The Recent Upturn in Revenues and OMB's Mid-Session Review

Summary

The Mid-Session Review issued on July 11 by the White House Office of Management and Budget projects that fiscal year 2006 revenues will be significantly above — and the 2006 deficit significantly below — the levels forecast in the President’s budget in February.

This year’s strong growth in revenues follows upon stronger-than-anticipated revenue growth in 2005. Members of the Administration greeted the higher-than-anticipated 2005 revenue growth as reason for optimism about the economy and the budget outlook and as evidence that the President’s tax cuts were “working.” Some Administration officials, including the President and Vice President, have even stated or implied that the tax cuts are paying for themselves. (See box below)

Administration officials are already drawing similarly optimistic conclusions from this year’s Mid-Session Review. For example, President Bush commented, “Some in Washington say we had to choose between cutting taxes and cutting the deficit…Today's numbers show that that was a false choice. The economic growth fueled by tax relief has helped send our tax revenues soaring. That's what's happened.”[1] But while unexpectedly high revenues are good news for the Treasury, the budget and economic picture remains far less rosy than the Administration’s claims suggest, and the tax cuts — rather than paying for themselves as the President’s comments would suggest — remain a major contributor to the nation’s serious fiscal problems.

Revenue growth over the current business cycle has been lower than in comparable past periods; in fact, revenue growth over the current business cycle is near zero after adjusting for inflation and population growth. Even when the stronger revenue growth now projected for 2006 is taken into account, real per-capita revenues have simply returned to the level they reached more than five years ago when the current business cycle began in March 2001. (March 2001 was the peak, and thus the end, of the previous business cycle and the start of the current business cycle.) In contrast, in previous post-World War II business cycles, total real per-capita revenue growth over the five and a half years following the business cycle peak has averaged about 10 percent. Moreover, even with higher-than-anticipated revenues this year, revenues in 2006 remain about $300 billion below the levels OMB and CBO projected for this year in early 2001, and about $100 billion below those levels adjusted for the cost of the tax cuts enacted since that time.

-

Revenue “surprises” are relatively common. Unanticipated revenue gains occurred in nearly every year of the 1990s expansion. Those revenue "surprises" followed tax increases rather than tax cuts. Moreover, there were negative revenue “surprises” in each year from 2001 through 2003, with end-of-year revenues well below the levels OMB had projected earlier in the year, even after adjusting for the cost of enacted tax cuts. When tax cut supporters take recent positive revenue “surprises” as evidence that tax cuts are “paying for themselves,” they ignore these other facts.

-

There is no evidence of a tax-cut fueled economic boom. Economic data, now available through the first quarter of 2006, show that the current economic expansion remains weaker than the average post-World War II economic recovery, with GDP and non-residential investment growth falling below — and employment and wage and salary growth falling far below — historical norms. While economic growth has been stronger in the past three years than in the earlier part of the current recovery, the evidence does not support Administration claims that the 2003 tax cuts caused the improvement. The economy’s performance improved at about the same point in the 1990s recovery, and that improvement coincided with tax increases enacted in 1993.

-

There is strong evidence that increased income disparities between high-income households and the rest of the population have contributed to the recent revenue gains. High-income taxpayers pay taxes at higher rates. As a result, an increase in the share of the nation’s income that goes to these households leads to an increase in revenues, even if there is no increase in overall economic growth. In its May Monthly Budget Review, the Congressional Budget Office wrote that this year’s stronger-than-expected increases in revenues may be due in part to increased income concentration. This is consistent with other recent evidence of rapidly rising income inequality.

-

Much of the unanticipated revenue increase comes from strong growth in corporate revenues, which reflects exceptionally strong growth of corporate profits during the current business cycle. Corporate profits have increased more rapidly during the current economic expansion to date than in any other comparable post-World War II period. This reflects the fact that corporate profits have captured an unusually large share of the total economic gains during the current recovery, while wages and salaries have captured an unusually small share. Wages and salaries have grown more slowly during the current recovery than in any comparable post-World War II period. Moreover, OMB now projects significantly more rapid growth in corporate profits in 2006 than it forecast in February, and notably slower wage and salary growth.

-

Even with higher-than-anticipated revenues this year, budget deficits remain disturbingly large for a mature economic recovery. OMB now projects a 2006 deficit of $296 billion. While that is lower than the deficit estimate issued at the start of the year, it still amounts to a deficit equal to 2.3 percent of GDP. That the deficit remains so large this year is particularly disturbing given that the U.S. is now in the fifth year of an economic expansion, and deficits likely will rise when the expansion ends, or even before. (The Administration itself still projects the deficit will rise again in 2007.[2]) It is also distressing given the major fiscal challenges the nation will face in the coming decades, as the baby boomers begin to retire in large numbers.

In short, while the Administration is emphasizing the improvement in OMB’s revenue estimates since February, the nation’s serious fiscal challenges remain. The recent revenue increases do not materially alter the longer run fiscal outlook. Nor do they change the fact that the Administration and Congress have enacted large tax reductions that have significantly increased the deficit, and that despite these tax cuts, economic growth in the current recovery has been unexceptional.

Weak Overall Revenue Growth During this Business Cycle Reflects the Impact of Tax Cuts

When discussing revenue growth since the enactment of the tax cuts, Administration officials frequently focus only on revenue growth since 2004. This provides a convenient “starting point” for their arguments, as it sets a very low bar. Measured as a share of the economy, revenues in 2004 were at their lowest level since 1959. Given this historically low starting point, it is not surprising that revenues have recovered significantly since then. Yet supporters of the tax cuts selectively cite revenue growth over just the past two years to argue that the tax cuts are fueling the large increase in revenues.

| Table 1: | |

| Current Business Cycle | 0.2% |

| Average for All Previous Post-World War II Business Cycles | 9.7% |

| 1990s Business Cycle | 10.7% |

Measured since the current business cycle began, however (in March 2001, shortly before enactment of the President’s first tax cuts), total per capita revenue growth has been near zero after adjusting for inflation and population growth, even after taking into account the stronger revenue growth now projected for 2006 (see Table 1). Based on OMB’s revised revenue estimate, real per-capita revenues in 2006 still will be only 0.2 percent above the level they attained more than five years ago at the start of the business cycle. In other words, the current revenue “surge” is merely restoring revenues to where they were half a decade ago. And in the case of individual income tax revenues, real per-capita revenues are 11 percent below where they were at that time.

In contrast, five and a half years after the peak of previous post-World War II business cycles, real per-capita revenues had increased by an average of 10 percent, and real per-capita income tax revenues had risen by more than 8 percent.[3] In addition, real per-capita revenues at this point in the 1990s business cycle were 11 percent higher than their level at the previous business-cycle peak, and income tax revenues were up 9 percent.

Despite Administration claims about standout revenue growth in 2005 and 2006, the most striking record set during the current business cycle has been one related to revenue losses. In 2001, 2002, and 2003, revenues fell in nominal terms for three straight years, an occurrence unprecedented since before World War II.

This discouraging record, and the fact that real per-capita revenues have barely reached the level they were at when the business cycle began more than five years ago, largely reflects the impact of the tax cuts enacted in 2001 and since. According to the Joint Committee on Taxation, the tax cuts enacted since 2001 have reduced revenues by $1 trillion between 2001 and 2006.

Furthermore, the Congressional Research Service recently examined revenue data through 2004 and observed, “Actual tax receipts fell significantly more than predicted by the ex ante [i.e. Joint Tax Committee] scores, even after controlling for economic conditions. This suggests that the tax cuts may have resulted in even more revenue loss than predicted” (emphasis added).[4] That is, far from paying for themselves, the tax cuts may have been even more costly than anticipated.

As of 2006 — taking into account the higher revenue growth now expected — revenues will remain about $300 billion below the baseline revenue projection for 2006 that OMB issued in February 2001. Since the tax cuts enacted since 2001 were projected to cost about $200 billion in 2006, this comparison leaves a shortfall of about $100 billion — rather than a revenue surge — still to be explained.

As the CRS analysis implies, one possible explanation is that the tax cuts have led to larger revenue losses than predicted. Another possible explanation is that the unexpectedly large revenue losses were linked to the large decline in the stock market and the initially sluggish recovery. A third possibility is that the 2001 revenue projections were simply too high for technical reasons. A combination of these factors may be at work.

Regardless of the relative impact of these various factors, the one explanation that cannot be supported by the data is the claim that the tax cuts have “paid for themselves.”[5] Unfortunately, this is a claim that Administration officials and various Congressional leaders have been voicing with increasing frequency in the past year (See box below).

Short-Term Revenue “Surprises” Are Not Unusual in Economic Recoveries

Some tax-cut proponents likely will cite the fact that revenue levels for 2006 are expected to be higher than was projected in February as evidence that the Congressional process for estimating the cost of tax cuts systematically overestimates those costs. They made such arguments last year when revenues came in higher than anticipated.[6]

Such claims, however, ignore two crucial points. First, positive revenue “surprises” occurred in almost every year of the economic expansion of the 1990s, and taxes were raised rather than cut in the early 1990s. This suggests that revenue “surprises” during economic recoveries are, in some sense, unsurprising. They are relatively common during expansionary periods and are not a justification for rejecting standard cost estimates of tax cuts and replacing those estimates with “dynamic scoring.” [7] (Further, in the Mid-Session Review, the Administration itself reports that the economic benefits of extending its tax cuts could offset at most a very small fraction of their long-term cost.[8])

Second, there were significant negative revenue “surprises” in 2001, 2002, and 2003. During those years, revenues turned out to be considerably lower than OMB’s February forecasts, adjusted to reflect the Joint Tax Committee’s estimates of the revenue losses from the tax cuts that were subsequently enacted.

One could argue that negative “surprises” show the Joint Tax Committee has been understating the tax cuts’ costs; as noted, the Congressional Research Service has raised that as one possible explanation for lower-than-expected revenues. Claims that the Joint Tax Committee systematically overstates the cost of tax cuts can appear plausible only if one ignores both the early years of the current recovery and the experience of the 1990s and arrives at sweeping generalizations based on two years of data.

The Role of the Economy in the Recent Revenue Growth: A Return to Normal, Not a Tax-Cut Fueled Boom

Generally speaking, revenue growth closely tracks economic growth. The current business cycle has been exceptional only in that the revenue losses in 2001, 2002, and 2003 were much deeper than would have been expected following a relatively mild recession, a departure from the norm that primarily reflects the impact of the tax cuts. Still, as would be expected, revenue growth during current recovery has followed a path similar to that of economic growth — very weak initially and then stronger.

From November 2001 through mid-2003, the current economic recovery was exceptionally weak. In fact, had average growth rates remained as low through the end of 2005 as they were through the middle of 2003, overall economic growth — as well as growth in consumption, non-residential investment, net worth, wages and salaries, and employment — all would have been weaker than in any other recovery since the end of World War II.

No Evidence that Capital Gains and Dividend Tax Cuts Have Boosted the Economy

The economy began to improve in mid-2003, although the economic recovery as a whole remains somewhat weaker than average for post-World War II recoveries.[9] The President and some Congressional leaders have credited the capital gains and dividend tax cuts enacted in 2003 for the stronger economic performance. They have produced no evidence, however, to support this leap from correlation (that the tax cuts coincided with improvement in the economy) to causation (that the tax cuts actually caused the improvement). They also have ignored evidence suggesting that there was little or no causal connection.

Administration Has Claimed Recent Revenue Growth Shows Tax Cuts “Pay for Themselves”

Following the unexpectedly strong growth in revenues in 2005, the President, the Vice President, and key Congressional leaders asserted that the revenue increase showed tax cuts were “paying for themselves” by boosting economic growth, and they are now reiterating these claims. President Bush stated today, “The economic growth fueled by tax relief has helped send our tax revenues soaring. That's what's happened.”a Early in the year, he commented, “You cut taxes and the tax revenues increase.”b Similarly, Vice-President Cheney has claimed, “The tax cuts have translated into higher federal revenues.”c Majority Leader Frist wrote that recent experience demonstrates, “when done right, tax cuts actually result in more money for government.”d

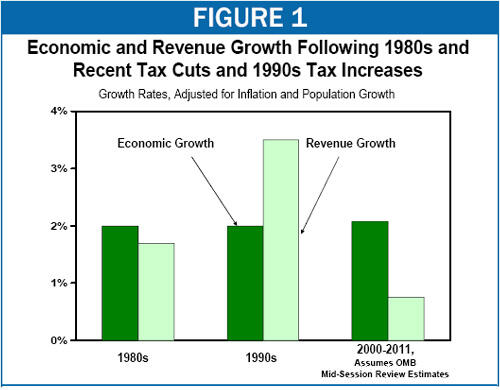

In looking at only one or two year’s worth of recent experience, however, such claims ignore the rest of the historical record, which tells a far different story. In 1981, Congress approved very large supply-side tax cuts, dramatically lowering marginal income-tax rates. In 1990 and 1993, by contrast, Congress raised marginal income-tax rates on the well off. Despite the very different tax policies followed during these two decades, there was virtually no difference in real per-person economic growth in the 1980s and 1990s. Real per-person revenues, however, grew about twice as quickly in the 1990s, when taxes were increased, as in the 1980s, when taxes were cut (see graph).

Moreover, based on the Administration’s own, new projections, GDP growth during the current decade is expected to be only about the same as during the 1980s and 1990s. Yet even after taking into account the unexpected increase in revenues this year and the new, higher projections for future years, the Administration’s own estimates indicate that revenue growth in this decade is expected to be much weaker than in either the 1980s or the 1990s.

a “Remarks by the President on the Mid-Session Review,” July 11, 2006.

b “President Discusses 2007 Budget and Deficit Reduction in New Hampshire,” February 8, 2006.

c Nell Henderson, “Cheney says New Unit Will Prove Tax Cuts Boost Revenue,” The Washington Post, February 11, 2006.

dBill Frist, “Tax Cuts Make Money,” USA Today, February 21, 2006.

Informed observers such as Federal Reserve Chairman Ben Bernanke, who was a Federal Reserve Board governor in 2003, were predicting improvement in the economy before the 2003 tax cuts were enacted (and independent of those tax cuts). Furthermore, the economy’s overall performance during the 1990s recovery followed a pattern similar to that for the current recovery — it was initially weak and then began to improve about two years into the recovery (before growing especially robustly late in the recovery). The improvement a few years into the 1990s recovery coincided closely with a tax increase.

If one accepts the notion that any economic change that follows a tax change must have been caused by the tax change, one could conclude that tax increases are an even stronger economic panacea than tax cuts. The more reasonable conclusion, of course, is that weak recoveries eventually tend to return to historical norms, whether there are tax cuts, tax increases, or no tax changes at all.[10]

The Role of Increasing Income Inequality in Recent Revenue Growth

Beyond the basic point that revenue growth has more or less tracked economic growth (apart from the revenue losses stemming from the tax cuts), analysts still do not have enough data to specify the precise factors behind the recent spurt in revenues. Nevertheless, a few intriguing facts are known.

First, about half of the revenue “surprise” estimated by OMB comes from unexpectedly strong growth in corporate tax receipts. This is in line with economic data showing that the growth of corporate profits in the current recovery to date has been stronger than in any comparable post-World War II period and that corporate profits have captured an exceptionally large share of the total economic growth that has occurred in the current recovery, with wages and salaries receiving an exceptionally small share. It is also in line with another revision to OMB's February projections. As of February, OMB estimated that growth in corporate profits and in wages and salaries in 2006 would be approximately equal, with both forms of income growing by about 3 percent (after adjusting for inflation). In the Mid-Session Review, however, OMB estimates that corporate profits will grow by more than 12 percent this year, after adjusting for inflation, while wages and salaries will grow by less than 2 percent.

Second, CBO has reported that much of this year’s growth in individual income-tax revenues has been concentrated in nonwithheld receipts, which largely represent taxes on investment income, such as interest, dividends, and capital gains. These sources of income tend to flow disproportionately to high-income households.

Finally, it is noteworthy that stronger-than-expected revenue growth in 2005 was not accompanied by stronger-than-expected economic growth.[11]

These facts have led some to suggest that the higher-than-expected revenue growth observed this year and last year may stem partly from increases in income inequality. In its May 2006 Monthly Budget Review, CBO commented, “growth in incomes in 2005 may have been concentrated more than expected among higher-income taxpayers, who face the highest tax rates.” [12] A May Wall Street Journal article offered the same explanation: “As America’s rich get richer, the taxes they pay on their increasing income is yielding a windfall for the U.S. Treasury.” [13]

Certainly, the strong growth in nonwithheld receipts likely reflects growing income inequality, given that investment income is concentrated among high-income taxpayers. But there is also evidence of rapid growth in high-income salaries and executive compensation, and so growth in other revenue sources may also reflect increased inequality. As the investment firm Goldman Sachs explained in a recent analysis of long-term trends toward increased income inequality, “Because the income tax code is progressive — higher incomes mean higher tax rates — for any given level of national income, a more skewed distribution of income should generate more tax revenue.”[14] Increased income inequality can thus yield higher-than-expected revenue growth even in the absence of higher-than-expected economic growth, as was observed last year.

Other New Evidence of Rising Income Inequality

New data from economists Thomas Piketty and Emmanuel Saez for years through 2004 show that income concentration increased dramatically in 2004. The jump in income concentration in 2004 was one of the largest one-year increases on record, with data going back to 1913.[15] The Piketty/Saez data show, for example, that the top one percent of households garnered 36 percent of the increase in household income in 2004, with the average incomes of the top one percent of households growing more than five times as fast (in percentage terms) as the average incomes of the rest of the population.

Other data also point to this trend. Data through the first quarter of 2006 show that wage and salary growth has been unusually weak during the current recovery, while the growth of corporate profits has been unusually rapid. With the wide disparity between gains in wages and gains in corporate profits continuing through the first part of 2006, it is likely that the trend toward increased income inequality that Piketty and Saez document through 2004 has continued since then as well. High-income households own a highly disproportionate share of corporate assets and derive significant income from those assets. Large increases in corporate profits boost their incomes without having much effect on the incomes of other households. Further, as noted, executive compensation and bonuses have been increasing rapidly in recent years, but workers’ wages have stagnated through much of the current recovery period.[16]

Medium- and Long-Term Budget Outlooks Remains Bleak

OMB now projects that this year’s budget deficit will equal $296 billion, or 2.3 percent of GDP. While the decline in the deficit estimate is welcome news, such a deficit still would represent a swing from surplus to deficit of $800 billion (or 6 percent of GDP) as compared to the budget projections that CBO and OMB issued in early 2001, when they forecast a substantial surplus in 2006. In CBO’s most recent examination of the factors behind the swing from surpluses to deficits, CBO’s data attribute about 30 percent of the budget deterioration in 2006 (relative to the projections that CBO made at the start of 2001) to the tax cuts, another 30 percent to technical reestimates, a little more than 25 percent to increases in security spending, and the remaining 15 percent to other spending increases.

The Historical Average Is Not Very Useful for Assessing the Appropriate Level of Revenue In the Years Ahead

The Administration argues that its tax cuts must be extended beyond their scheduled expiration, despite the nation’s fiscal situation. It claims that the President’s tax policies are essential for the economy and are raising an appropriate amount of revenue, and that any steps toward deficit reduction should occur on the spending side of the budget. The new budget projections are likely to show that revenues in 2006 will be 18.3 percent of GDP, the average over the past 30 years, and Administration officials and tax-cut proponents are likely to cite this figure as evidence that taxes are at an appropriate level and cannot safely go higher.

Such an argument, however, assumes that the historical average somehow constitutes the standard for revenue adequacy. In fact, revenues at their 30-year average of 18.3 percent of GDP would not have balanced the budget in any of the last 30 years. The only balanced budgets over this period occurred in the last four years of the Clinton Administration, from 1998-2001, when the 1990 and 1993 tax increases and the economic boom of the late 1990s raised tax revenues above the historical average.

Although federal spending today is not above its historical average level as a share of the economy (spending in 2006 is slightly below the 30-year average of 20.9 percent of GDP), revenues at their historical average of 18.3 percent of GDP leave a deficit of more than 2 percent of GDP, or about $300 billion. Persistent deficits of this size are unsustainable; they cause the debt to grow faster than the economy, with the result that the nation’s debt burden constantly rises.

Of particular concern is the fact that the government’s future obligations will exceed historical revenue levels by substantial amounts. During the next 30 years, continuing growth in the cost of health care and the aging of the population will lead to significant increases in Medicare, Medicaid, and Social Security costs. If revenues remain at 18.3 percent of GDP, the federal budget will, under reasonable budget projections, be in deficit every year for as far as the eye can see, and deficits will be on an ever-upward trajectory. For these reasons, comparing current revenues to the historical average does not provide much useful information about what level of revenues will be adequate or appropriate in the years ahead.

Furthermore, OMB’s new projections show that the deficit will rise next year (in fiscal year 2007) as a share of the economy. The new OMB projections show deficits falling in years after that, but those estimates hinge on highly unrealistic assumptions. In particular, the OMB projections assume an unrealistically low level of funding for the Iraq War in fiscal year 2008 and no new funding beyond that. Further, OMB assumes that Alternative Minimum Tax relief will not be extended beyond 2007, with the result that 30 million taxpayers will pay the AMT in 2010. (By 2010, the annual cost of AMT relief will exceed $70 billion.)`

CBO projections that are based on more reasonable assumptions indicate that if the tax cuts are extended beyond 2010, deficits will remain equal to or greater than 2 percent of GDP through 2016, after which the nation’s fiscal condition is expected to worsen further as a result of rising health care costs and demographic changes. This troubling outlook is little changed by the latest revenue figures as there is little reason to believe the new figures indicate substantial long-term fiscal improvement.

Indeed, some observers expect revenue growth to slow even before the end of the current recovery. Goldman Sachs recently warned that “the fact that the bulk of surprises have occurred in nonwithheld personal taxes and in corporate taxes continues to suggest that the strength [of the recent revenue growth] is largely transitory.”[17]

Conclusion: Nation Still Faces Major Long-Run Fiscal Challenges

High deficits at this stage in the recovery are particularly disturbing given the major fiscal challenges the nation will face in the coming decades, as the baby boomers begin to retire in large numbers. Commenting on the increase in this year's revenues and these future challenges, former CBO Director Doug Holtz-Eakin said, “The long-term outlook is such a deep well of sorrow that I can’t get much happiness out of this year.”[18]

This troubling outlook is not materially changed by the latest revenue figures. Simply put, there is little reason to believe the new figures indicate substantial long-term fiscal improvement or are a true indication of revenue adequacy.

End Notes

[1] “Remarks by the President on the Mid-Session Review,” July 11, 2006.

[2] As discussed on page nine, the Administration projects that deficits will fall in later years, but these projections rely on unrealistic assumptions.

[3] More precisely, we compare revenue growth across business cycles by constructing quarterly revenue figures as weighted averages; for example, we estimate revenues in the second quarter of fiscal year 2001 to be (1/2) x revenues in fiscal year 2000 plus (1/2) x revenues in fiscal year 2001. We then compare growth over the 22 quarters following the business cycle peak.

[4] Marc Labonte, “What Effects Have the Recent Tax Cuts Had on the Economy?” Congressional Research Service, updated April 14, 2006.

[5] For a more general discussion of claims that tax cuts “pay for themselves,” see Richard Kogan and Aviva Aron-Dine, “Claim that Tax Cuts ‘Pay for Themselves’ Is Too Good to Be True: Data Show No ‘Free Lunch’ Here,” Center on Budget and Policy Priorities, revised July 12, 2006.

[6] See for example, Wall Street Journal, “Tastes Great, More Filling,” February 3, 2006.

[7] For more on dynamic scoring, see Jason Furman, “A Short Guide to Dynamic Scoring,” Center on Budget and Policy Priorities, July 12, 2006.

[8] See James Horney, “A Smoking Gun: President’s Claim That Tax Cuts Pay for Themselves Refuted By Administration’s Own Analysis,” Center on Budget and Policy Priorities, revised July 14, 2006.

[9] For more detailed comparisons, see Isaac Shapiro, Richard Kogan, and Aviva Aron-Dine, “How Does this Recovery Measure Up?” Center on Budget and Policy Priorities, revised July 10, 2006.

[10] For further discussion, see Aviva Aron-Dine and Joel Friedman, “The Capital Gains and Dividend Tax Cuts and the Economy: New Treasury Report Paints Misleading Picture,” Center on Budget and Policy Priorities, March 27, 2006.

[11] It seems possible, but not at all certain, that there will be stronger-than-anticipated economic growth in fiscal year 2006. OMB now projects real GDP growth of 3.6 percent in fiscal year 2006, as compared with its 3.4 percent real growth projection in February. Goldman Sachs, however, notes that, “the US economy ended the first half of 2006 on an uninspiring note,” with several economic indicators performing more weakly than expected in the second quarter of the calendar year (for which GDP data is not yet available). Goldman Sachs, “The Stance of Monetary Policy: Enough’s Enough,” US Economics Analyst, July 7, 2006.

[12] Congressional Budget Office, Monthly Budget Review, May 4, 2006.

[13] Deborah Solomon, “Their Income Up, U.S. Rich Yield a Tax Windfall,” Wall Street Journal, May 20, 2006.

[14]Goldman Sachs, “The Macro Effects of Rising Income Inequality,” US Economics Analyst, June 30, 2006.

[15] Thomas Piketty and Emmanuel Saez, “Income Inequality in the United States: 1913-1998,” Quarterly Journal of Economics, February 2003, http://elsa.berkeley.edu/~saez/pikettyqje.pdf. The updated data series is available at http://elsa.berkeley.edu/~saez/TabFig2004prel.xls. Also see Aviva Aron-Dine and Isaac Shapiro, “New Data Show Extraordinary Jump in Income Concentration in 2004,” Center on Budget and Policy Priorities, July 10, 2006.

[16] See Isaac Shapiro and Joel Friedman, “New CBO Data Indicate Growth in Long-Term Income Inequality Continues,” Center on Budget and Policy Priorities, January 29, 2006.

[17] Goldman Sachs explains: “By far the largest component [of the unexpected growth in personal tax receipts] reflect[s] one-off events such as better than expected year-end bonuses, capital gains realizations, and the like. … While the strength in corporate taxes appears more genuinely rooted in profit growth, this is more vulnerable in a mature expansion. … [P]rospects for further strong growth in profits appear constrained.” Ed McKelvey, GS US Daily Comment, May 9, 2006.

[18] Edmund L. Andrews, “Surprising Jump in Revenues Is Curbing Deficit,” New York Times, July 9, 2006.

More from the Authors

Areas of Expertise

Areas of Expertise