The Importance Of Social Security To The Hispanic Community

Executive Summary

Social Security is of particular importance to Hispanic Americans. In fact, research demonstrates that Hispanics benefit more from the Social Security system than does the rest of the population.

Specifically, Hispanics receive higher average returns on the taxes they have paid into the system than do other workers. Hispanics also rely on Social Security for a greater share of their income in retirement.

Despite this, there has been a campaign to sell the Hispanic community on the notion that the current Social Security system is a bad deal for Hispanics and that Hispanics would be better off if part, or all, of Social Security were replaced by private accounts. An extensive body of research and data allows us to assess these claims. The research and data show that arguments being spread about Social Security being disadvantageous for Hispanics rest on serious distortions and, in fact, that the opposite is the case.

This analysis is divided into three sections. The first explores the economic and demographic characteristics that lead Hispanics, as a group, to benefit disproportionately from taxes paid into the Social Security system; it surveys major studies based on Social Security records that confirm that Hispanics fare better than other workers under Social Security. The second section explains why arguments that Hispanics would fare better under private accounts rest upon comparisons that “stack the deck” by omitting critical data and thus are not methodologically valid. The final section presents data that show the degree to which elderly Hispanics, more than the rest of the population, rely on Social Security for their retirement.

The major findings of this analysis include the following:

- On average, Hispanics have lower lifetime earnings, a higher incidence of disability, more children per family, and, by official measures, longer life expectancies than the population as a whole. Due to Social Security’s progressive benefit formula; its benefits for people with disabilities and for children of retired, disabled, or deceased workers; and its inflation-adjusted benefit that lasts as long as a retired or disabled beneficiary is alive, each of these population characteristics increases the Social Security benefits that Hispanic participants receive, relative to the amount of taxes they pay.

- Studies produced by the Government Accountability Office (GAO), economists at the Social Security Administration and the Urban Institute, and other researchers all confirm that Hispanics, in general, receive a higher average rate of return on their Social Security contributions than the rest of the population.[2] These detailed studies rely on actual Social Security records to compute how different groups fare under Social Security. As one of these studies summarized the findings, in Social Security “…Hispanics have returns and transfers that are significantly above those for whites and blacks.” [3]

- A well publicized 1998 Heritage Foundation report argued that Hispanics would fare much better if a system of private accounts replaced the current Social Security system. Unlike the other studies cited here, that Heritage report was not based on a statistical analysis of actual Social Security records; it was based instead on hypothetical case studies that Heritage staff constructed. That Heritage report has been subject to careful scrutiny and has been discredited, with particularly strong criticism coming from the non-partisan actuaries at the Social Security Administration. Careful analysis shows that Hispanics would be harmed, not helped, by replacing Social Security with private accounts. Hispanics benefit disproportionately from several types of insurance that Social Security provides, such as disability insurance, and from Social Security’s redistributive nature, which favors workers with lower-than-average wages. These features would be lost under a pure system of private accounts, under which each person’s benefits would depend solely on that person’s level of earnings and payroll tax payments.

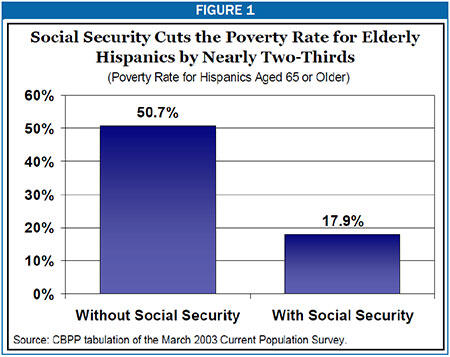

- Social Security is a particularly important source of income for elderly Hispanics. In the absence of Social Security, more than half of elderly Hispanics would live in poverty. As of 2002, Social Security lifted 673,000 elderly Hispanics out of poverty and reduced the poverty rate among Hispanics aged 65 and over from 51 percent to 18 percent, a reduction of 33 percentage points. The anti-poverty effects of Social Security are roughly similar across the Hispanic community, irrespective of the country of origin.

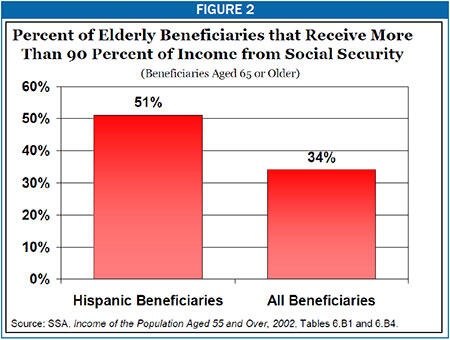

- Hispanic beneficiaries also rely on Social Security for a greater share of their income than does the population as a whole. As of 2002, some 51 percent of elderly Hispanic Social Security beneficiaries relied on Social Security for more than 90 percent of their income, compared to 34 percent of beneficiaries overall. Elderly Hispanics receive a smaller-than-average share of their retirement benefits from pensions and annuities than do other elderly individuals, and a larger share from Social Security.

- Young Hispanics are less likely to participate in an employment-based retirement plan, and tend to have fewer assets, than other young people. Of Hispanic wage and salary workers age 21-64, only 29 percent participated in an employer-sponsored retirement plan in 2003. This compares to a participation rate of 53 percent among white wage and salary workers and 45 percent among black wage and salary workers in the same age range. Thus, while young Hispanics are likely to be more successful economically than their parents, they, too, will need to rely heavily on Social Security.[4]

Based on these findings, we have also issued a separate report that analyzes the implications for the Hispanic community of various proposals to change Social Security.[5]

I. How Hispanic Fare Under Social Security

The Social Security system is redistributive; it disproportionately benefits people with:

- lower-than-average lifetime earnings;

- a higher-than-average incidence of disability;

- more children per family; and

- longer-than-average life expectancies.

These features of Social Security are of particular importance to Hispanics, because they have all four of these characteristics.

Lower-Than-Average Earnings

The Social Security benefit formula is progressive. For each dollar contributed to the Social Security system, a worker with low lifetime covered earnings gets more in benefits from Social Security than a worker with high lifetime earnings. As a whole, Hispanics receive lower average wages than the rest of the population. Thus, due to the progressive benefit formula, Hispanics tend to receive more back from Social Security relative to the taxes they pay into the system than does the rest of the population.

- The median earnings for Hispanics in jobs covered by Social Security was $22,400 in 2002, compared to $28,400 for all covered workers. [6] In other words, the median income for a Hispanic worker covered by Social Security was 20 percent lower than the median income for covered workers as a whole.

- Similarly, Hispanic Americans have lower average lifetime earnings covered by Social Security than the rest of the population. Lifetime earnings are of particular importance since lifetime earnings are used in the Social Security benefit calculation. According to a GAO analysis of workers born from 1931 through 1940, 38 percent of Hispanics are in the lowest lifetime earnings quintile. By comparison, 17 percent of non-Hispanic whites are in the lowest quintile.

At the other end of the income distribution, only 9 percent of Hispanics are in the highest lifetime earnings quintile. In contrast, 22 percent of non-Hispanic whites are in the top quintile.[7] People in the top quintile receive a lower return on Social Security taxes they pay than do people in lower income quintiles.

A Higher Incidence of Disability

Hispanics also have a somewhat higher probability of becoming disabled and receiving Social Security disability insurance benefits. Social Security disability insurance provides a lifetime benefit to covered workers who are no longer able to work due to disability. Those who receive disability checks tend to receive substantially more benefits per taxes paid into Social Security than those who are not disabled, since people with disabilities begin to receive benefits and cease contributing payroll taxes at an earlier age than non-disabled workers.

In its study on minorities and Social Security, GAO found that Hispanics made up 8.4 percent of its sample (which consisted of covered workers born from 1931 through 1964) but represented 10.1 percent of Disability Insurance beneficiaries. [8]

Families With More Children

Finally, Social Security tends to benefit disproportionately those families that have a larger number of children, because Social Security provides benefits to the dependent children of retired, deceased, and disabled workers. In 2003, four million children directly received Social Security benefits totaling about $20 billion.[9] Hispanics tend to have more children per family. As of 2003, the Hispanic fertility rate stood at 2.8 children per woman, while the national fertility rate was 2.0 children per woman.[10] Due to their higher than average fertility rates, Hispanic families tend to gain disproportionately from Social Security benefits directed to children.

Longer-than-Average Life Expectancy

Social Security also disproportionately benefits people who have longer-than-average life expectancies, and, according to official government estimates, Hispanics have substantially longer life expectancy than the rest of the population. Social Security provides guaranteed retirement and disability benefits that last as long as a beneficiary lives and are adjusted every year to keep pace with inflation. Those who live longer receive checks for a longer period of time and thus receive more in Social Security benefits relative to the taxes they pay into the system.

- The Social Security Administration estimates, based on Census data, that Hispanic men aged 65 in 2004 can expect to live an additional 20 years, compared to 16 years for all men.

- The Social Security Administration also finds that Hispanic women aged 65 in 2004 can expect to live an average of 23 years, compared to 20 years for all women.[11]

GAO has come to similar conclusions, as have the Social Security actuaries. [12]

Major Studies Confirm that Social Security is Especially Favorable to Hispanics

These four characteristics — lower lifetime incomes, longer life expectancies, higher disability incidence, and larger families — lead Hispanic Americans to receive more in Social Security benefits per dollar contributed to the system than the rest of the population. This elevated rate of return has consistently been confirmed by the leading studies in the field, which use Social Security records in combination with other data sources to examine the distribution of Social Security taxes and benefits for different groups in the population. [13]

Harvard economists Jeffrey Liebman and Martin Feldstein produced two of the first studies to use Social Security records as a basis for analysis and to report Hispanics’ rate of return on tax contributions to the Social Security system. In these analyses, Liebman and Feldstein found that the rate of return that Hispanics receive on their contributions to the Social Security system is about 35 to 60 percent higher than the rate of return for the population as a whole.[14] This is a significantly higher rate of return than for either non-Hispanic blacks or whites; both of those groups have rates of return close to the average for all workers. Moreover, the studies by Liebman and Feldstein do not take into account two factors that would increase further the rate of return for Hispanics, relative to that for the population as a whole. The studies do not take into account either the effects of Social Security disability insurance or Hispanics’ apparently longer average life expectancies. These factors further increase the rate of return for Hispanics.

Liebman and Feldstein’s finding — that Hispanics have a higher rate of return than the rest of the population — has been echoed by studies produced by the GAO and economists at the Social Security Administration and the Urban Institute. Like the Liebman and Feldstein analyses, these studies examined the distribution of Social Security benefits based on a sample of Social Security records combined with other data sources. (The recent studies use what is known as the Model of Income in the Near Term, or MINT, which projects retirement income and now appears to be the Social Security Administration’s major source for distributional information. This is the same model that the White House has been using in material it has been issuing recently on Social Security.)

A study by economists with the Social Security Administration and the Urban Institute looked at four cohorts of workers born from 1931 to 1964. (i.e., a cohort consisting of those born from 1931 to 1940, a cohort of those born from 1941 to 1945, and so on). The study separated the results for men and women. For each of the eight resulting groups, the study found that Hispanics receive a higher average rate of return on their Social Security tax contributions than the population as a whole, although the differences are smaller than Liebman and Feldstein found. In all cases, the rate of return that Hispanics received was higher than the rate of return received by non-Hispanic whites; in most cases, it also was higher than the rate of return received by non-Hispanic blacks.[15]

A major GAO study on Social Security and minorities similarly concluded that Hispanics receive a higher rate of return on their Social Security contributions than the rest of the population and that this rate of return is higher than that received by non-Hispanic whites or blacks. [16] In Congressional testimony, the GAO summarized some of the factors leading to these results. The GAO testified: “Social Security’s progressive benefit formula has particular importance for blacks and Hispanics because they tend to have lower lifetime taxable earnings than whites. The consensus among researchers is generally that the progressivity of the benefit formula outweighs the negative effect of lower life expectancy for blacks in terms of what they receive from Social Security relative to what they contribute. Hispanics’ longer life expectancy, combined with the progressive benefit formula, indicates that they fare even better than blacks under Social Security.”[17]

Factors Reducing Hispanics’ Return on Contributions to Social Security

Due to the characteristics described in this analysis, Hispanics receive higher rates of return on their contributions to Social Security than other workers. There also are several factors that reduce Hispanics’ rate of return.

- The threshold to qualify for benefits . To qualify for Social Security retirement benefits, a worker must contribute to the Social Security system for at least ten years. This creates a cliff in the system that can adversely affect workers with short work histories. Despite the fact that they have contributed payroll taxes, those who work for less than ten years in covered employment receive no retirement benefits, while someone who works exactly ten years can receive substantial benefits. New immigrants, of which there are many in the Hispanic community, tend to have relatively short work histories in the United States.* Furthermore, the Social Security system also makes it more difficult for domestic workers (many of whom are Hispanic) than for others to get work counted toward the ten-year threshold. Thus, Hispanics are disproportionately harmed by the way the threshold is structured.**

- Marriage rates . A slightly smaller share of the elderly Hispanic population aged 65 or older is or has been married than is true of the rest of the elderly population. Thus, the Hispanic population may not benefit quite as much as they otherwise would from spousal benefits. (On the other hand, a greater share of Hispanic married couples are one-earner families than is true of population as a whole. One-earner families benefit greatly from Social Security’s spousal benefit, and this would tend to raise Hispanics’ rates of return on their contributions to Social Security.)

- Lower mortality rates and survivors benefits. According to official government measures, Hispanics of working age also have lower mortality rates than others of the same age, which would tend to reduce the benefits Hispanics receive from Social Security survivors benefits.

The effects of these factors, are substantially outweighed, however, by the impact of the characteristics described in this analysis that significantly increase the rate of return that Hispanics receive on their Social Security contributions. Studies that use actual Social Security records show that when all factors are taken together, Hispanics receive a substantially higher rate of return on Social Security than the rest of the population.

The finding that Hispanics receive a higher rate of return on Social Security contributions than the rest of the population applies to Hispanics who are citizens or legal residents. Undocumented workers, who are disproportionately Hispanic, frequently pay taxes into the Social Security system under false or non-work status Social Security numbers. Stephen Goss, Chief Actuary of the Social Security Administration, was quoted in a recent New York Times article as saying that the Social Security Administration assumes that three-quarters of undocumented immigrants pay payroll taxes. Many of these undocumented immigrants will never collect Social Security benefits based.*** It should be noted that no Social Security reform plans being seriously considered, including private account plans, would expand benefits to undocumented workers.

* Short work histories also can increase workers’ rates of return on their contributions to Social Security, if the workers modestly surpass the ten-year eligibility threshold for benefits. Due to the progressive nature of the Social Security benefit formula, the system will pay back more to workers — like those with short work histories — who have low lifetime earnings, if they qualify for benefits.

** For more details on how the threshold can have adverse consequences for the Hispanic populations, see National Council of La Raza, The Social Security Program and Reform: A Latino Perspective, 2005, available at http://www.nclr.org/files/32018_file_Social_Security_Prog_FNL.pdf .

*** Eduardo Porter, “Illegal Immigrants are Bolstering Social Security with Billions,” New York Times, April 5, 2005.

Finally, the Social Security actuaries have officially endorsed the consistent finding of these studies — that Hispanics receive more back from Social Security per tax dollar contributed than the rest of the population. An analysis by the actuaries reports that “a somewhat higher rate of return for Hispanic Americans is to be expected, based on the higher life expectancy for Hispanic Americans, and the fact that Hispanic Americans have lower than average earnings.”[18] Similarly, a fact sheet that the Social Security Administration issued several years ago notes that Hispanics “on average receive a higher rate of return on taxes paid.” [19]

II. Private Accounts and the Rate of Return Myth

As noted, Hispanics benefit disproportionately from several types of insurance that Social Security provides and from Social Security’s redistributive nature. Private accounts, by contrast, would tie each person’s benefits directly to that person’s level of earnings and tax contributions, without adjustment for lower earnings, a higher incidence of disability, longer life expectancy, or other such factors. Thus, replacing the Social Security system with private accounts would tend to be harmful to the Hispanic community.

Despite this, a few reports have claimed that Hispanics would be better off if Social Security were entirely replaced by private accounts. These reports are marred by serious analytic flaws.[20]

Comparing Apples to Oranges: Ignoring Transition Costs and Stock-Market Risk

As noted, Martin Feldstein and Jeffrey Liebman confirmed the finding that Hispanics receive a higher rate of return on taxes paid into Social Security than the rest of the population. But, in one paper, they also claimed that Hispanics — and indeed the entire U.S. population — would be better off if the Social Security system were replaced with private accounts since private accounts would earn a higher rate of return. [21] In comparing Social Security to private accounts, this paper suffered from several serious limitations that plague reports that make this argument. The paper ignored two critical factors, which skewed its comparison and led to faulty results. [22]

- Transition costs. The paper failed to take into account the substantial “transition costs” of switching from Social Security to a private account system. Current payroll taxes are used largely to fund current Social Security benefits. If the payroll taxes of current workers are diverted to private accounts, Social Security will not have the funds to pay promised benefits to current beneficiaries and those about to retire. To maintain benefits for these people, either taxes on current workers must be increased or the government must borrow very large sums that eventually will have to be paid back. The resulting tax increases or reductions in the benefits of future retirees made to repay the borrowed funds must be taken into account in computing the gains or losses of replacing Social Security with private accounts. The Feldstein-Liebman paper, however, neglects to do that. Once this is done, the “free lunch” results reflected in the paper’s estimates disappear and the results change markedly. Stated another way, comparisons that ignore the substantial new sums being injected into the system under a move to private accounts — from either tax increases or government borrowing — “stack the deck:” they compare returns under a Social Security system with one level of financing to rates of return under a private-accounts system with substantial additional financing, without taking the cost of the added financing into account. Such an approach is widely regarded by economists and Social Security analysts as not being valid.

- Stock-market risk. The estimates in the Feldstein-Liebman paper also ignored the additional risk associated with investing in the stock market, as compared to paying into the traditional Social Security system. Investors demand a higher average rate of return on stocks than on investments with less volatile returns, such as U. S. Treasury bonds, in order to compensate them for the greater risk they take by investing in stocks. The nonpartisan Congressional Budget Office and a wide range of economists agree that the cost of this added risk must be incorporated into analyses of rates of return under plans that shift large sums from safe investments such as Treasury bonds to the stock market. The Feldstein-Liebman paper does not incorporate this cost.

Once transition costs and stock-market risk are taken into account, a system with private accounts is not found to produce a better rate of return for the population as a whole than the current traditional Social Security system. This “bottom line” finding is reflected in the analyses of the Social Security actuaries. In the mid-1990s, the actuaries issued analyses of three plans to restore long-term Social Security solvency that were developed by the 1994-1996 Advisory Council on Social Security. One of those plans replaced part of Social Security with private accounts. A second plan added private accounts on top. The third plan did not include private accounts. When the actuaries analyzed the rates of return under the three plans in an analytically valid manner (taking care to avoid apples-to-oranges comparisons), they found that all three plans produced roughly the same rate of return for the population as a whole.[23] Here, as elsewhere in economics, there is no “free lunch.” And for Hispanics in particular, the Social Security system is superior to private accounts, because Hispanics benefit disproportionately from Social Security’s social insurance and redistributive nature, which would be lost if Social Security were ended and replaced by private accounts.

Heritage Foundation Report

A well publicized 1998 Heritage Foundation report also claimed that the “Social Security system’s rate of return for most Hispanic Americans will be vastly inferior to what they could expect from placing their payroll taxes in even the most conservative private investments.” [24] The Heritage report, as well, reached this conclusion based on faulty methodology.

The Heritage report has been subject to careful scrutiny and has been widely discredited. The study has been criticized by, among others, Stephen Goss, the Chief Actuary of the Social Security Administration, [25] and Robert Myers, the former Chief Actuary of the Social Security Administration who for decades was the leading adviser on Social Security to Congressional Republicans and who served as Executive Director of the 1983 Greenspan Commission.[26]

Major flaws with the Heritage report include: [27]

- Like the Feldstein and Liebman paper, the Heritage Foundation report failed to take into account the transition costs of switching to a system of private accounts, as well as the cost associated with the risks of investing in the stock market.

- Furthermore, Heritage used an inappropriate measure of life expectancy that substantially skewed its results. As reported by Stephen Goss, now Social Security’s Chief Actuary, “the [Heritage] approach consistently overestimates the expected number of years of work and consistently underestimates the expected number of years [of benefits] after reaching retirement age. As a result, it grossly underestimates the expected rates of return from Social Security retirement benefits.” [28]

- Compounding these problems, Heritage erroneously calculated rates of return for Social Security by assuming that Social Security solvency would be restored solely through a payroll tax increase that both would start earlier than needed and be larger than needed to restore solvency. This assumption artificially lowered the rate of return that Heritage computed for Hispanics under the Social Security system. Heritage also failed, when calculating the rate of return, to take into account Social Security’s disability insurance system, which disproportionately benefits Hispanic workers. Heritage underestimated the benefits of Social Security’s survivors insurance, as well.

- Another shortcoming of the report was that Heritage failed to incorporate the administrative expenses and fees that would be associated with private accounts and be financed out of the accounts. This oversight inflated the rate of return that the report claimed the accounts would produce.

Heritage also failed to acknowledge that, as Goss pointed out in an official memorandum released by the Social Security actuaries, even “by their [Heritage’s] own calculations…Hispanic Americans would be expected to receive a substantially higher rate of return from Social Security than would the general population, on average”.[29]

Social Security: A Key Support for Elderly Hispanics

Social Security is a particularly important source of support for the 1.2 million elderly Hispanics that receive Social Security benefits. As a recent study from the Pew Hispanic Center finds, “Latinos age 65 or older are in worse economic condition than other racial and ethnic groups. They lack income from private pension plans or personal wealth, and [in the absence of Social Security] most of them live in poverty. As a result, elderly Hispanics are much more dependent on the Social Security system than other groups of retirees.” [30]

Without Social Security, over half of elderly Hispanics would live in poverty. Thanks to Social Security, less than a fifth do. Census data show that Social Security reduced the poverty rate for elderly Hispanics from 51 percent to 18 percent in 2002, lifting 673,000 elderly Hispanics out of poverty. As shown in Table 1, the anti-poverty effects of Social Security are roughly similar across the Hispanic community, irrespective of the country of origin.[31]

|

Table 1: |

||||

|

Country of Origin |

Poverty Rate |

Number Lifted Out of Poverty |

||

|

Without Social Security |

With Social Security |

Percentage Point Reduction from Social Security |

||

|

Hispanic |

50.7% |

17.9% |

-32.8% |

673,000 |

|

Mexican |

51.6% |

20.1% |

-31.5% |

347,000 |

|

Cuban |

53.7% |

15.0% |

-38.7% |

132,000 |

|

Central/South American |

42.3% |

12.4% |

-29.9% |

78,000 |

|

Puerto Rican |

50.9% |

16.3% |

-34.6% |

72,000 |

|

Other Hispanic |

N/A* |

N/A* |

N/A* |

45,000 |

|

* Note: Sample size is too small to calculate percentages. |

||||

Social Security provides a larger share of the total income of elderly Hispanics (including the income of elderly Hispanics who are not beneficiaries) than it does of the income of the elderly population as a whole. [32] As of 2002, some 44 percent of the total income of elderly Hispanics came from Social Security. This compares to 39 percent for the elderly population as a whole.

As can be seen in Table 2, elderly Hispanics receive a particularly small share of their income from pensions and annuities and financial assets. This is important to note since, together with Social Security, these forms of income are what support retirement security. The elderly population as a whole received about 19 percent of its income from pensions and annuities in 2002. By contrast, elderly Hispanics received 13 percent of their income from those sources. Elderly Hispanics also received a much smaller share of their income in the form of income from assets, which is another key to retirement security. Income from assets represented only 6 percent of their income, as opposed to 14 percent of income for the population as a whole. [33]

As a result, a majority of elderly Hispanic Social Security beneficiaries rely on their Social Security checks for most or all of their income.

|

Table 2 |

|||

|

Hispanic Elderly |

All Elderly |

Difference |

|

|

Social Security |

44.2% |

39.4% |

+4.8% |

|

Pensions/Annuities* |

13.3% |

19.0% |

-5.7% |

|

Subtotal: Retirement Benefits |

57.5% |

58.4% |

-0.9% |

|

Income from Assets |

6.3% |

13.6% |

-7.3% |

|

Earnings |

30.4% |

24.9% |

+5.5% |

|

Public Assistance |

3.6% |

0.7% |

+2.9% |

|

Other |

2.2% |

2.4% |

-0.2% |

|

Total |

100.0% |

100.0% |

0.0% |

| * Note: “Pensions/Annuities” includes income from private pensions and annuities, government employee pensions, and railroad retirement. Source: Social Security Administration, “Income of the Population Aged 55 or Older, 2002,” Tables 7.1 and 7.4. |

|||

- In 2002, some 51 percent of elderly Hispanic Social Security beneficiaries relied on Social Security for 90 percent or more of their income, compared to 34 percent of Social Security beneficiaries overall.

- Similarly, 41 percent of elderly Hispanic Social Security beneficiaries relied on Social Security for all of their income, compared to 22 percent for beneficiaries as a whole.[34]

The importance of Social Security to elderly Hispanics does not seem likely to diminish in the coming years. As the Pew Hispanic Center concludes, “Current indicators suggest that future Hispanic retirees will depend on Social Security to as great an extent as today’s retirees, if not more so.” [35]

- The Pew Hispanic Center finds that young Hispanics have far fewer assets than non-Hispanic whites of the same age. For instance, the Pew Hispanic Center reports that median net household wealth for Hispanics age 35-44 is less than one-sixth as high as median wealth for non-Hispanic whites of the same age.

- Median net household wealth among Hispanics age 35-44 stood at $9,994 in 2002, the Pew Center reports. Median wealth among non-Hispanic whites in the same age bracket stood at $66,077.[36]

Moreover, a recent study by the Employee Benefit Research Institute shows that Hispanic workers have far lower participation rates in employer-sponsored retirement plans than either whites or blacks.

- Of the 16.3 million Hispanic wage and salary workers aged 21-64 in 2003, only 29 percent participated in an employer-sponsored retirement plan. This compares to a participation rate of 53 percent among white wage and salary workers and 45 percent among black wage and salary workers in the same age range.

- In addition, while both white and black participation in employer-sponsored retirement plans has increased somewhat since 1987 (the first year for which the EBRI report provides data), Hispanic participation has actually fallen slightly over the same period. [37]

Given this growing gap in the rate of participation in retirement plans, it seems likely that elderly Hispanics will continue to rely more heavily on Social Security than the rest of the population.

Smaller Benefits But Higher Returns

Elderly Hispanics tend to receive a smaller median Social Security benefit, in dollar terms, than does the population as a whole because the incomes of elderly Hispanics and, thus, their payroll tax contributions are lower during their working years. For workers born from 1925-1929, one study found that Hispanics’ average annual earnings taxed by Social Security were 43 percent lower than for the population as a whole.*

This does not mean that Hispanics benefit less from Social Security than does the rest of the population. As detailed in this analysis, the opposite is the case. Because their lifetime earnings (as covered by Social Security) are lower, on average, Hispanics contribute less to the system, but they receive a substantially higher rate of return on the contributions they make than do other workers. Thus, while Hispanics’ Social Security checks may be smaller, their returns are greater, based on what they contributed.

* Jeffrey B. Liebman, “Redistribution in the Current U.S. Social Security System,” in The Distributional Effects of Social Security and Social Security Reform, Martin Feldstein and Jeffrey B. Liebman, eds., Chicago: University of Chicago Press, 2002.

Conclusion

The Hispanic community has a great deal at stake in the debate over Social Security reform. As noted in this analysis, Hispanics gain from the various types of insurance and redistributive mechanisms that Social Security provides. The Social Security system disproportionately benefits people with low incomes, higher-than-average disability rates, more children per family, and long lives. Hispanics exhibit all four of these characteristics. They consequently receive a higher rate of return on the taxes they pay into the system than the rest of the population. Furthermore, elderly Hispanics rely on Social Security for a larger share of their income than the rest of the population does.

The Hispanic community consequently needs to be wary of “reforms” that would substantially reduce Social Security benefits and shrink the social insurance aspects of Social Security — and instead tie each person’s benefits more directly to that person’s level of earnings and tax contributions. We have also issued a separate analysis that explores the implications for the Hispanic community of proposals to reduce Social Security benefits and to replace part of Social Security with a system of private accounts. [38]

End Notes

[1] Fernando Torres-Gil is Director of the UCLA Center for Policy Research on Aging and Acting Dean of the UCLA School of Public Affairs. Robert Greenstein is Executive Director, and David Kamin is a Research Assistant, at the Center on Budget and Policy Priorities.

[2] Recent CBPP analyses describe how rate-of-return comparisons are often used improperly by advocates of private accounts who claim that the rate of return on private accounts is higher than under the traditional Social Security system. These claims rest on “apples-to-oranges” comparisons that do not take into account all of the benefits provided by Social Security and also the additional costs entailed in replacing part of Social Security with private accounts. (For additional details, see pp. 8-11.)

Rate-of-return comparisons can be informative, when done on an “apples-to-apples” basis. Here, we are comparing Hispanics’ rate of return on contributions to the Social Security system to the rate of return that other populations receive on contributions to Social Security. This is a valid comparison, done on a consistent basis, that helps to illustrate who benefits more from the Social Security system.

[3] Jeffrey Liebman, “Redistribution in the Current U.S. Social Security System,” in The Distributional Effects of Social Security and Social Security Reform, Martin Feldstein and Jeffrey Liebman, eds., Chicago: University of Chicago Press, 2002, p. 31.

[4] In Congressional testimony several years ago, the National Council of La Raza (NCLR) reached many of the same conclusions as this analysis. NCLR found that Hispanics receive higher rates of return on their contributions to Social Security than other workers, and NCLR criticized proposals that would replace Social Security with private accounts as being detrimental to the Hispanic community. National Council of La Raza, “Social Security Reform: Issues for Hispanic Americans,” Submitted to the Committee on Ways and Means, Subcommittee on Social Security, Presented by Eric Rodriguez, Senior Policy Analyst, on behalf of Sonia M. Perez, Senior Vice President, February 10, 1999, available at http://www.nclr.org/content/publications/download/29396.

[5] Fernando Torres-Gil, Robert Greenstein, and David Kamin, “Hispanics and Social Security Reform: The Implications of Reform Proposals,” Center on Budget and Policy Priorities, June 28, 2005.

[6] Social Security Administration (SSA), “Social Security is Important to Hispanics,” September 2004, available at http://www.ssa.gov/pressoffice/factsheets/hispanics.htm.

[7] Government Accountability Office (GAO), “Social Security and Minorities: Earnings, Disability Incidence, and Mortality are Key Factors that Influence Taxes Paid and Benefits Received,” April 2003, p. 11, available at https://www.cbpp.org/sites/default/files/atoms/files/d03387.pdf

[8] GAO, “Social Security and Minorities,” p. 12.

[9] SSA, Annual Statistical Supplement, 2004, Table 5.A1.4, available at http://www.ssa.gov/policy/docs/ statcomps/supplement/.

[10] Brady E. Hamilton, Joyce A. Martin, and Paul D. Sutton, Centers for Disease Control and Prevention, “Births: Preliminary Data for 2003,” National Vital Statistics Reports, November 23, 2004, p. 2, available at http://www.cdc.gov/nchs/data/nvsr/nvsr53/nvsr53_09.pdf. In recent years, the Hispanic fertility rate has declined. From 1990 to 2003, the Hispanic fertility rate fell from 3.0 children per woman to 2.8 children per woman, even while the national fertility rate held steady. Nonetheless, it is likely that Hispanics will continue to have higher fertility rates than the rest of the population for many decades to come. In fact the Census Bureau, in its long-term population projections, assumes that fertility rates for the Hispanic population, while falling, will remain above the fertility rate for the rest of the population through 2100. Thus, for the foreseeable future, Hispanics are likely to continue to gain disproportionately from Social Security’s benefits for children.

[11] SSA, “Social Security is Important to Hispanics.”

[12] Several researchers have raised questions as to whether Hispanics’ longer-than-average life expectancies are real or are a product of measurement error. For instance, see Alberto Palloni and Elizabeth Arias, “Paradox Lost: Explaining the Hispanic Adult Mortality Advantage,” Demography, vol. 41, no. 3, August 2003, pp. 385-415. Even if Hispanics did not have longer-than-average life expectancies, they would receive well-above-average rates of return on their contributions to the Social Security system because they exhibit all of the other characteristics described here. This is confirmed by the studies described in the next section of this paper, which do not assume that Hispanics have longer-than-average life expectancies and still find that Hispanics receive a higher rate of return on the taxes they pay into the Social Security system than does the rest of the population.

[13] The results of these studies, which use Social Security records combined with other data sources, exclude those undocumented workers who, because of their illegal work status, do not receive benefits based on their contributions to Social Security. Despite their illegal work status, undocumented immigrants frequently do pay taxes into the Social Security system under false or non-work status Social Security numbers, and many of these undocumented immigrants will never collect Social Security benefits based on these taxes paid while working illegally. (Only those who eventually become legal workers may collect benefits.) The studies cited here do not consider the negative rates of return for these undocumented immigrants on their payments to Social Security.

[14] One paper was written by Liebman alone; Liebman co-authored the other paper with Feldstein. In both papers, the authors used a sample of Social Security records and other data sources to determine the economic and demographic characteristics of Social Security participants. To better capture the rate of return on Social Security over the long term, they assumed that covered workers would face a payroll tax rate six percentage points higher than under current law. This would be sufficient to cover the cost of Social Security benefits modeled in the paper on a cash basis in 2075.

Under these assumptions, Liebman, in one paper, found that the annual rate of return on Hispanics’ contributions to the Social Security system is 2.46 percent above inflation, whereas the rate of return for the population as a whole is 1.53 percent above inflation. In a second paper, Liebman and Feldstein reported that the annual rate of return on Hispanics’ contributions to the Social Security system is 1.81 percent above inflation, whereas the rate of return for the population as a whole is 1.35 percent above inflation. By the first estimate, Hispanics’ rate of return on Social Security is about 60 percent above the rate of return for the rest of the population. By the second estimate, Hispanics’ rate of return is about 35 percent above the rate of return for the rest of the population.

See Jeffrey B. Liebman, “Redistribution in the Current U.S. Social Security System,” in The Distributional Effects of Social Security and Social Security Reform, Martin Feldstein and Jeffrey B. Liebman, eds., Chicago: University of Chicago Press, 2002. Also, Martin Felstein and Jeffrey B. Liebman, “The Distributional Effects of an Investment-Based Social Security System,” in The Distributional Effects of Social Security and Social Security Reform, Martin Feldstein and Jeffrey B. Liebman, eds., Chicago: University of Chicago Press, 2002.

[15] Lee Cohen, C. Eugene Steurele, and Adam Carasso, “The Effect of Disability Insurance on Redistribution Within Social Security By Gender, Education, Race, and Income,” June 2002, available at http://www.bc.edu/centers/crr/papers/Fourth/cp_02_3_steuercohencaras.pdf .

[16] GAO, “Social Security and Minorities.”

[17] GAO, Testimony before the Social Security Subcommittee, House Committee on Ways and Means, February 10, 1999, available at http://www.gao.gov/archive/1999/he99060t.pdf.

[18] Memorandum from Stephen C. Goss, Deputy Chief Actuary, to Harry C. Ballantyne, Chief Actuary, “Comments on Heritage Rates of Return for Hispanic Americans,” Social Security Administration, April 2, 1998.

[19] SSA, “Social Security and Hispanic Americans: Some Basic Facts,” July 1998.

[20] For additional analysis of the “rate of return myth,” see Jason Furman, “https://www.cbpp.org/sites/default/files/atoms/files/6-2-05socsec.pdf” Center on Budget and Policy Priorities, June 2, 2005.

[21] Felstein and Liebman, “The Distributional Effects of an Investment-Based Social Security System.”

[22] For a detailed critique of the Feldstein and Liebman analysis, see Peter Orszag and John Orszag, “https://www.cbpp.org/sites/default/files/atoms/files/4-26-00socsec.pdf,” Center on Budget and Policy Priorities, April 26, 2000. For additional analysis of the problems with comparing the rate of return on private accounts to the rate of return on Social Security, see Jason Furman, “

” Center on Budget and Policy Priorities, June 2, 2005.[23] Advisory Council on Social Security, Report of the 1994-1996 Advisory Council on Social Security: Findings and Recommendations, January 1997.

[24] William W. Beach and Gareth G. Davis, “Social Security’s Rate of Return for Hispanic Americans,” Heritage Foundation, March 27, 1998, available at http://www.heritage.org/Research/SocialSecurity/CDA98-02.cfm.

[25] See Goss, “Comments on Heritage Rates of Return for Hispanic Americans.” Also, Memorandum from Steve Goss, Deputy Chief Actuary, “Problems with ‘Social Security’s Rate of Return’: A Report of the Heritage Center for Data Analysis,” February 4, 1998.

[26] Robert J. Myers, “A Glaring Error: Why One Study of Social Security Misstates Returns,” The Actuary, September 1998, p. 5, available at http://library.soa.org/library/actuary/1990-99/ACT9809.pdf.

[27] For a more detailed critique of the Heritage Foundation’s findings, see Kilolo Kijakazi, “https://www.cbpp.org/sites/default/files/atoms/files/10-5-98socsec.pdf,” Center on Budget and Policy Priorities, October 8, 1998. This report draws from that analysis.

[28] Goss, “Problems with ‘Social Security’s Rate of Return.’”

[29] Goss, “Comments on Heritage Rates of Return for Hispanic Americans.”

[30] Richard Fry, Rakesh Kochhar, Jeffrey Passel, and Roberto Suro, “Hispanics and the Social Security Debate,” Pew Hispanic Center, March 16, 2005, p. 10, available at http://pewhispanic.org/files/reports/43.pdf.

[31] In determining poverty status, these calculations use family disposable income (that is, after-tax cash income plus food, housing, and energy assistance). This approach results in lower estimates of poverty than the official Census Bureau poverty data, which rely on pre-tax income and do not include non-cash benefits. (Under the Census Bureau’s official poverty measure, Social Security has nearly the same anti-poverty effect as reported here. Based on the official poverty measure, Social Security reduced the poverty rate among elderly Hispanics by 31 percentage points in 2002, from 52.1 percent to 21.4 percent.) For more details on the methodology, see the “Technical Note” in Arloc Sherman and Isaac Shapiro, “https://www.cbpp.org/sites/default/files/atoms/files/2-24-05socsec.pdf,” Center on Budget and Policy Priorities, February 24, 2005.

[32] It should be noted that a smaller percentage of elderly Hispanics receive Social Security than of other retirees. The lower participation rates are a result of a number of factors. Undocumented workers, many of whom are Hispanic, also are ineligible for benefits. In addition, as noted, Social Security’s eligibility threshold, which requires ten years of covered work, can adversely affect Hispanic workers. Undocumented workers — many of whom are Hispanic — also are ineligible for benefits.

Despite these lower participation rates, the elderly Hispanic population — including non-beneficiaries — receives a greater share of its income, on average, from Social Security than the population as a whole (see table 2). This is because those Hispanic retirees who do receive Social Security checks rely especially heavily on that income to support their retirement.

[33] Social Security Administration, “Income of the Population Aged 55 or Older, 2002,” March 2005, Tables 7.1 and 7.4, available at http://www.ssa.gov/policy/docs/statcomps/income_pop55/2002/.

[34] Ibid., Tables 6.B1 and 6.B4.

[35] Fry, et. al., “Hispanics and the Social Security Debate,” p. 12.

[36] Wealth figures expressed in 2003 dollars. Ibid., p. 17.

[37] Craig Copeland, “Employment-Based Retirement Plan Participation: Geographic Differences and Trends,” Employee Benefit Research Institute Issue Brief, October 2004, available at http://www.ebri.org/ibpdfs/1004ib.pdf.

[38] “Hispanics and Social Security: The Implications of Reform Proposals,” June 28, 2005.