Tax Extenders Package Is Fundamentally Flawed

The emerging “tax extenders” package marks a significant step backward on several key issues facing the nation: long-term budget deficits, high levels of poverty (especially among children), and widening inequality. It would permanently enlarge budget deficits — and, by so doing, increase pressures to cut domestic programs more deeply — while favoring large corporations and leaving out millions of families that work for low or modest wages.

At a cost of more than $400 billion over ten years, the package makes permanent a series of temporary tax breaks known as the “tax extenders” and substantially enlarges some of them, while extending most of the remaining extenders for two years. This would undo more than half of the revenue raised by the “fiscal cliff” legislation at the end of 2012, and would consequently result in the overwhelming share of the deficit reduction achieved since 2010 — more than 85 percent of it — coming from budget cuts, with little net revenue savings. And, with congressional Republicans insisting that future congressional budget resolutions balance the budget in ten years without new revenues, the extenders package would increase pressure to cut domestic programs more deeply.

Moreover, if policymakers make a number of extenders permanent now without paying for them, they won’t have to offset the cost of making these tax breaks permanent as part of future tax reform legislation. That would enable them to produce a tax reform bill that cuts the top tax rate more deeply, curbs fewer special-interest tax breaks, or both — and yet still is labeled “revenue neutral.”

Finally, the package is lopsided in whom it benefits and whom it ignores. Two-thirds of its more than $400 billion in tax benefits would go to businesses. Yet it fails to extend the temporary tax provisions most important for reducing poverty and increasing opportunity among low-income working families with children. Those provisions, improvements in the Earned Income Tax Credit (EITC) and the low-income component of the Child Tax Credit (CTC) that were first enacted in 2009 and are scheduled to expire after 2017, lift more than 16 million people out of poverty or closer to the poverty line each year, including nearly 8 million children. By making a slew of the corporate tax extenders permanent while failing to extend these CTC and EITC provisions, the package risks stranding those provisions and making it less likely they will continue beyond 2017.

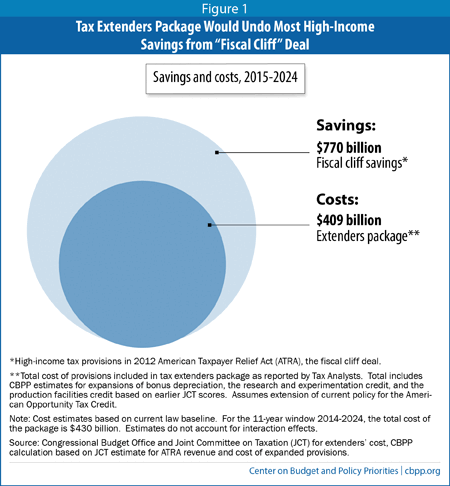

Reverses Majority of “Fiscal Cliff” Revenue Savings

The 2001 Bush tax cuts were both expensive and regressive. The 2012 “fiscal cliff” deal moderated a portion of these excesses by restoring $770 billion in revenue from high-income households over 2015-2024, mostly by returning the top tax rate to pre-Bush levels. The emerging tax extenders package, however, costing over $400 billion, would give back more than half of those “fiscal cliff” revenues (see Figure 1).[1] This includes the cost not only of reinstating and making permanent some business tax breaks that Congresses previously have enacted on a temporary basis, but also greatly enlarging several of these provisions. For example, the package appears to include a provision that would more than double the size of the Research and Experimentation tax credit, already one of the largest business tax extenders.

Congressional Republicans have signaled their commitment to advancing a budget plan next year that would balance the budget in ten years with no new revenues, cuts in Social Security benefits for current retirees, or defense cuts. Such a plan already would require deep cuts in important areas; the extenders package would require the cuts to be still more severe. As incoming House Budget Committee Chairman Tom Price (R-GA) said recently, “anything that’s made permanent now makes it more difficult to get to balance.”[2] If the tax extenders package is enacted, the risk will increase that Medicare, Medicaid, education, basic research, transportation, and other priorities will ultimately be cut more heavily.

Strands Vital Pro-Work Tax Provisions

Parties to the tax extenders negotiations discussed making permanent — as part of the extenders package — several EITC and CTC provisions for low-income working parents and their children first enacted in 2009. Yet the new package excludes them. By making key corporate tax provisions permanent while leaving out key working-family provisions, the package increases the risk that these provisions will die after 2017.

The omission of the EITC and CTC provisions is reminiscent of the disappointing outcome of the 2012 fiscal cliff negotiations, which severed the link that policymakers had established between those working-family provisions and a large cut in the estate tax for the nation’s wealthiest heirs. The fiscal cliff legislation made that tax cut for wealthy heirs permanent but extended the EITC and CTC provisions only through 2017. The new extenders package would now eliminate the link between some of the key tax extenders and the working-family provisions — the fact that both must be extended to remain in effect. The fewer such linkages, the greater the risk the low-income working-family provisions will end after 2017.

If the CTC and EITC provisions expire:

- More than 16 million people in low-income working families would be pushed into, or deeper into, poverty. Some 50 million Americans overall with modest incomes — including 31 million children — would lose part or all of their EITC or CTC and see their after-tax income go down.

- The effects would be particularly sharp on families raising children on minimum-wage earnings. A single mother raising two children on full-time, minimum-wage earnings of $14,500 would lose her entire CTC of $1,725.

- Many married couples with modest incomes would face bigger marriage penalties. One of the two EITC provisions set to expire after 2017 provides marriage-penalty relief; without it, many low-income married filers will face significantly larger marriage penalties.

- Larger families, too, would face a cut in their EITC. After 2017, the maximum EITC for families with more than two children would fall by over $700 (to the level of the maximum EITC for families with two children).

Meanwhile, the lopsided package would deliver substantial tax benefits to high-income filers. As noted, roughly two-thirds of the package consists of business tax cuts, which benefit high-income people far more than low- or moderate-income people, since they disproportionately own the businesses or stock in the corporations that will benefit.

Paves the Way for Tax Reform With Inadequate Revenues

Finally, making a number of extenders permanent now, in advance of tax reform, would lower the revenue baseline — that is, the revenues projected under current law. This means tax reform would need to raise less revenue to be considered “revenue-neutral.”

Lawmakers fashioning a tax reform bill no longer would have to offset the cost of extenders they want to make permanent; instead, they would get a windfall of more than $400 billion they could use to cut the top tax rate more deeply, curb fewer unproductive or low-priority tax breaks, or both. And as noted, one likely result would be to place greater pressure on key programs — both those already squeezed by sequestration, such as education and basic research, and programs ranging from Medicaid to veterans’ programs.

The best course for Congress and the President to follow would be to reject this lopsided, fiscally profligate package and to continue the tax extenders for a short duration during which they seek to produce a balanced, fiscally responsible tax reform measure to strengthen the nation’s tax code.

End Notes

[1] Tax Analysts has issued a list of the provisions reportedly in the deal. See Lindsey McPherson, “Lawmakers Reach Extenders Deal Making 10 Provisions Permanent,” Tax Analysts, November 25, 2014, http://services.taxanalysts.com/taxbase/uttmnews.nsf/DocNoLookup/852578370019994F85257D9B006518D2?OpenDocument.

[2] Richard Rubin and James Rowley, “Extension of Lapsed Breaks Faces Obstacles in Congress,” Washington Post, November 25, 2014, http://washpost.bloomberg.com/Story?docId=1376-NFB5EX6VDKJ301-14FAILS96HREN87S4KEQT8UQA0.

More from the Authors