|

Revised June 13, 2006

NEW JOINT TAX COMMITTEE ESTIMATES SHOW MODIFIED

KYL PROPOSAL STILL VERY COSTLY:

True Cost Partially Masked

By Joel Friedman and Aviva Aron-Dine

On June 8, the Senate rejected, by a vote of

57-41, a motion to consider permanent repeal of the estate tax (under Senate

rules, the measure required 60 votes to pass). During the lead-up to the

vote, Senator Jon Kyl floated a modification of his longstanding “compromise”

proposal to repeal most but not quite all of the estate tax. His hope,

apparently, was to persuade a sufficient number of Senators who oppose repeal

that his proposal could now serve as a reasonable compromise solution.

But new Joint Committee on Taxation estimates

(which are attached) indicate that Senator Kyl’s modified proposal differs

little in cost from the original version.

- The new variant of the Kyl proposal costs

nearly as much as the earlier Kyl proposal — and about three-quarters as much

as full repeal over the long term.

- Moreover, the new Joint Tax Committee

estimate understates the cost of the estate tax policy that Senator Kyl

actually seeks to implement, because what amounts to a gimmick in the design

of the plan compels the Joint Tax Committee to make an assumption that lowers

the cost estimate.

- Taking this into account, the new variant of

the Kyl proposal would likely cost about 80 percent as much as full repeal —

or about $800 billion over the first ten years in which its budgetary effects

would be fully felt (2012-2021), including the costs of the increased interest

payments that would have to be made on the national debt.

Modified Proposal Little Different than Original

Senator Kyl is a staunch advocate of

estate-tax repeal, but has recently acknowledged that repeal supporters “do not

have the votes” in the Senate for permanent repeal and that their “position is

eroding,” as was confirmed by this week’s vote.

Given this situation, he has for several months been promoting a “compromise”

position: an estate tax with a $5 million exemption ($10 million per

couple) and a 15 percent rate. According to Joint Committee on Taxation

estimates, this proposal would cost 84 percent as much as repeal. Over the

2012-2021 period, the first decade in which the proposal’s costs are fully

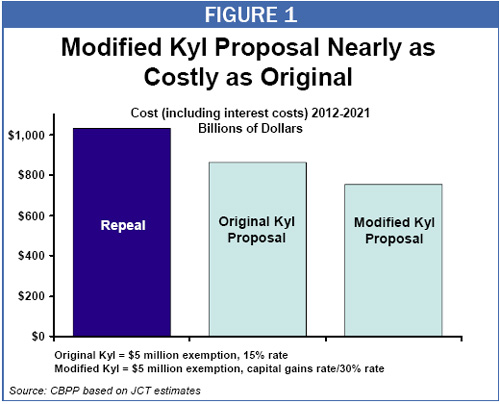

reflected in the estimates, it would reduce revenues by about $680 billion.

Because Senator Kyl has not proposed to offset these revenue losses, they will

result in higher deficits and debt, generating $180 billion in higher interest

costs over the period for a total ten-year cost of $860 billion.

Due to the proposal’s high cost, most have

recognized it as little different than repeal.

In an attempt to generate more support for his proposal and to portray it as a

reasonable compromise, Senator Kyl has suggested several modifications. The new

version of the proposal calls for an estate tax with a $5 million ($10 million

per couple) exemption, indexed for inflation, and a rate linked to the capital

gains rate — now 15 percent — for the taxable value of an estate up to $30

million. The proposal would then apply a rate of 30 percent to the taxable

value of an estate above $30 million. It also would eliminate the deduction for

state estate taxes paid, thereby raising a small amount of additional revenue at

the expense of states.

The Joint Committee on Taxation estimates

show that with these changes, Senator Kyl’s proposal would lose $60 billion in

revenue in 2016, or 74 percent of the revenue that the Joint Tax Committee

projects would be lost by estate tax repeal in that year.

The Joint Committee’s estimate similarly shows the new proposal losing 74

percent as much as full repeal over the 2012-2016 period, which constitutes the

first five-year period in which the proposal’s budgetary effects would be fully

felt. The addition of the new 30 percent tax bracket for estates over $30

million thus does little to mitigate the high cost of Senator Kyl’s original

proposal (see Figure 1).

Joint Tax Committee Estimates

Assume 20 Percent Rate,

Not 15 Percent, for Kyl

Proposal

Moreover, while this cost estimate reflects

Senator Kyl’s intended exemption level and his elimination of the state estate

tax deduction, it does not reflect the permanent 15 percent rate that Senator

Kyl seeks for the taxable value of an estate below $30 million. In

preparing its cost estimates, the Joint Committee on Taxation must assume

current law, under which the 15 percent tax rate on capital gains is slated to

revert to 20 percent at the end of 2010, one year after Senator Kyl’s proposal

would take effect.

Yet if, as the White House, the Congressional

Republican Leadership, and Senator Kyl all intend, the 15 percent capital gains

rate is extended, the cost of the new Kyl proposal would be greater than the

Joint Tax Committee estimates show. Urban Institute-Brookings Institution Tax

Policy Center estimates indicate that the cost would reach about 80 percent of

the cost of repeal over the long term, which means more than $600 billion in

revenue losses from 2012-2021, the first ten-year period in which the proposal’s

full budgetary effects would be felt.

The total cost would be about $800 billion over the 2012-2021 period once the

cost of the increased interest payments on the debt are included, as they should

be in assessing the proposal’s impact on deficits and debt. This is the period

in which the baby boomers will be retiring in large numbers and federal health

care and retirement costs will rise.

End Notes:

Susan Cornwell, “Republican Says Compromise Likely on Estate Tax,” Reuters,

May 2, 2006.

For a discussion of the original Kyl proposal, see Joel Friedman, “Estate

Tax “Compromise” With 15 Percent Rate Is Little Different Than Permanent

Repeal,” Center on Budget and Policy Priorities, June 2, 2006.

Elizabeth McNichol, “Estate Tax ‘Compromise’ Proposals May Endanger State

Estate and Inheritance Taxes,” Center on Budget and Policy Priorities, June

8, 2006.

According to the most recent Joint Tax Committee estimates (see Appendix),

Senator Kyl’s proposal would cost $275 billion from 2007-2016, some 71

percent of the $387 billion cost of full repeal over this period. (This new

estimate of the cost of repeal is slightly higher than the previous Joint

Tax Committee estimate from earlier this year.) From 2012-2016 — the years

that reflect the ongoing long-term cost of the proposal — the cost is 74

percent of full repeal. The 74 percent figure is the relevant one, since

2012-2016 are the relevant years for the cost comparison.

The years before

2012 are not relevant for assessing the ongoing fiscal impact of the

proposal. Under the Kyl plan, current law would remain unchanged in the

years through 2009. And in 2010, the new Kyl proposal would take effect in

place of repeal, which otherwise would occur for one year sunder current

law. As a result, the revenue loss relative to current law in 2010 and

2011, the years in which the one-year repeal would reduce estate tax

revenues, would be limited. The cost of the new Kyl proposal, relative to

the cost of extending repeal, is anomalously low in the years before 2012

for this reason. The long-term budgetary effect of the proposal first shows

up in 2012.

The Tax Policy Center estimated the cost of Senator Kyl’s new proposal,

assuming that the 15 percent rate would remain in effect, and found it would

cost 96 percent as much as much as the original Kyl proposal. As explained

above, the Joint Committee on Taxation’s estimates show the original

proposal would cost 84 percent as much as repeal, which implies that the

modified proposal would still cost around 80 percent of repeal.

|