BEYOND THE NUMBERS

More States Protecting Residents Against Skimpy Short-Term Health Plans

Since the Trump Administration issued new rules last year expanding short-term health plans, which are exempt from the Affordable Care Act’s (ACA) protections for people with pre-existing conditions and benefit standards, nearly a dozen states have set their own limits and consumer protections for short-term plans. Others should follow suit.

The new federal rules define short-term plans as those lasting less than a year, up from three months under the previous (2016) rules, and let insurers renew them. This lets a parallel market for skimpy plans operate alongside the market for comprehensive individual health insurance, exposing consumers to new risks and raising premiums for those seeking comprehensive coverage — especially middle-income consumers with pre-existing conditions.

The rules took effect in early October, just before the November 1 start of the ACA’s open enrollment period, creating confusion for consumers because they had limited time to sign up for comprehensive 2019 ACA plans and were subjected to heavy marketing from companies selling short-term plans as an alternative.

Short-term plans don’t have to cover all of the ACA’s essential health benefits, and they often don’t cover such essential benefits as maternity and mental health care, substance-use disorder treatment, and prescription drugs. Also, they can deny coverage or charge higher prices to people with pre-existing conditions, and they typically don’t cover medical services related to a pre-existing condition.

Short-term plans can offer healthier people lower premiums (because they include fewer benefits and cover less costly populations), so they will lure healthy enrollees away from the individual and small-group markets, leaving a less healthy and thus costlier group behind. This dynamic, known as adverse selection, will likely raise premiums for traditional, more comprehensive health coverage and undermine ACA protections for people with pre-existing conditions. Meanwhile, healthy people who enroll in short-term plans may face gaps in coverage and catastrophic costs if they get sick and need care.

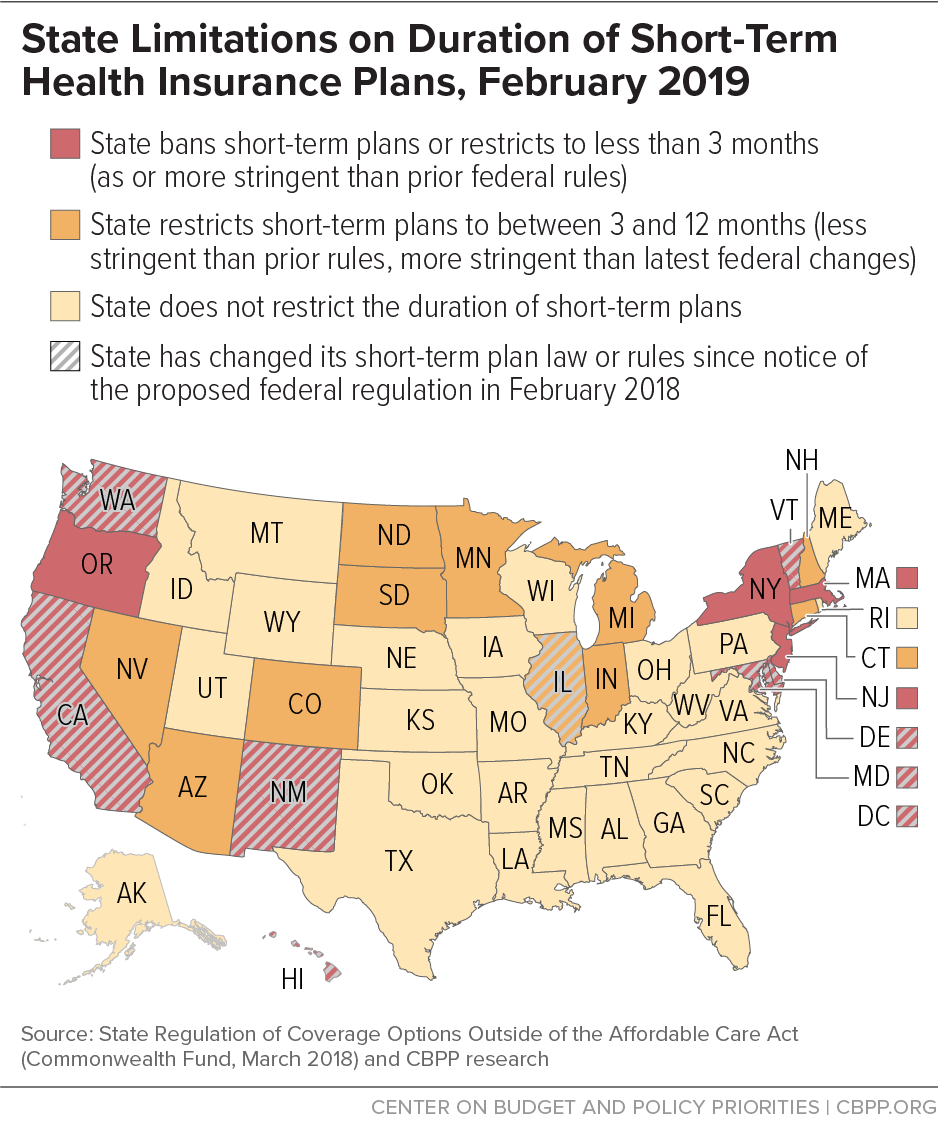

Fortunately, states can set their own standards for short-term plans, and a number of states have acted since the new federal rules came out:

- California banned short-term plans, barring health insurers from issuing, selling, or renewing them within the state.

- Colorado, which already limited short-term plans to six months, issued rules requiring them to be available to consumers regardless of their medical history, to limit their age-related premium differences so that the oldest adults pay no more than three times what younger adults pay, and to cover the ACA’s essential health benefits, among other changes.

- Delaware issued rules limiting short-term plans to three months, with no extensions or renewals, and requiring them to spend at least 60 percent of consumers’ premium payments on medical care.

- The District of Columbia passed legislation limiting short-term plans to three months, restricting insurers from excluding coverage of pre-existing conditions, and barring insurers from selling the plans to someone who had a short-term plan within the prior nine months.

- Hawaii lawmakers passed, and Democratic Governor David Ige signed, a bill prohibiting insurers from issuing a short-term plan to someone who was eligible to buy coverage through the ACA marketplace during an open or special enrollment period the prior year. It also limits short-term plans to less than 91 days and prohibits extensions or renewals.

- Illinois lawmakers enacted legislation, on a bipartisan basis and overriding then-Governor Bruce Rauner’s veto, to limit short-term plans to six months, restrict extensions and renewals, and require warning language for consumers.

- Maryland lawmakers passed, and Republican Governor Larry Hogan signed, a law limiting short-term plans to less than three months and prohibiting extensions or renewals of short-term plans.

- New Mexico issued rules defining short-term plans as nonrenewable and lasting no more than three months.

- Vermont lawmakers passed, and Republican Governor Phil Scott signed, a law limiting short-term plans to three months, prohibiting renewals and extensions, and establishing minimum financial, marketing, and other standards for the plans.

- Washington State adopted rules limiting short-term plans to three months, with no renewals, and setting requirements about the information consumers must receive about the plans’ coverage limitations.

Massachusetts, New Jersey, and New York already effectively prohibited short-term plans, and Oregon limits short-term plans to three months and restricts renewals.

Several other states have protections that may mitigate the effects of the federal rule changes. (See map.) Yet most states lack sufficient protections against potential adverse selection due to those federal changes (as well as federal changes promoting association health plans, as we explain here). And some states are moving in the wrong direction: Indiana lawmakers, for example, are considering rolling back the state’s six-month limit on short-term plans.

Despite Administration efforts to undercut the ACA, states retain broad authority to protect consumers and create a level playing field for insurers in their individual and small-group markets — and insurers, patient groups, and consumer advocates have urged them to exercise it. Other states that haven’t yet acted should do so.