Republican Leaders’ Tax Framework Provides Windfall to High-Income Households, With Working Families Largely an Afterthought

The “Big Six” Republican tax framework announced last week by President Trump and Republican leaders in Congress specifies large tax cuts aimed at profitable corporations and wealthy households while offering only vague promises for lower- and middle-income working families. It closely follows many aspects of the House GOP’s “Better Way” plan released last year, which was heavily tilted to those high on the income scale. Like that plan, the new framework offers little for working families with modest incomes compared to what it would do for those at the top.

The framework contrasts sharply with President Trump’s campaign statements that “too many of our leaders have forgotten that it’s their duty to protect the jobs, wages and well-being of American workers before any other consideration,” and his promise less than two weeks ago that wealthy people “will not be gaining at all with this plan.”[1]

The Tax Policy Center (TPC) estimates of the Trump and congressional Republican framework show that in 2027 (when key features of the plan are in full effect):[2]

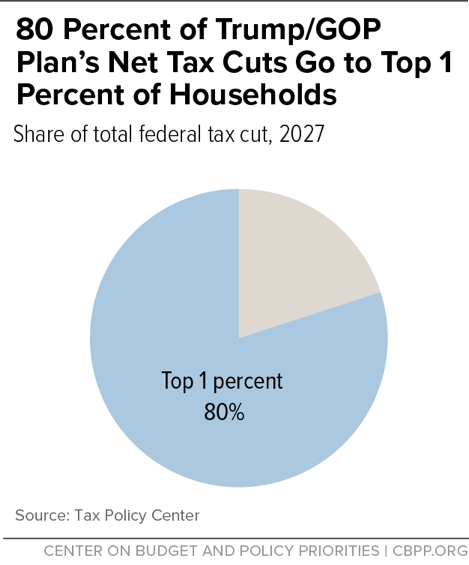

- The top 1 percent of households would get roughly 80 percent of the framework’s net tax cuts.The top 1 percent of households (those with incomes above $912,100) would get 80 percent of the framework’s net tax cuts (see Figure 1), or more than $200,000 annually (an 8.7 percent boost in after-tax income), on average.

- The top 0.1 percent of households (those with incomes above $5.1 million) would get 40 percent of the framework’s net tax cuts, or more than $1 million annually (a 9.7 percent boost in after-tax income), on average.

- Meanwhile, the bottom 80 percent of the population would get less just 13 percent of the tax cuts and see a less than 0.5 percent increase in after-tax income, on average.

Framework Closely Resembles Regressive “Better Way” Plan

The Republican leaders’ framework shares core elements with the Better Way plan, including: cutting the corporate rate to 20 percent; setting a special, 25 percent rate for “pass-through” business income; eliminating the estate tax and Alternative Minimum Tax (AMT); eliminating the deduction for state and local tax payments; increasing the standard deduction; eliminating personal exemptions; and raising the Child Tax Credit for some families. Its proposed marginal income tax rates of 12, 25, and 35 percent are very similar to the Better Way’s 12, 25, and 33 percent structure. And its promised reductions of tax breaks and base broadeners — relying heavily on repealing the deduction for state and local taxes — are also similar.

High-Income Households Would Receive Large Benefits

The specific provisions of the Republican leaders’ framework that would most benefit high-income households include:

- Reducing the top individual income tax rate to 35 percent. The framework’s cut in the top individual income tax rate from 39.6 percent to 35 percent would benefit the fewer than 1 in 100 households that currently face the top rate. By itself, the rate cut would give a $24,000 tax cut each year for a couple with $1 million in taxable income. The framework states that an “additional top rate may apply to the highest-income taxpayers to ensure that the reformed tax code is at least as progressive as the existing tax code.” But even if the very wealthiest people continued to pay the 39.6 percent rate, they still would benefit handsomely from the other provisions in this framework, discussed below.

- Setting a special, much lower top rate of 25 percent for “pass-through” income. This is income from businesses such as partnerships, S corporations, and sole proprietorships that business owners claim on their individual tax returns. It is now taxed at the same rates as wages and salaries. (Pass-through businesses, which include hedge funds, real estate developers, and law firms, are exempt from the corporate income tax and from taxes on dividends, so they often face lower total taxes than corporations.) TPC finds that 79 percent of the benefit of this tax cut would flow to filers with incomes above $1 million. And we estimate that the 400 households with the highest incomes would receive an average tax cut of $5.5 million from this provision alone.[3]

- Repealing the estate tax. Because only the wealthiest 0.2 percent of estates pay this tax at all, only the heirs of these estates would benefit from its repeal. The first $5.49 million of an estate’s value (effectively $11 million for a couple) already is entirely exempt from the tax.

- Cutting the corporate rate to 20 percent (from 35 percent). Mainstream economic estimates conclude that the bulk of the benefit from cutting corporate tax rates goes to investors and CEOs, not rank-and-file workers.[4]

- Eliminating the Alternative Minimum Tax. This tax is designed to ensure that higher-income people who take large amounts of deductions and other tax breaks pay a minimum level of tax.

In total, TPC estimates that the 1 percent of households would receive about 80 percent of the framework’s net tax cuts in 2027, or more than $200,000 annually (an 8.7 percent boost in after-tax income), and that the top 0.1 percent of households would receive roughly 40 percent of the framework’s net tax cuts, or more than $1 million annually (a 9.7 percent boost in after-tax income).[5]

Little Discernible Benefit for Struggling Working Families

The Republican leaders’ framework adjusts numerous individual income tax provisions, but the end result would likely be close to a wash for many low- and middle-income families. The document’s rhetoric focuses on changes benefiting these households, such as the proposed increases in the standard deduction and Child Tax Credit. In many cases, however, these benefits are offset by other provisions in the framework, such as the elimination of personal exemptions and the increase in the bottom marginal rate from 10 percent to 12 percent for some filers.

The framework is missing important details, such as the amount of the increase in the maximum Child Tax Credit. But the framework does indicate that amounts above $1,000 per child would not be refundable, which also was the case under the Better Way plan. If the framework follows the Better Way plan here, a broad swath of low- and middle-income working families likely would see little overall benefit. For example, assuming an increase in the maximum Child Tax Credit of $500, to $1,500 per child (as the Better Way plan did), then:[6]

- A married couple with one child claiming the standard deduction would get no tax cut if they earn $24,850 or below.[7]

- A married couple with one child earning $48,700 (the median income in 2015 for a working-class family of that size[8]) and claiming the standard deduction would get a net tax cut of just $180.[9]

Making the same assumptions, TPC estimates that overall, the plan would deliver only 13 percent of its tax cuts to the bottom 80 percent of households, and those households’ after-tax incomes would rise by less than half a percent, on average (compared to the roughly 10 percent boost in income that those in the top 0.1 percent would enjoy).

While the framework states that “the committees will work on additional measures to meaningfully reduce the tax burden on the middle-class,” the document suggests that’s more of an afterthought than a central theme of the plan. It stands in contrast to the quite specific proposals that would deliver a windfall for the nation’s wealthiest people.

End Notes

[1] Steve Holland and David Morgan, “Trump says rich might pay more in taxes, talks with Democrats,” Reuters, September 13, 2017, https://www.reuters.com/article/us-usa-tax/trump-says-rich-might-pay-more-in-taxes-talks-with-democrats-idUSKCN1BO1HM and Tessa Berenson, “Read Donald Trump’s Speech on Jobs and the Economy,” Time, September 15, 2016, http://time.com/4495507/donald-trump-economy-speech-transcript/.

[2] Tax Policy Center, “A Preliminary Analysis of the Unified Framework,” September 28, 2017, http://www.taxpolicycenter.org/publications/preliminary-analysis-unified-framework.

[3] For details on the calculation, see: Chuck Marr et al., “Will New Trump Tax Plan Include Pass-Through Tax Break for Wealthiest?” Center on Budget and Policy Priorities, February 27, 2017, https://www.cbpp.org/research/federal-tax/will-new-trump-tax-plan-include-pass-through-tax-break-for-wealthiest.

[4] See Chye-Ching Huang and Brandon DeBot, “Corporate Tax Cuts Skew to Shareholders and CEOs, Not Workers as Administration Claims,” Center on Budget and Policy Priorities, updated August 16, 2017, https://www.cbpp.org/research/federal-tax/corporate-tax-cuts-skew-to-shareholders-and-ceos-not-workers-as-administration.

[5] Note: an earlier version of this paper included our preliminary rough estimates based on older TPC analyses that in 2017, the top 1 percent would get about 50 percent of the net tax cuts (worth about $150,000 on average) and that the top 0.1 percent would get about 30 percent of the tax cut (worth about $800,000 on average). The TPC estimates for 2027 are more tilted to the top in part because they take into account the effect of the Big Six proposal to adjust inflation measures in the tax code, which has a larger effect in later years. For 2017, TPC’s estimates are similar to our initial estimates, and show that the top 1 percent would get 53.3 percent of the tax cuts, worth $723,000 on average; and the top 0.1 percent would get 30.3 percent of the tax cuts, worth $129,000 on average.

[6] These calculations also assume the Big Six framework uses the same income thresholds for its tax brackets as the Better Way plan.

[7] These families do not earn enough to owe any federal income taxes, before factoring in tax credits, and so could not benefit from increasing the standard deduction or from expanding the Child Tax Credit without increasing the amount of the credit that can be received as a tax refund.

[8] Chuck Marr, Brandon DeBot, and Emily Horton, “How Tax Reform Can Raise Working-Class Incomes,” Center on Budget and Policy Priorities, September 13, 2017, https://www.cbpp.org/research/federal-tax/how-tax-reform-can-raise-working-class-incomes.

[9] This couple’s standard deduction would rise from $12,700 to $24,000, and its Child Tax Credit would increase from $1,000 to $1,500, but the plan’s other changes (such as the elimination of personal exemptions and the increase in the bottom marginal rate from 10 percent to 12 percent) would offset most of the tax benefit of these changes.

More from the Authors