Policy Basics: Marginal and Average Tax Rates

Misunderstandings about two different types of tax rates often create confusion in discussions about taxes. A taxpayer’s average tax rate (or effective tax rate) is the share of income that they pay in taxes. By contrast, a taxpayer’s marginal tax rate is the tax rate imposed on their last dollar of income.

Taxpayers’ average tax rates are lower — usually much lower — than their marginal rates. People who confuse the two can end up thinking that taxes are much higher than they actually are.

Under a Progressive Tax System, Marginal Rates Rise With Income

The federal income tax system is progressive, meaning that it imposes a higher average tax rate on higher-income people than on lower-income people.

It achieves this by applying higher marginal tax rates to higher levels of income. For example, in 2020, the first portion of any taxpayer’s taxable income is taxed at a 10 percent rate, the next portion is taxed at a 12 percent rate, and so on, up to a top marginal rate of 37 percent.

Average Tax Rate Is Generally Much Lower Than Marginal Rate

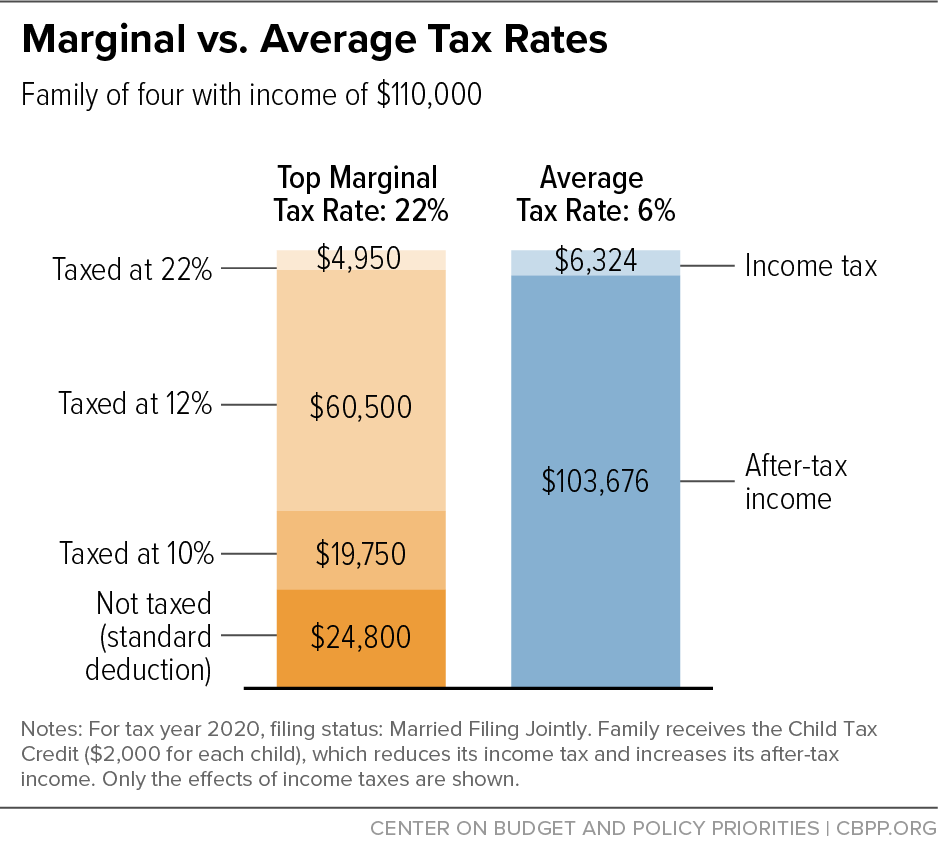

As an example, the graph below shows a married couple with two children earning a combined salary of $110,000. They face a top marginal tax rate of 22 percent, so they would commonly be referred to as “being in the 22 percent bracket.” But their average tax rate — the share of their salary that they pay in taxes — is only 6 percent, as explained below.

An individual’s average tax rate tends to be much lower than his or her marginal tax rate for three main reasons.

1. Because of deductions, not all income is subject to taxation.

In the example above, the couple can claim the standard deduction for tax year 2020 totaling $24,800. Subtracting that $24,800 from the couple’s $110,000 salary leaves them with $85,200 in taxable income — the amount of income subject to federal income taxes.

2. The top marginal tax rate applies only to a portion of taxable income.

As the graph shows, the first $19,750 of the couple’s taxable income is taxed at a 10 percent rate; the next $60,500 is taxed at 12 percent. Only the last $4,950 of their income faces their top marginal rate of 22 percent.

The couple’s resulting tax liability — before credits are taken into account — is $10,324.

3. Credits directly reduce the amount of taxes a filer owes.

Taxpayers subtract their credits from the tax they would otherwise owe to determine their final tax liability. In our example, the couple can claim the Child Tax Credit for both children, further reducing their tax by $4,000.

Our example couple is left with a final tax liability of $6,324. Dividing that amount by the couple’s total income ($110,000) results in an effective tax rate of 6 percent.

Note that this example reflects tax changes made by the 2017 tax law, which are set to expire after 2025. The 2017 tax law increased the standard deduction for married couples from $12,000 in 2017 to $24,000 in 2018 (the standard deduction is tied to inflation, so it increased to $24,800 in 2020) and eliminated the personal exemption, which reduced taxable income by $4,050 per family member in 2017. It also increased the maximum child tax credit from $1,000 per child to $2,000 per child and modified some of the individual tax brackets.