The Legacy of the 2001 and 2003 “Bush” Tax Cuts

The biggest tax policy changes enacted under President George W. Bush were the 2001 and 2003 tax cuts, often referred to as the “Bush tax cuts” but formally named the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) and the Jobs and Growth Tax Relief Reconciliation Act of 2003 (JGTRRA). High-income taxpayers benefitted most from these tax cuts, with the top 1 percent of households receiving an average tax cut of over $570,000 between 2004-2012 (increasing their after-tax income by more than 5 percent each year). Despite promises from proponents of the tax cuts, evidence suggests that they did not improve economic growth or pay for themselves, but instead ballooned deficits and debt and contributed to a rise in income inequality.

What Were Their Main Features?

The 2001 and 2003 tax cuts reduced the top four marginal income tax rates (see Table 1), as well as the tax rate on capital gains and dividends. Reducing the top marginal tax rates (the tax on each additional dollar of income above a threshold) reduced the average tax rate (total tax liability as a share of total income) for all taxpayers with incomes above those thresholds. [1]

| TABLE 1 | ||

|---|---|---|

| Income Tax Rate Reductions Under the 2001 and 2003 Tax Cuts | ||

| Taxable Incomea | Previous Rate | New Rate |

| Below $17,000 | 15% | 10% |

| $17,000 — $68,000 | 15% | 15% |

| $68,000 — $137,000 | 28% | 25% |

| $137,000 — $209,000 | 31% | 28% |

| $209,000 — $374,000 | 36% | 33% |

| Above $374,000 | 39.6% | 35% |

The 2001 and 2003 tax cuts also phased out the estate tax, repealing it entirely in 2010.

In addition, the tax cuts included three components that are often referred to as “middle-class” tax cuts. One provision created a new bottom income tax rate of 10 percent for some of the income that was previously taxed at a 15 percent rate. Another provision increased the Child Tax Credit from $500 to $1,000 per child and made many low-income working families eligible for the credit.[2] The third provision was “marriage penalty relief” — a set of changes that reduced taxes for some married couples.

Many higher-income people benefitted from these provisions as well. All high-income taxpayers benefitted from the creation of a new 10 percent rate at the bottom, and some high-income married couples benefitted from the “marriage penalty relief” provision.

Nearly all of the tax cuts were originally scheduled to expire at the end of 2010, but policymakers extended many of their provisions for two years as a part of a budget deal in December 2010. This agreement reinstated the estate tax starting in 2011, but with a lower tax rate and higher exemption levels, applying only to the wealthiest estates (those worth more than $5 million per person or $10 million per couple, indexed for inflation).[3] The 2012 American Taxpayer Relief Act (ATRA) made permanent the tax provisions affecting low- and moderate-income households, but allowed certain tax rate cuts that affected only the highest-income taxpayers to expire, including restoring the top income tax rate to its previous level of 39.6 percent. The budget deal, enacted with President Obama’s support, made about 82 percent of the cost of the Bush tax cuts permanent.[4]

How Much Did They Cost?

The cost of the tax laws enacted during George W. Bush’s administration is equal to roughly 2 percent of gross domestic product (GDP) in 2010, the year the provisions were fully phased in.[5] This figure includes the amount the tax cuts increased the cost of “patching” the Alternative Minimum Tax (AMT) to keep the tax from affecting millions of upper-middle-class households, a problem the tax cuts helped to cause.[6]

At the time, many policymakers — including President Bush and Federal Reserve Chair Alan Greenspan — cited projected surpluses and falling debt as a reason to cut taxes.[7] But as the nation’s fiscal outlook changed, because the tax cuts were financed by borrowing, they added to a growing national debt.

The 2 percent of GDP cost figure does not include the extra interest costs resulting from the required borrowing. In 2013 CBPP estimated that, when the associated interest costs are taken into account, the Bush tax cuts (including those that policymakers made permanent) would add $5.6 trillion to deficits from 2001 to 2018.[8] This means that the Bush tax cuts will be responsible for roughly one-third of the federal debt owed by 2018.

Whom Did They Benefit the Most?

The largest benefits from the Bush tax cuts flowed to high-income taxpayers.

From 2004-2012 (the years for which comparable estimates are available), the top 1 percent of households received average tax cuts of more than $50,000 each year. On average, these households received a total tax cut of over $570,000 over this period. [9]

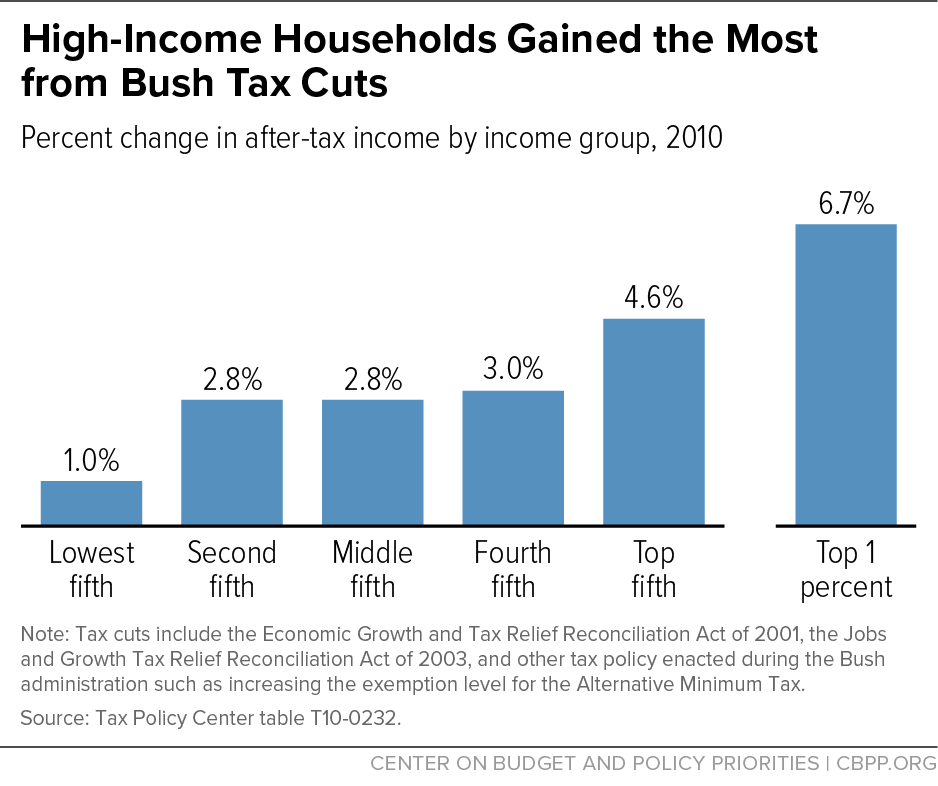

High-income taxpayers also received the largest tax cuts as a share of their after-tax incomes. The Tax Policy Center estimated that in 2010, the year the tax cuts were fully phased in, they raised the after-tax incomes of the top 1 percent of households by 6.7 percent, while only raising the after-tax incomes of the middle 20 percent of households by 2.8 percent. The bottom 20 percent of households received the smallest tax cuts, with their after-tax incomes increasing by just 1.0 percent due to the tax cuts.[10] (See Figure 1.)

How Did They Affect Economic Growth?

Policymakers enacted the 2001 and 2003 tax cuts with the promise that they would “pay for themselves” by delivering increased economic growth, which would generate higher tax revenues.[11] But even President Bush’s Treasury Department estimated that under the most optimistic scenario, the tax cuts would at best pay for less than 10 percent of their long-term cost with increased growth.[12]

Evidence suggests that the tax cuts — particularly those for high-income households — did not improve economic growth or pay for themselves, but instead ballooned deficits and debt and contributed to a rise in income inequality.[13]

In fact, the economic expansion that lasted from 2001 to 2007 was weaker than average. A review of economic evidence on the tax cuts by Brookings Institution economist William Gale and Dartmouth professor Andrew Samwick, former chief economist on George W. Bush’s Council of Economic Advisers, found that “a cursory look at growth between 2001 and 2007 (before the onset of the Great Recession) suggests that overall growth rate was … mediocre” and that “there is, in short, no first-order evidence in the aggregate data that these tax cuts generated growth.”[14]

In comparison, the economic expansion of the early 1990s — which followed considerable tax increases — produced a much faster rate of job growth and somewhat faster GDP growth than the expansion of the early 2000s.[15] An analysis of business activity between 1996 and 2008 found that even the sharp cut in dividend tax rates in 2003, which proponents claimed would spur immediate business growth, had no significant impact on business investment or employee compensation after 2003.[16]

And, when the tax cuts were scheduled to expire at the end of 2012, extending the high-income tax cuts in particular was projected to have almost no effect on economic growth. The Congressional Budget Office (CBO) estimated in 2012 that extending the high-income tax cuts would have boosted GDP by just 0.1 percent in 2013.[17] Indeed, allowing the high-income tax cuts to expire after 2012 does not appear to have had any substantial negative impacts on economic growth, as proponents of the tax cuts had claimed, and the economy has continued to grow steadily since then.[18] This is consistent with the broader empirical literature about taxes on high-income people and economic growth. As one comprehensive review of the empirical literature by three leading tax economists found, “there is no compelling evidence to date of real responses of upper income taxpayers to changes in tax rates.”[19]

End Notes

[1] For an explanation of the relationship between marginal and average tax rates, see “Policy Basics: Marginal and Average Tax Rates,” Center on Budget and Policy Priorities, updated July 9, 2015, https://www.cbpp.org/research/policy-basics-marginal-and-average-tax-rates.

[2] “Policy Basics: The Child Tax Credit,” Center on Budget and Policy Priorities, updated October 21, 2016, https://www.cbpp.org/research/federal-tax/policy-basics-the-child-tax-credit.

[3] “Policy Basics: The Estate Tax,” Center on Budget and Policy Priorities, updated July 5, 2016, https://www.cbpp.org/research/policy-basics-the-estate-tax.

[4] Chye-Ching Huang, “Budget Deal Makes Permanent 82 Percent of President Bush’s Tax Cuts,” Center on Budget and Policy Priorities, January 3, 2013, https://www.cbpp.org/research/budget-deal-makes-permanent-82-percent-of-president-bushs-tax-cuts.

[5] This figure is based on a compilation of Congressional Budget Office (CBO) cost estimates that includes both the revenue and outlay effects of all major tax legislation enacted during the George W. Bush Administration: the 2001 EGTRRA, the 2003 JGTRRA, the Working Families Tax Relief Act of 2004, and the Tax Increase Prevention and Reconciliation Act of 2005 (enacted in 2006). It also includes the costs of provisions extending these tax cuts in the American Recovery and Reinvestment Act of 2009. Based on analysis in Kathy Ruffing and Joel Friedman, “Economic Downturn and Legacy of Bush Policies Continue to Drive Large Deficits,” Center on Budget and Policy Priorities, February 28, 2013, https://www.cbpp.org/research/economic-downturn-and-legacy-of-bush-policies-continue-to-drive-large-deficits. For a detailed description of methodology used in this analysis, see box “What Did Bush-Era Tax Cuts Cost through 2011?” in Kathy Ruffing and James R. Horney, “Downturn and Legacy of Bush Policies Drive Large Current Deficits,” Center on Budget and Policy Priorities, updated October 10, 2012, https://www.cbpp.org/research/downturn-and-legacy-of-bush-policies-drive-large-current-deficits.

Another methodology for estimating the cost of the Bush tax cuts, which focuses on the initial costs of enacting the original 2001 and 2003 tax bills, finds that EGTRRA and JGTRRA combined decreased revenues by about 2.1 percent of GDP in 2004. See Jerry Tempalski, “Revenue Effects of Major Tax Bills Updated Tables for All 2012 Bills,” U.S. Department of the Treasury, February 2013, https://www.treasury.gov/resource-center/tax-policy/tax-analysis/Documents/WP81-Table2013.pdf.

[6] “Patching” the AMT refers to increasing the exemption level for the AMT, which was necessary in order to prevent a growing number of middle-class taxpayers from falling under the AMT. The rate reductions in the 2001 and 2003 tax cuts would have caused millions more taxpayers to fall under the AMT, undoing a significant portion of the tax cuts within the first ten years. The tax cuts thus increased the cost of patching the AMT each year in order to prevent these taxpayers from falling under the AMT. For more on the interaction between the 2001 and 2003 tax cuts and the AMT, see Aviva Aron-Dine and Bob Greenstein, “The AMT’s Growth Was Not ‘Unintended,’” Center on Budget and Policy Priorities, November 30, 2007, https://www.cbpp.org/research/the-amts-growth-was-not-unintended?fa=view&id=857.

[7] Frank Bruni, “Bush Defends Size of Surplus and Tax Cuts,” New York Times, August 22, 2001, http://www.nytimes.com/2001/08/22/us/bush-defends-size-of-surplus-and-tax-cuts.html, and John M. Berry, “Greenspan Supports a Tax Cut,” Washington Post, January 26, 2001, https://www.washingtonpost.com/archive/politics/2001/01/26/greenspan-supports-a-tax-cut/72f4925a-96d5-4120-8e0a-264a3d1d7476/?utm_term=.efda36f8cb0e.

[8] Ruffing and Friedman. This was our last update of this analysis.

[9] Average tax cuts are expressed in 2017 dollars. Tax change is distributed by percentiles of cash income adjusted for family size. These tax cuts include the full AMT patch, the rebates in the 2008 stimulus (which was passed under President Bush), and the initial phasedown of the estate tax through 2010. They do not include the tax provisions of the 2009 stimulus package (which was passed under President Obama) or the estate tax cuts in 2011 and 2012 that prevented the estate tax from returning to its original level after 2010. Chye-Ching Huang and Nathaniel Frentz, “Bush Tax Cuts Have Provided Extremely Large Benefits to Wealthiest Americans Over Last Nine Years,” Center on Budget and Policy Priorities, July 30, 2012, https://www.cbpp.org/research/bush-tax-cuts-have-provided-extremely-large-benefits-to-wealthiest-americans-over-last-nine.

[10] Tax Policy Center Table T10-0232. Tax change is distributed by percentiles of cash income adjusted for family size.

[11] The Joint Committee on Taxation (JCT) modeled the macroeconomic impact of most of the provisions in JGTRRA in 2003, and found that even under the most aggressive assumptions, economic growth generated by the tax cuts would decrease the revenue loss by less than 30 percent. See Joint Committee on Taxation, “Overview of the Work of the State of the Joint Committee on Taxation to Model the Macroeconomic Effects of Proposed Tax Legislation to Comply With House Rule XIII.3.(h)(2),” December 22, 2003, http://www.jct.gov/x-105-03.pdf.

[12] Jason Furman, “Treasury Dynamic Scoring Analysis Refutes Claims by Supporters of the Tax Cuts,” Center on Budget and Policy Priorities, revised August 6, 2006, https://www.cbpp.org/research/treasury-dynamic-scoring-analysis-refutes-claims-by-supporters-of-the-tax-cuts.

[13] “Chart Book: The Bush Tax Cuts,” Center on Budget and Policy Priorities, December 12, 2012, https://www.cbpp.org/research/chart-book-the-bush-tax-cuts.

[14] William Gale and Andrew Samwick, “Effects of Income Tax Changes on Economic Growth,” Brookings Institution, March 24, 2017, https://www.brookings.edu/wp-content/uploads/2016/07/09_Effects_Income_Tax_Changes_Economic_Growth_Gale_Samwick_.pdf.

[15] Aviva Aron-Dine, Richard Kogan, and Chad Stone, “How Robust Was the 2001-2007 Economic Expansion?” Center on Budget and Policy Priorities, updated August 29, 2008, https://www.cbpp.org/research/how-robust-was-the-2001-2007-economic-expansion.

[16] Danny Yagan, “Capital Tax Reform and the Real Economy: The Effects of the 2003 Dividend Tax Cut,” American Economic Review, 2015, https://eml.berkeley.edu/~yagan/DividendTax.pdf.

[17] Congressional Budget Office, “Economic Effects of Policies Contributing to Fiscal Tightening in 2013,” November 2012, https://www.cbo.gov/sites/default/files/112th-congress-2011-2012/reports/11-08-12-FiscalTightening.pdf.

[18] For more on the economic recovery since 2009, see: “Chart Book: The Legacy of the Great Recession,” Center on Budget and Policy Priorities, updated March 30, 2017, https://www.cbpp.org/research/economy/chart-book-the-legacy-of-the-great-recession.

[19] See Chye-Ching Huang, “Recent Studies Find Raising Taxes on High-Income Households Would Not Harm the Economy,” Center on Budget and Policy Priorities, April 24, 2012, https://www.cbpp.org/research/recent-studies-find-raising-taxes-on-high-income-households-would-not-harm-the-economy; and Chye-Ching Huang and Nathaniel Frentz, “What Really Is the Evidence on Taxes and Growth?” Center on Budget and Policy Priorities, February 18, 2014, https://www.cbpp.org/research/what-really-is-the-evidence-on-taxes-and-growth.