Three Types of “Repatriation Tax” on Overseas Profits: Understanding the Differences

Two proposals to address multinational corporations’ large stockpile of offshore profits — a transition tax on those profits and a repatriation tax holiday — may appear similar at first blush but are opposites in many ways. A transition tax is a sound policy that would raise revenues for infrastructure investments or other uses; a repatriation holiday is a tax cut that loses revenue and consequently cannot pay for anything. A third proposal, a “deemed repatriation,” could resemble a transition tax or a repatriation tax holiday, depending on the tax rate. All three types of proposals are sometimes referred to as “repatriation taxes,” but it is important to distinguish among them because of their very different effects on revenue and multinationals’ incentives to shift profits offshore. (See Figure 1.)

U.S.-based multinationals do not pay U.S. corporate tax on their foreign profits until the profits are “repatriated” to the United States. As a result, many firms use accounting maneuvers to report as much of their profits offshore as possible to avoid U.S. taxes. Multinationals have roughly $2.6 trillion in profits booked offshore, the Joint Committee on Taxation (JCT) estimates.[2] Both a transition tax and a repatriation tax holiday try to deal with these offshore profits — but in very different ways.

Heightening the confusion, several proposals have claimed to link each of these approaches to boosting investment in U.S. infrastructure. But while a transition tax can pay for such added investment, a repatriation holiday cannot. As Senate Finance Committee Chairman Orrin Hatch (R-UT) has stated, “Tax holiday proposals designed to pay for [replenishing the Highway Trust Fund] sound great until you look at the details. Saying you’re going to use something that loses money to pay for anything is just wrong. Therefore, saying you’re going to use it to pay for infrastructure is just bad policy, plain and simple.”[3]

Similarly, White House National Economic Council Director Jeff Zients has said the Administration is “not supportive of a voluntary repatriation holiday. . . . It costs a lot of money” and has emphasized that the Administration’s proposal for a transition tax “is very different than a repatriation holiday, which we believe is bad policy.”[4]

| Figure 1 | ||

|---|---|---|

| Three Types of “Repatriation Tax” on Overseas Profits | ||

| Transition Tax | Stand-Alone Deemed Repatriation |

Repatriation Tax Holiday |

| Compulsory | Compulsory | Optional |

| Raises revenue that could help pay for infrastructure or other one-time investments. | Raises revenue in the long run if the rate is high enough. Loses revenue in the long run if the rate is too low. | Loses revenue; cannot be used as a funding source. |

| Part of corporate tax reform, which can be designed to permanently reduce or eliminate incentives to shift profits offshore. | Stand-alone proposal that reduces or increases incentives for corporations to shift profits offshore, depending on the rate. | Stand-alone proposal that increases incentives for corporations to shift profits offshore. |

| Example: President Obama has proposed a 14 percent transition tax, with revenue going to infrastructure investment. | No congressional proposals to date. | Example: Senators Paul and Boxer proposed in 2015 a five-year repatriation holiday with stated goal of replenishing Highway Trust Fund. |

Transition Tax

Any corporate tax reform that alters the tax treatment of future overseas profits will likely include a one-time transition tax on existing foreign profits as part of the shift to the new tax system. A transition tax or “toll charge” would clean the slate of existing tax liabilities. Such a tax would be mandatory: multinationals would have to pay U.S. taxes on existing foreign profits whether they repatriate them or not. To achieve this, transition taxes would deem all foreign profits to have been repatriated and thus subject to the transition tax rate. (Most proposals would allow the companies to pay the tax over a period of years.) Future overseas profits would then be taxed under the new rules agreed to as part of tax reform.

A transition tax would raise one-time revenues that could help fund infrastructure investments or reduce deficits. For example, the President’s budget proposes a compulsory 14 percent transition tax on existing offshore profits, which would raise $299 billion to fund infrastructure investments, as part of transitioning to a new international tax system.[5]

Former Ways and Means Committee Chairman Dave Camp also included a transition tax in his 2014 tax reform proposal, at a maximum rate of 8.75 percent on most foreign profits.[6] Senators Rob Portman (R-OH) and Chuck Schumer (D-NY) also proposed in 2015 a framework for international tax reform and endorsed the broad transition tax approach in President Obama and Chairman Camp’s frameworks.[7]

Since transition tax revenues would be one-time in nature, they could not help pay for permanent corporate rate cuts on an ongoing basis (or provide permanent infrastructure funding either). For example, as noted above the President’s 14 percent transition tax proposal raises $299 billion. As the President’s Framework for Business Tax Reform notes, if those revenues were coupled with corporate rate cuts:[8]

[…A] package that appears revenue-neutral in the first ten years would lose roughly $380 billion in the second decade, and even more thereafter. For this reason, the one-time revenues raised by business tax reform should be matched with one-time investments or deficit reduction, as the President’s Framework proposes.

Repatriation Tax Holiday

A repatriation tax holiday is designed to encourage multinationals to return overseas profits to the United States by offering them a temporary, sharply reduced U.S. tax rate on those profits. It gives participating multinationals very large tax breaks (especially those that have aggressively shifted profits offshore) and increases deficits over the long term, as explained below. Because it loses revenues, it cannot be used to fund infrastructure investments or anything else.

The repatriation tax holiday enacted in 2004 failed to produce any of the promised economic benefits, such as boosting jobs or domestic investment, according to a wide range of independent studies by economists associated with the National Bureau for Economic Research, the Congressional Research Service, the Treasury Department, and other analysts.[9]

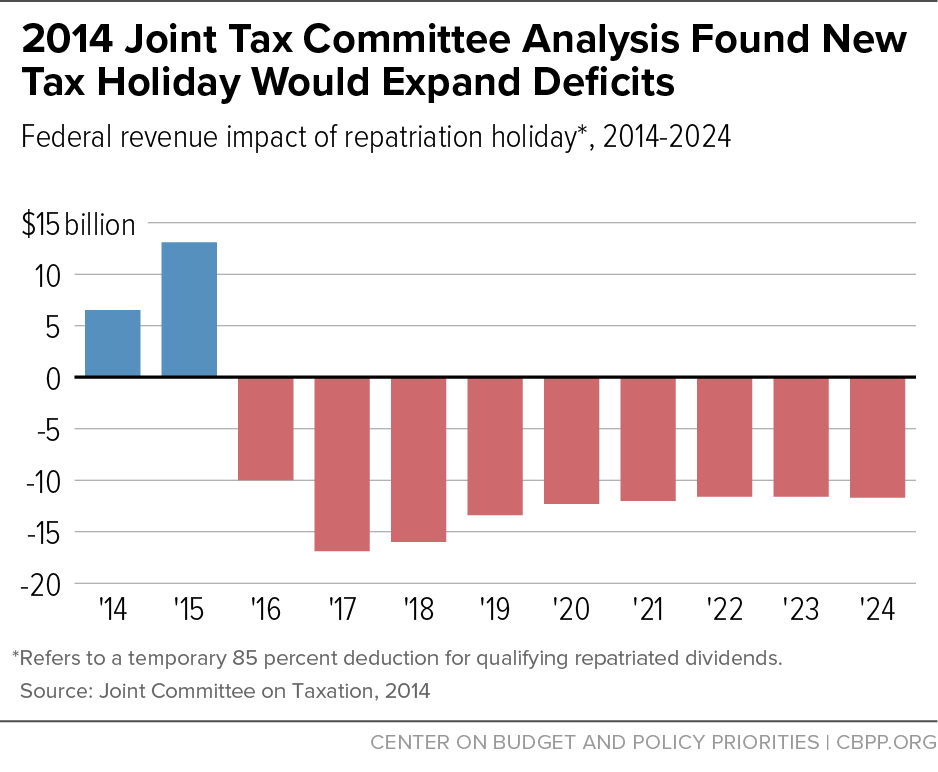

Enacting a second repatriation tax holiday would boost revenues during the holiday period as companies rushed to take advantage of the temporary low rate, but would bleed revenues thereafter. A two-year holiday at a tax rate of 5.74 percent would lose $96 billion over 11 years, JCT estimated in 2014 (see Figure 2).[10] As JCT explained, the biggest reason for the revenue loss over time is that a second holiday would encourage companies to shift more profits and investments overseas in anticipation of more tax holidays, thus avoiding taxes in the meantime.

Because a repatriation tax holiday loses revenue, claims that it can pay for infrastructure are mistaken. Senators Rand Paul (R-KY) and Barbara Boxer (D-CA) proposed in 2015 a repatriation tax holiday at a 6.5 percent rate that they claimed could help finance infrastructure investment.[11] But JCT estimates that their proposal would lose $118 billion over ten years, so it couldn’t finance infrastructure spending.[12]

Key Differences Between a Transition Tax and a Repatriation Holiday

1. A transition tax is compulsory and raises revenues; a repatriation tax holiday is optional and loses revenues. As noted, the President’s proposed transition tax would raise $299 billion over 2016-2025. Because the revenues stop flowing in after the transition period, it makes sense to use them for one-time infrastructure investments, as the President proposes. A repatriation holiday, in contrast, reduces revenues over time.

2. A transition tax is part of corporate tax reform that can be designed to reduce or eliminate incentives to shift profits and investments offshore; a repatriation tax holiday increases those incentives. A transition tax would be coupled with corporate tax reforms that could be designed to reduce or eliminate the incentive for companies to shift profits offshore. The President, for example, has proposed a 19 percent minimum tax on future offshore profits, so multinationals could no longer defer tax on their foreign profits until choosing to repatriate them. By contrast, a repatriation tax holiday is a stand-alone tax cut that lacks such reforms; it would strongly encourage firms to shift profits and investment offshore in subsequent years in anticipation of another tax holiday.

3. A transition tax could bring other benefits as part of corporate tax reform. Unlike a repatriation tax holiday, which has been shown to provide none of the promised economic benefits, a transition tax could yield economic benefits if used for one-time investments, such as infrastructure, or to reduce the deficit.

The most fiscally responsible approach would be for corporate tax reform to reduce deficits. But even a reform package that is revenue neutral should meet the revenue-neutrality standard over the long run as well as in the initial ten-year budget window. Otherwise, policymakers could use timing gimmicks to craft a corporate tax reform package that is revenue neutral over the first ten years but swells deficits and debt after that.[13]

Stand-alone Deemed Repatriation

A “stand-alone deemed repatriation” is in many ways a hybrid between a repatriation holiday and a transition tax. Like a transition tax, it would be compulsory and deem overseas profits to have been repatriated and subject to U.S. tax. Unlike a transition tax, it would be a stand-alone measure not coupled with a permanent reform to the international tax system.[14] How a stand-alone deemed repatriation would impact revenues and tax avoidance would depend on the rate.

-

If the deemed repatriation rate is set low, it would work more like a repatriation tax holiday. Imagine if a deemed repatriation rate were set at the 5.25 percent rate offered under the 2004 repatriation tax holiday. Even though companies would be required to treat all their offshore profits as having been repatriated and subject to the tax, because the rate is so low, they would likely choose to repatriate most of their profits even if the tax were instead structured as a voluntary “holiday.”

Like a repatriation tax holiday, a deemed repatriation would generate one-time revenues. But revenues would be lost on some of the profits repatriated at the low 5.25 percent rate that would have otherwise been repatriated over time at the normal 35 percent statutory rate. A deemed repatriation at a low rate would also encourage multinationals to expect that future deemed repatriations or tax holidays will be set at a similarly low rate. Thus, also like a repatriation tax holiday, a deemed repatriation at a low rate would encourage multinationals to shift more profits offshore in the future (because it would make them more confident that any eventual U.S. tax on those profits would be far lower than 35 percent). This would further bleed future revenues.

- If the deemed repatriation rate is set high (close to the 35 percent statutory rate), it would work more like a transition tax. For example, consider a deemed repatriation rate at or very near to the 35 percent statutory rate. The higher rate would generate more initial revenues from the deemed repatriation. In addition, to the extent that some of the profits deemed to have been repatriated would have been repatriated voluntarily over time at the usual 35 percent rate, the loss of revenue on those future repatriations would be smaller. Finally, the higher rate might alter multinationals’ expectations about the rate that they will eventually face on any future offshore profits — it could reduce their expectations that policymakers will offer them future tax holidays or deemed repatriations at much lower tax rates. That might therefore even reduce their incentive to shift profits offshore, and bolster future revenues.

- If the deemed repatriation rate is set between these two extremes, it is difficult to predict precisely how multinationals would respond.[15] Any “deemed repatriation” rate should be set as close to the 35 percent statutory rate as possible — at least high enough to avoid giving multinationals even more reason to shift future profits overseas. Otherwise, it would effectively act like a repatriation tax holiday, and would worsen tax avoidance and lose revenues in later years.[16] As with a transition tax, any one-time revenues from a “stand-alone” deemed repatriation should be dedicated to one-off investments or deficit reduction, and not paired with proposals that have lasting costs.

We are not aware of any congressional proposals for a deemed repatriation, though commentators and policymakers have discussed the option.[17]

End Notes

[1] Brandon DeBot co-authored the original version of this paper.

[2] U.S. House of Representatives Committee on Ways and Means, “Brady, Neal Highlight Another Reason for Pro-Growth Tax Reform,” September 29, 2016, http://waysandmeans.house.gov/brady-neal-highlight-another-reason-pro-growth-tax-reform/. Note that many of these so-called “offshore” profits are held in U.S. banks and assets: see Chuck Marr and Chye-Ching Huang, “Repatriation Tax Holiday Would Lose Revenue and Is a Proven Policy Failure,” Center on Budget and Policy Priorities, June 19, 2014, http://bit.ly/1Oec6gY, Box 3.

[3] John D. McKinnon, “Idea for Corporate Tax Holiday Gains Bipartisan Traction in Senate,” Wall Street Journal, January 29, 2015, http://on.wsj.com/162WHPg.

[4] The White House, “Press Briefing by Senior Administration Officials on the President's FY2016 Budget,” February 2, 2015, https://www.whitehouse.gov/the-press-office/2015/02/02/press-briefing-senior-administration-officials-presidents-fy2016-budget.

[5] President’s Fiscal Year 2017 Budget Summary Tables, https://www.whitehouse.gov/sites/default/files/omb/budget/fy2017/assets/tables.pdf. For more, see: Chye-Ching Huang, “Obama’s Transition Tax on Offshore Profits Is Sound, But a Higher Rate Would Bring More Revenue Without Adverse Economic Effects,” Center on Budget and Policy Priorities, November 13, 2014, http://bit.ly/1tRBjYK.

[6] Jane G. Gravelle, “Statement of Jane G. Gravelle, Senior Specialist in Economic Policy, Congressional Research Service, Before The House Ways and Means Committee on Select Revenue Measures, United States House of Representatives,” June 24, 2015, http://waysandmeans.house.gov/wp-content/uploads/2015/06/2015-06-24-SRM-Gravelle-Testimony.pdf.

[7] Senate Finance Committee, “International Tax Reform Working Group: Final Report,” July 7, 2015, http://www.finance.senate.gov/download/the-international-tax-bipartisan-tax-working-group-report.

[8] The White House and the Department of the Treasury, “The President’s Framework for Business Tax Reform: an Update,” April 2016, https://www.treasury.gov/resource-center/tax-policy/Documents/The-Presidents-Framework-for-Business-Tax-Reform-An-Update-04-04-2016.pdf, p. 28.

[9] For more, see Marr and Huang, 2014.

[10] Senate Finance Committee, “JCT Estimates Repatriation Tax Holiday Would Cost $95 Billion,” June 9, 2014, http://www.finance.senate.gov/ranking-members-news/jct-estimates-repatriation-tax-holiday-would-cost-95-billion.

[11] Chuck Marr, “Paul-Boxer Repatriation Tax Holiday Can’t Pay for Highways,” Center on Budget and Policy Priorities, January 29, 2015, http://bit.ly/1Dlnj9D.

[12] Joint Committee On Taxation, “Testimony Of The Staff Of The Joint Committee On Taxation Before The Select Revenue Measures Subcommittee Of The House Committee On Ways And Means Hearing On The Taxation Of The Repatriation Of Foreign Earnings As A Funding Mechanism For A Multi-Year Highway Bill,” June 24, 2015, https://www.jct.gov/publications.html?func=startdown&id=4797. For more, see Chye-Ching Huang, “Paul-Boxer Repatriation Tax Holiday May Hide True Long-Term Costs,” Center on Budget and Policy Priorities, February 5, 2015, http://bit.ly/1v2GEaN.

[13] Chye-Ching Huang, Chuck Marr, and Nathaniel Frentz, “Timing Gimmicks Pose Threat to Fiscally Responsible Corporate Tax Reform,” Center on Budget and Policy Priorities, updated January 13, 2014, http://bit.ly/1Nu59q2.

[14] Such a deemed repatriation could be coupled with other tax and spending measures that do not fundamentally alter deferral or other central elements of the current international tax system. That is, such a proposal may still be part of a broader legislative package, but “stand-alone” in the sense of being a proposal that is separate from any major changes to the international tax system.

[15] The available scores of compulsory transition taxes and repatriation tax holidays do not provide enough information to predict how JCT would score the revenue impact of deemed repatriation taxes set at various rates.

[16] As Jane Gravelle has noted, whether or not the tax would apply to non-cash foreign profits held offshore would be another important determinant of the revenue impact.

[17] Ibid at p.5, and http://waysandmeans.house.gov/event/chairman-reichert-announces-hearing-on-repatriation-of-foreign-earnings-as-a-source-of-funding-for-the-highway-trust-fund/.

More from the Authors