The Capital Gains and Dividend Tax Cuts and The Economy

New Treasury Report Paints Misleading Picture

The Treasury Department recently released a report entitled “The Economic Effects of Cutting Dividend and Capital Gains Taxes in 2003.” While the text of the new document acknowledges that gains in the economy since 2003 “are the result of a combination of many factors,” the pictures that accompany the report communicate a less nuanced message. [1] The graphs display GDP, non-residential investment, and employment growth since the current economic recovery began in November 2001, and they highlight the fact that growth rates generally increased around the time of the 2003 tax cuts. The expected inference, of course, is that the 2003 tax cuts — and, in particular, the capital gains and dividend tax cuts — caused the improvement in the economy.

A more comprehensive look at the evidence, however, indicates that, while the dividend and capital gains tax cuts were indeed correlated with the upturn in the recover, they were not the cause of the improvement. In painting a simple picture of coincident timing, the Treasury documents omit many relevant facts, such as information regarding:

-

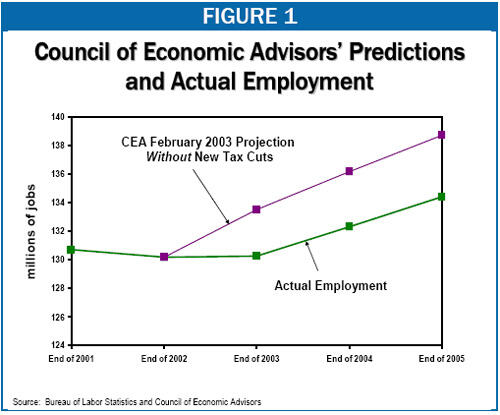

Likely economic conditions without the tax cuts. By the beginning of 2003, a number of significant factors were aligned to support the recovery, including very low short-term interest rates. As a result, as of early 2003, various expert observers, including Federal Reserve Chairman Ben Bernanke and economists surveyed by the Wall Street Journal, were predicting that GDP and investment growth would accelerate in 2003. Furthermore, the President’s own Council of Economic Advisors was predicting a significant increase in employment growth starting in 2003, even without additional tax cuts. In fact, while the Treasury report emphasizes employment gains that it implies are due to the 2003 tax cuts, actual employment at the end of 2005 was significantly below the level CEA predicted it would reach without the tax cuts (see Figure 1).

-

Implication of Treasury claims. Had the current recovery continued on the path it was on from November 2001 through mid-2003, it would have been the weakest recovery since World War II. In other words, by implying that the economy would not have improved without the 2003 tax cuts, Treasury is in essence claiming that, despite aggressive monetary policy by the Federal Reserve and significant tax cuts enacted in 2001 and 2002, this recovery would have been the worst in half a century. As noted, this was not the consensus among economists at the time.

-

Experiences in other recoveries. The path that the recovery followed after the recession in 2001 was very similar to the path of the 1990s recovery. Like the current recovery, the 1990s recovery was initially relatively weak, and growth accelerated about 18 months after the recovery began. In the case of the 1990s, however, the improvement was more pronounced than in the case of the current recovery, and the stronger growth coincided with a tax increase. If every economic change that followed a tax change was caused by that tax change, then the 1990s experience would show that tax increases provide more potent economic stimulus than tax cuts. The more appropriate lesson to draw may be that initially weak recoveries eventually tend to improve, independent of tax policy decisions.

-

Economic theory and evidence surrounding capital gains and dividend tax cuts. Capital gains and dividend tax cuts are generally understood to be “supply-side” tax cuts — that is, even if they “work,” their effects are felt in the long run, not as short-run economic stimulus. The Congressional Budget Office, for instance, found that “little fiscal stimulus would be provided by cutting capital gains tax rates.”[2] Conservative economist Gary Becker, a supporter of the dividend tax cut, wrote that it “will not yield immediate benefits…. Any short-run stimulus from eliminating the dividend tax would be too weak to have a significant benefit to the economy.”[3] Kevin Hassett, another conservative economist who supports the dividend tax cut, has called it “preposterous” to claim that reducing taxes on dividends created millions of new jobs.[4]

Some supporters of the capital gains and dividend tax cuts argue that they boosted the economy in the short run by boosting the stock market. A Federal Reserve study, however, found that the dividend and capital gains tax cuts were not the reason the market rose in 2003. (Not surprisingly, the Treasury report did not cite this Federal Reserve study.) -

Historical Norms. Even if one were to grant the claim that the tax cuts caused the improvement in the recovery, this would not establish that tax cuts are strong engines of growth. The current recovery, despite at least one major tax cut every year for four years, remains weak relative to past post-World War II recoveries. This means that the Administration and Congress have expended over $1 trillion in tax relief (through 2006), and wracked up correspondingly large budget deficits, without producing even an average economic expansion.

By trying to link the dividend and capital gains tax cuts to improvements in the economy since 2003, the Treasury Department presumably hopes to bolster the case for extending these tax cuts beyond their scheduled expiration at the end of 2008. Yet, even if one were to accept its findings, the Treasury report fails to build a compelling economic case for extending the tax cuts. If the main goal of these tax cuts were economic stimulus, and if they had succeeded in stimulating the economy, then the appropriate response would be to let them expire at the end of 2008, by which point they would have had ample time to work.

The more serious economic claims on behalf of the tax cuts, however, have to do with their effects on long-run growth. The real question is thus how these supposed positive growth effects compare with the negative effects of the increased deficits that would result from extending the tax cuts without paying for them. (While some have tried to argue that these tax cuts “pay for themselves” and thus do not add to deficits, this claim is inconsistent with the evidence and rejected by respected institutions such as the Congressional Budget Office; see the Appendix.) The negative effects of the resulting deficits on long-term growth may equal or outweigh any positive effects of the tax cuts. The Congressional Research Service, for example, found that the dividend tax cut “would harm long-run growth as long as it is based on deficit finance.”[5] The Treasury report ignores these issues, emphasizing instead its simpler, rosier pictures.

Improvement Expected with or without Tax Cuts

Contrary to tax cut boosters’ claims, there is no reason to believe that, without the tax cuts, the recovery would not have improved. Rather, there is good reason to think an upturn was likely regardless.

-

Already, in January 2003, before the capital gains or dividend tax cuts were even proposed, the Wall Street Journal’s survey of economists found that most thought “a modest economic recovery should take firmer root in 2003, led by businesses expected to pour their recuperating profits into investment.”[6]

-

Similarly, in February 2003, then Federal Reserve Board Governor and current Federal Reserve Board Chairman Ben Bernanke predicted “an increasingly robust economic recovery during this year and next” because of firms’ need to replace old capital, improvements in business cash flows, and diminishing uncertainty about geopolitical events.[7]

-

In addition to the factors named by Bernanke, various events that coincided with the 2003 tax cuts may have played a role in strengthening the recovery. For example, the Federal Reserve Board lowered interest rates to a 41-year low and oil prices fell, both in the same quarter as the tax cuts.

-

As of February 2003, the President’s own Council of Economic Advisors was predicting that employment growth would accelerate significantly beginning in 2003 — even without a new tax cut (see Figure 1 on page 1). At the end of 2005, total employment was more than four million below the level CEA predicted it would reach without the President’s proposed tax cut (and more than six million below what CEA forecast with the President’s proposed tax cut in place).[8]

An improvement in the economy thus was expected before the dividend and capital gains tax cuts were enacted. And it was not expected that the in the absence of these tax cuts, the recovery would remain as weak as it was at the start of 2003. If average growth rates had remained as low through the end of 2005 as they had been from the beginning of the recovery through mid-2003, growth in the Gross Domestic Product (the best measure of the size of the economy) and consumption, non-residential investment, net worth, wage and salary, employment, and revenue growth would all have been weaker in the current recovery than in any previous recovery since the end of World War II.

1990s Investment Growth Coincided with a Tax Increase

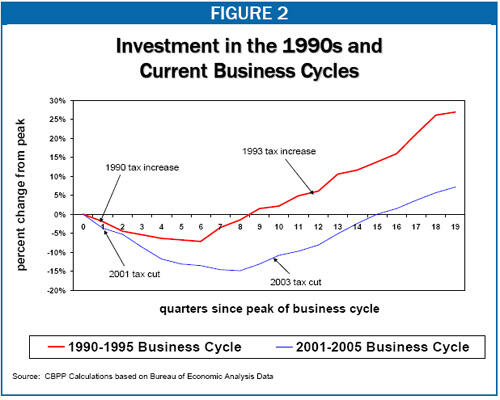

Also highly relevant is the case of the 1990s recovery, which followed or coincided with two significant tax increases. While the 1990s recovery was, overall, somewhat stronger than the current one, it followed a strikingly similar pattern. In both recoveries, GDP, investment, and employment growth were relatively weak during the early stages of the expansion and then began to improve about two years after the recovery began.

Figure 2 displays the same non-residential investment data highlighted in the Treasury graphs — but with the addition of data on non-residential investment growth during the 1990s. The graph shows that investment has indeed increased since the second quarter of 2003, when the capital gains and dividend tax cuts were enacted. But it shows that investment also increased at the point in the 1990s recovery that coincided with a significant tax increase. Further, the comparison shows that, overall, investment growth was much stronger during the 1990s recovery.

Based on the logic employed by some tax cut proponents, the graph should lead one to conclude that, while tax cuts are good for investment, tax increases are even better. The more appropriate lesson to draw may be that weak recoveries eventually tend to improve, whether there are tax cuts, tax increases, or no tax changes at all.

Dividend and Capital Gains Tax Cuts Did Not Function as Stimulus

While economists disagree about the ultimate merits of dividend and capital gains tax cuts financed by government borrowing, they generally agree that, to the extent these tax cuts help the economy, they do so in the long run, not the short run.

Writing about the dividend tax cut, Gary Becker, a conservative Nobel Laureate economist and supporter of the proposal, commented that “the tax cut will not yield immediate benefits;” its purpose is to “boost the economy in the longer run.” Becker continued, “Any short-run stimulus from eliminating the dividend tax would be too weak to have a significant benefit to the economy.” [9] Similarly, a statement by a group of economists, including ten other Nobel laureates, noted that the dividend tax cut “is not credible as short-term stimulus.”[10]

A Congressional Budget Office study found that the same was true of capital gains tax cuts: “in general, little fiscal stimulus would be provided by cutting capital gains tax rates.”[11] This is the case in part because the initial benefits of capital gains tax cuts (and of dividend tax cuts as well) are directed in large part toward investments that have already taken place. That is, rather than spurring new investment, the bulk of the initial benefits of the tax cuts go toward rewarding investment decisions that have already been made.

Simulations of the effects of dividend and capital gains tax cuts have found they are highly ineffective as economic stimulus. An Economy.com study found that reducing the taxation of dividends and capital gains would generate less than a dime of stimulus for each dollar of lost revenue; a Goldman Sachs analysis estimated the dividend tax cut would provide eight cents of stimulus for each dollar of cost.[12] (By comparison, Economy.com estimated that more efficient stimulus proposals such as extending federal unemployment benefits would yield more than a dollar of stimulus per dollar of revenue loss.)

Evidence available so far confirms the simulation results and economic theory: the dividend and capital gains tax cuts have had little short-run impact. For instance, supporters of the tax cuts frequently claim that the tax cuts influenced the economy in the short run by boosting the stock market. But a study by three Federal Reserve economists finds that the tax cuts were not the reason the stock market rose in 2003.[13] The study compared the performance of taxable stocks in the United States to the performance of European stocks and Real Estate Investment Trusts; it thus was able to separate out correlation — the market’s rise did coincide with the tax cuts — from causation: the tax cuts were not the cause of the market’s rise. (The Treasury report neglected to cite this Federal Reserve study.)

Huge Tax Cuts Have Yielded a Below Average Recovery

The Treasury report, and other recent claims by tax-cut supporters, in part conflate the effects of the 2003 dividend and capital gains tax cuts with the effects of other tax cuts enacted in 2003, and even with tax cuts enacted in earlier years. Since 2001, Congress has enacted and the President has signed legislation providing over $1 trillion in tax relief between 2001 and 2006. Considered as a whole (and in contrast to the dividend and capital gains tax cuts considered in isolation), this massive tax-cut infusion probably did have some impact on the economy.

But the enacted tax cuts provided relatively little economic stimulus given their very high cost. While a few of the smaller tax-cut provisions — for example, the temporary bonus depreciation provision included in the 2002 tax cut bill — were designed to have high “bang for the buck” in stimulating the economy, the majority of the tax cuts’ were poorly designed for short-term stimulus. They were backloaded, were provided to high-income taxpayers who have a lower propensity to consume additional income, or were targeted at encouraging saving, not consumption or immediate investment. For this reason, studies of the tax cuts have concluded that they did little for the economy relative to alternative stimulus options and “played a relatively minor role in the economic recovery compared with other factors.”[14]

Moreover, overall, the economic recovery is still below average, relative to other post-World War II recoveries, with respect to growth in GDP, investment, net worth, consumption, employment, and wages and salaries; only corporate profits have grown rapidly.[15] If tax cuts are crucial to economic growth, then with at least one major tax cut a year for four straight years, the current recovery should stand out brightly in comparison to previous recoveries. Instead, it has remained comparatively weak, particularly with respect to job creation. Overall employment growth in this recovery has been slower than during any comparable post-World War II period.

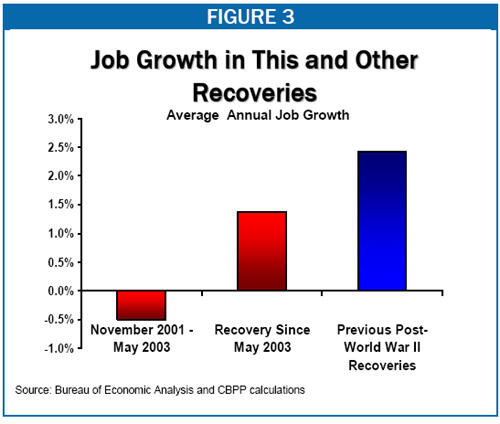

The new Treasury report highlights employment growth since 2003, again implying that the somewhat stronger growth in the second half of the recovery is due to the tax cuts. But again, the simple picture presented is incomplete. Figure 3 shows the data presented in the Treasury materials, with the addition of data on average job growth in previous post-World War II recoveries. While job growth has at least been positive in the second half of the recovery, as opposed to negative in the first half, it remains weak relative to historical norms. As noted above, it also remains weak relative to what the President’s Council of Economic Advisors predicted in February 2003 would occur even without the passage of the 2003 tax cuts. Relative to those CEA predictions, the economy at the end of 2005 was short more than four million jobs. The CEA forecasts assumed that employment would grow at a rate similar to the average for past recoveries; the shortfall relative to the CEA forecast thus reflects this recovery’s weakness relative to the average past post-World War II recovery.

Meanwhile, although the tax cuts have not produced strikingly strong economic growth, they have produced strikingly low revenue levels and have contributed to strikingly large budget deficits. If all of the tax cuts and Alternative Minimum Tax Relief are extended, revenues as a share of the economy over the next ten years are projected to remain below their average level in the 1960s, 1970s, 1980s, or 1990s, even as the baby-boom generation begins to retire.

Treasury Report Does Not Build a Case for Extending Capital Gains and Dividend Tax Cuts

If the main goal of the capital gains and dividend tax cuts were economic stimulus, and if these tax cuts had succeeded in stimulating the economy (as the Administration claims), the appropriate response would be to allow them to expire at the end of 2008, leaving them abundant time to complete their work. Moreover, there certainly would be no pressing need to extend these tax cuts immediately. Even Council of Economic Advisors Chair Edward Lazear, a strong supporter of the capital gains and dividend tax cuts, recently acknowledged that he does not “think there will be much effect on the market” from failing to extend them this year.[16]

The more credible economic claims on behalf of the tax cuts, however, have to do with their effects on long-run growth. While the Treasury report discusses these issues, it ignores crucial evidence that casts doubt on the value the tax cuts have for the economy in the long run.

Economists disagree about whether cutting dividend taxes affects long-run investment and growth or merely provides a windfall to current shareholders. The Treasury report keeps its discussion of this issue abstract and fails to mention an important empirical study of the 2003 dividend tax cut, by economists Alan Auerbach and Kevin Hassett, that found support for the latter view.[17] In presenting that study at an American Enterprise Institute event, Hassett commented that the findings implied it was “not likely that tinkering with the dividend tax rate will have much effect on investment.”[18]

Furthermore, even if the dividend and capital gains tax cuts did have some positive impact on efficiency and growth, this effect likely would be counterbalanced or outweighed by the negative effects of the additional deficits that would result from making the tax cuts permanent.

-

The Joint Committee on Taxation estimates that making these tax cuts permanent would cost $197 billion over the next decade; when additional interest costs are included, this means that extending the tax cuts would add $231 billion to deficits.

-

The Congressional Research Service has analyzed the 2003 dividend tax cut under a variety of assumptions and concluded that, in the long-run, “the dividend relief proposal would harm long-run growth as long as it is based on deficit finance” (emphasis added).[19]

-

Similarly, Brookings Institution economists William Gale and Peter Orszag found that, even if one adopts optimistic assumptions about the dividend tax cut’s impact on economic efficiency, as long as the tax cut continued adding to the deficit, “the net effects would be roughly a zero effect on long-term growth.”[20]

The Treasury report ignores the question of how the dividend and capital gains tax cuts’ costs compare with their benefits. Other supporters of these tax cuts imply that have no costs because they will “pay for themselves.” But this contention is refuted by the evidence and rejected by respected institutions such as CBO and the Congressional Research Service (see Appendix). A serious argument for extending the capital gains and dividend tax cuts would involve weighing their costs and benefits. It would not center around a mere chronological juxtaposition.

Appendix: The Tax Cuts and the Increase in Capital Gains Tax Receipts

Overall revenue growth during the current recovery has been exceptionally weak. Revenues, adjusted for inflation and population growth, have fallen at an average annual rate of 0.6 percent in this recovery; in contrast, during the average post-World War II recovery, revenues grew at an annual real per-person rate of 2.7 percent. In 2005, revenue growth finally improved, and the President, Vice-President, and certain Congressional leaders have seized on this growth to argue that the tax cuts enacted in 2001 and 2003 have “paid for themselves.” But this claim is refuted by the evidence and rejected by credible economists across the political spectrum. [21]

Recently, the debate over tax cuts and revenues has been fueled by new CBO estimates of capital gains tax receipts over the 2003-2005 period. In its January 2006 Budget and Economic Outlook report, CBO showed that capital gains realizations and the resulting revenues were higher than had been originally projected. Some have tried to argue that this unanticipated increase in capital gains receipts indicates that the capital gains tax cut boosted the economy and that extending the tax cut will increase rather than reduce revenues.

Unexpected Capital Gains Receipts Growth Not Linked to Economic Growth

For unanticipated increases in capital gains receipts to indicate that the capital gains tax cut boosted the economy, the unanticipated receipt growth would have to be linked to unanticipated economic growth. But in fact, stronger-than-expected capital gains receipts could not have resulted from stronger-than-expected economic growth because growth was slightly weaker than was expected at the point in early 2004 when the lower capital gains receipts were forecast. Although capital gains receipts in 2004 and 2005 were higher than CBO forecast in January 2004, actual growth of real economic activity turned out to be slightly lower in 2004 and 2005 than CBO had projected.

CBO raised its estimate of the level of capital gains revenues based on data showing that capital gains realizations were higher than would have been expected based on information about real economic activity and the tax rate on capital gains. Higher levels of realizations — that is, more people choosing to sell their assets and realize their gains — should not be confused with stronger economic growth. Investors may choose to accelerate gains for any number of reasons, but such timing decisions have no significant effect in boosting the economy in the short run.

What the higher capital gains realizations presumably do reflect, in part, is the rise in the stock market in 2003, when the market rebounded after three consecutive down years. The tax cuts, however, do not appear to have been the reason the stock market rose. As noted earlier in this analysis, a recent study by three Federal Reserve economists concluded that the capital gains and dividend tax cuts were not the reason the market went up.[22]

Unexpected Capital Gains Receipt Growth Does Not Mean Tax Cuts Raise Revenue

Some advocates of extending the capital gains tax cut have suggested that doing so would be costless because the tax cut will “pay for itself” or even raise revenue. For example, a recent Wall Street Journal editorial tells lawmakers not to worry about the projected budgetary cost of extending the capital gains tax cut because “the surest way to cost the Treasury money would be to let those tax rates increase.”[23]

As with their claims about the economy, proponents of extending the capital gains tax cut appear to have leapt to the conclusion that, because the increase in capital gains revenues followed a tax cut, it must have been caused by the tax cut. Again, the experience of the 1990s may be instructive. As CBO describes in a recent letter, “substantial increases in [capital] gains of 40 percent, 25 percent, and 21 percent occurred in years immediately following the rate reduction [in capital gains tax rates] enacted in 1997. Those increases might suggest a large behavioral response to the tax rate cut — except that realizations also increased by 45 percent in 1996, before the rate cut. Thus, changes in realizations are not necessarily the result of changes in taxes; other factors matter as well.”[24]

Some tax cut proponents also suggest that CBO and the Joint Committee on Taxation systematically miss the positive impact of capital gains tax cuts on revenues and that lawmakers would be justified in ignoring the official cost estimates and assuming that extending the tax cut will pay for itself. In particular, some imply that CBO and the Joint Committee on Taxation ignore the behavioral effects of capital gains tax cuts — notably, that investors are likely to increase realizations in the initial years after capital gains tax rates are reduced. This, however, is not the case.

-

CBO and Joint Tax Committee estimates do account for the impact of tax cuts on capital gains realizations, reflecting higher realizations in the years after capital gains rate cuts. The estimates show that extending the capital gains tax cut would lose revenue, even given this behavioral effect.

-

CBO’s January 2006 Budget and Economic Outlook report notes that capital gains realizations in the past few years have been above historical norms relative to the size of the economy and the tax rate on capital gains. CBO explains that it does not expect this trend to continue because, in the past, capital gains realizations have reverted to historical norms over time. If capital gains realizations return to more normal levels, the growth of capital gains tax receipts will slow as well.

-

In its recent letter, CBO discusses its capital gains forecasting record and concludes that it “has not systematically underestimated realizations after reductions in capital gains tax rates.” Rather, it finds that capital gains realizations and revenues are "characterized by high volatility," influenced by a range of factors (such as changes in asset values, investor decisions, and broader economic trends) that make them hard to predict. But, according to CBO, "much of that volatility seems unrelated to changes in capital gains tax rates." [25]

Evaluating the arguments surrounding capital gains tax cuts, the Congressional Research Service concludes, “It appears that over the long run, the revenue generated from an increase in capital gains realizations accompanying a tax cut would not be large enough to offset the static revenue loss from the tax cut itself.”[26] Policymakers evaluating the merits of the case for extending the capital gains tax cut should take the cost into account, not ignore it.

End Notes

[1] Treasury Department, “The Economic Effects of Cutting Dividend and Capital Gains Taxes in 2003,” March 14, 2006.

[2] Congressional Budget Office, “Economic Stimulus: Evaluating Proposed Changes in Tax Policy,” January 2002.

[3] Gary Becker, “The Dividend Tax Cut Will Get Better with Time,” Business Week, February 10, 2003, p. 24.

[4] Robert Samuelson, “Presidential Prosperity Games,” Washington Post, December 21, 2005.

[5] Jane Gravelle, “Dividend Tax Relief: Effects on Economic Recovery, Long-Term Growth, and the Stock Market,” Congressional Research Service, March 28, 2003.

[6] John Hilsrenrath and Constance Mitchell Ford, “Economists Expect Spending by Businesses to lead Recovery,” Wall Street Journal, January 2, 2003.

[7] Remarks by Governor Ben S. Bernanke at the 41st Annual Winter Institute, St. Cloud, Minnesota, February 21, 2003, http://www.federalreserve.gov/boardsdocu/speeches/2003/20030221/default.htm.

[8] For further discussion, see Economic Policy Institute, “Job Watch: Tracking Jobs and Wages,” January 7, 2005, http://www.jobwatch.org/email/jobwatch_20050107.html.

[9] Gary Becker, “The Dividend Tax Cut Will Get Better with Time,” Business Week, February 10, 2003, p. 24.

[10] “Economists’ Statement Opposing the Bush Tax Cuts.” Available at http://www.epinet.org/stmt/2003/statement_signed.pdf.

[11] Congressional Budget Office, “Economic Stimulus: Evaluating Proposed Changes in Tax Policy,” January 2002.

[12] Mark M. Zandi, “Assessing President Bush’s Fiscal Policies,” Economy.com, July 2004 and Goldman Sachs, “Fiscal Policy — In Search of Balance, Creativity and Grit,” May 2, 2003.

[13] Gene Amromin, Paul Harrison, and Steve Sharpe, “How Did the Dividend Tax Cut Affect Stock Prices?” Federal Reserve Board Discussion Paper, December 2005, http://www.federalreserve.gov/PUBS/FEDS/2005/200561/200561pap.pdf.

[14] William Gale and Peter Orszag, “Bush Administration Tax Policy: Short-Term Stimulus,” Tax Notes November 1, 2004. See also Mark M. Zandi, “Assessing President Bush’s Fiscal Policies,” Economy.com, July 2004.

[15] For further comparisons, see Isaac Shapiro, Richard Kogan, and Aviva Aron-Dine, “How Does this Recovery Measure Up?” Center on Budget and Policy Priorities, revised January 9, 2006.

[16] Wesley Elmore, “White House Advisor Questions Effect of Failure to Extend Investment Tax Breaks,” Tax Notes March 15, 2006.

[17] For discussion of theories of how dividend tax cuts affect investment (in the context of the 2003 tax cuts), see Alan Auerbach and Kevin Hassett, “The 2003 Dividend Tax Cuts and the Value of the Firm: an Event Study,” OTPR/Burch Center Conference, May, 2005.

[18] Kevin Hassett, Presentation at American Enterprise Institute Forum, “How Did Firms Respond to the Dividend Tax Cuts?” November 8, 2005.

[19] Jane Gravelle, “Dividend Tax Relief: Effects on Economic Recovery, Long-Term Growth, and the Stock Market,” Congressional Research Service, March 28, 2003.

[20] William Gale and Peter Orszag, “An Economic Assessment of Tax Policy in the Bush Administration, 2000-2004,” Boston College Law Review, Vol. 45, No. 4, 2004.

[21] For a general discussion of claims that tax cuts caused these revenue increases and have “paid for themselves,” see Richard Kogan and Aviva Aron-Dine, “Claim that Tax Cuts ‘Pay for Themselves’ Is Too Good to Be True: Data Show ‘No Free Lunch Here,’” Center on Budget and Policy Priorities, March 8, 2006.

[22] Gene Amromin, Paul Harrison, and Steve Sharpe, “How Did the Dividend Tax Cut Affect Stock Prices?” Federal Reserve Board Discussion Paper, December 2005, http://www.federalreserve.gov/PUBS/FEDS/2005/200561/200561pap.pdf.

[23] Wall Street Journal, “Non-Dynamic Duo,” March 2, 2006.

[24] Congressional Budget Office, “CBO’s Methods for Projecting Capital Gains Realizations,” February 23, 2006, p. 3.

[25] Congressional Budget Office, “CBO’s Methods for Projecting Capital Gains Realizations,” p. 5.

[26] Gregg E. Eisenwein, “Capital Gains Tax Rates and Revenues,” Congressional Research Service, updated February 17, 2006.

More from the Authors

Areas of Expertise