Getting Serious About Deficits?

Calls To Offset Hurricane Spending Miss The Point; Balanced Set Of First Steps Toward Fiscal Discipline Needed

Discussions have started in recent days about offsetting some or all of the expenditures that the federal government will need to make for relief and recovery from the recent hurricanes. From the standpoint of safeguarding the nation’s fiscal health, these discussions often seem inconsistent and confused.

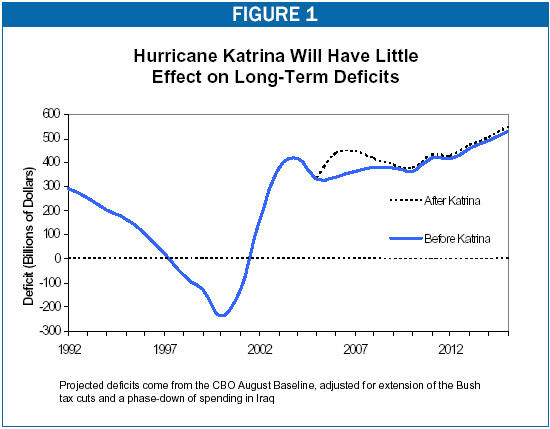

Many policymakers speak of the need to offset hurricane-related expenditures as though those expenditures pose a serious threat to the nation’s fiscal well-being. Yet most economists and fiscal policy analysts agree that those costs do not by themselves represent such a threat, as long as the costs remain temporary and end once the relief and reconstruction job is done.

The real threat to the nation’s fiscal — and ultimately, its economic — health is posed by the large mid-term and long-term deficits that loom as far as the eye can see. One-time costs for hurricane relief and reconstruction will worsen this problem only to the extent that they increase the interest costs the government will have to pay in future years as a result of having borrowed money to finance the hurricane-related activities. If we spend $200 billion for hurricane costs (and the likely amount now looks smaller than that) and borrow the entire amount, the projected deficit ten years from now will be about 3 percent higher than it otherwise would be, as a result of these added interest costs. This is not a large amount.

This is the reason that the budget enforcement rules of the 1990s, which contributed to the elimination of deficits during that decade, required entitlement increases and tax cuts to be offset but provided an exemption for one-time emergency spending. The one-time expenditures that the federal government incurred in response to those disasters that occurred during the 1990s did not prevent the achievement of a balanced budget in that decade.

Adding further to the confusion surrounding the current debate is that many policymakers who speak of the need to offset hurricane-related expenditures do not appear to be calling for similar offsets for the cost of hurricane-related tax cuts. Both the expenditures and tax cuts will add to short-term deficits.

Of greatest concern is the fact that some policymakers seem to be calling for offsetting the costs of temporary hurricane-related expenditures while planning to proceed with measures that will increase deficits on an ongoing basis, such as measures to extend tax cuts with an eye to later making them permanent, and doing so without offsetting the costs. Seeking to offset one-time emergency expenditures that will have little bearing on future deficits, but not to offset other policy actions that will make mid-term and long-term deficits even larger, stands sound fiscal policy on its head. From the standpoint of restoring fiscal discipline, such an approach is upside down.

Furthermore, some who are calling for budget cuts to offset the hurricane-related spending reportedly favor focusing those cuts heavily on basic assistance programs for the poor, such as Medicaid, food stamps, and welfare reform funding, even as tax cuts primarily benefiting high-income households are extended and further enlarged.[1] Asking Americans at the bottom of the income scale to bear the heaviest burden in offsetting the hurricane-related costs seems inconsistent with the President’s declaration, in his nationwide address on September 15, that “we have a duty to confront this poverty with bold action.

One example of the confusion that surrounds the current debate is the call by the Republican Study Committee, a group of the House of Representatives’ most conservative members, for a one-year delay in implementing the Medicare prescription drug benefit as a way to offset some of the hurricane-related costs. Under the RSC proposal, the prescription drug legislation would take effect in its current form, without any economies being achieved in it, but with the start date pushed back 12 months to January 1, 2007. Such an action would have virtually no discernible effect on mid-term and long-term deficits. A much sounder approach involving Medicare would be to allow the drug benefit to take effect as scheduled on January 1, 2006, but to make changes in that legislation and other Medicare rules related to the Medicare payment system to reduce Medicare costs on an ongoing basis. In June, the Medicare Payment Advisory Commission, Congress’ official expert advisory board on Medicare payments, warned that billions of dollars of excessive and unwarranted payments will be made to managed care companies under the prescription drug legislation and other Medicare rules, and that Congress should act to fix this problem. MedPAC recommended changes that would save $20 billion to $30 billion over five years and continue producing savings after that. Action to correct these overpayments would make much more sense than a one-year delay in the drug benefit.

The debate about offsetting the costs of hurricane relief and reconstruction thus has the potential to be a distraction from the real fiscal problems that the nation faces. Yet this debate also could present an opportunity for policymakers finally to start addressing the nation’s deep fiscal problems. Accordingly, this analysis discusses initial steps that policymakers can, and should, take to begin dealing with the daunting fiscal challenges that the nation faced even before the hurricanes — and that it continues to face now.

II. What Should be Done?

The nation needs major action by policymakers to put all parts of the budget — including revenues — on the table, to invoke a spirit of “shared sacrifice” and a willingness to target “weak claims” rather than “weak clients” (to use the felicitous phrase of David Stockman, President Reagan’s first budget director), and to start making tough choices. Sadly, action of this nature does not seem likely at the present time.

But policymakers can at least do two things now. First, they can take action to stop digging the long-term deficit hole deeper. Second, they can consider a balanced package of initial steps to start reducing the large long-term deficits that lie ahead. The remainder of this paper examines what policymakers could do in each of these areas.

STOP DIGGING THE HOLE DEEPER

Three steps should be taken here. Policymakers should reinstitute the “Pay-As-You-Go rules” that worked effectively in the 1990s. They should drop plans to use the fast-track “reconciliation” process in coming months to increase deficits. And they should forgo implementing scheduled tax cuts that have not yet taken effect unless the cost of those tax cuts is fully offset.

1. Reinstating the “Pay-As-You-Go” rules

In 1990, the first President Bush and Congressional leaders of both parties designed rules to require entitlement expansions and tax cuts (including extensions of supposedly temporary tax cuts) to be “paid for” through offsetting entitlement reductions or tax increases. (The rule contained an exception for expenditures or tax relief to meet emergency needs, such as relief and recovery from hurricanes, earthquakes, and other disasters.) This rule worked effectively through most of the 1990s, until budget surpluses emerged. It kept entitlement increases and tax cuts from enlarging the deficit, and it contributed to the remarkable improvement in the fiscal outlook that occurred in that decade. Virtually all of Washington’s principal “budget watchdog” organizations — the Concord Coalition, the Committee for Economic Development, the Committee for a Responsible Federal Budget, and the Center on Budget and Policy Priorities — have called for a return of these rules. So, on repeated occasions, has Federal Reserve Board Chairman Alan Greenspan. Such a step is long overdue.[2]

2. Dropping this year’s reconciliation legislation

The fast-track budget “reconciliation” procedures were originally designed to facilitate the passage of deficit-reduction legislation, by preventing such legislation from being subject to a filibuster in the Senate. In recent years, the original intent of reconciliation has been stood on its head, with the reconciliation procedures used to push through deficit-increasing legislation.[3]

Unfortunately, this year’s reconciliation directives continue that trend. The Congressional budget resolution adopted this spring calls for using the reconciliation process to pass legislation that would increase deficits by more than $35 billion over five years. The intended reconciliation legislation would include $35 billion in entitlement reductions and $70 billion in tax cuts, for a net increase in the deficit of $35 billion. (The actual increase in the deficit would be slightly larger because of the added interest payments on the debt that would have to be made.)

Apparently to mask the fact that the planned entitlement reductions — many of which would come in programs for the poor — would be used not to reduce the deficit but to defray a portion of the cost of the tax cuts, Congressional leaders this year split reconciliation into two bills: a bill intended to cut programs such as Medicaid, food stamps, and student loans, and a separate tax-cut bill. The two reconciliation bills are slated to move one week apart from each other. This cosmetic step, however, does not alter the bottom line — this year’s reconciliation legislation would increase deficits.

Adding to the disturbing nature of this use of the reconciliation process is the fact that it would likely increase hardship among poor Americans — potentially making people below the poverty line pay more for essential health care services and medications, and cutting food stamp benefits that already average only $1 per person per meal — in order to cover a portion of the cost of tax cuts that would go disproportionately to the most affluent people in the country. A centerpiece of the tax-cut reconciliation bill is expected to be an extension of the capital gains and dividend tax cuts that were enacted in 2003 and are slated to expire at the end of 2008. The Urban Institute-Brookings Institution Tax Policy Center reports that 53 percent of the benefits from these two tax cuts are going to the 0.2 percent of Americans who make over $1 million per year.

Instead of moving reconciliation legislation that would increase deficits while heightening hardship among those at the bottom of the income scale, Congress should identify those tax cuts slated to expire at the end of 2005that need to be extended — such as relief from the Alternative Minimum Tax — and extend them outside of the reconciliation process, through legislation in which their costs are offset, in accordance with the Pay-As-You-Go principle. A number of revenue options for offsetting the costs of these tax-cut extensions are available.

For example, in January 2005, the Joint Congressional Committee on Taxation — Congress’ official source of analysis, cost estimates, and advice on tax policy matters — issued a major report detailing options to achieve $190 billion in revenues over five years and $400 billion over ten years from closing unwarranted or unproductive tax breaks and improving tax compliance. Not all of the Joint Committee’s proposals would garner widespread support. But some are common-sense ways of closing especially dubious tax loopholes or curbing tax avoidance.[4] Revenues from a modest fraction of the Joint Committee’s proposals could offset the costs of extending tax cuts that are expiring and need to be extended now.

3. Shelving upper-income tax cuts that are not yet in effect

Recent tax cuts for upper-income Americans have been generous. The Urban Institute-Brookings Tax Policy Center reports that households with incomes of over $1 million are now receiving tax cuts from the 2001 and 2003 tax-cut legislation that average $103,000 a year. Nevertheless, on January 1, 2006, two costly new tax cuts that will exclusively benefit high-income households — and that were not requested by President Bush — will start taking effect for the first time. The nation cannot afford additional upper-income tax cuts. Accordingly, these tax cuts should be cancelled. (Alternatively, if policymakers are determined to institute them, their costs should be offset through reductions in other tax cuts for those at the top of the income scale.)

The two new tax cuts in question were enacted in 2001, when Congress added them to the tax package that President Bush submitted. Congress used a budget gimmick to fit the costs of these two measures into the overall amount available to it for tax cuts that year — it pushed off the start of these two tax cuts until 2006 and then phased the two tax cuts in gradually so they would not take full effect until 2010. That way, little of their cost appeared in the ten-year budget window that was being used to measure the cost of the 2001 tax-cut legislation.

One of the two new tax cuts in question repeals a provision of the tax code under which the personal exemption is phased out for people at high income levels. (This is sometimes referred to as the “PEP,” or personal exemption phase-out, provision.) The other new tax cut repeals a provision of the tax code under which limits are placed on the total amount of itemized deductions that taxpayers with high incomes may claim. (This is referred to as the “Pease” provision, after the Congressman who originally designed it.) Both of the tax-code provisions that the new tax cuts would repeal were signed into law by President Bush’s father as part of the landmark, bipartisan deficit-reduction law of 1990.

The scheduled implementation of these two new tax cuts on January 1 will benefit only households at high income levels. The Urban Institute-Brookings Tax Policy Center reports that when these two tax cuts are fully in effect, 54 percent of their tax-cut benefits will go to households with income of over $1 million a year, with those households getting an average annual tax cut of $19,200 from these two measures. The Tax Policy Center also found that nearly all (97 percent) of the benefits from these tax cuts will go to the 3.7 percent of households that have incomes of more than $200,000. The remaining three percent of the tax-cut benefits will go to households with incomes between $100,000 and $200,000, but the tax cuts will do little for most of those people; for households in the $100,000-$200,000 range, the average tax cut will be just $25.[5]

But while only a small slice of very affluent Americans will benefit substantially from these new tax cuts, the cost will be substantial. Assuming the two tax cuts are extended beyond 2010, the cost of these tax cuts will be $146 billion over the first ten years they are in full effect (2010 through 2019). When the added interest payments on the debt are taken into account, the total cost of the new tax cuts rises to nearly $200 billion over that ten-year period.

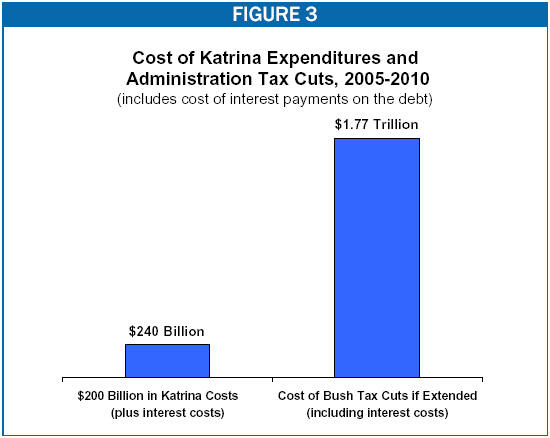

Thus, by 2020, the cost of the two new tax cuts, if extended, will roughly equal the total costs of relief and reconstruction from the recent hurricanes. Over the longer term, the cost of these new tax cuts will dwarf the costs resulting from the hurricanes. Shelving tax cuts such as these that are not yet in effect and that the nation cannot afford should be a basic component of efforts to stop digging the deficit hole deeper.

INITIAL STEPS TO START FILLING IN THE HOLE

As noted earlier, major bi-partisan efforts ultimately will be needed to make large-scale progress on the long-term fiscal problems the nation faces. Legislation will be needed to address the high and relentlessly rising costs of the U.S. health care system, to restore Social Security solvency, and to raise significantly more revenue. Unfortunately, such measures do not seem politically possible now. But policymakers should at least consider a balanced package of initial steps. Such a package would include both spending restraint and revenue enhancements. A package of initial, deficit-reduction measures could include the following.

1. Instituting MedPAC’s recommendations to rein in excessive payments to certain Medicare managed care plans

The Medicare Payment Advisory Commission (MedPAC), the official, independent advisory body to Congress on Medicare payment policy, issued a major report in June 2005 that calls for changes in how the Medicare program sets payment levels for managed care plans. MedPAC identified a large volume of excessive and wasteful payments that are being, or will be, made to such companies as a result of inefficiencies in the Medicare payment structure. (In some cases, the excessive payments result from mandates that Congress has imposed on the Medicare program at the companies’ behest.) MedPAC found that the excessive payments not only raise program costs but also tilt the “playing field” in favor of the companies receiving the excess payments, and accord those companies an unfair competitive advantage over traditional fee-for-service Medicare in seeking to attract patients. The MedPAC recommendations are based on extensive analysis of the amounts that Medicare pays different types of managed care plans and traditional fee-for-service providers to deliver the same health care services.

Congressional Budget Office estimates show that the MedPAC recommendations would save $20 billion to $30 billion over five years. The MedPAC recommendations include:

- Eliminating extra payments to certain new regional Preferred Provider Organizations, which will be on top of these PPOs’ regular Medicare fees and will place the total fees these PPOs receive above the fees paid to Medicare HMOs and the amounts spent to provide comparable services through traditional fee-for-service Medicare;

- Setting the base payment levels for all Medicare managed care plans (including both the new PPOs and Medicare HMOs) at the same level that it costs to treat beneficiaries with comparable health conditions through traditional Medicaid fee-for-service arrangements, rather than paying the managed care companies more than it would cost to treat the same patients through traditional Medicare; and

- Ending the practice under which the federal government essentially pays twice for some of the costs that teaching hospitals incur. Medicare pays twice for some of the costs that teaching hospitals incur in treating Medicare beneficiaries who are enrolled in managed-care plans, because Medicare makes an upward adjustment to cover these costs both in the payments that it makes directly to the hospitals and in the payments that it makes to the managed care plans that enroll these beneficiaries.)

2. Reforming agricultural subsidies

Mandatory spending on farm price support and income support programs is expected to total about $21 billion this year. Most independent policy analysts across the political spectrum agree that much of this spending is inefficient or unnecessary. A great deal of it goes to very large agricultural entities, not to small family farmers. Producers of some crops receive generous subsidies while producers of other crops get none.

Some of these subsidies (and some similar subsidies in other countries) also distort international markets and are a target of World Trade Organization efforts to liberalize would agricultural markets. Of particular concern, some of these subsidies apparently contribute to the depth and breadth of severe poverty and hunger in some of the world’s most impoverished countries by tilting markets away from poor farmers in those areas.

Various proposals have been made to reform the agricultural subsidies. One set of reforms is included in the budget that President Bush submitted in February. The Congressional Budget Office estimates that the President’s proposals to reform agricultural subsidies would save $7.5 billion over five years and $17.1 billion over ten years.

3. Paring back the earmarks in the highway bill

The recent highway legislation contains more than 6,300 earmarked projects at a total cost of over $22 billion, according to the Congressional Research Service. While some of these projects may be meritorious, others are not. CRS notes that of the congressional earmarks, 5,145 were designated as “high priority projects,” which is almost three times as many as the 1,849 similarly labeled projects in the previous highway bill.

A project that has gotten considerable play in the national press consists of two earmarks totaling $175 million to construct a bridge from Ketchikan, Alaska (pop. 13,000) to Gravina Island, Alaska (pop. 50), where the local airport is located. Tens of millions more would go for other, related projects in and around Ketchikan. According to the organization Taxpayers for Common Sense, the bridge would be taller than the Brooklyn Bridge and nearly as long as the Golden Gate Bridge and would replace the need for residents to reach the airport by taking a $6 ferry ride lasting seven minutes.

Highways are not the only source of wasteful or low-priority projects. According to a joint report by the National Wildlife Federation and Taxpayers for Common Sense, the budget of the Corps of Engineers includes numerous projects that either have little merit or would actually be harmful. The report lists projects such as the Grand Prairie irrigation project in eastern Arkansas at $319 million and the Big Sunflower River Dredging Project and Yazoo Backwater Pump at $243 million. According to the report, these projects and others like them would do significant environmental harm, are not designed to protect populations or property from floods, and would have only minor and local economic benefits that do not justify the costs.

4. Paring back special-interest tax breaks and expenditures in the recent energy and corporate tax bills

Over the past year, Congress has enacted two tax-cut packages laden with ill-advised targeted tax breaks — the corporate tax package in October 2004 and the energy bill in July 2005. Despite supporting the corporate measure, the Bush Administration complained bitterly about “a myriad of special interest tax provisions that benefit few taxpayers and increase the complexity of the tax code” that were inserted in the House and Senate bills. [6] Many of these provisions were retained in the final measure, including special tax breaks for ceiling fan importers, horse and dog racing, NASCAR, restaurants, and railroads, to name a few. Even the measure’s centerpiece tax cut for domestic manufacturers was so distorted by the end of the process that it, too, deserves “bad marks,” according to Congressional Research Service economist and tax expert Jane Gravelle, because it distorts investment decisions and imposes significant administrative and compliance costs.[7] In total, the measure included $130 billion of tax cuts between 2005 and 2014. Canceling just a fraction of these measures would yield significant savings.

The energy bill also included a number of special-interest tax breaks. For instance, the measure gave write-offs for electricity transmission equipment, natural gas pipelines, and oil refiner equipment, and provided tax credits for nuclear power production and clean-coal technology. (Taxpayers for Common Sense has compiled a list of dubious tax breaks and spending contained in the energy bill.[8])

The oil and gas producers who will benefit handsomely from the measure already pay federal taxes at a very low rate. Between 2001 and 2003, the federal taxes of the petroleum and pipeline companies in the Fortune 500 list averaged only 13.3 percent of their earnings, well below both the 35 percent corporate tax rate and the average effective tax rate for other industries.[9]

The special interest provisions in these bills should be reexamined and the bills’ costs pared back.

5. Ending other unproductive tax breaks, curbing tax shelters, and attacking tax avoidance

As noted earlier in this paper, Congress’ Joint Committee on Taxation issued an important report in January 2005 setting forth a series of specific options to eliminate questionable or unwarranted tax breaks and to help curb the extensive tax avoidance that now occurs. Taken as a whole, these options would save about $190 billion over five years and $400 billion over ten years. Some of the Joint Committee’s options would require taking on “sacred cows” and do not appear politically feasible. But numerous other options warrant serious consideration. Substantial savings could be at stake.

6. Reducing spending and raising revenues by using a more accurate measure of inflation

A number of federal entitlement programs, including Social Security, provide benefits that are adjusted each year to keep pace with inflation, as reflected in the Consumer Price Index. A number of features of the tax code also are adjusted annually for inflation, in accordance with changes in the CPI.

Research indicates that the CPI slightly overstates inflation. This is a judgment that most experts — including analysts at the Bureau of Labor Statistics, which maintains the CPI — share.

Accordingly, the Bureau of Labor Statistics has developed an alternative CPI, sometimes known as the “superlative CPI” or the “chained CPI,” which takes into account the tendency for consumers to buy more products whose prices have increased slowly and fewer products whose prices have increased rapidly. (For example, people who ordinarily purchase beef twice a week may switch to pork or chicken if the price of beef rises too high and the price of chicken or pork remains low.) The BLS began to issue inflation estimates using both the traditional CPI and this new “superlative CPI” in the summer of 2002. The superlative CPI is expected to rise, on average, about two-tenths of one percentage point less per year than the traditional CPI.[10]

It is a basic principle of federal policy that Social Security and other benefits should keep pace with inflation so that program beneficiaries do not lose ground as the years go by. Another basic principle is that the tax code should be adjusted for inflation so that taxpayers are not pushed into higher tax brackets or do not otherwise have their tax bills raised solely because of inflation. These principles surely should be maintained. But there is no need to adjust benefits or tax-code features by more than inflation.

Congress could address this matter by requiring that the programs and the parts of the tax code that are adjusted for inflation in accordance with the CPI by adjusted from now on in accordance with the superlative CPI. Such a change is best viewed not as a benefit cut or a tax increase, but as more of a technical change to achieve Congress’ stated goal of keeping pace with inflation in as accurate a way as possible.

In any year, the effects would be very small. Cost-of-living adjustments would on average be about two-tenths of a percentage point below what they would be if the old CPI were used. The long-term effects on the budget would be larger, however, because the effects would compound over time. In the 2004 Brookings Institution volume Restoring Fiscal Security (which also calls for this change), Brookings analysts estimated that if this change had taken effect in 2005, it would save about $35 billion a year by 2014, with those savings about equally divided between the program and revenue sides of the budget.[11]

The savings would continue to grow in years after 2014. This proposal thus has the virtue of phasing in slowly and producing savings that grow over time as the fiscal picture is darkening. In other words, the savings would mount as the need for savings increased.

It should be noted that over the past decade, the Bureau of Labor Statistics has made a number of other changes directly in the CPI itself that have significantly reduced the degree to which the CPI overstates inflation. These changes, which in combination are more than twice as large as the change proposed here, have been non-controversial. They have been incorporated directly into the official CPI and have affected the annual adjustments in Social Security, other programs, and the tax code without arousing opposition or protest. For technical reasons, the Bureau of Labor Statistics cannot incorporate the modest improvement reflected in the superlative CPI directly into the official CPI. That is why the BLS developed the superlative CPI alongside the traditional CPI.

This proposal also has one other benefit — by causing Social Security expenditures to be modestly lower than they otherwise would be, it would contribute to restoring long-term Social Security solvency. According to the Social Security actuaries, this proposal would close nearly one-fifth of Social Security’s long-term (i.e., 75-year) financing shortfall. (Under Congressional Budget Office estimates, the proposal would close about one-fourth of the shortfall.) The eminent Social Security expert and sage Robert Ball has endorsed this change as one of the steps that should be taken to restore Social Security solvency.[12]

Conclusion

Despite the flurry of recent statements about offsetting costs related to the hurricanes, there is little sign that policymakers are getting serious about mid-term and long-term deficits. In fact, there is considerable risk that between now and the time when Congress adjourns in November or December, it will take actions that increase mid-term and long-term deficits (through tax-cutting measures that cost more than its program cuts save) while making the lives of millions of the nation’s poorest citizens harsher. Such a course of action would be doubly unfortunate.

But there is still the possibility for the current focus on hurricane-related costs to provide an impetus for policymakers to start, at long last, taking steps to address the nation’s troubled fiscal outlook. This analysis suggests a series of balanced initial steps, involving both spending and revenues, that policymakers could take to stop digging the hole deeper and start making progress in closing the fiscal gap. These proposals represent only first steps. Much larger actions on both the program and revenue sides of the budget ultimately will be necessary.

End Notes

[1] Several news accounts have reported that House Republican leaders and leaders of the Republican Study Committee plan to focus cuts to offset the hurricane-related costs on Medicaid, food stamps, welfare reform, as well as across-the-board reductions in non-defense discretionary programs outside homeland security. See Ben Pershing, “GOP Still Seeking Spending Cuts,” Roll Call, September 28, 2005; and John Stanton, “Frist, GOP Leaders Move to Regain Footing in Debate Over Katrina Relief Spending,” CongressDailyAM, September 28, 2005.

[2] A reinstated Pay-As-You-Go rule should retain the emergency exception. Such an exception allows for an immediate response to devastating events like Hurricanes Katrina and Rita. As demonstrated by the progress during the 1990s from budget deficits to budget surpluses, such an exception does not significantly diminish the effectiveness of the Pay-As-You-Go rule.

[3] Both the 2001 and 2003 tax cuts were passed through use of the reconciliation procedures.

[4] For example, the Joint Committee recommended that some taxes be withheld when the federal government and state and local governments pay for goods and services. Such withholding would raise revenues by promoting improved tax compliance. Another Joint Committee proposal would require courts to apply tests to certain uncommon transactions to ensure these transactions are being undertaken for real business purposes rather than for tax-avoidance reasons.

[5] A modest number of households in the $75,000 to $100,000 range also will get tiny tax cuts from these two tax-cut measures. The average annual tax cut for households in this income range will be $1.

[6] Letter from Treasury Secretary John Snow to Rep. William Thomas, October 4, 2004.

[7] Jane Gravelle, “The 2004 Corporate Tax Revisions as a Spaghetti Western: Good, Bad, and Ugly,” April 2005, presented at the National Tax Association Spring Symposium, May 19-20, 2005.

[8] Taxpayers for Common Sense, “Top Ten Worst Provisions in the $85 Billion Conference Energy Bill,” July 27, 2005.

[9] Citizens for Tax Justice, “Conference Committee Energy Bill Rewards Corporate Tax Avoiders, Creates Conflicting Incentives,” July 28, 2005.

[10] The Social Security actuaries estimate the average annual difference to be 0.22 percent.

[11] Alice M. Rivlin and Isabel Sawhill, eds., Restoring Fiscal Security, the Brookings Institution, 2004, page 42.

[12] Robert M. Ball, “How to Fix Social Security?” Aging Today, March-April, 2004.