What to Watch For in the Census Bureau's Report on Health Insurance Coverage in 2012

The Census Bureau will release estimates on September 17 of the number of Americans with and without health insurance coverage in 2012, based on its annual Current Population Survey (CPS). Other survey data and historical trends provide clues to what the Census data will likely show.

Preliminary survey data from the Centers for Disease Control and Prevention (CDC) indicate that in 2012, the number of uninsured Americans fell for the second consecutive year. These data further suggest that federal policies were primarily responsible for the gains in coverage.

As in 2011, the largest increase in coverage, according to the CDC data, occurred among young adults, a group benefiting from an Affordable Care Act (ACA) provision that allows adult children up to age 26 to stay on their parents’ private insurance plans. In contrast, private health coverage among adults aged 26 to 64 — a group for whom the ACA’s major coverage expansions will not take effect until 2014 — declined for the fifth consecutive year in 2012.

Number of Uninsured Fell Substantially but Remains Much Higher Than Before Recession

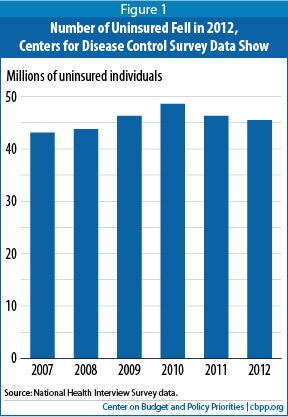

In June, the CDC released early estimates from its National Health Interview Survey (NHIS), a nationally representative sample that tends to track well with the more widely known Census Bureau data from the CPS. NHIS data indicate that the number of Americans without health insurance coverage declined by 800,000 in 2012, to 45.5 million (see Figure 1).

The share of Americans without coverage also dropped for a second straight year — from 15.1 percent in 2011 to 14.7 percent in 2012. After reaching a historic high of 16.0 percent in 2010, the uninsured rate in 2012 returned to its 2007 level, prior to the Great Recession.[1]

The CDC data also show, however, that due to population growth, 2.6 million more Americans lacked health insurance coverage in 2012 than in 2007. All of this increase occurred among adults aged 26 or older.

Health Reform Provision Expanded Coverage for Young Adults

According to the NHIS data, the number of Americans with health insurance rose in 2012, due primarily to a continued increase in the share of young adults with private coverage. In 2011, adults aged 19 through 25 experienced an unprecedented gain in private coverage and consequent drop in the share without insurance coverage. These coverage gains continued in 2012, as some 57.2 percent of adults aged 19-25 had private coverage — a full percentage point more than in 2011 and 6.2 percentage points more than in 2010. Similarly, the percentage of young adults who lack insurance declined by 1.5 percentage points between 2011 and 2012 — from 27.9 percent to 26.4 percent — as a result of the large increase in private coverage, as well as notable enrollment growth in public programs such as Medicaid and CHIP.

A provision of the Affordable Care Act likely explains much or all of the increase in private coverage among young adults. Under the ACA, adult children can now obtain coverage through their parents’ health insurance plans up to their 26th birthday. The NHIS data show that while the share of young adults with private coverage rose by 6.2 percentage points between 2010 and 2012, the share of those aged 26 through 35 with private coverage fell by 0.8 percentage points. The Commonwealth Fund earlier estimated that as many as 6.6 million young adults remained on or joined their parents’ plans between November 2010 and November 2011 because of the ACA provision.[2]

This ACA provision took effect in September 2010, meaning that 2012 represented the second full year that it affected health insurance coverage rates. The coverage gains resulting from the provision may grow over time.

Continuing Erosion of Private Coverage Remains a Concern

The NHIS data show that private insurance coverage rates for non-elderly adults overall remained stable for a third straight year at 64.1 percent of this population. This masks, however, the offsetting effects of a gain in private coverage among those aged 19 through 25 and continued deterioration of private coverage among those not affected by the ACA provision for young adults because they are 26 or older. Among people aged 26 through 64, the private coverage rate fell for the fifth consecutive year in 2012. It also may be noted that the 64.1 percent private coverage rate for the non-elderly adult population overall is far below the peak of 74.7 percent reached in 1999.

The major coverage provisions of the ACA scheduled for implementation in 2014 should help stem — and begin to reverse — the persistent erosion of private coverage. Reforms will take effect in the private individual and small group markets, new health insurance marketplaces will be established in states for individuals and small businesses, and the federal government will provide premiums and cost-sharing subsidies to low- and moderate-income individuals who purchase private insurance through these marketplaces. In addition, small employers will be eligible for tax credits if they offer coverage through the new marketplaces. Firms with 50 or more employees will be required to offer coverage or pay a penalty (this requirement has been delayed until 2015).

More than three of every five non-elderly Americans continue to get coverage through employers, and the NHIS data show a wide disparity in the uninsured rates between unemployed individuals aged 18-64 (47.1 percent of whom lack coverage) and employed individuals (18.5 percent of whom lack coverage). The new marketplaces will reduce this disparity by creating health insurance markets that offer affordable coverage to people who lack access to affordable coverage through work.

Public Programs Continue to Serve More During the Recession, Particularly Children

Medicaid and CHIP are a growing source of coverage for children and adults, particularly during the recent recession and its aftermath. The percentage of children under age 18 with publicly funded coverage rose by 1.1 percentage points in 2012, to 42.1 percent, according to the NHIS data. This growth was the reason why the overall percentage of children who were uninsured fell again, by 0.4 percentage points to a historic low of 6.6 percent, even though the percentage of children with private coverage remained unchanged.

Since the CDC began collecting these data in 1997, the percentage of children who are uninsured has been cut in half, despite the continued erosion of private insurance coverage. In the typical state, Medicaid and CHIP cover children in families with income up to 250 percent of the poverty line (roughly $47,725 for a family of three). Federal policies — including the temporary increase in Medicaid funding for states through June 2011 (provided by the 2009 Recovery Act and a subsequent extension), as well as the ACA requirement that states maintain their Medicaid and CHIP eligibility levels and enrollment procedures — bolstered Medicaid and CHIP’s ability to offset the loss of private coverage during and after the economic downturn.

The public coverage rate among adults also has risen steadily, reaching 16.4 percent in 2012. (The increase has been more modest among adults — a gain of 4.1 percentage points since 2007 — than among children, where the gain over this period was 9.4 percentage points.) Unlike among children, this growth has not fully offset the decline in private insurance coverage, so the percentage of non-elderly adults who lack coverage has continued to grow.

State Medicaid income eligibility limits for parents are far lower than those for children; the eligibility limit in the typical (or median) state is only 61 percent of the poverty line for working parents and 37 percent of the poverty line for unemployed parents. In addition, few states offer any Medicaid coverage to non-disabled adults without children. Through the ACA, states will be able for the first time — beginning in 2014 — to extend Medicaid at relatively little cost to themselves to adults with incomes up to 133 percent of the poverty line.[3] This should result in substantial progress in covering adults, just as expansions in Medicaid and CHIP have done for children.

However, only about half of the states will take up the Medicaid expansion in 2014. And nearly half of the states that have turned down or are leaning against the expansion are in the South, the region with the highest share of uninsured residents. According to the NHIS data, 17.5 percent of all people living in the South were uninsured in 2012, a higher share than in any other part of the country.

End Notes

[1] All NHIS estimates and analysis cited in this paper are based on Robin Cohen and Michael Martinez, “Health Insurance Coverage: Early Release of Estimates From the National Health Interview Survey, 2012,”Centers for Disease Control and Prevention, June 2013.

[2] Sara Collins et al., “Young, Uninsured, and in Debt: Why Young Adults Lack Health Insurance and How the Affordable Care Act is Helping: Findings from the Commonwealth Fund Health Insurance Tracking Survey of Young Adults, 2011,” the Commonwealth Fund, June 2012.

[3] The federal government will pay 100 percent of the costs associated with this expansion in the first three years and then no less than 90 percent on a permanent basis.

More from the Authors

Areas of Expertise