16, 2015, https://economicsone.com/2015/04/16/a-monetary-policy-for-the-future/.

[48] Scott Roger, “Inflation Targeting Turns 20,” IMF: Finance & Development (2010), pp. 46-49.

[49] Ben Bernanke, “A Perspective on Inflation Targeting,” Annual Washington Policy

Conference of the National Association of Business Economists, Washington, D.C., 2003.

[50] Frederic S. Mishkin, “International Experiences With Different Monetary Policy Regimes,” Journal of Monetary Economics 43 (1999), pp. 579–605; Marco Vega and Diego Winkelried, “Inflation Targeting and Inflation Behavior: A Successful Story?” International Journal of Central Banking 1, no. 3 (2005), pp. 153-75.

[51] Laurence Ball and Niamh Sheridan, “Does Inflation Targeting Matter?” in Ben Bernanke and Michael Woodford, eds., The Inflation Targeting Debate (Chicago: University of Chicago Press, 2004).

[52] Lars Svensson, “Inflation Forecast Targeting: Implementing and Monitoring Inflation Targets,” European Economic Review 41 (1997), pp. 1111–46.

[53] Christian Gillitzer and John Simon (in “Inflation Targeting: A Victim of its Own Success,” International Journal of Central Banking 11, no. S1 (2015), pp. 259-87) write that “it is suggested that the European Central Bank delayed lowering interest rates because it was overly concerned about headline inflation rates that were being boosted by temporary oil and commodity price increases,” a clear example of prioritization of price stability.

[54] According to the Board of Governors of the Federal Reserve, inflation higher than 2 percent “would reduce the public’s ability to make accurate longer term and financial decisions,” and “a lower inflation rate would be associated with an elevated probability of falling into deflation”; see “Why Does the Fed Aim for 2 Percent Inflation Over Time?” https://www.federalreserve.gov/faqs/economy_14400.htm.

[55] Laurence Ball, “The Case for a Long-Run Inflation Target of Four Percent,” International Monetary Fund, 2014.

[56] Kahn, “Beyond Inflation Targeting.”

[57] S. Ambler, “Price-Level Targeting and Stabilization Policy: A Survey,” Journal of Economic Surveys 23, no. 5 (2009), pp. 974–97.

[58] Lars E.O. Svensson, “Commentary: How Should Monetary Policy Respond to Shocks While Maintaining Long-Run Price Stability? — Conceptual Issues,” 1996, larseosvensson.se/files/papers/S96SVEN.PDF.

[59] R. Dittmar, W.T. Gavin, and F.E. Kydland, “The Inflation-Output Variability Tradeoff and Price-Level Targets,” Federal Reserve Bank of St. Louis Review (1999), pp. 23-32.

[60] In the event of a persistent output gap, Dittmar, Gavin, and Kydland (“The Inflation-Output Variability Tradeoff”) find theoretical evidence for the effectiveness of price-level targeting rules as a means to avoid inflation instability.

[61] Kahn, “Beyond Inflation Targeting”; J.C. Williams, “Monetary Policy at the Zero Lower Bound: Putting Theory Into Practice,” Federal Reserve Bank of San Francisco (2014), pp. 1-16.

[62] R. Billi, “Price-Level Targeting and Risk Management in a Low-Inflation Economy,” Federal Reserve Bank of Kansas City (2008).

[63] R. Amano, T. Carter, and D. Coletti, “Next Steps for Canadian Monetary Policy,” Bank of Canada Review (2009).

[64] Specifically, Hall (“Monetary Strategy With an Elastic Price Standard”) proposes a constant price-level target and argues that the deviation of the price level from target can be eight times the deviation of unemployment from its normal level.

[65] Gauti Eggertsson and Michael Woodford, “The Zero Bound on Interest Rates and Optimal Monetary Policy,” Brookings Papers on Economic Activity, 2003.

[66] Laurence Ball, N. Gregory Mankiw, and Ricardo Reis, “Monetary Policy for Inattentive Economies,” Journal of Monetary Economics 52, no. 4 (2005), pp. 703-25.

[67] Ambler, “Price-Level Targeting and Stabilization Policy.”

[68] Minutes of the Federal Open Market Committee, November 1-2, 2011, http://www.federalreserve.gov/monetarypolicy/fomcminutes20111102.htm.

[69] In simulation exercises, targeting the NGDP trajectory results in better price stability and output stability than targeting the NGDP growth rate; see Hall and Mankiw, “Nominal Income Targeting.”

[70] James Meade, “The Meaning of Internal Balance,” Economic Journal 91: 423-35.

[71] It should be noted that such simulations are sensitive to modeling assumptions; see Glenn Rudebusch, “Assessing Nominal Income Rules for Monetary Policy With Model and Data Uncertainty,” Economic Journal 112 (April 2002), pp. 402–32.

[72] Minutes of the Federal Open Market Committee, November 1-2, 2011.

[73] Scott Sumner, “Re-Targeting the Fed,” National Affairs 9 (Fall 2011), http://www.nationalaffairs.com/doclib/20110919_Sumner.pdf.

[74] Christina Romer, “Dear Ben: It’s Time for Your Volcker Moment,” New York Times, October 29, 2011, http://www.nytimes.com/2011/10/30/business/economy/ben-bernanke-needs-a-volcker-moment.html?_r=0.

[75] Margaret Jacobson and Filippo Occhino, “Behind the Slowdown of Potential GDP,” Federal Reserve Bank of Cleveland Economic Trends (2013), https://www.clevelandfed.org/newsroom-and-events/publications/economic-trends/2013-economic-trends/et-20130212-behind-the-slowdown-of-potential-gdp.a11spx.

[76] Scott Sumner, “How Nominal GDP Targeting Could Have Prevented the Crash of 2008,” in David Beckworth, ed., Boom and Bust Banking: The Causes and Cures of the Great Recession (Oakland, Calif.: Independent Institute, 2012).

[77] The Economist, “NGDP Targeting Will Not Provide a Volcker Moment,” November 1, 2011, http://www.economist.com/blogs/freeexchange/2011/11/case-against-case-nominal-gdp-target.

[78] “Nominal GDP Forecast,” OECD Data – OECD Economic Outlook: Statistics and Projections, https://data.oecd.org/gdp/nominal-gdp-forecast.htm.

[79] Evan F. Koenig, “Like a Good Neighbor: Monetary Policy, Financial Stability, and the Distribution of Risk,” International Journal of Central Banking 9, no. 2 (2013), pp. 57-82.

[80] Scott Sumner, “Using Futures Instrument Prices to Target Nominal Income,” Bulletin of Economic Research 41, no. 2 (1989), pp. 157–62; Scott Sumner, “Let a Thousand Models Bloom: The Advantages of Making the FOMC a Truly ‘Open Market,’” Contributions to Macroeconomics 6, no. 1 (2006), pp. 1–27.

[81] Sumner, “Re-Targeting the Fed.”

[82] Mike Sankowski, “Why Scott Sumner’s NGDP Level Futures Will Give Goldman Sachs $500bn in One Day, Part I,” Monetary Realism, July 10, 2012, http://monetaryrealism.com/why-scott-sumners-ngdp-level-futures-will-give-goldman-sachs-500bn-in-one-day-part-i/.

[83] Gregory Mankiw and Ricardo Reis, “What Measure of Inflation Should a Central Bank Target?” Journal of the European Economic Association 1, no. 5 (2003), pp. 1058-86. Other authors have found that optimal monetary policy aims to minimize not only inflation volatility and output volatility, but also wage volatility. See Christopher J. Erceg, Dale W. Henderson, and Andrew T. Levin, “Optimal Monetary Policy With Staggered Wage and Price Contracts,” Journal of Monetary Economics 46, no. 2 (2000), pp. 281-313; and Pierpaolo Benigno and Michael Woodford, “Optimal Stabilization Policy When Wages and Prices Are Sticky: The Case of a Distorted Steady State,” Journal of the European Economic Association 3, no. 6 (2004), pp. 1185-1236.

[84] Josh Bivens, “A Vital Dashboard Indicator for Monetary Policy: Nominal Wage Targets,” Economic Policy Institute, 2015.

[85] Joseph Stiglitz, Rewriting the Rules of the American Economy, Roosevelt Institute, 2015; Ian Dew-Becker and Robert Gordon, “Where Did the Productivity Growth Go? Inflation Dynamics and the Distribution of Income,” National Bureau of Economic Research, 2005.

[86] This relationship between labor market conditions and wage inflation is known as the Phillips curve, first documented by A.W. Phillips in 1958. Modern variants of the Phillips curve typically use price inflation, while the original curve uses wage inflation. See “The Relation Between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861–1957,” Economica 25, no. 2 (1958), pp. 283–99.

[87] Bivens (“A Vital Dashboard Indicator”) notes that price inflation occurring in the absence of wage inflation is usually the result of supply shocks (for example, in cases of import price increases). Monetary policy is most effective at counteracting demand shocks, which affect both price and wage inflation.

[88] Ekaterina Peneva and Jeremy Rudd, “The Passthrough of Labor Costs to Price Inflation,” Finance and Economics Discussion Series 2015-042, Board of Governors of the Federal Reserve System, 2015, http://dx.doi.org/10.17016/FEDS.2015.042.

[89] David Glasner, “NGDP Targeting v. Nominal Wage Targeting,” Uneasy Money Blog, December 9, 2011, https://uneasymoney.com/2011/12/09/ngdp-targeting-v-nominal-wage-targeting/.

[90] Scott Sumner, “Nominal GDP Targeting in Developing Countries,” Library of Economics and Liberty, August 23, 2014, http://econlog.econlib.org/archives/2014/08/nominal_gdp_tar_1.html.

[91] Hall and Mankiw, “Nominal Income Targeting.”

[92] Finn Kydland and Edward Prescott, “Rules Rather Than Discretion: The Inconsistency of Optimal Plans,” Journal of Political Economy 85, no. 3 (June 1977), pp. 473-92; Frederic S. Mishkin, “International Experiences With Different Monetary Policy Regimes,” Journal of Monetary Economics 43 (1999), pp. 579–605.

[93] Ben Bernanke, “’Constrained Discretion’ and Monetary Policy,” remarks to the Money Marketeers of New York University, February 3, 2003, http://www.federalreserve.gov/boarddocs/Speeches/2003/20030203/default.htm#.

[94] Lars Svensson, “What Is Wrong With Taylor Rules? Using Judgment in Monetary Policy Through Targeting Rules,” National Bureau of Economic Research, 2003, http://www.nber.org/papers/w9421.

More from the Authors

Carola Binder is an assistant professor at Haverford College in the Department of Economics.

Alex Rodrigue is a math and economics major at Haverford College.