Joint Committee on Taxation Distribution Tables Confirm Skewed Priorities of House Tax Bill

The Joint Committee on Taxation (JCT), Congress’ official estimator of tax legislation, has released an estimate of how the tax bill proposed by House Ways and Means Committee Chairman Kevin Brady would change revenues at different income levels across the distribution.[1] Because the JCT estimates exclude the bill’s proposed cuts to the estate tax and present a limited set of distributional measures, understanding them requires some analysis and adjustment. But the estimates show that the tax cuts proposed in the House bill are overwhelmingly skewed to the top. They also show that some income groups, including some moderate-income households, would see tax increases (on average) in some years, in a bill that cuts taxes overall by $1.5 trillion over a decade.

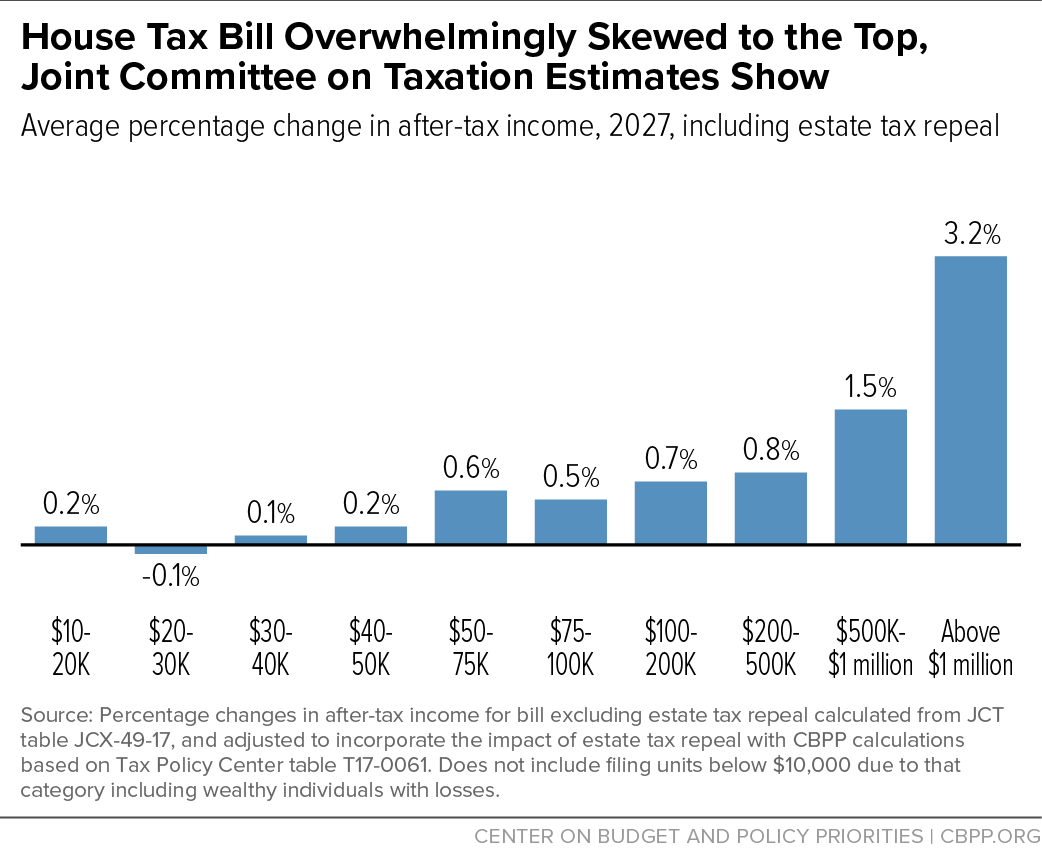

The Tax Cuts in the House Bill Are Overwhelmingly Skewed to the Top

Households with annual incomes over $1 million would see their after-tax incomes increase by 3.2 percent, 16 times the percentage increase for any income group in the bottom half of the income distribution.Based on the JCT distribution tables, adjusted to incorporate the effects of repealing the estate tax, we estimate that in 2027:

- Households with annual incomes over $1 million would see their after-tax incomes increase by 3.2 percent, 16 times the percentage increase for any income group in the bottom half of the income distribution. (See Figure 1.) (The disparity in average tax cuts measured in dollars would be even larger.)

- About 45 percent of cost of the bill’s tax cuts would go to households with incomes above $500,000 (fewer than 1 percent of filers). About 38 percent of the bill’s cost would go to tax cuts for households with incomes over $1 million (about 3 out of every 1,000 filers).[2]

These estimates focus on 2027, the year for which the JCT tables are most informative because 2027 best reflects the distribution of the plan once in full effect. For example, the plan uses the “chained” Consumer Price Index (CPI), a slower-growing measure of inflation, to index tax brackets and other provisions of the tax code, and the effects of this provision would grow over time. Likewise, by 2027, the plan’s temporary family tax credit would have expired, and the impact of its one-time tax on multinationals’ foreign profits would have faded.[3]

As noted, our estimates also adjust the JCT estimates to add in the effects of repealing the estate tax. The House bill would cut, and then in 2023 repeal, the estate tax. This is one of the tax plan’s most regressive aspects, delivering a tax cut windfall to the heirs of the wealthiest 0.2 percent of estates in the country, worth an average of $3 million per estate by 2027.[4] Those tax cuts don’t appear in the JCT distribution tables, because JCT’s standard approach does not incorporate estate tax changes in its distribution estimates. In contrast, other analysts, such as the Tax Policy Center (TPC) and career experts at the Treasury Office of Tax Analysis, do include the effect of estate tax changes when assessing the distribution of tax proposals. In order to present the full effect of the House bill in 2027, therefore, the estimates we present above adjust the JCT estimates to incorporate the bill’s proposed repeal of the estate tax, using TPC estimates of the distribution of the estate tax.[5]

The Bill Would Raise Taxes on Many Individuals

The House and Senate adopted a budget resolution that allows them to add $1.5 trillion in tax cuts to the deficit over ten years. Overall, Chairman Brady’s bill includes tax cuts that are close to that total. Yet the JCT distribution tables show that the bill does not provide tax cuts to every income group in every year over the decade.

Specifically, the JCT estimates of the individual and business provisions show tax increases for: filers with incomes between $20,000 and $40,000 from 2023 to 2025; filers with incomes between $20,000 and $30,000 in 2027; and filers with incomes between $200,000 and $1 million in 2023.[6] (JCT also presents the effects of the individual and business provisions separately. These tables show that the business tax provisions would increase taxes for all income groups in 2023, while individual income taxes would increase for filers with incomes between $20,000 and $40,000 in 2023 and each year after; and for filers with incomes between $200,000 and $500,000 in 2023 and each year after.) These tax increases would likely be due to:

- Letting a key individual income tax provision expire in 2023. The bill would repeal (immediately and permanently) personal exemptions, and increase the 10 percent tax rate to 12 percent for many households. To protect households from the increased taxes they would otherwise face largely due to these provisions, the bill includes a $300 credit that could be claimed for each non-child dependent. But this provision would expire after 2023 — so many families would then face tax increases.

- Moving to the chained CPI. As mentioned above, the bill adopts the chained CPI to adjust tax brackets and other key elements of the tax code. The chained CPI grows more slowly than the inflation measure used under current law, and, over time, would increase taxes roughly proportionately across the income distribution. The effect of this provision would take time to accumulate.

- Timing shifts and expiring business tax provisions. The business tax provisions include one-time revenue raisers (such as a one-time tax on multinationals’ foreign profits), provisions that the bill would sunset (“full expensing”), and other new provisions in the bill whose impact on revenues would not be steady over time. [7] (This time pattern likely explains why JCT estimates that businesses taxes would rise in 2023 across all income groups: on net, the 2023 calendar year would be the least favorable for businesses overall, but after that, the business tax cuts would start to grow again.)

It is also critical to note that the JCT tables show only the average impacts across each income category. Within each income group, there will be filers facing tax cuts and tax increases — depending on households’ family structure, sources of income, and deductions. The averages mask these potentially very large differences within income groups. Eventual TPC estimates of the bill will, if they follow their typical approach, show the number of filers in each income category facing tax cuts and tax increases, and the average tax cut within each category.

What’s already clear from the JCT tables, however, is that the tax increases that some filers face under the plan would pay for tax cuts that would be, on net, extremely skewed to the very wealthy and profitable corporations. And that’s before accounting for how these tax cuts would swell federal budget deficits.[8] By increasing deficits, tax cuts would create pressure to cut programs that primarily benefit low- and middle-income families, making their true distributional impacts even more skewed than the JCT tables show.[9]

End Notes

[1] JCT, “Distribution Effects Of The Chairman’s Amendment In The Nature Of A Substitute To H.R.1, The “Tax Cuts And Jobs Act,” JCX-49-17, November 3, 2017, https://www.jct.gov/publications.html?func=startdown&id=5029.

[2] Note that the Tax Policy Center’s (TPC) estimates include about twice as many filers with incomes over $1 million as the JCT estimates do, because TPC uses a more comprehensive measure of income than JCT. Because of this and other methodological differences, when TPC estimates the effects of the House tax bill, it will likely show a larger share of the tax cut flowing to millionaires than JCT. For the same reasons, it is difficult to directly compare the new JCT estimates with TPC estimates of earlier GOP tax proposals, such as the Unified Framework.

[3] The chained CPI raises $0.7 billion in fiscal year 2018 but $27.8 billion by 2027. The one-off tax on foreign profits raises $65.7 billion in fiscal year 2018 but loses revenue (due to the treatment of foreign tax credits) by 2027. JCT, “Estimated Revenue Effects Of The Chairman’s Amendment In The Nature Of A Substitute To H.R. 1, The ‘Tax Cuts And Jobs Act,’ Scheduled For Markup By The Committee On Ways And Means On November 6, 2017,” JCX-47-17, November 3, 2017, https://www.jct.gov/publications.html?func=startdown&id=5027.

[4] Chye-Ching Huang, “Doubling Exemption on Estate Tax, Then Repealing It, Would Give Millions to Wealthiest Heirs,” CBPP, November 2, 2017, https://www.cbpp.org/blog/doubling-exemption-on-estate-tax-then-repealing-it-would-give-millions-to-wealthiest-heirs.

[5] JCT distribution tables do not explicitly show percentage changes in after-tax income for each income group, the measure preferred by most tax analysts for comparing how a tax plan affects filers at different income levels. But the JCT tables do give the average tax rates — under current law and under the bill — for each income group, and percentage changes in after-tax income can be calculated directly from the change in average tax rates. For example, JCT estimates that households with incomes over $1 million would face a tax rate of 32.1 percent under current law, versus 30.6 percent under the proposal. The share of their income left after taxes is 100 percent (representing before-tax income) minus the average tax rates, so 67.9 percent for millionaires under current law and 69.4 percent under the bill. The percentage change in after-tax income can then be calculated by comparing these two estimates. For millionaires, this calculation shows that, according to JCT estimates, the House bill would increase after-tax incomes by 2.2 percent on average in calendar year 2027 (69.4/67.9 – 1 = 2.2). The JCT tables also give the dollar tax cuts for each income group under the tax proposal, allowing us to calculate the share of tax cuts going to each income group.

The total tax cut going to millionaires in 2027 increases from $36.6 billion shown in the JCT table to an estimated $57.9 billion when the impact of estate tax repeal is incorporated, raising their percent increase in after-tax income from 2.2 percent to 3.2 percent. To incorporate the impact of the estate tax, we first assume that the revenue loss from estate tax repeal is $38.0 billion, JCT’s estimate of the fiscal year 2027 revenue impact (JCX-47-17). (The JCT distribution estimates are based on calendar year effects, and so this fiscal year revenue estimate is conservative, as the revenues lost from estate tax repeal are growing.) We distribute this $38 billion tax cut to each income group according to the shares of the estate tax borne by each income group for 2027 in TPC Table T17-0061. We then translate that into a percentage change in after-tax income for each income group using the ratio calculated from the JCT tables, as described above.

JCT’s tables do not provide the number of filers in each income group, so we do not calculate average dollar tax changes per filer in each income group.

[6] JCX-49-17.

[7] In particular, the bill also restricts how businesses can use certain losses to offset taxes on other profits. The tax increase from this “net operating loss” provision is biggest in fiscal year 2023, but then fades away.

[8] See, Jason Furman and Greg Leiserson, “The real cost of the Republican tax cuts,” Vox, November 1, 2017, https://www.vox.com/the-big-idea/2017/10/31/16581822/republican-tax-cuts-real-costs. For an illustration of this point using the GOP “Unified Framework,” see Chye-Ching Huang and Brendan Duke, “Vast Majority of Americans Would Likely Lose From Senate GOP’s $1.5 Trillion in Tax Cuts, Once They’re Paid For,” CBPP, October 4, 2017, https://www.cbpp.org/research/federal-tax/vast-majority-of-americans-would-likely-lose-from-senate-gops-15-trillion-in.

[9] Republican leaders have already indicated that they intend to use future legislation to make such budget cuts, perhaps as soon as a new reconciliation bill next year, and will use deficits to justify doing so. As Roll Call recently reported, it “interviewed half a dozen House Budget Committee members, as well as a few other fiscal hawks in the GOP conference, and they all said they anticipate mandatory spending cuts [i.e., cuts in entitlement programs] being a priority for the fiscal 2019 budget reconciliation process.” Lindsey McPherson, “On Debt Reduction, GOP Says Wait Till Next Year,” Roll Call, October 26, 2017, https://www.rollcall.com/news/politics/on-debt-reduction-republicans-say-wait-till-next-year.

More from the Authors