What The New CBO Report Shows

Budget And Economic Outlook Has Not Improved

Over the last few months it has become clear that federal revenues collected in the fiscal year that ends this September 30 will be higher, and the deficit will be lower, than either the Administration or the Congressional Budget Office estimated earlier this year. The Administration and conservative pundits have claimed that the unanticipated increase in revenues this year is proof that the President’s 2001 and 2003 tax cuts “are working” — boosting the economy and increasing revenues not only for this year, but for future years as well — and that deficits will be brought under control if only the Congress continues to support the President’s policies.

In contrast to the Administration’s optimistic spin on the good news for this year, the Budget and Economic Outlook: An Update released on August 15 by CBO indicates that there has been no general improvement in the outlook for the economy, and little change in the outlook for the budget in coming years. Instead, the new CBO report indicates that:

- The unanticipated increase in revenues this year is largely the result of temporary factors, such as an increase in corporate book profits relative to the size of the economy, and revenues over the next 10 years are not expected to be significantly higher than CBO estimated last March;

- The economy has grown slightly more slowly this year than CBO forecast last January (after adjusting for inflation), and CBO’s outlook for the economy over the next 10 years now seems slightly worse than CBO had earlier expected; and,

- There has been no significant improvement in the bleak deficit outlook for the next 10 years. When you take into account the President’s proposed extension of expiring tax cuts, continuation of current Alternative Minimum Tax relief, and a conservative estimate of future funding for the wars in Iraq and Afghanistan, projected deficits never dip below $330 billion over the next 10 years and total $4.0 trillion over the 2006-2015 period. The resulting growth in the debt is not sustainable.

The CBO report reinforces a report recently issued by the Center on Budget and Policy Priorities, showing that the recent recovery has been less robust than the average post-war recovery.[1] (GDP, employment, investment, and other measures of the economy have grown more slowly than average — only corporate profits have grown at a faster-than-average rate.) The information in the CBO report and the CBPP report refute claims that the President’s tax cuts have led to exceptional economic growth that will bring deficits under control if only Congress continues to support the President’s policies. They show instead that returning the nation to a sustainable fiscal path will require changes in the policies that have been adopted in recent years.

Causes of this Year’s Unanticipated Revenue Increase and Implications for Future Years

CBO’s Update confirms that revenues for the current fiscal year will be about 4 percent higher than either CBO or the Administration estimated earlier this year. CBO now estimates that revenues for this year will be $85 billion higher than estimated in March. Although CBO now estimates that outlays for 2005 will be $51 billion higher than it estimated in March, largely because of supplemental funding provided in May for the wars in Iraq and Afghanistan, the increase in projected revenues has led CBO to lower its estimate of the deficit for 2005 to $331 billion, from the $365 billion estimated in March (see Table 1).

| TABLE 1: | ||

| CBO’s March estimate, FY 2005 deficit | $365 | |

| Higher than expected revenues | -85 | |

| Higher than expected expenditures | 51 | |

| Net reduction in the deficit | -33 | |

| CBO’s August estimate, FY 2005 deficit | 331 | |

| Source: CBO August Update, Table 1-7. Numbers do not add due to rounding. | ||

The Administration says that the unanticipated increase in revenues this year indicates that the President’s 2001 and 2003 tax cuts are “working” even better than it had earlier thought, improving the outlook for the economy and revenues in future years. In July’s Mid-Session Review of the Budget, the Office of Management and Budget increased the revenues projected for 2006 through 2010 (the President’s budget only provides budget estimates through 2010) by $409 billion above what it had estimated in February. (For an analysis of the argument that the unanticipated increase in revenues in 2005 proves the President’s tax cuts are working, see the Center on Budget and Policy Priorities report, “Revenue Collections in 2005: What Does the Recent Increase in Revenues Signify,” revised August 16, 2005.)

In contrast to the Administration, CBO believes that the unanticipated increase in revenues in 2005 is largely the result of temporary factors and does not indicate that revenues in future years are likely to be significantly higher than was estimated last March. For instance, CBO attributes a substantial part of the unanticipated increase in revenues this year to an increase in corporate income tax revenues and explains that “the sources of the current strength in corporate tax receipts will not be known until information from tax returns becomes available in future years, but CBO anticipates that most of that strength will be temporary.”[2] It goes on to give examples of possible factors affecting the increase in corporate tax receipts this year — for instance, an increase in corporate book profits as a share of GDP in calendar year 2004 — that are unlikely to carry over into future years.

Overall, CBO now projects that revenues will be $179 billion higher than it projected in March for 2006 through 2015. Much of this projected increase, however, is the result of the higher inflation CBO projects for this year and next. That increase in inflation pushes nominal wages and salaries in 2006 through 2010 above what CBO projected in March, even though CBO now projects that real GDP will be lower in every year than it projected earlier. That is, the economy is projected to grow more slowly than previously thought once inflation is taken into account.[3] Furthermore, this increase in revenues stemming from the increase in inflation is offset by increased expenditures for such inflation-sensitive programs as Social Security and Medicare.

CBO’s Economic Outlook has not Improved

CBO does not believe that the unanticipated increase in revenues this year indicates that the tax cuts enacted in 2001 and 2003 have produced a stronger economy than CBO had previously expected. As noted above, CBO says that the unanticipated increase in revenues in 2005 is likely due largely to temporary factors such as a temporary increase in corporate book profits. None of these likely causes of the revenue increase in 2005 indicate that the economy is going to be stronger this year or in future years than was thought earlier this year.

CBO’s new economic projections for 2005 and each subsequent year through 2015 are slightly less favorable than the projections it made last January.[4] CBO’s estimate of real economic growth in the current fiscal year is slightly lower than it forecast in January, 3.7 percent instead of 3.8 percent. Likewise, its projection of the size of the economy (real, inflation-adjusted, GDP) for 2006 through 2015 is somewhat lower than its January projection for each of those years — by 2015 CBO’s projection of real GDP is more than $100 billion lower than it projected in January. In addition, CBO’s new projection of employment is slightly lower in all years than its January projection. Neither CBO’s short-term nor mid-term view of the economy has improved.

CBO’s projections of nominal GDP for the next 10 years have increased somewhat relative to CBO’s January projections. Since CBO projects that real GDP will be lower in every year than it projected in January, this increase in nominal GDP is purely the result of increased inflation.[5] While this inflation-driven increase in nominal GDP does increase revenues, it also increases spending by roughly the same amount, leaving deficits largely unchanged. It certainly does not indicate any improvement in the economy or the well-being of the people of the United States.

CBO’s Budget Outlook Has Not Significantly Improved

CBO does not think that the unanticipated increase in revenues this year has significantly improved the longer-term budget outlook.[6] The report states that “although the deficit for 2005 is lower than previously expected, the fiscal outlook for the coming decade remains about the same as what CBO described in March.”[7]

If one looks only at the changes in CBO’s projected deficits that are not related to enactment of new legislation, one sees that CBO has not substantially reduced its estimate of the deficit over the next 10 years. If CBO had believed that the unanticipated increase in revenues in 2005 indicated a general improvement in the underlying strength of the economy or the collection of federal taxes, it would have shown that improvement as “economic and technical changes” that substantially increase revenues and reduce deficits in 2006 and later years. But the economic and technical changes shown in CBO’s report (see Table 1-7 of the report) reduce the deficit by only $89 billion over 10 years. (These changes average about $9 billion a year, or about five one-hundreths of one percent of the economy over the 10-year period.) And, these economic and technical factors actually increase the deficits projected for 2012 through 2015.

Deficits Will Remain Large If the 2001 and 2003 Tax Cuts Are Extended

CBO’s new report indicates that if the President’s proposal to make the 2001 and 2003 tax cuts permanent is adopted, deficits will remain quite large over the next 10 years. Deficits are expected to become even larger in succeeding years as increasing numbers of baby-boomers retire and per-person health care costs continue to rise at a rapid rate.

CBO’s official baseline projections show deficits that generally decline over the next 10 years. As CBO points out, however, the official baseline is not an indicator of what is actually likely to happen to the budget. For instance, following the baseline rules, CBO assumes that all of the 2001 tax cuts will expire in 2010, as slated under current law. It also assumes that current relief from the Alternative Minimum Tax will expire at the end of this year because Congress and the President have not yet extended that relief. Both of these assumptions seem unrealistic, and neither reflect tax policies currently in effect.

In order to provide a more realistic picture of the current budget path, CBO has provided estimates of the effects that various policies not included in the official baseline would have on the deficit.[8] For instance, CBO estimates that making the 2001 and 2003 tax cuts permanent would increase deficits by $1.9 trillion over 10 years.[9] This estimate of the effect of extending the President’s tax cuts on future deficits calls into question the claim that those tax cuts have not substantially increased the deficit. (See the box on this page about the effects of the tax cuts already enacted since 2001.) It also estimates that extending current AMT relief would increase deficits by $775 billion over 10 years.[10]

In one instance, the official baseline may overstate costs. The baseline rules call for CBO to assume that appropriations provided in the current year will be provided in the same amount (adjusted for inflation) in future years. Since $95 billion in supplemental appropriations were provided in 2005 (the $84 billion enacted last May that was largely for the wars in Iraq and Afghanistan plus $11 billion enacted earlier in fiscal year 2005 that was primarily for disaster relief), the CBO baseline assumes that $95 billion (adjusted for inflation) will be provided each year, 2006 through 2015. While the costs of the wars in Iraq and Afghanistan are likely to be substantial in those years, it is likely that the cost of the wars will be less on average over the next 10 years than the amount provided this year.

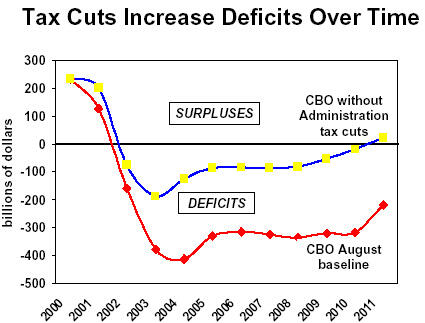

Without the Tax Cuts, Deficit Picture Would be Dramatically Improved

This year’s deficit would be much smaller if the President’s tax cuts had not been enacted. Based on the official cost estimates by the Joint Committee on Taxation, and accounting for the increased interest payments caused by borrowing to finance the tax cuts, the cost of the tax cuts enacted in 2001 and 2003 is equal to about 2 percent of GDP this year, while this year’s deficit equals 2.7 percent of GDP.a

Looking out over the next couple of years as well, the deficit picture would look far different except for the tax cuts. As the figure below indicates, large deficits will persist on into the future under the official CBO baseline forecast. But in the absence of the tax cuts, the baseline would show the nation returning to a surplus in 2011.

Further, because of the tax cuts (assuming they are extended), revenues will constitute a smaller share of the economy over the next 10 years than they averaged in the 1950s, the 1960s, the 1970s, the 1980s, or the 1990s.

aEven if one were to assume some positive feedback effects on the economy, the cost of the tax cuts would represent a large share of the current deficit.

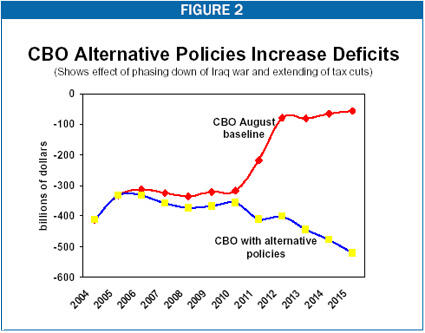

If one starts with CBO’s baseline and assumes that the 2001 and 2003 tax cuts are made permanent, (as the President has proposed), that the current AMT relief is extended (as seems virtually certain unless the AMT is reformed in an even more costly manner or is repealed), and that funding for the wars in Iraq and Afghanistan is provided at the levels CBO assumes in its scenario of a gradual drawdown of forces:

The deficit would never fall below $330 billion or 2.3 percent of gross domestic product over the next 10 years and would total $4.0 trillion in the 2006-2015 period (see Table 2 and Figure 2); and,

| TABLE 2: | ||

| Official CBO “baseline” deficit, cumulative 2006-2015 | $2.1 | |

| Extend tax cuts beyond scheduled expiration | 1.9 | |

| Provide relief from the Alternative Minimum Tax | 0.8 | |

| Gradually phase down activities in Iraq and Afghanistan | -0.7 | |

| CBO baseline adjusted for alternative policies | 4.0 | |

| Source: CBO August Update, Table 1-6. Note that each figure includes the direct costs or savings from the policy and the resulting cost or saving in interest on the debt. Numbers do not add due to rounding. | ||

Federal debt held by the public would grow faster than the economy in every year for the next 10 years, from 37.7 percent of GDP at the end of 2005 (it had been equal to 33 percent of GDP at the end of 2001) to 44.4 percent of GDP at the end of 2015.

Such increases in debt cannot be sustained indefinitely — neither individuals nor the government can permanently increase their debt faster than their ability to repay that debt. Eventually, federal revenues will have to be increased or spending reduced by amounts sufficient to at least stabilize the debt-to-GDP ratio.

Conclusion

CBO has concluded that the unanticipated increase in revenues in 2005 does not indicate a general improvement in the economic or budget outlook. CBO’s view of the economy is, if anything, slightly less sanguine than it was in January. And unlike the Administration, CBO has not significantly increased its projection of revenues in future years. When adjusted to account for extension of the 2001 and 2003 tax cuts, continuation of AMT relief, and a more modest level of future funding for the wars in Iraq and Afghanistan, CBO’s budget projections show that deficits will remain quite high for the next 10 years. In short, CBO’s report indicates that changes in the policies that have been pursued in recent years will be necessary to bring the deficit under control.

End Notes

[1] Isaac Shapiro, Richard Kogan, and Aviva Aron-Dine, “How Does This Recovery Measure Up?,” Center on Budget and Policy Priorities, August 9, 2005.

[2] Congressional Budget Office, The Budget and Economic Outlook: An Update, August 2005, page 24.

[3] “Real” GDP shows the actual level of goods and services produced after accounting for inflation. Increases in nominal GDP resulting from inflation do not reflect any increase in the goods or services that are available, only the fact that consumers must pay more for the same level of goods and services.

[4] CBO issues economic and budgetary projections each January. Although it revised its baseline budgetary projections for technical reasons when it analyzed the President’s budget in March, CBO did not revise its economic assumptions at that time — it used the same economic assumptions in March as in January.

[5] CBO estimates that both the consumer price index and the GDP price index will grow faster in 2005 and 2006 than it assumed earlier this year, but its projections of inflation in 2007 through 2115 are unchanged.

[6] CBO’s baseline projections of the deficit for 2006 through 2015 are actually $1.13 trillion higher than CBO projected last March, but the bulk of that increase is the result of legislation enacted since March. In particular, $84 billion in supplemental appropriations enacted since March, primarily for the wars in Iraq and Afghanistan, account for an increase in expenditures of nearly $1.2 trillion, including interest. Under the baseline rules, CBO assumes that the same amount — adjusted for inflation — will be enacted in 2006 and each succeeding year through 2015. Thus, CBO’s March baseline assumed none of this $84 billion in supplemental funding in 2006 or any future year (because it had not been enacted by March), while its new baseline assumes $84 billion in 2006 and every future year, growing with inflation. Neither assumption is realistic.

[7] The Budget and Economic Outlook, page ix.

[8] See Table 1-6 on pages 16-17 of The Budget and Economic Outlook.

[9] These estimates include the increase in interest payments resulting from the additional federal debt needed to finance the tax cuts or spending increases.

[10] This includes the increased cost of AMT reform resulting from the extension of the 2001 and 2003 tax cuts.

More from the Authors

Areas of Expertise