Smaller Deficit Estimate No Surprise: New OMB Estimates Do Not Support Claims About Tax Cuts

The Office of Management and Budget today released a report estimating that revenues for the current fiscal year will be higher, and the deficit lower, than the administration and the Congressional Budget Office projected five months ago. OMB now estimates that the deficit for fiscal year 2007 will be $205 billion, down from the $244 billion estimate in the President’s budget in February. The administration and its supporters are portraying the new estimates as important evidence the President’s tax and budget policies are “working” by boosting the economy, generating more revenue, and improving the budget outlook.

Unfortunately, the reality is different. Careful analysis of the Mid-Session Review data and other data about the budget and the economy shows that:

-

The increase in revenues and the reduction in the deficit, relative to what OMB projected in February, should be no great surprise. A CBO analysis demonstrates that over the last quarter century, relatively large reestimates of revenues and the deficit for the current fiscal year are the norm rather than the exception. The CBO data also indicate that at this point in the economic cycle — several years into an expansion — there is a clear tendency for mid-year reestimates to show an improvement in the budget outlook.

-

The increase in estimated revenues in 2007 does not indicate that the 2001 and 2003 tax cuts are boosting the economy. To the contrary, the administration is now forecasting slower economic growth for the current year than it did in February. Furthermore, overall the performance of the economy since 2001 has not been especially robust; the current recovery has been weaker than the average economic recovery since the end of World War II.

-

The recent increase in revenues has come largely in the form of increased corporate income taxes, taxes on high-income individuals, and taxes on capital gains. These increases reflect historically high corporate profits, increased concentration of income at the top of the income ladder, and high stock prices, rather than a surge in economic growth or wages. Moreover, the high corporate profits, increased inequality, and rise in the stock market are unlikely to be the result of the tax cuts.

-

Revenue growth during the recovery has been disappointing rather than impressive. Even with the recent revenue increases, growth in revenues since 2001 has been far below average for comparable periods of previous business cycles since the end of World War II, which is exactly what one would expect, given the large tax cuts enacted in 2001 and 2003.

-

Nor does the improvement in the deficit forecast for the current fiscal year indicate an improvement in the longer-term budget outlook. The Mid-Session Review itself does not show any improvement in the budget outlook for 2008 through 2012 compared to what was assumed in the President’s February budget (in fact, deficits are $137 billion higher), and nothing contained in the new report indicates any change in the fact (acknowledged by the administration) that current budget policies are not sustainable over the long run. Federal deficits and debt will explode in coming decades unless current policies regarding spending and revenues are changed.

-

Without the $300 billion cost of the 2001 and 2003 tax cuts in fiscal year 2007 alone, the $205 billion deficit projected in the Mid-Session for the current year would be a surplus. Some supporters of the tax cuts would argue that this estimate of the cost of the tax cut is too high because it does not take into account the “dynamic” effects that the tax cuts have had on the economy, but the nonpartisan Congressional Research Service concluded last year that “at the current time, as the stimulus effects have faded and the effects of added debt service has grown, the 2001-2004 tax cuts are probably costing more than expected” (emphasis added) [1]

The Facts About the Mid-Session Review and the Budget

The Mid-Session Review projects a deficit for the current year (fiscal year 2007) of $205 billion. This is $39 billion less than was estimated in the budget President Bush submitted to Congress on February 5.[2]

OMB now projects that spending will be $6 billion lower this year than it projected in February, which contributes to the lowering of the deficit estimate. But the main reason for the decline in the projected deficit is the increase in projected revenues, relative to OMB’s February estimate. At that time, the President’s budget estimated that revenues in the current year would total $2,540 billion. The Mid-Session Review estimates revenues will total $2,574 billion, an increase of $34 billion.

The administration is portraying this increase in revenues as a surprise that provides new evidence the 2001 and 2003 tax cuts are boosting economic growth and revenues. The facts do not support the administration’s position, however, as is explained below.

A Mid-Session Improvement in Budget Estimates Is Not a Surprise

This marks the fourth straight year that OMB has substantially reduced its estimate of the deficit for the current year in its Mid-Session Review. It is easy to understand how an administration likes to be able to report during the course of a year that the budget outlook is improving; it is much easier to take credit for an “improving” outlook than to explain why things are not turning out as well as predicted.

CBO also has reduced its estimate of the current-year deficit during the last few years.[3] Given the complexity of the nearly $2.8 trillion federal budget and the thousands of factors that affect the levels of expenditures and revenues in any given year, it is not surprising that the estimated deficit for the current fiscal year can change by billions of dollars as the year progresses.

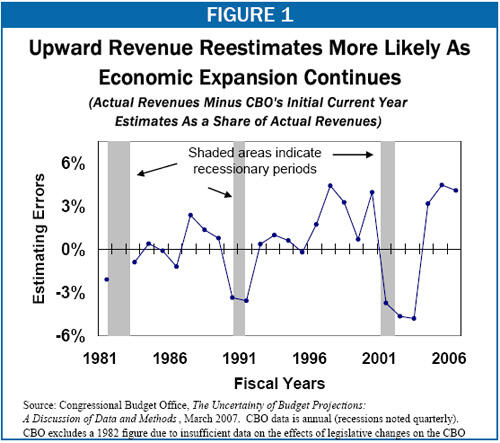

It is important to recognize that this is not a phenomenon unique to the past few years. Data published by CBO indicate that from fiscal year 1981 through 2006, the estimates that CBO made early in the calendar year of the surplus or deficit for the current fiscal year (generally an estimate made in January for the current fiscal year) were off by an average of 3.7 percent of actual revenues for that year. (This excludes changes in the deficit caused by legislation enacted after the initial estimates were produced.)[4] That is equivalent to being off by $89 billion in 2006.

There is nothing unusual in OMB or CBO changing its estimate of the deficit for the current year by the $39 billion reestimate contained in the Mid-Session Review (which is equal to 1.5 percent of projected revenues for 2007). Nor should it be a surprise that the reestimate will show an improvement in the deficit for this year. CBO’s analysis of its past errors in forecasting deficits and surpluses makes clear that there is a tendency to overestimate deficits (or underestimate surpluses) at this point in the business cycle, several years into an expansion.[5]

The same is true of revenues. CBO’s data show that over the past quarter century, CBO has underestimated or overestimated current-year revenues by an average of 2.8 percent of actual revenues, which is equivalent to $68 billion in 2006. Furthermore, there is a tendency to underestimate revenues as an economic recovery grows longer, as can be seen below in Figure 1.[6] Thus, the $34 billion reestimate of revenues (1.3 percent of projected revenues for 2007) in the Mid-Session Review should be a surprise only to those who have not been paying attention to the recent or longer-term history of revenue estimating.

The Improvement in the Deficit for 2007 Does Not Show that “The Tax Cuts are Working”

The administration and proponents of the President’s 2001 and 2003 tax cuts have sought to portray virtually every recent increase in revenues and the deficit outlook as evidence that “the tax cuts are working” — that is, that the tax cuts have spurred economic growth and boosted revenues well above what had been anticipated. In their less careful statements, they seem to suggest the tax cuts are paying for themselves.[7]

In reality, economic and revenue data indicate that the tax cuts have not provided any special boost to the economy or revenues:

-

The unanticipated increase in revenues in 2007 does not stem from more-rapid-than-expected economic growth in 2007, since the administration is now lowering its forecast of economic growth in 2007 (compared to what it forecast in February).[8]

-

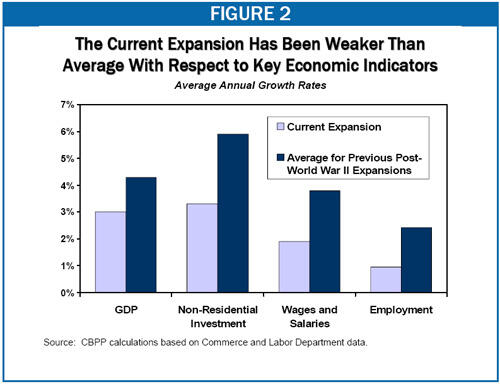

In addition, economic data show that the performance of the economy since 2001 has not been especially robust.[9] To the contrary, the current recovery has been notably weaker than the comparable period of the average recovery since the end of World War II (see Figure 2). With respect to economic growth, consumption, investment, wages and salaries, and jobs, the current recovery is either the weakest or among the weakest since World War II.[10] The economy’s overall performance over the past five and a half years also has been weaker than its performance in the early 1990s in years following significant tax increases. (GDP growth in the current recovery has been slightly weaker than in the 1990s. Job creation, wage and salary growth, and investment growth have all been substantially weaker.)

-

Analysis of the recent growth in revenues as a share of the economy also does not support the arguments of those who attribute the recent increases in revenues to the tax cuts.[11] A recent CBO analysis attributes a significant share of the increase since 2003 in revenues as a share of GDP to a large increase in the percentage of national income going to corporate profits.[12] When corporate profits increase at the expense of employee compensation and other forms of income — as has occurred to a striking degree in recent years — revenues rise as a share of GDP, because the other forms of income may not be subject to tax or may be taxed at lower rates than corporate profits.

In addition, data presented by economists Thomas Picketty and Emanuel Saez show that the share of the nation’s pre-tax income going to the top one percent of households jumped dramatically between 2003 and 2005 (the latest year for which data are available). Increases in income concentration tend to raise revenues because they put more income in the hands of people who pay taxes at higher rates.[13]

Supporters of the tax cuts cannot claim credit for the revenue growth that resulted from these developments unless they also claim credit for the developments themselves. That is, they would have to argue that the tax cuts caused the share of the nation’s income going to corporate profits and high-income households to increase and consequently caused the share going to employee compensation and middle- and lower-income households to fall. Tax cut supporters have been notably silent on this score. -

CBO’s analysis does attribute a small share of the increase in revenues since 2003 to an increase in capital gains receipts resulting from higher capital gains realizations. Much of that increase likely reflects the growth in the stock market since 2003. But strong evidence refutes any claim that the 2003 tax cuts caused this stock-market increase. A careful study by three Federal Reserve economists compared the performance of taxable stocks in the United States to the performance of European stocks and to Real Estate Investment Trusts, neither of which benefited from the 2003 tax cuts. The study found that the European stock market and U.S. real estate markets behaved similarly to the U.S. stock market. This casts very serious doubt on the assertion that the capital gains and dividend tax cuts were a crucial factor behind the rise in the U.S. stock market, which itself was simply returning to the levels it had attained at the start of the decade.

-

Furthermore, the recent increases in revenues have not raised revenues to impressive or unexpected heights. To the contrary, the growth in revenues since 2001 has been disappointing by historical standards, as one would expect given the large tax cuts enacted in 2001 and 2003. Based on the Mid-Session Review estimates, revenues in 2007 will be only 3.1 percent higher than when the current business cycle began in 2001, after adjusting for inflation and population growth. This is far below the 12 percent average revenue increase over comparable periods of previous post-World War II business cycles and even farther below the 16 percent increase in the 1990s.

The MSR Does Not Signal an Improvement in the Long-run Budget Outlook

Virtually all budget analysts, including those in the administration, agree that current tax and spending policies are not sustainable in the long run — that the retirement of the baby-boom population and the growing per-person cost of providing health care in the United States will push up the cost of programs such as Social Security, Medicare, and Medicaid faster than revenues will grow, resulting in rapidly rising deficits and debt in the decades ahead.[14]

Although the Mid-Session Review estimates that the deficit for 2007 will be smaller than the administration projected earlier this year, the deficits projected for 2008 through 2012 are somewhat ($137 billion) higher than what was forecast in the President’s budget in February. More importantly, the Mid-Session Review contains no information that would indicate any change in the conclusion that today’s budget policies are not sustainable. The increase in revenues in 2007 in no way suggests that revenues are likely to grow enough in coming decades to cover the cost of providing promised benefits and services. It remains the case that it will take major changes in tax and spending policies, as well as fundamental reforms in the nation’s health care system that allow Medicare and Medicaid costs to be constrained in a reasonable fashion, to bring future deficits under control.

Without the Tax Cuts the Budget Would Be in Surplus

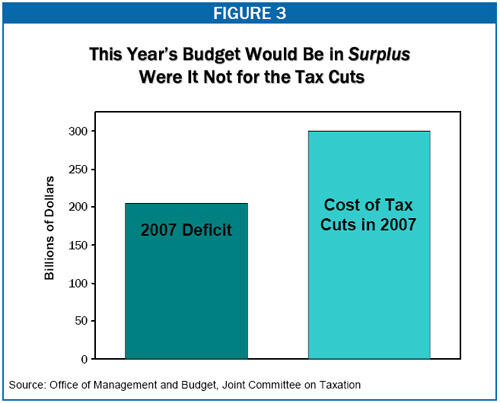

The Mid-Session Review estimates there will be a federal budget deficit of $205 billion in 2007. The administration is crowing that this is $39 billion lower than it estimated in February. The administration ignores the fact that the budget would be in balance this year if it were not for the cost of the tax cuts enacted since 2001 (see Figure 3).

Based on Joint Committee on Taxation estimates, the total cost of the tax cuts enacted since January 2001 is $300 billion in 2007, taking into account the increased interest costs on the debt that have resulted from the deficit-financing of the tax cuts. This means that even with the spending for the wars in Iraq and Afghanistan and the response to Hurricane Katrina, there would be a federal budget surplus of nearly $100 billion this year if the tax cuts had not been enacted, or if the costs of the tax cuts had been offset. Finally, while supporters of the tax cuts claim that positive economic effects have lowered the tax cuts’ cost, the non-partisan Congressional Research Service concluded in a September, 2006 report that “at the current time, as the stimulus effects have faded and the effects of added debt service has grown, the 2001-2004 tax cuts are probably costing more than expected” (emphasis added).[15]

End Notes

[1] Jane G. Gravelle, “Revenue Feedback from the 2001-2003 Tax Cuts,” Congressional Research Service, September 27, 2006.

[2] The February budget assumed the deficit in fiscal year 2007 would be $244 billion if the supplemental funding the President requested for operations in Iraq and Afghanistan was enacted, which it subsequently was. The administration estimates that the enacted supplemental appropriations will increase outlays in 2007 by $4.5 billion more than it estimated that the supplemental appropriations proposed in the budget would cost.

[3] In its June 6, 2007 Monthly Budget Review, CBO has indicated that the deficit estimate for 2007 in its upcoming August Budget and Economic Outlook: An Update will also be significantly lower than it had projected in January.

[4] This is the “root mean square” of the errors, which gives the average error without regard to the fact that errors in some years result from an overestimate of the deficit and errors in other years result from an underestimate of the deficit. (The root mean square is calculated by taking the square root of the arithmetic mean of the square of each year’s error.) Under this calculation, a 3 percent overestimate and a 3 percent underestimate are averaged together as a 3 percent error. Simply taking the arithmetic mean of a 3 percent overestimate and a 3 percent underestimate would yield an average error of zero (+3 plus -3, divided by 2 equals 0). In fact, the arithmetic mean of CBO’s deficit errors is 1.2 percent of actual revenues, which indicates that CBO’s underestimates and overestimates tend to offset each other over time. For an explanation of CBO’s analysis of estimating errors see Congressional Budget Office, The Uncertainty of Budget Projections: A Discussion of Data and Methods, March 2007.

[5] This tendency is offset to a large degree over time by a tendency to underestimate deficits as an economic expansion draws to a close and in the early years of an economic recovery.

[6] Overestimates at other points in the business cycle tend to offset this tendency; the arithmetic mean of CBO’s revenue errors for the current fiscal year, measured over the period since 1981, is only 0.3 percent of actual revenues. As an example, the initial underestimates of revenues in each of the last three years — 2004, 2005, and 2006 — followed three years of sizable overestimates of revenues in 2001, 2002, and 2003. Federal revenues actually declined in nominal terms for three years in a row in 2001, 2002, and 2003, marking the first time this had occurred since the 1920s.

[7] Despite statements by the President and Vice President that seem to suggest the tax cuts actually increased revenues above what would have happened without the tax cuts, even the administration has concluded that the economic feedback from the tax cuts could in the long run boost revenues by no more than 10 percent of the “static” estimate of the cost of the tax cuts, assuming the tax cuts are fully offset by reductions in spending. This is a very far cry from the tax cuts paying for themselves. See Jason Furman, “Treasury Dynamic Scoring Analysis Refutes Claims by Supporters of the Tax Cuts,” Center on Budget and Policy Priorities, revised August 24, 2006.

[8] See “Joint Press Release of the Council of Economic Advisers, the Department of the Treasury, and the Office of Management and Budget,” June 6, 2007. http://63.161.169.137/cea/forecast20070606.pdf

[9] See Aviva Aron-Dine, Chad Stone, and Richard Kogan, “How Robust is the Current Economic Expansion?”, Center on Budget and Policy Priorities, revised June 28, 2007.

[10] Proponents of the capital gains and dividend tax cuts enacted in 2003 argue that those cuts have provided the real economic impact and, therefore, that it is the performance of the economy since 2003 that matters. Even since 2003, however, growth in GDP, wages and salaries, and employment have been below average for a post-World War II recovery.

[11] See, Aviva Aron Dine, “The Effects of the Capital Gains and Dividend Tax Cuts on the Economy and Revenues: Four Years Later, a Look at the Evidence,” Center on Budget and Policy Priorities, July 10, 2007.

[12] Letter from Congressional Budget Office Director Peter R. Orszag to Senate Budget Committee Chairman Kent Conrad, May 18, 2007, http://www.cbo.gov/ftpdocs/81xx/doc8116/05-18-TaxRevenues.pdf

[13] See Aviva Aron-Dine, “New Data Show Income Concentration Jumped Again in 2005: Income Share of Top 1% Returned to Its 2000 Level, the Highest Since 1929,” Center on Budget and Policy Priorities, March 29, 2007.

[14] See, for instance, Richard Kogan, Matt Fiedler, Aviva Aron-Dine, and James Horney, “The Long-Term Fiscal Outlook is Bleak: Restoring Fiscal Sustainability Will Require Major Changes to Programs, Revenues, and the Nation’s Health Care System,” Center on Budget and Policy Priorities, January 29, 2007; and, “The Long-Run Budget Outlook” section of the Analytical Perspectives volume of the Budget of the United States for Fiscal Year 2008, February 5, 2007, pp. 183 – 192.

[15] Jane G. Gravelle, “Revenue Feedback from the 2001-2003 Tax Cuts,” Congressional Research Service, September 27, 2006.

More from the Authors