HOUSE

BUDGET COMMITTEE PROCESS PROPOSAL WOULD NOT RESTRAIN THOSE

AREAS OF THE BUDGET THAT HAVE CONTRIBUTED MOST TO THE DEFICITS

By

|

PDF of report |

|

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Budget process legislation that the House Budget

Committee approved March 17 fails to address those areas of the budget that

have contributed most to the return of deficits in the past few years. The

legislation purports to resurrect the

In addition, like the budget process legislation of the 1990s, the bill that the Budget Committee approved would allow emergency spending to be exempt from its discretionary spending caps. The bill also specifically excludes from the spending caps the cost in 2005 of supplemental funds for “contingency operations related to the global war on terrorism.”

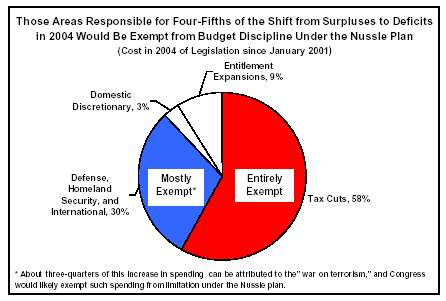

Since 2001, Congress has enacted costly tax cuts and major increases in defense, homeland security, and international affairs spending. As the Figure shows, the cost of these two types of legislation constitutes the vast majority of all costs in 2004 that result from legislation enacted in the last three years. Given the exclusions from budget enforcement in the Budget Committee bill for tax cuts and emergency and “war-on-terrorism” costs, it appears that the budget areas that are responsible for about four-fifths of the shift from surpluses to deficits in 2004 would be largely or entirely exempt from budget discipline.

- Under the budget rules in effect during the 1990s, the costs of tax cuts and entitlement expansions had to be offset fully. The new legislation, by contrast, completely exempts tax cuts from any restraint. This includes the cost of any new tax cuts as well as the cost of extending the 2001 and 2003 tax cuts (which alone would cost $1.3 trillion, including interest, over the next ten years). Unlike entitlement expansions, tax cuts would not have to be paid for.

- The Budget Committee’s bill also reestablishes caps on discretionary spending, but spending designated as being for the “the war on terror” would likely be exempt from the caps.[1]

- According to Congressional Budget Office estimates, the cost in 2004 of legislation enacted since the start of 2001 equals about $500 billion, which is about the size of the deficit this year. CBO estimates show that tax cuts account for 58 percent of this cost, or well over half of it. As noted, the Budget Committee exempts tax cuts from any limitation.

- Increases in national security spending — for defense, homeland security, and international aid — account for another 30 percent of the cost in 2004 of legislation enacted since January 2001. About three-quarters of the spending increases for national security are directly related to funding the “war on terrorism.” Such costs would likely be excluded from the spending caps in the new bill.[2]

- Thus, if the Budget Committee’s bill had been in place over the last three years, approximately four-fifths of all actions Congress took since 2001 that have added $500 billion to the 2004 deficit would have been exempt from fiscal discipline.

- Entitlement increases enacted since the start of 2001 account for only nine percent of the cost of legislation in 2004. Increases in spending for domestic discretionary programs outside homeland security account for another three percent. The cost of the tax cuts this year is nearly five times the cost of the increases in entitlement and domestic discretionary spending enacted since 2001.

-

A similar result holds if one examines the cost over a

ten-year period of the legislation enacted since the start of 2001.

Assuming the tax cuts are extended as the Bush Administration and House

Budget Committee Chairman Jim Nussle have proposed, the cost of the tax cuts

over the ten years from 2002 to 2011 will be about four times the cost over

this period of the increases in entitlement and domestic discretionary

programs outside homeland security enacted since 2001, including the

prescription drug benefit. (This calculation assumes, as virtually all

observers expect, that relief from the Alternative Minimum

The House Budget Committee’s budget process bill essentially diverts attention from the largest contributors to the reemergence of today’s deficits — the tax cuts and the “war on terrorism.” The bill focuses instead on entitlement and domestic discretionary programs outside homeland security, areas that have played a smaller role in the shift from surpluses to deficits. While exempting unforeseen costs of the “war on terrorism” from budget enforcement is legitimate, consistent with the long-time treatment of the cost of emergencies, exempting tax cuts from budget enforcement is not. The Budget Committee plan is thus a blow to efforts at reestablishing fiscal discipline.

Furthermore, the Budget Committee plan would likely make it more difficult to resurrect strong, effective fiscal discipline measures. The deficit reduction of the 1990s was successful in large part because it enforced budget discipline on everyone — both those who favored tax cuts and those who advocated spending increases. Each side was willing to accept the imposition of the limits — and thereby to constrain its policy priorities — knowing that the budget rules were being imposed equally on the other side. The Budget Committee plan would impose lopsided budget rules that could undercut future deficit-reduction efforts, by making it more difficult to resurrect the successful formula of the 1990s, under which pay-as-you-go requirements applied to both entitlements and taxes. Having succeeded in securing the restoration of the discretionary spending caps and the pay-as-you-go rules to entitlements without the rules also being applied to taxes, tax-cut advocates would (if this legislation is enacted) have no incentive to compromise in the years ahead and agree to the application of fiscal discipline to tax cuts as well.

End Notes:

[1] The bill specifically exempts from the discretionary caps a 2005 supplemental appropriation that would pay for “contingency operations related to the global war on terrorism.” Further funding for the “war on terrorism” after 2005 would likely be declared an “emergency” and also exempted from the discretionary caps.

[2] If the Budget Committee bill had been in force over the last three years, increases in spending for national security due to the war on terror would almost certainly have been declared an emergency and exempted from the discretionary caps, just as the 2005 supplemental would likely be exempted. For purposes of this analysis, we assume that the following legislation was enacted as a result of the terrorist attacks of September 2001 and actions that the government later took to combat terrorism and so would have been exempt: 1) the emergency supplemental appropriations enacted in the fall of 2001 and the spring and fall of 2003; 2) the $10 billion "contingent" increase in defense funding requested by the President and enacted by Congress for FY 2003; and 3) homeland security increases in 2002, 2003, and 2004. Together, these costs account for nearly three-quarters of all increases in defense, homeland security, and international affairs shown in the figure on page one. There were other increases in defense that would likely have been exempted on the grounds that they were necessary to fight the war on terror, but they are not included here in our analysis of the spending increases that would have been exempt.