What Would It Say about Congress’s Priorities to Waive PAYGO for the AMT Patch?

In January the House of Representatives reinstated “Pay-As-You-Go” (PAYGO) budgeting rules, and in May the Senate followed suit. PAYGO requires Congress to offset the cost of any legislation that increases entitlement spending or reduces revenues. As a CBPP analysis released today explains, Congress to date has complied with the PAYGO rules.[1] Both houses of Congress have offset the costs of legislation ranging from an expansion of the State Children’s Health Insurance Program (SCHIP) to increases in Pell Grants to increases in funding for renewable energy to implementation of recommendations of the 9/11 Commission.

One of Congress’s avowed goals for the rest of this year is to extend the Alternative Minimum Tax (AMT) “patch” through 2007. Because the AMT exemption level is not indexed for inflation, and because the 2001 and 2003 tax cuts reduced regular income tax rates without making corresponding changes in the AMT, the number of AMT taxpayers is expected to increase from about 4 million in 2006 to 23 million in 2007 in the absence of congressional action. The AMT patch is a temporary increase in the AMT exemption level that Congress has put in place each year since 2001 to keep the number of AMT taxpayers from exploding. It is an expensive fix; patching the AMT just for 2007 carries a price tag of $51 billion.

The House Democratic leadership has made clear that, like any other legislation, the AMT patch needs to be paid for, and the Ways and Means Committee last week adopted legislation that would patch the AMT for 2007 and offset the cost. But Senate Finance Committee Chairman Max Baucus, while saying that he would prefer to pay for a patch, has raised the possibility that the Senate may waive the PAYGO rules in order to deficit finance AMT relief. Some other members of the Senate Finance Committee have also expressed interest in waiving PAYGO for a patch.

The PAYGO rules reflect a few basic principles:

- Given the massive fiscal challenges the nation faces in coming decades, it is irresponsible to foist the cost of new budget and tax policies off on future policymakers and taxpayers; rather, policymakers should face up to these costs now.

- Things worth doing are worth paying for. Program expansions and tax cuts should be enacted only if they are valuable enough that it is worth scaling back other programs or increasing taxes to pay for them.

- Large, persistent deficits have costs for the economy; policymakers should therefore avoid adding to deficits and should pay for desired policy changes up front.[2]

If Congress were to waive PAYGO for the AMT patch, the clear message would be that the patch — unlike funding for children’s health care, student aid, or renewable energy — is “too important for PAYGO.” This claim is illogical on its face: it should be easier, not harder, to find spending worth cutting or taxes worth raising to pay for policies that are exceptionally important. But, even setting aside that point, none of the justifications that have been offered for why the AMT patch possesses unique importance withstand scrutiny. Rather, waiving PAYGO for the AMT patch for any of these reasons would signal misplaced priorities.

Rationale #1: The AMT patch is a crucial middle-income tax break.

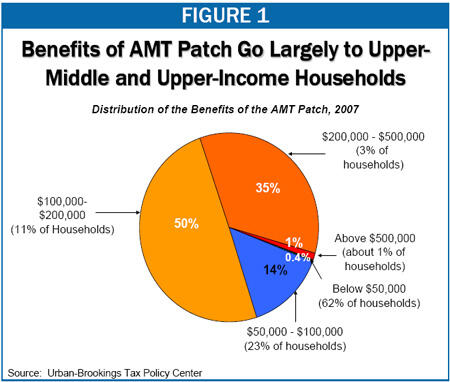

Reality: More than four-fifths of the benefits of a patch go to households with incomes above $100,000, a group that makes up just 15 percent of all households.

To be sure, 7 million people, or about a third of those who would be helped by the patch, have incomes below $100,000, according to estimates by the Urban Institute-Brookings Institution Tax Policy Center. But less than 15 percent of the tax benefits that the patch provides go to these individuals, while more than a third of the benefits go to people with incomes over $200,000. (See Figure 1.)

The reason for this disparity is that, under current law, large number of middle-income people will pay relatively small amounts in AMT taxes, while a smaller number of upper-income people will pay large amounts. Unless measures to reform the AMT are very carefully targeted, a large share of their benefits will go to those at high income levels.

It is instructive to compare the AMT patch with other policy changes — the costs of which Congress has offset — in terms of their impact on different income groups. Estimates from the Congressional Budget Office (CBO) show that the vast majority of the children who would gain health coverage under the SCHIP bill come from families with incomes below 200 percent of the poverty line (an income level that translates into about $40,000 for a family of four).[3] Similarly, most funding in the student aid bill recently signed into law went toward aid for low-income college students; the bill also included reductions in interest rates for subsidized student loans, which benefit the broad middle class. Investments in energy independence and homeland security presumably help all Americans.

Almost no one is seriously arguing that the AMT should not be patched; the question is whether the patch should be paid for. Waiving PAYGO for the AMT patch would signal that Congress applies fiscal discipline to policies that primarily benefit low- and moderate-income families, but not to those that primarily benefit people at higher income levels.

Rationale #2: The AMT’s growth was unanticipated and accidental.

Reality: Lawmakers not only anticipated the AMT’s growth, they counted on it to mask and defer the true costs of the 2001 tax cut. About three quarters of the cost of this year’s AMT patch is simply the price tag for keeping the AMT from taking back a large share of the tax cuts.

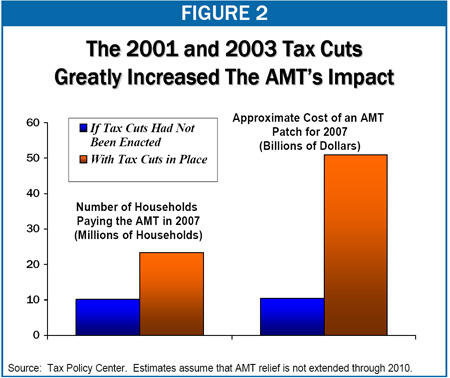

The Tax Policy Center estimates that, if the 2001 and 2003 tax cuts had not been enacted, 10 million taxpayers would owe AMT in 2007, and reducing that figure to 2-3 million would cost less than $15 billion.[4] With the tax cuts in place, however, about 23 million taxpayers are scheduled to owe AMT in 2007, and the patch will cost $51 billion, or more than three times as much. (See Figure 2.) These effects should come as no surprise to supporters of the 2001 tax cut, who knowingly used the AMT to mask and defer the tax cut’s true cost.

In the spring of 2001, when congressional leaders were formulating their large tax-cut package, they faced an obstacle. The budget resolution Congress approved that year allowed for tax cuts costing up to $1.35 trillion over ten years. The combined cost of all the tax cuts sought by the Administration and the congressional leadership, however, was much higher. Former Ways and Means Committee Chairman Bill Thomas described the “problem” as a need to get “a pound and a half of sugar into a one-pound bag.”[5]

Congressional leaders accomplished this goal by employing various gimmicks. Among the most important of these was the use of the AMT to dramatically reduce the tax cuts’ official cost.

Taxpayers owe AMT whenever their tax liability is higher as calculated under the AMT than as calculated under the regular income tax. Therefore, substantially reducing households’ tax liability under the regular income tax without changing what they owe under the AMT inevitably subjects more households to the AMT — and increases the amount of revenue the tax collects. The Joint Committee on Taxation explicitly brought this issue to Congress’s attention in the spring of 2001, when it provided lawmakers with estimates of how the tax cuts under consideration would increase the number of taxpayers hit by the AMT.

Congressional leaders could have chosen to act on the information the Joint Tax Committee provided, reforming the AMT so that it did not affect rapidly increasing numbers of households and so that taxpayers would receive the full value of whatever new tax cuts were enacted. But that would have meant scaling back other tax cuts under consideration in order to remain within the overall $1.35 trillion limit for the tax cut. So the congressional leaders chose instead to take advantage of the fact that, without a permanent AMT fix, the Joint Tax Committee would be required to estimate the cost of the 2001 tax bill on the assumption that the AMT would take back a substantial portion of its new tax cuts. This assumption dramatically reduced the bill’s “scored” cost, allowing more tax cuts to be squeezed in.

Meanwhile, tax cut supporters were confident that Congress would come back in future years and enact AMT relief without paying for it. That is, they anticipated that they would get the full tax cut, but they would only have to confront part of its cost up front. In short, the designers of the 2001 tax cut knowingly used the AMT as a massive gimmick to mask the true cost of the tax cut and the fact that, if fully implemented, it would blow through the $1.35 trillion amount Congress had allotted itself for the legislation.

As noted above, most of the cost of the 2007 AMT patch will simply go toward making sure the AMT does not take away taxpayers’ 2001 and 2003 tax cuts. To be sure, even those who question these tax cuts generally agree that the AMT is not the preferred mechanism for scaling them back. But making sure that upper-middle-income and upper-income households get the full value of tax cuts that weren’t really affordable in the first place does not seem like it should carry more weight than covering uninsured children or expanding college access. In addition, waiving PAYGO for the AMT patch would reward the dishonest budget gimmickry used to pass the 2001 and 2003 cuts.

Rationale #3: The AMT patch just holds households harmless, so it should not have to pass the same fiscal responsibility test as other legislation.

Reality: Deficit-financed legislation burdens future taxpayers and the economy whether its purpose is to hold people harmless or make them better off. And in other high-priority legislation considered this year, Congress appropriately chose to offset the cost of holding individuals harmless.

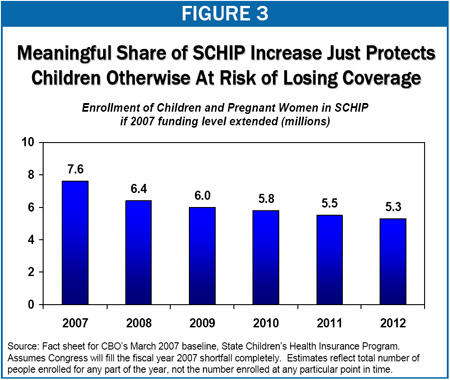

For example, although the SCHIP bill passed by both houses of Congress is typically described as a $35 billion program expansion (over five years), a substantial share of this sum is needed simply to maintain the current program. The Congressional Budget Office estimates that without increased funding, the program will serve 2.3 million fewer individuals by 2012. (See Figure 3.) Some initially argued that Congress should not have to offset the cost of filling this shortfall, but lawmakers correctly concluded that the principles behind PAYGO required offsetting the bill’s full cost.

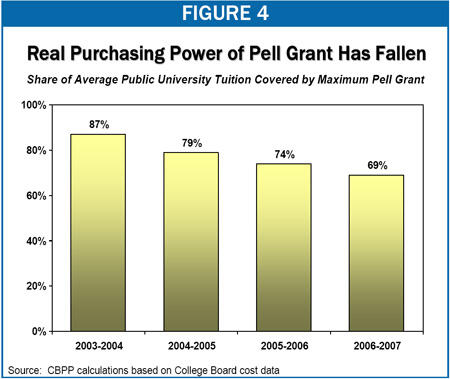

The recently enacted Pell Grant increase is another example. A very low-income student who started college in 2002-2003 at a school charging average public university tuition would have been eligible at that time for a Pell Grant covering almost 90 percent of that cost. If costs at her school simply increased at average rates, the student’s senior year Pell Grant would have covered only about two thirds of tuition.[6] (See Figure 4.) Indeed, if college costs continue to rise significantly faster than inflation, the recently enacted Pell Grant increase will barely maintain the maximum grant’s real purchasing power at its 2006-2007 level. But even though most or all of the recently enacted increase in student aid funding is needed just to hold students harmless, no one argued that the bill should receive a PAYGO waiver: however important its goals, deficit-financing its costs would be damaging.

Providing a PAYGO waiver for the AMT patch on the grounds that it merely holds households harmless would signal that Congress is more concerned with averting higher tax bills for relatively affluent individuals than with averting the loss of health coverage for low- and moderate-income students or reductions in the value of student aid for low- and moderate-income college students.

Rationale #4: AMT relief costs too much to subject it to PAYGO.

Reality: Abiding by PAYGO is more, not less, important when the legislation in question is expensive. And offsets are available that could cover the AMT patch.

The AMT patch is indeed more expensive than many of the other bills passed by Congress this year. But as a justification for a PAYGO waiver, this makes no sense. Logically, whatever the harms of deficit financing, they are larger for bigger bills.

Moreover, the claim that the AMT patch’s cost is so high that policymakers simply cannot offset it is not accurate. Last week, the House Ways and Means Committee adopted legislation that patched the AMT for 2007 and was fully offset. Meanwhile, a bill recently introduced by House Ways and Means Committee Chairman Charles Rangel includes offsets sufficient to cover the much larger cost of permanent AMT repeal. The Tax Policy Center and others also have offered a menu of options for covering the cost of permanent AMT reform or repeal.[7]

The core principle behind PAYGO is that things that are worth doing are worth paying for. Providing a PAYGO waiver for the AMT patch on the grounds that AMT relief is too expensive for PAYGO would signal disregard for the basic principles that motivated Congress to reinstate PAYGO rules in the first place.

End Notes

[1] Richard Kogan and James Horney, “The House Has Complied This Year With Its New ‘Pay-As-You-Go’ Rule, But Greater Challenges Lie Ahead,” Center on Budget and Policy Priorities, November 7, 2007, https://www.cbpp.org/11-7-07bud.htm.

[2] For further discussion, see Aviva Aron-Dine and Robert Greenstein, “The Economic Effects of the Pay-As-You-Go Rule,” Center on Budget and Policy Priorities, March 19, 2007, https://www.cbpp.org/3-19-07bud.htm.

[3] Center on Budget and Policy Priorities, “Bipartisan Legislation to Strengthen Children’s Health Care Focuses on Low-Income Children,” October 5, 2007, https://www.cbpp.org/policy-points10-5-07.htm.

[4] This estimate reflects what it would have cost to index the 2000 AMT exemption for inflation before the 2001 tax cut.

[5] “News Conference With Representative Bill Thomas, Chairman of the House Ways and Means Committee,” Federal News Service Transcript, March 15, 2001.

[6] Estimates of college costs are from: College Board, “Trends in College Pricing 2006,” http://www.collegeboard.com/.../press/cost06/trends_college_pricing06.pdf

[7] See for example: Leonard E. Burman and Greg Leiserson, “A Simple, Progressive Replacement for the AMT,” Tax Notes, June 4, 2007, http://www.taxpolicycenter.org/UploadedPDF/1001081_amt.pdf; Leonard E. Burman, William G. Gale, Gregory Leiserson, and Jeffrey Rohaly, “Options to Fix the AMT,” Tax Policy Center, January 19, 2007, http://www.taxpolicycenter.org/UploadedPDF/411408_fix_AMT.pdf; Citizens for Tax Justice, “A Progressive Solution to the AMT Problem,” December 2006, http://www.ctj.org/pdf/amtsolution.pdf.

More from the Authors