Research Note: New Paper Sets Out Policy and Legal Case Against Indexing Capital Gains by Regulation

indexing capital gains would be unsound policy: it would deliver a large tax cut for wealthy households that would lose significant revenue and open new tax avoidance opportunities.Prominent conservatives have called for the Treasury Department to issue a regulation that would “index capital gains” for inflation.[1] An important new paper by tax experts Daniel Hemel and David Kamin[2] explains why indexing capital gains would be unsound policy: it would deliver a large tax cut for wealthy households that would lose significant revenue and open new tax avoidance opportunities.[3] The paper also explains that in 1992, the Treasury Department under President George H.W. Bush concluded after a careful examination that it has no authority to index capital gains and shows why the argument that Treasury has this authority has, if anything, gotten weaker since then.

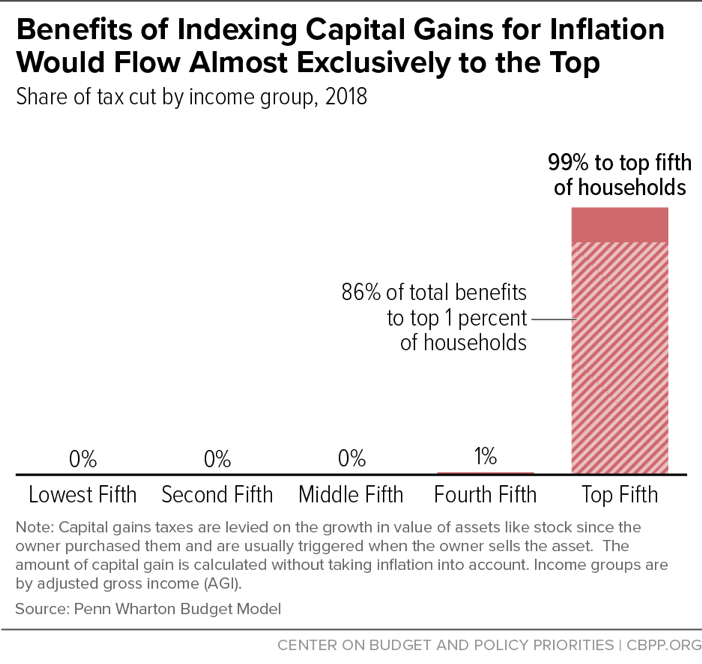

Capital gains taxes are levied on the growth in value of assets like stock since the owner purchased them and are usually triggered when the owner sells the asset. The amount of capital gain is calculated without taking inflation into account. However, the top long-term capital gains rate is 23.8 percent, far below the current 40.8 percent top tax rate on earnings from work. The lower rate and other tax preferences for income from capital gains is sometimes explained, in part, as a rough adjustment for inflation.[4] Nevertheless, some conservatives argue that the tax should apply only to the growth in assets above the rate of inflation, effectively providing another adjustment for inflation on top of the low 23.8 percent rate. Further, they claim that Treasury can interpret the tax code in a way that would allow this adjustment without new legislation. Hemel and Kamin explain, however, that both the policy case and the legal case against this proposal are overwhelming.

Indexing Capital Gains Would Be Poor Tax Policy

Indexing capital gains for inflation by regulation “would generate opportunities for tax arbitrage, reduce revenue significantly, and deliver benefits almost exclusively to those at the top of the income distribution,” Hemel and Kamin conclude. It would cost perhaps $100 billion to $200 billion over a decade, and more than 86 percent of the benefit would go to the top 1 percent of households, estimates suggest (see Figure 1).[5] That’s because capital gains are heavily concentrated among extremely wealthy households. For example, the Tax Policy Center estimates that just 4 percent of households in the lowest-income 60 percent of households report positive long-term capital gains, compared to 59 percent of households in the top 1 percent.[6] Contrary to claims from proponents that low- and moderate-income households would gain substantially through their retirement savings, the estimates above take into account holdings in retirement plans, and such households would see virtually no benefit.

Indexing capital gains for inflation would also add to the preferences that income from wealth already enjoys in the tax code. For instance, the top tax rate on capital gains is 23.8 percent, compared to a top rate of 40.8 percent on wages and salaries.[7] Further, asset owners have considerable discretion over when they pay the tax, as taxes on capital gains aren’t due when those gains are made, but usually only when the assets are sold. One justification offered for these preferences — which are themselves costly, skewed to the wealthy, and create tax avoidance opportunities — is that they roughly adjust for the lack of inflation indexing for capital gains.[8] But even if one were to accept that argument, indexing capital gains for inflation without also increasing capital gains rates would then be double-dipping.

Hemel and Kamin also note that indexing capital gains but not other parts of the tax code would create new tax avoidance opportunities. Consider a taxpayer who borrows funds to buy an asset. Her interest payments, which partly reflect the expected impact of inflation, are deductible. Adjusting only her capital gain for inflation — and not her interest payments — would therefore affect only half of the tax equation. For example, if the asset grows in value only at the rate of inflation, she would owe no capital gains tax, but she could still deduct the full interest payments. A transaction with no real economic change would, therefore, reduce the borrower’s taxes.

These gaming opportunities are “greatest for taxpayers with the highest marginal rates (who also tend to be the taxpayers with the highest incomes),” Hemel and Kamin explain. Thus, inflation indexing would likely be even more tilted towards the wealthy than the estimates above show.[9]

Treasury Lacks Legal Authority to Index Capital Gains

A rigorous legal analysis that the Treasury Department and Department of Justice conducted in 1992 concluded firmly that Treasury lacks legal authority to index capital gains for inflation.[10] The analysis found that under section 1012 of the Internal Revenue Code (IRC), the “cost” of an asset used to calculate capital gains does not mean “inflation-adjusted cost” as indexing proponents argue, but rather the nominal price that the owner paid for the asset. To reach this conclusion, Treasury carefully examined both the dictionary definition of “cost” and the term’s context in section 1012.

While proponents of indexing capital gains argue that developments since 1992 bolster their argument that Treasury can choose to reinterpret “cost” as “inflation-adjusted” cost, Hemel and Kamin show that those arguments are baseless.[11] If anything, the case that Treasury has this authority is even weaker than in 1992:

- Indexing proponents cite the 2002 Verizon Communications case, in which the Supreme Court stated that dictionary definitions don’t determine the meaning of “cost” in a section of the Telecommunications Act and that in the specific context of the Telecommunications Act, “cost” was inflation indexed. But as noted above, Treasury’s 1992 analysis relied on the dictionary definition of “cost” as well as a range of other interpretive tools, including an investigation of the term’s meaning within the context of the IRC. And the Verizon Communications decision emphasized that when interpreting statutes, context is vital.

- A number of courts, including the Supreme Court in a 1936 case, have suggested over time that “cost” in section 1012 (or its predecessors) is unambiguous and refers to the nominal amount paid for property. However, indexing proponents suggest that a 2005 Supreme Court case (Brand X) indicates that those previous decisions — and Treasury’s long-standing interpretation — don’t eliminate Treasury’s latitude on this issue and that Treasury would be owed deference if it were to change the interpretation. Hemel and Kamin explain that indexing proponents are misreading the Brand X case and that its logic, in fact, cuts against their position. Specifically, Brand X says that if courts previously found the meaning of a statute to be unambiguous, those decisions would determine the outcome; Treasury would only have leeway if the decisions were made in the face of ambiguity as to the statute’s meaning. However, the best reading of those previous cases suggests that the courts found there wasn’t any ambiguity in section 1012 regarding the meaning of “cost.” That’s also consistent with Treasury’s 1992 analysis.

- Indexing proponents note that in the 2012 Mayo Foundation case, the Supreme Court made clear that the “Chevron” approach to interpreting statutes — which states that if a statute is ambiguous and the administrative agency’s interpretation is reasonable, courts will defer to the agency’s interpretation — should be used in tax law, just as in other areas of law. But the Mayo case doesn’t call Treasury’s 1992 analysis into question, Hemel and Kamin explain, because Treasury already assumed in 1992 that the Chevron approach was appropriate for analyzing Treasury’s discretion when it came to indexing. Using that framework, Treasury found that there wasn’t discretion given the lack of ambiguity.

- Hemel and Kamin cite a major doctrinal development since 1992 making it even less likely that the courts would allow Treasury to assert that the IRC gives it discretion to index capital gains. A series of Supreme Court decisions have narrowed agency discretion and the application of Chevron deference when it comes especially to questions of “vast economic and political significance.” As Hemel and Kamin summarize, these decisions suggest that “linguistic ambiguity on its own,” even if that existed in this context, wouldn’t necessarily cause the courts to defer to an agency’s interpretation of the word “cost.” According to these decisions, “courts must consult contextual clues and common sense before concluding that Congress has delegated a decision of ‘vast economic and political significance’ to an agency.” For several reasons, including the huge cost of indexing capital gains, Hemel and Kamin find that “it simply belies common sense to conclude that Congress would delegate to Treasury what is essentially a binary choice: cut the effective tax rate on capital gains by one-third or not at all.”

If Treasury were to nevertheless assert that it has authority to index capital gains and unilaterally do so, a number of parties could plausibly challenge them in court, Hemel and Kamin explain. But the specter of being challenged in court shouldn’t be what dissuades the Administration from this course: “As a policy matter, indexing [capital gains] for inflation via regulatory action would be a recipe for arbitrage, revenue losses, and even wider wealth inequality. As a legal matter, the same arguments that led officials in the first Bush administration to reject the idea in 1992 are applicable today.”

End Notes

[1] Naomi Jagoda, “Conservatives eye new tax cut for capital gains,” The Hill, April 25, 2018, http://thehill.com/business-a-lobbying/business-a-lobbying/384728-conservatives-eye-new-tax-cut-for-capital-gains.

[2] Associate Professor Daniel Hemel (University of Chicago Law School) and Professor David Kamin (New York University School of Law), “The False Promise of Presidential Indexation,” SSRN, May 24, 2018, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3184051.

[3] These flaws — benefits skewed to the wealthiest, large revenue losses, and new tax avoidance opportunities — also characterize the major provisions of the 2017 tax law, as discussed in this CBPP analysis. Chuck Marr, Brendan Duke, and Chye-Ching Huang, “New Tax Law Is Fundamentally Flawed and Will Require Basic Restructuring,” CBPP, April 9, 2018, https://www.cbpp.org/research/federal-tax/new-tax-law-is-fundamentally-flawed-and-will-require-basic-restructuring.

[4] As a 1998 Congressional Budget Office report stated, “a preferential rate on nominal [capital] gains provides a rough adjustment for the fact that some gains reflect inflation instead of real increases in purchasing power.” “How Capital Gains Tax Rates Affect Revenues: The Historical Evidence,” March 1988, https://www.cbo.gov/sites/default/files/cbofiles/ftpdocs/84xx/doc8449/88-cbo-007.pdf. See also Leonard Burman, Statement before the House Committee on Ways and Means and the Senate Committee on Finance on Tax Reform and the Tax Treatment of Capital Gains, September 12, 2012, https://www.taxpolicycenter.org/sites/default/files/alfresco/publication-pdfs/904606-Tax-Reform-and-the-Tax-Treatment-of-Capital-Gains.PDF.

[5] John Ricco, “Indexing Capital Gains to Inflation,” March 23, 2018, https://budgetmodel.wharton.upenn.edu/economic-matters/2018/3/23/indexing-capital-gains-to-inflation; Leonard Burman, “Should Treasury Index Capital Gains?” Tax Policy Center, May 10, 2018, https://www.taxpolicycenter.org/taxvox/should-treasury-index-capital-gains.

[6] CBPP analysis of Tax Policy Center table T18-0053.

[7] For long-term capital gains, high earners face a 20 percent rate on the gain plus an additional 3.8 percent net investment income tax, for a total of 23.8 percent. For wages and salaries, high earners face a 37 percent top rate plus an additional 3.8 percent in Medicare payroll taxes for a total of 40.8 percent.

[8] Chuck Marr and Chye-Ching Huang, “Raising Today’s Low Capital Gains Tax Rates Could Promote Economic Efficiency and Fairness, While Helping Reduce Deficits,” CBPP, September 12, 2012, https://www.cbpp.org/research/raising-todays-low-capital-gains-tax-rates-could-promote-economic-efficiency-and-fairness.

[9] Indexing capital gains for inflation by legislation could mitigate such tax avoidance opportunities, but would leave in place the fact that the underlying policy is regressive and costly.

[10] Timothy Flanigan, “Legal Authority of the Department of the Treasury to Issue Regulations Indexing Capital Gains for Inflation,” Department of Justice, September 1, 1992, https://www.justice.gov/file/20536/download.

[11] See Hemel and Kamin for full citations of cases referenced.

More from the Authors