BEYOND THE NUMBERS

Trump’s Pass-Through Proposal: New Figures on High-End Tax Cuts

Millionaires would get average tax cuts of $114,000 in 2018 from a plan — very similar to what President Trump has proposed — to let the owners of “pass-through” such as partnerships, S corporations, and sole proprietorships pay only a maximum 15 percent rate on their business income, according to new estimates from the Tax Policy Center (TPC).

TPC estimates this proposal would cost some $1.9 trillion in lost federal revenue over the next decade — from the rate cut itself as well as the new tax avoidance opportunities that it would open for high-income individuals.

President Trump and House Speaker Paul Ryan (in his “Better Way” tax plan) both proposed a special, much lower top rate for such “pass-through” income, which these business owners claim on their individual tax returns and on which they currently pay tax at the rates that apply to wages and salaries. We’ve explained that these tax cuts would mainly benefit the high-income investors who receive the bulk of pass-through income. The new TPC estimates show just how regressive a special pass-through rate would be.

TPC analyzed the cost and distribution of several possible pass-through tax cuts, including one that’s very similar to the Trump plan: a 15 percent pass-through rate and assuming a top individual income tax rate of 33 percent. President Trump has proposed a 15 percent pass-through rate and a top individual income tax rate of 35 percent.

The estimates show:

- More than two-thirds of the tax cut would flow to millionaires. (See first chart.) Households with incomes above $1 million would receive a $114,000 average tax cut from just this provision, boosting their after-tax income by more than 5 percent in 2018.

Benefiting the most would be wealthy people including hedge fund managers, lawyers, consultants, and investment managers, who comprise the majority of pass-through business owners in the top tax bracket. President Trump himself owns about 500 pass-throughs, according to his lawyers, which is why some have called this tax break the “Trump loophole.”

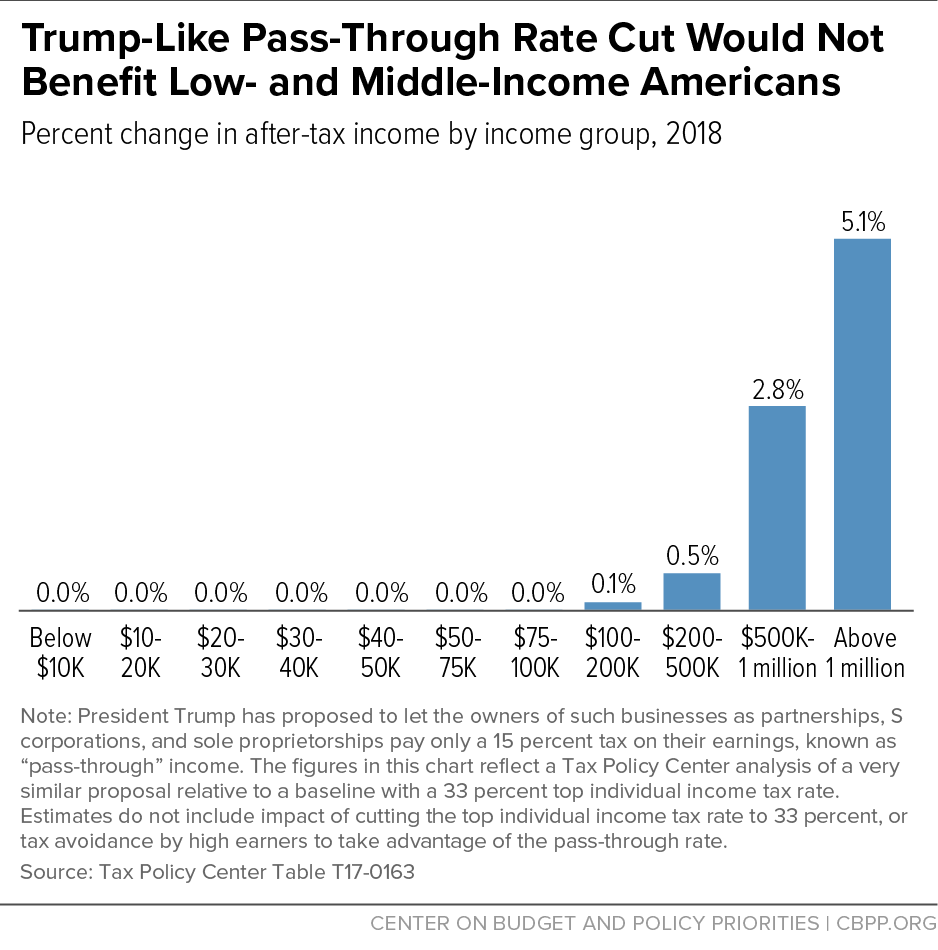

- The pass-through rate cut won’t help many “Mom-and-Pop” small businesses. Most small businesses are, in fact, small and, therefore, their owners don’t make as much as wealthy investors or face top tax rates. Roughly 70 percent of taxpayers who now have pass-through income already pay a top rate of 15 percent or less on such income, so they wouldn’t receive any benefit from a new 15 percent pass-through rate. Indeed, the TPC estimates show that the impact on low- and middle-income owners of pass-throughs is basically zero. (See second chart.) Only about 2 percent of households with incomes below $100,000 would get any tax cut, while about 58 percent of millionaires would — and their tax cuts would be much bigger.

- The proposal invites massive tax avoidance and is fiscally reckless. Reducing the tax rate on pass-through income to 15 percent would cost about $1.4 trillion in lost federal revenues over the next decade. But the total revenue loss would far exceed that level.

That's because a new 15 percent rate would invite massive tax avoidance. High-income people would have a powerful incentive to re-characterize their wage income as pass-through income, so that they could pay a 15 percent tax on it rather than their much higher top individual tax rate. The President has not proposed any rules to prevent tax avoidance, and experts are highly skeptical that any rules would be effective. This new tax avoidance would cost another $584 billion in lost revenue, or about 30 percent of the total $1.9 trillion revenue loss, TPC estimates.

The distribution of this additional revenue loss is not reflected in the charts above, but the entire $584 billion would go to high earners — meaning that the revenue loss from tax avoidance alone would exceed the total tax cuts on actual business income for the bottom 99 percent of Americans.

Finally, TPC’s estimates understate the federal revenue loss as well as the tax benefits for those at the top in two other important ways. First, the TPC estimates don’t reflect the large tax benefits that high-income taxpayers — including taxpayers with pass-through income — would get from Trump’s proposal to cut the top individual income tax rate to 35 percent, from the current 39.6 percent. Second, the gap between Trump’s top tax rate of 35 percent and the 15 percent pass-through rate is larger than the top tax rate of 33 percent that TPC assumed.