JCT Estimates: Amended Senate Tax Bill Skewed to Top, Hurts Many Low- and Middle-Income Americans

By 2027, every income group below $75,000 would face tax increases, on average.The amended tax bill that Senate Finance Committee Chairman Hatch released on November 14 is even more skewed to the wealthy than the bill he released on November 9,[1] estimates from the Joint Committee on Taxation (JCT) show, and its tilt would worsen over time.[2] The original bill provided by far the largest benefits to high-income people, and many middle- and lower-income households would end up worse off.[3] Under the amended bill, in 2025 (when most of its provisions would be in place), high-income households would get the largest tax cuts as a share of after-tax income, on average, while households with incomes below $30,000 would on average face a tax increase. By 2027, when many of its provisions would have expired, those at the top would still get large tax cuts, but every income group below $75,000 would face tax increases, on average. Yet despite raising taxes on millions of middle- and lower-income households, the bill would add $1.5 trillion to deficits over the decade due to its large tax cuts for high-income households and corporations.

Amended Bill Sunsets Most Individual Provisions After 2025

Senator Hatch’s amendments to the bill would enable Senate Republicans to pass it with a bare majority through the process known as “reconciliation.” To meet the Senate’s reconciliation rules, however, the bill cannot raise deficits in any year after 2027. Senator Hatch’s amendment achieves this by setting most of the of the bill’s individual income tax provisions to expire after 2025. Only three parts of the bill would be permanent:

- Large net tax cuts for corporations. The bill cuts the corporate tax rate from 35 percent to 20 percent and sets an even lower rate on the U.S. taxes that multinationals would pay on their foreign profits. Other corporate provisions would raise revenues, but not enough to cover the cost.

- Repeal of the Affordable Care Act’s (ACA) individual mandate. The revised bill includes a permanent repeal of the ACA’s requirement that people get health insurance or pay a penalty. This provision would generate $53 billion in annual savings by 2027, paying for about one-third (about 4.7 percentage points) of the bill’s 15-percentage-point permanent cut in the corporate rate.[4] Repealing the individual mandate would leave 13 million more people uninsured, raise premiums for millions more, and cause uncertainty and instability in the individual health insurance market.[5]

- A slower inflation adjustment, the “chained CPI.” Another way the bill pays for its permanent corporate tax cuts is by adopting a different inflation measure — the chained Consumer Price Index (CPI) — to adjust tax brackets and other tax parameters every year. The chained CPI grows more slowly than the current inflation measure, so taxpayers across the board would pay slightly more, with the impact growing over time. [6]

The new tables from JCT, Congress’ official estimator of tax legislation, show how the bill affects households, on average, in different parts of the income distribution for 2019 and every second year thereafter until 2027. Because the JCT estimates exclude the bill’s estate tax cut and present a limited set of distributional measures, understanding them requires some analysis and adjustment. Below we explain what the JCT tables show about the impact of the bill, both in 2025 and in 2027.

This paper focuses primarily on the Senate bill’s percentage changes in households’ after-tax income, the measure that most tax experts agree is the most informative way to examine how tax proposals affect different households along the income scale.[7] That’s because what affects people’s standard of living is a change in their after-tax (“disposable”) income, and looking at changes in after-tax incomes in percentage terms allows for fair comparisons among groups with widely different average incomes. This measure (excluding the impact of estate tax changes) can be calculated directly from the estimates that JCT presents.

Senate Republicans have focused on a different measure, the percent reduction in federal taxes for different income groups, and have used it to assert that middle-class households are “big winners” under previous versions of the bill. But this metric doesn’t accurately show how much better or worse off people are under a given bill, as New York University Professor David Kamin has explained.[8]

The Bill’s Impact in 2025

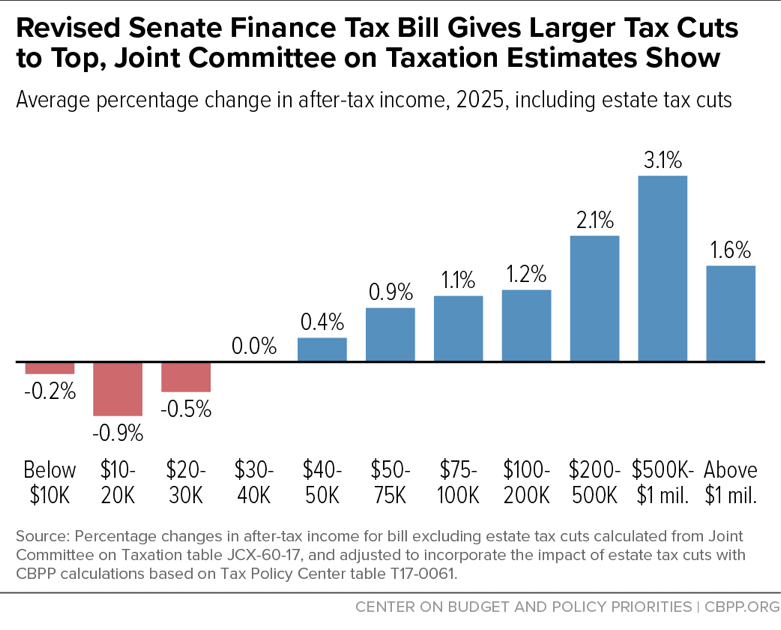

By 2025 most of the bill’s provisions would be in effect and the impact of some provisions that grow over time would be more fully apparent. Unlike the Tax Policy Center and career experts at the Treasury Department’s Office of Tax Analysis, JCT generally does not incorporate estate tax changes in its distribution estimates, so we adjust the JCT estimates to add the bill’s doubling of the estate tax exemption to $22 million per couple ($11 million per person), which would benefit only the heirs of the nation’s largest 0.2 percent of estates.[9] We estimate that in 2025, the bill would (see Figure 1 and Table 1):

- Boost the average after-tax income of households with incomes over $1 million by 1.6 percent or more than $35,000.[10]

- Give far smaller tax cuts to those toward the middle of the income distribution. Households with incomes between $40,000 and $50,000, for example, would get a percentage increase in after-tax income that is about one-fourth of what millionaires would see.

- Reduce the after-tax incomes of households with incomes below $30,000, on average, while doing virtually nothing for those with incomes between $30,000 and $40,000.

| TABLE 1 | ||||

|---|---|---|---|---|

| Senate Finance Committee Tax Bill Distribution, 2025, Including Estate Tax Cuts | ||||

| Income group | Percentage change in after-tax income (including estate) | Average tax increase (+) or cut (-) | ||

| Below $10K | -0.2% | $10 | ||

| $10-20K | -0.9% | $180 | ||

| $20-30K | -0.5% | $170 | ||

| $30-40K | 0.0% | -$10 | ||

| $40-50K | 0.4% | - $190 | ||

| $50-75K | 0.9% | -$610 | ||

| $75-100K | 1.1% | -$1,010 | ||

| $100-200K | 1.2% | -$1,680 | ||

| $200-500K | 2.1% | -$5,770 | ||

| $500K-$1 million | 3.1% | -$17,460 | ||

| More than $1 million | 1.6% | -$35,410 | ||

The bill’s large tax cuts for high-income households reflect a series of provisions that provide large benefits to the wealthy but little or nothing to everyone else. These include: corporate rate cuts, the benefits of which flow overwhelmingly to wealthy investors and CEOs; the large estate tax cut; a tax cut for “pass-through” income, or income that owners of such businesses as partnerships, S corporations, and sole proprietorships claim on their individual tax returns and that is taxed at the same rates as wages and salaries; repeal of the Alternative Minimum Tax, which is designed to ensure that the wealthiest households pay at least some minimum level of tax; and a cut in the top individual income tax rate.[11]

Households with incomes below $30,000 would face tax increases, on average, for two main reasons. First, most of the bill’s changes to the individual income tax would largely end up being a wash for this income group, on average. (For example, raising the standard deduction would lower households’ tax liability, while repealing personal exemptions would raise it.)[12] And the bill’s Child Tax Credit expansion would give only token help to millions of low- and moderate-income working families (while doing far more for higher-income families).[13]

Second, repealing the individual mandate would hurt low- and moderate-income people overall, leaving 13 million more people uninsured, raising premiums for millions more, and creating uncertainty across the health insurance market.[14] The JCT tables do not fully incorporate these harms; in particular, they do not account for increases in individual market premiums, which would affect millions of middle-income consumers, or for the decline in Medicaid coverage stemming from repeal.[15] (Awareness of the mandate is what leads some people to explore their coverage options and learn that they are eligible for Medicaid.) The JCT tables do, however, include the reductions in premium tax credits that would occur because fewer low- and moderate-income people would sign up for marketplace coverage.

Some Republicans argue that the coverage losses caused by repealing the individual mandate —and the related reductions in financial assistance for low-income households — should be ignored because these coverage losses are “voluntary” (that is, they occur because people choose to go uninsured). But this view is deeply mistaken.

Regardless of why they lose coverage, those who would become uninsured would suffer harm. People without health insurance lack access to preventive care, are less likely to receive needed care, and have worse health outcomes. They also face huge financial risks, including the possibility of medical bankruptcy if they become seriously ill and need treatment.

What’s more, many of the coverage losses that result from repealing the mandate would occur because the mandate serves an important outreach function, as noted above: it leads uninsured people who don’t realize that they’re eligible for Medicaid or marketplace subsidies to explore their options and enroll. Coverage losses that come because people never learn about programs or financial assistance for which they’re eligible aren’t “voluntary” in any meaningful sense.[16]

The Bill’s Impact in 2027

By 2027, when the bill’s sunsets would have taken effect, provisions that harm low- and moderate-income families — namely, repeal of the individual mandate and adoption of the chained CPI — would remain, and would be used to pay for corporate tax cuts, which likewise would be permanent. The JCT tables show the results (see Figure 2 and Table 2).[17]

- The highest-income groups would still get the largest tax cuts as a share of after-tax income. Millionaires, for example, would see a 0.4 percent ($8,500) increase. This is because the bill’s permanent corporate tax cuts would primarily flow to wealthy investors and highly paid CEOs and other executives.[18]

- Every income group below $75,000 would face tax increases, on average. For example, households between $40,000 and $50,000 would see a 0.6 percent ($280) decline in their after-tax incomes. Many millions more families would face a tax increase in 2027 than in 2025 due to the expiration of such provisions as the increases in the Child Tax Credit and standard deduction.[19] Further, the effect of the chained CPI would grow over time as it would fall further and further behind the tax code’s current measure of inflation.

| TABLE 2 | ||||

|---|---|---|---|---|

| Senate Finance Committee Tax Bill Distribution, 2027, Excluding Estate Tax Cuts | ||||

| Income group | Percentage change in after-tax income (excluding estate) | Average tax increase (+) or cut (-) | ||

| Below $10K | -0.3% | $20 | ||

| $10-20K | -1.5% | $310 | ||

| $20-30K | -1.0% | $360 | ||

| $30-40K | -0.6% | $290 | ||

| $40-50K | -0.6% | $280 | ||

| $50-75K | -0.1% | $140 | ||

| $75-100K | 0.0% | -$30 | ||

| $100-200K | 0.1% | -$110 | ||

| $200-500K | 0.1% | -$440 | ||

| $500K-$1 million | 0.4% | -$1,420 | ||

| More than $1 million | 0.4% | --$8,500 | ||

Finally, even these figures likely understate the degree to which the bill would leave many families worse off. Despite raising taxes on millions of Americans, the bill adds $1.5 trillion to deficits over ten years. When policymakers eventually offset the costs of these deficit-financed tax cuts, the same low- and middle-income families that see little initial benefit — or even face tax increases — from the bill would likely bear much of the burden in the form of cuts in programs on which they rely. That is, these families would likely lose more in health care, education, job training, and other services than they gain in tax cuts, while high-income households would likely remain large net winners. [20]

Appendix: Methodology

This paper presents estimates of how the Senate bill affects the after-tax income of households across the income spectrum as well as the average dollar changes in tax liability. JCT distribution tables do not explicitly present this information, but we are able to calculate these measures using the data that JCT does provide. The JCT distribution tables also exclude the effects of the bill’s proposed changes to the estate tax, and we make adjustments to include those effects.

First, we calculate percentage changes in after-tax income using the average tax rates reported by JCT. For example, JCT estimates that households with incomes over $1 million in 2027 would face a tax rate of 31.8 percent under the Senate bill, versus 32.1 percent under current law. Millionaires thus would have 68.2 percent of their income left after taxes under the bill, versus 67.9 percent under current law. The percentage change in after-tax income due to the bill can then be calculated by comparing these two estimates. For millionaires, this calculation shows that, according to JCT estimates, the Senate bill would increase after-tax incomes by 0.4 percent on average in calendar year 2027 (68.2 percent / 67.9 percent – 1 = 0.4 percent).

Second, to incorporate the impact of the estate tax for 2025, we first add estate tax liability to each income group’s taxes under current law, using JCT estimates of estate tax liability (JCX-67-15) and Tax Policy Center estimates of the distribution of this liability (TPC Tables T17-0057 and T17-0061). (We adjust JCT’s fiscal year estimates into calendar-year equivalents because the distribution numbers are reported in calendar years.) We then distribute the reduction in estate tax liability —calculated from the revenue loss from the Senate bill’s estate tax cut (JCX-59-17) — among income groups using the same method. Next, we divide these estate tax estimates for current law and the Senate proposal by each income group’s average pre-tax income to yield new average tax rates. (Pre-tax income is calculated by dividing taxes by the average tax rate under present law as provided by JCT.) We then translate that into a percentage change in after-tax income for each income group using the ratio approach, as described above.

Finally, we calculate average dollar changes in tax liability by dividing the entire tax change reported by JCT by its estimate of the number of filers in each income group. The estate tax cut as described above is included when appropriate (that is, in 2025, but not in 2027, when all of the individual provisions have expired under the bill).

We used these approaches because we felt they were the most direct methods of calculating these figures with the estimates JCT provides. Because JCT presents some of its estimates using rounded numbers, it is possible to derive slightly different results using different methods. For instance, the average tax cuts calculated using percentage change in after-tax income are similar to, but do not exactly equal, the tax cuts calculated using the aggregate tax change, though both approaches are reasonable.

End Notes

[1] U.S. Senate Finance Committee, “Hatch Unveils Pro-Growth, Pro-Jobs, Pro-Family Tax Overhaul Plan,” November 9, 2017, https://www.finance.senate.gov/chairmans-news/hatch-unveils-pro-growth-pro-jobs-pro-family-tax-overhaul-plan-.

[2] JCT, JCX-60-17, “Distributional effects of the “Tax Cuts and Jobs Act,” as ordered reported by the Senate Committee on Finance on November 16, 2017, Submitted On: November 24, 2017,” https://www.jct.gov/publications.html?func=startdown&id=5042.

[3] JCT, “Description of The Chairman’s Mark of the ‘Tax Cuts And Jobs Act,’” November 9, 2017, https://www.finance.senate.gov/imo/media/doc/11.9.17%20Chairman's%20Mark.pdf.

[4] Aviva Aron Dine, “Senate Tax Bill Would Add 13 Million to Uninsured to Pay for Tax Cuts of Nearly $100,000 Per Year for the Top 0.1 Percent,” CBPP, November 15, 2017, https://www.cbpp.org/blog/senate-tax-bill-would-add-13-million-to-uninsured-to-pay-for-tax-cuts-of-nearly-100000-per-year.

[5] Aviva Aron-Dine, “Republicans Considering Increasing Number of Uninsured by Millions, Raising Premiums to Help Pay for Tax Cuts,” CBPP, November 9, 2017, https://www.cbpp.org/research/health/republicans-considering-increasing-number-of-uninsured-by-millions-raising-premiums.

[6] TPC table T13-0105 http://www.taxpolicycenter.org/model-estimates/distributional-effects-indexing-tax-parameters-using-chained-cpi/tax-parameters-0.

[7] See Tax Policy Center, “Measuring the Distribution of Tax Changes,” http://www.taxpolicycenter.org/resources/measuring-distribution-tax-changes; “How should progressivity be measured?” http://www.taxpolicycenter.org/briefing-book/how-should-progressivity-be-measured.

[8] See David Kamin, “The Senate Bill Really is Regressive,” Medium, November 12, 2017, https://medium.com/whatever-source-derived/the-senate-bill-really-is-regressive-fe56b83b3789.

[9] Chye-Ching Huang, “Doubling Estate Tax Exemption Would Give Windfall to Heirs of Wealthiest Estates,” CBPP, November 9, 2017, https://www.cbpp.org/blog/doubling-estate-tax-exemption-would-give-windfall-to-heirs-of-wealthiest-estates.

[10] See the Appendix for the methodology used in this report.

[11] For further discussion, see Sharon Parrott, “Senate Tax Bill Has Same Basic Flaws as House Bill,” CBPP, November 14, 2017, https://www.cbpp.org/research/federal-tax/senate-tax-bill-has-same-basic-flaws-as-house-bill.

[12] JCT’s estimates of the prior version of the Senate bill (which did not include mandate repeal) showed the vast majority of filers in these income ranges facing minimal tax changes. See Chye-Ching Huang, “JCT: Senate Tax Bill Benefits Well-Off the Most, and Millions of Low- and Middle-Income People Face Tax Increases,” CBPP, November 13, 2017, https://www.cbpp.org/blog/jct-senate-tax-bill-benefits-well-off-the-most-and-millions-of-low-and-middle-income-people.

[13] Chuck Marr, “New Senate Child Credit Proposal Still Doesn’t Prioritize Families That Most Need It,” CBPP, November 15, 2017, https://www.cbpp.org/blog/new-senate-child-credit-proposal-still-doesnt-prioritize-families-that-most-need-it.

[14] Aviva Aron-Dine, “Senate Tax Bill Would Add 13 Million to Uninsured to Pay for Tax Cuts of Nearly $100,000 Per Year for the Top 0.1 Percent,” CBPP, November 15, 2017, https://www.cbpp.org/blog/senate-tax-bill-would-add-13-million-to-uninsured-to-pay-for-tax-cuts-of-nearly-100000-per-year.

[15] CBO has issued an analysis of how the tax bill affects federal spending such as Medicaid. For an analysis of the JCT and CBO estimates together, see Chye-Ching Huang, “CBO and JCT Estimates Show Senate Bill Skewed to Top, Harmful to Low- and Middle-Income Americans,” CBPP, November 18, 2017, https://www.cbpp.org/blog/cbo-and-jct-estimates-show-senate-bill-skewed-to-top-harmful-to-low-and-middle-income-americans. The CBO estimates do not, however, include the impact of increases in individual market premiums.

[16] Aviva Aron-Dine, “Yes, the Massive Coverage Losses From Repealing the Individual Mandate Would Be Harmful,” CBPP, November 16, 2017, https://www.cbpp.org/blog/yes-the-massive-coverage-losses-from-repealing-the-individual-mandate-would-be-harmful.

[17] The bill’s cuts to the estate tax expire at the end of 2025, along with the bulk of the individual income tax provisions, so the 2027 effects are calculated directly from the JCT tables without an adjustment for the estate tax.

[18] Chye-Ching Huang and Brandon DeBot, “Corporate Tax Cuts Skew to Shareholders and CEOs, Not Workers as Administration Claims,” CBPP, August 16, 2017, https://www.cbpp.org/research/federal-tax/corporate-tax-cuts-skew-to-shareholders-and-ceos-not-workers-as-administration.

[19] Even if lawmakers made these provisions permanent, the added benefits for many low- and moderate-income families would not be large enough to outweigh the harm they would suffer from the mandate repeal and a chained CPI, along with other individual tax provisions such as the repeal of personal exemptions.

[20] CBPP, “Budget Briefs: The Republican Two-Step Fiscal Agenda,” https://www.cbpp.org/budget-briefs-the-republican-two-step-fiscal-agenda

More from the Authors

Areas of Expertise