House GOP “A Better Way” Tax Cuts Would Overwhelmingly Benefit Top 1 Percent While Sharply Expanding Deficits

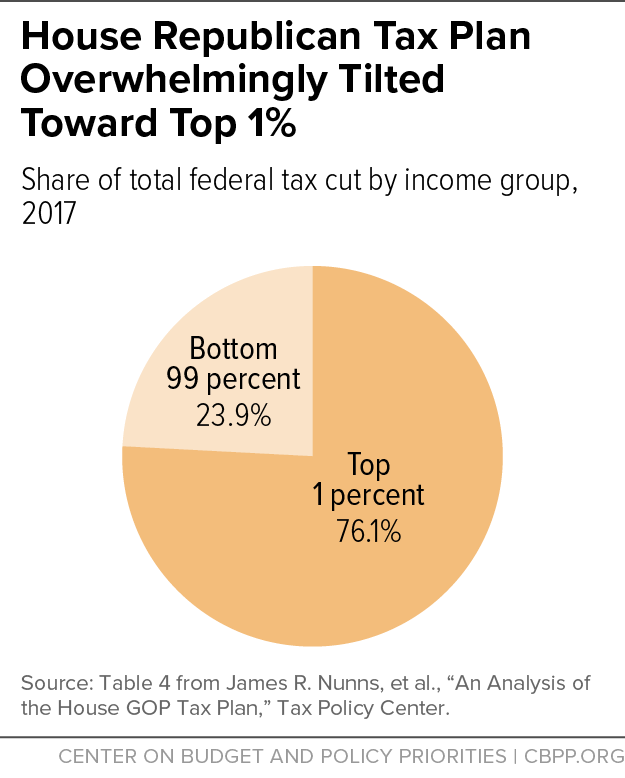

The policy agenda the House GOP issued this year includes a sweeping tax reform plan, which a new Tax Policy Center (TPC) analysis out today shows would overwhelmingly benefit the highest-income households. Under the plan, 76.1 percent of the net tax cuts would flow to the richest 1 percent of households in 2017. And by 2025, essentially all of the net tax cuts — 99.6 percent — would go to the top 1 percent. (See Figure 1.) The plan is more regressive and more heavily tilted toward those at the top of the income scale than past GOP tax cut proposals.The figures are similarly striking for households with incomes over $1 million, who would reap 71.2 percent of the tax cuts in 2017 and 96.5 percent of the net tax cuts in 2025.[1] The plan is actually more regressive and more heavily tilted toward those at the top of the income scale than past GOP tax cut proposals.

The TPC analysis also finds the plan would lose $3.1 trillion in revenue over the first ten years and $2.2 trillion over the second decade under a conventional approach to estimating the revenue impacts of tax changes. Although Speaker Ryan’s staff has said that the plan would be revenue neutral, the TPC analysis shows it would increase deficits very substantially, unless the plan were changed or accompanied by deep budget cuts to offset its cost. Relying on huge economic growth effects to help fill that hole would not be realistic. Even when counting revenues associated with economic growth estimated using a “dynamic” model that tends to generate larger growth impacts than the type of model most in line with empirical estimates, TPC finds that the plan would still cost more than $2.5 trillion.

Republican presidential nominee Donald Trump also has proposed costly and regressive tax cuts and has now modified his plan to align it somewhat more closely with the House GOP plan.[2] (Both plans now have the same top rate and include moves toward expensing of business investment and substantial reductions in the corporate tax rate.) This suggests that rather than being a moderating check on Mr. Trump in this area if he is elected, House Republicans could push still farther in terms of orienting new tax cuts toward the top.

Overview of House GOP Tax Plan

The House Republican leadership released the House GOP tax plan in June, as part of its “A Better Way” policy agenda. The plan makes major changes to both the individual income and corporate income tax and eliminates the estate tax entirely.

On the individual tax side, the new tax rate structure would have three brackets of 12 percent, 25 percent, and a top rate of 33 percent. High-income people’s pass-through income — business income that’s claimed on individual tax returns — would be taxed at a special lower top rate of 25 percent. The plan would cut the effective top tax rate on capital gains and dividends income from its current 23.8 percent (which is the tax rate on such income from income and payroll taxes combined) to 16.5 percent.

The plan would also make significant changes to tax deductions. It would increase the standard deduction and eliminate the personal exemption, effectively folding it into a larger Child Tax Credit. While the charitable and mortgage interest deductions would remain, the state and local tax deduction and various other itemized deductions would be eliminated.

On the corporate side, the corporate tax rate would be cut sharply to 20 percent from its current 35 percent. Businesses would be allowed to immediately deduct or expense the cost of new investments — instead of deducting the cost of those assets over time as they lose value — though they would no longer be allowed to deduct net interest payments. Various other changes to corporate taxation are described in detail by the TPC analysis.

House GOP Tax Plan Found to Be Extraordinarily Regressive

The House GOP’s tax plan is heavily lopsided: it provides very modest tax cuts, at most, to poor and middle-class people, and its major tax-cut provisions are targeted narrowly at the very top of the income and wealth scales. Moreover, if the tax cuts would ultimately be paid for through large budget cuts, as the House GOP budget framework (which calls for balancing the budget in ten years) requires, low- and middle-income families and individuals would likely end up significant net losers.

Low- and moderate-income earners would see a number of changes but no direct boost to their incomes from the tax cuts. The standard deduction, personal exemption, and Child Tax Credit would be reconfigured, and the two bottom current tax rates, 10 and 15 percent, would be merged into a new 12 percent bracket. The combined effect on people’s after-tax incomes, however, would be barely detectable. According to TPC, for both 2017 and 2025, the bottom four quintiles (i.e., the bottom 80 percent of Americans) would not see a change in after-tax income up or down of more than one-half of 1 percent (before considering the likely negative effects on these households of financing the package through budget cuts).

By contrast, the average after-tax income of the top 1 percent — households with incomes above roughly $700,000 a year, a group whose average income is $1.6 million — would increase by an average of $212,660 or 13 percent in 2017, TPC estimates. For the top one-tenth of 1 percent — a group whose average income is $7.5 million — average after-tax income would increase a stunning $1.3 million, an average of 17 percent.[3] Recent Census data show that median household income grew 5.2 percent in 2015, after adjusting for inflation, after years of stagnation. The House GOP tax plan would provide more than triple that percentage increase in after-tax income for this very high-income group.

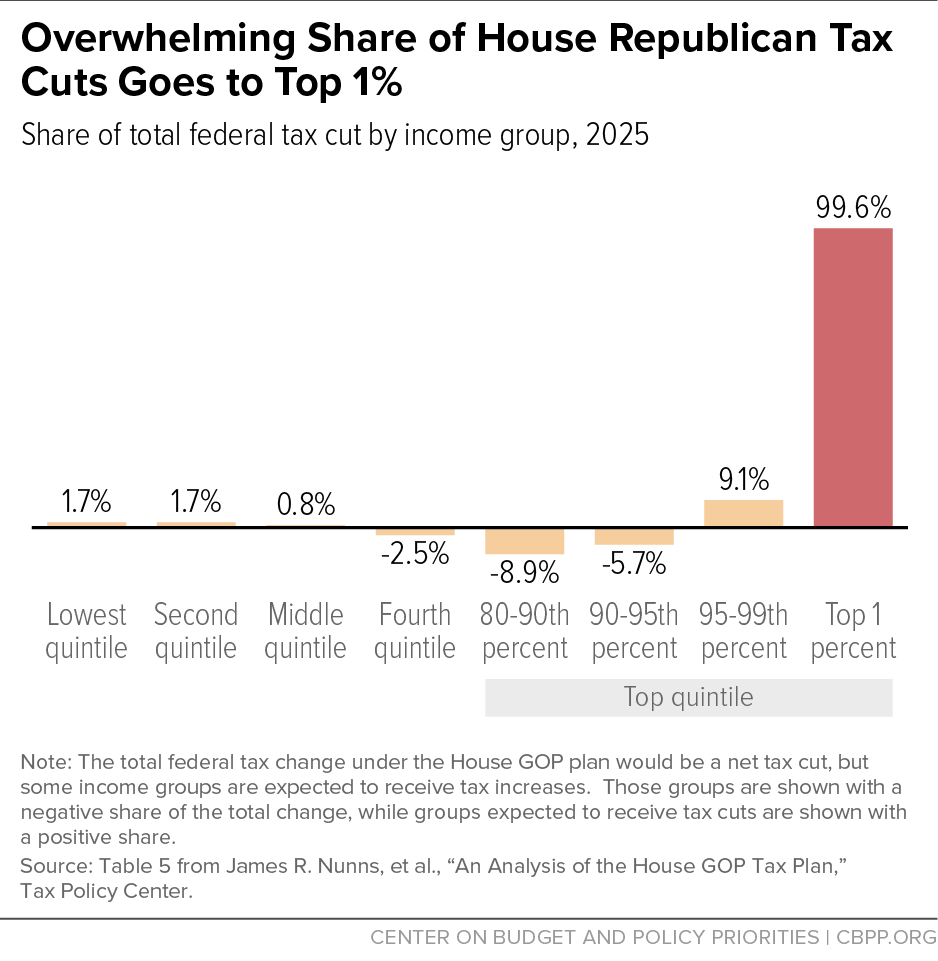

The picture gets even more stark in 2025, when TPC estimates that 99.6 percent of the plan’s net tax cuts would go to the top 1 percent (see Figure 2).[4] Because the plan contains a number of elements that either only have revenue effects in the first decade or have significant timing components, the 2025 estimates are likely to be more representative of the plan’s distributional impact over the long run.[5]

This massive windfall at the very top is due to the plan’s skewed tax cuts for individuals at the pinnacle of the income distribution, which on net overwhelm the smaller progressive revenue raisers in the plan. The tax cuts oriented toward the top include:

- Lower taxes on capital gains and dividends. This income is extremely concentrated, with 78 percent of long-term capital gains and 52 percent of qualified dividends flowing to the top 1 percent of households.[6] The House GOP plan eliminates the 3.8 percent Medicare tax now levied on this income. In addition, it provides an exemption from income tax for 50 percent of this income, which (combined with the plan’s reduction in rates) would reduce the top income tax rate on capital gains and dividends from its already favorable 23.8 percent to 16.5 percent.

- Special rate for pass-through business income. Pass-through income from businesses structured as partnerships, S corporations, and sole proprietorships can be claimed on individual income tax returns, thereby avoiding the corporate income tax. This income, too, is highly concentrated; in 2016, 54 percent of pass-through income flowed the top 1 percent of households and accounted for 23 percent of those households’ total income, according to TPC.[7] (Moreover, 87 percent of taxpayers with business income are already in tax brackets with tax rates of 25 percent or less and most of these face a rate of 15 percent of less.[8]) Pass-through income already enjoys generous tax advantages, but the House GOP plan would add to them by providing a special low individual tax rate of 25 percent on this income.

- Elimination of the estate tax. Currently, more than $10 million per couple of an estate is entirely tax-free. As a result, the estate tax affects the estates of only the wealthiest two of every 1,000 people who die — the top 0.2 percent. For the other 99.8 percent of Americans, there is no estate tax. For those few large estates that do face the tax, the average effective tax rate is below 20 percent. Nevertheless, the House GOP plan would eliminate the estate tax, which would benefit only the top 0.2 percent of estates and give very large tax cuts to heirs who receive multi-million-dollar inheritances.

- Cuts in corporate taxes. The plan includes a raft of corporate tax provisions that, on net, would lose substantial revenue in the first and second decades. Tax cuts on investment made through corporations flow primarily to corporate shareholders and other high-income investors. TPC takes into account the type of corporate tax cut and the length of time it has been in effect when assessing its distribution[9] and finds the overall net result of these provisions would tilt heavily to high-income households.

The distributional impacts of the plan would likely be still more skewed when the House GOP’s overall budget framework is taken into account. [10] The budget plan that the Republican majority on the House Budget Committee approved in March would cut programs for low- and moderate-income people by about $3.7 trillion over the next decade, and it promises to balance the budget in ten years without raising any revenues (and essentially holding Social Security and defense harmless). In 2026, it would cut programs for low- and moderate-income people by 42 percent overall, causing tens of millions of people to lose health coverage and millions to lose basic food or other support.

The House GOP budget plan also assumes that the House GOP’s tax proposals wouldn’t themselves add to deficits. Since the TPC estimates show the tax plan would lose several trillion dollars, for House leaders to reach their goal of balancing the budget over ten years, the budget cuts would need to be much deeper than those the House GOP budget already contains. Budget cuts of this magnitude would almost certainly more than wipe out any tax-cut benefit that low- and middle-income households would receive from the tax package.

The TPC estimates also pour cold water on claims that huge economic growth boosts from the plan would help to fill the revenue hole. The Tax Foundation estimates that such “dynamic” effects would reduce the costs of the House GOP tax plan by a large amount — from $2.4 trillion to under $200 billion. But, as we have recently explained, the Tax Foundation estimates should be viewed with great skepticism, as the model and assumptions on which they rest lie far outside the economic mainstream.[11] TPC uses assumptions that are closer to those used by mainstream economic analysts. In its analysis of the long-run impacts of the House GOP tax plan, TPC uses an “overlapping generation” (OLG) model, a type of model that tends to give larger growth impacts than the “Solow” models that produce results most in line with empirical estimates.[12] (TPC intends to add a Solow model to its line-up, but it is not yet complete.) Even using the OLG model, TPC estimates that macroeconomic effects would reduce the cost from $3.1 trillion over ten years to about $2.5 trillion, a far smaller percentage decrease from growth effects than the Tax Foundation estimates.[13] The TPC dynamic analysis also emphasizes that changing assumptions in the model can greatly alter the results of the analysis, and that “there is a substantial range of uncertainty in the macro forecasts” that its models make.[14]

End Notes

[1] James R. Nunns, et al., “An Analysis of the House GOP Tax Plan,” Tax Policy Center, September 16, 2016, http://www.taxpolicycenter.org/publications/analysis-house-gop-tax-plan, and TPC Tables T16-0196 and T16-0198, http://www.taxpolicycenter.org/simulations/house-gop-tax-plan-sep-2016.

[2] TPC estimated that 31 percent of tax cuts from the initial version of the Trump tax plan released last year would flow to millionaires, and 35 percent to the top 1 percent, in 2017. See James R. Nunns, et al., “Analysis of Donald Trump’s Tax Plan,” Tax Policy Center, December 22, 2015, http://www.taxpolicycenter.org/publications/analysis-donald-trumps-tax-plan. TPC has not yet analyzed the modified Trump tax plan that was revised yesterday.

[3] Average income from TPC Table T16-0072; other estimates from James R. Nunns, et al., “An Analysis of the House GOP Tax Plan.”

[4] The total federal tax change as a result of the House GOP plan would be a net tax decrease, but some income groups are expected to experience net tax increases.

[5] While both the individual income tax cuts and the corporate tax cuts are larger in the first decade than the second (both in dollar terms and as a share of GDP), this is particularly true for the corporate tax cuts. In large part, this is because one of the major tax provisions that affects corporations allows the cost of investments to be deducted in the year in which they are purchased instead of over time as the investments depreciate or lose value. The cost of this provision is much greater in earlier years as deductions are taken upfront, but some of that is reversed in later years when businesses no longer take depreciation deductions. This provision is paired with limiting deductions for interest.

[6] TPC Table T16-0195, http://www.taxpolicycenter.org/model-estimates/distribution-individual-income-tax-long-term-capital-gains-and-qualified-16.

[7] TPC Table T16-0181, http://www.taxpolicycenter.org/model-estimates/distribution-business-income-august-2016/t16-0181-distribution-business-income.

[8] TPC Table T16-0182, http://www.taxpolicycenter.org/model-estimates/distribution-business-income-august-2016/t16-0182-distribution-business-income.

[9] See James R. Nunns, “How TPC Distributes the Corporate Income Tax,” Tax Policy Center, September 13, 2012, http://www.taxpolicycenter.org/publications/how-tpc-distributes-corporate-income-tax.

[10] Richard Kogan and Isaac Shapiro, “House GOP Budget Gets 62 Percent of Budget Cuts From Low- and Moderate-Income Programs,” Center on Budget and Policy Priorities, March 28, 2016, https://www.cbpp.org/research/federal-budget/house-gop-budget-gets-62-percent-of-budget-cuts-from-low-and-moderate-income.

[11] Chad Stone and Chye-Ching Huang, “Trump Campaign’s ‘Dynamic Scoring’ of Revised Tax Plan Should Be Taken With More Than a Grain of Salt,” Center on Budget and Policy Priorities, September 15, 2016, https://www.cbpp.org/research/federal-tax/trump-campaigns-dynamic-scoring-of-revised-tax-plan-should-be-taken-with-more.

[12] Jane G. Gravelle, “Dynamic Scoring for Tax Legislation: A Review of Models,” Congressional Research Service, January 24, 2014, p. 17, http://graphics8.nytimes.com/packages/pdf/business/20140204_dynamic_scoring_report.pdf.

[13] Nunns et al., “An Analysis of the House GOP Tax Plan.”

[14] Nunns et al., “An Analysis of the House GOP Tax Plan,” p. 21.

More from the Authors

Areas of Expertise