Testimony: Chad Stone, Chief Economist, on Policy Prescriptions for the Economy

Before the Senate Budget Committee United States Congress

Chairman Conrad, Senator Sessions, and other members of the Committee, thank you for the opportunity to testify today on policy prescriptions for the economy.

To use the medical analogy in the title of this hearing, the U.S. economy is experiencing a long and difficult recovery from a severe acute illness — the 2007-2009 financial crisis and recession — and remains weak, with the risk of a relapse. Separately, U.S. policymakers have behaved with a reckless disregard for the long-term health of the economy over the last decade by abandoning, despite the efforts of this committee, the fiscal discipline that produced a balanced budget in the late 1990s and by failing to prepare for the stresses the retirement of the baby boom generation will put on the budget. Contrary to much of the rhetoric during the recent debt-ceiling debate, however, the United States' current acute economic problems — sluggish growth, a huge jobs deficit, and stubbornly high unemployment — do not stem directly from a lack of fiscal discipline, and a premature application of fiscal rectitude will do more harm than good.

My policy prescriptions follow from this diagnosis. First, it is time reject the arguments prominent in the debt ceiling debate that excessive government spending and the buildup of debt since 2008 are the causes of our current economic troubles and that cutting spending sharply and quickly is the cure. Indeed, the economic situation today cries out for significant fiscal stimulus such as that proposed in President Obama's American Jobs Act. Providing that stimulus can be accomplished without compromising our long-term fiscal stabilization objectives by pairing it with a credible program of deficit reduction that does not kick in immediately but rather is deferred until a time when the economy is expected to be stronger. I believe the economic risks from failing to provide fiscal support to the flagging economic recovery are much more significant than the economic risks from temporarily running larger budget deficits.

My prescription is fully consistent with mainstream economic analysis like that underlying recent statements by Congressional Budget Office (CBO) Director Doug Elmendorf and Federal Reserve Chairman Ben Bernanke, each of whom recognizes that the economy is currently fragile and short-term fiscal stimulus is not incompatible with longer-term fiscal restraint.

Testifying before the Joint Select Committee on Deficit Reduction earlier this week, Elmendorf said:

There is no inherent contradiction between using fiscal policy to support the economy today, while the unemployment rate is high and many factories and offices are underused, and imposing fiscal restraint several years from now, when output and employment will probably be close to their potential. If policymakers wanted to achieve both a short-term economic boost and medium-term and long-term fiscal sustainability, a combination of policies would be required: changes in taxes and spending that would widen the deficit now but reduce it later in the decade. Such an approach would work best if the future policy changes were sufficiently specific and widely supported so that households, businesses, state and local governments, and participants in the financial markets believed that the future fiscal restraint would truly take effect.[1]

In a speech on the U.S. economic outlook last week, Bernanke said:

[W]hile prompt and decisive action to put the federal government's finances on a sustainable trajectory is urgently needed, fiscal policymakers should not, as a consequence, disregard the fragility of the economic recovery. Fortunately, the two goals — achieving fiscal sustainability, which is the result of responsible policies set in place for the longer term, and avoiding creation of fiscal headwinds for the recovery — are not incompatible. Acting now to put in place a credible plan for reducing future deficits over the long term, while being attentive to the implications of fiscal choices for the recovery in the near term, can help serve both objectives.[2]

The rest of my testimony is an elaboration on these themes. In it, I stress the importance of differentiating between 1) the longer-term policies needed to produce sustainable growth and broadly shared prosperity at high levels of employment and 2) the short-term policies needed to restore high levels of employment in the wake of a deep recession. In particular, policies aimed at reducing the budget deficit are a key ingredient of longer-term policy but are likely to be counterproductive in the short run if implemented too precipitously.

I make the case for fiscal stimulus in the short term to support the economic recovery; I discuss recent analysis confirming the conventional wisdom that cutting the budget deficit too much too fast — whether through spending cuts, revenue measures, or a combination of the two – is harmful to the recovery; and I discuss why long-run fiscal stabilization should be achieved through a balanced package of spending and revenue measures that protects low-income programs, as recommended by recent budget commissions and as was done in previous major deficit reduction efforts.

The Case for Fiscal Stimulus

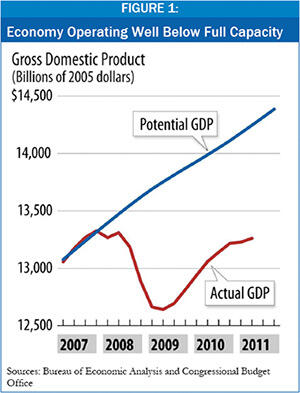

A host of developments precipitated by the bursting of the housing bubble threw the U.S. economy into a deep hole in 2008 and the first half of 2009, with for the output of goods and services (actual GDP) falling well below what the economy was capable of supplying with high employment, normal labor force participation, and full utilization of existing capacity (potential GDP). Extraordinary monetary and fiscal policy measures undertaken by the Federal Reserve, Congress and two administrations arrested the fall and kept the hole from getting deeper, [3] but we are still trying to dig out of that hole and we've had limited success so far. (Figure 1)

The Problem of Excess Capacity

CBO estimates that the recession and subsequent economic slump have already cost the economy $2½ trillion in lost output (the cumulative gap between actual and potential GDP since late 2007) and that without a pickup in the expected pace of recovery, we will lose another $2½ trillion before getting back to full employment. Moreover, as CBO notes, "Not only are the costs associated with the output gap immense, but they are also borne unevenly, falling disproportionately on people who lose their jobs, who are displaced from their homes, or who own businesses that fail." [4]

Policies that reduce the size of the output gap along the way to restoring full employment reduce the economic costs and human hardship of an economic slump. Long-term unemployment is at unprecedented levels, and as Tuesday's grim report from the Census Bureau on income, poverty, and health insurance in 2010 shows, the recovery is proceeding too slowly to reduce that hardship substantially anytime soon.

A large output gap stems mainly from inadequate aggregate demand for goods and services, and policies that increase aggregate demand are likely to be more successful at closing the output gap than policies that give businesses tax incentives to expand production. The problem for most businesses in an economic slump is not that they don't have enough capacity to meet existing demand but that they don't have enough demand to fully utilize their existing capacity. Thus policies that put more customers in the stores with more money to spend are likely to be more successful at closing the output gap and creating jobs than giving businesses tax breaks. Policies that focus on raising the purchasing power of unemployed workers and middle- and low-income households are likely to be more successful per dollar of budget costs at increasing spending and creating jobs than policies cutting tax rates for high income taxpayers who are likely to save a significant portion of any tax cut they receive.

Policies to Increase Aggregate Demand

Fiscal stimulus in the form of tax cuts aimed at middle and lower income households, relief for state and local governments to avoid layoffs of teachers and other critical employees, direct transfers to unemployed workers, and direct spending on infrastructure are all measures that can effectively raise aggregate demand under the right circumstances.

Prior to the Great Recession, mainstream economists were confident that monetary policy could moderate swings in the business cycle and skeptical that fiscal stimulus could be implemented quickly enough to be effective in the mild run-of-the-mill recessions thought likely to occur. The problem was not that cutting taxes and increasing government spending would not be able to increase aggregate demand but rather that the economy would already be recovering by the time the boost to economic activity kicked in and the Fed would react by tightening monetary policy (raising interest rates) to offset the by-then-unwanted stimulus.

That is not the situation we have been in since the recession began, and the Fed has stated that it does not anticipate raising interest rates over the next two years. According to most forecasts, we face a long period of high unemployment and excess productive capacity. These are just the economic circumstances in which appropriate fiscal stimulus will likely be most effective in stimulating demand and creating jobs.

CBO estimates that under these circumstances,

- purchases of goods and services by the federal government and transfers to state and local governments for infrastructure would have a multiplier (additional economic activity per dollar spent) of between 1.0 and 2.5 (once the money is actually dispersed

- transfers to individuals (such as unemployment compensation) would have a multiplier of 0.7 to 1.8,

- tax cuts for lower- and middle-income people would have a multiplier of 0.6 to 1.5.

In contrast,

- tax cuts for higher income people would have a multiplier of 0.2 to 0.6, and

- tax cuts for businesses primarily affecting cash flow (such as the net operating loss provision in the 2009 Recovery Act and the foreign dividend repatriation proposals now circulating) would have a multiplier of 0.0 to 0.4.

These are the multipliers CBO estimates would apply to provisions in the 2009 Recovery Act, which CBO estimates boosted GDP in 2010 by between 1.5 and 4.2 percent, boosted employment by between 1.3 and 3.3 million jobs, and lowered the unemployment rate by between 0.7 and 1.8 percentage points compared with what they would have been without those measures. The contribution of the various measures in the Recovery Act to those results are a function of how much money was spent, the timing of that spending, and the estimated multiplier for that type of spending.

Private forecasters like my co-panelist Mark Zandi and Macroeconomic Advisers also attribute positive macroeconomic effects to the Recovery Act, the payroll tax holiday and extension of unemployment insurance benefits in the tax/unemployment insurance compromise enacted at the end of last year, and the President's latest American Jobs Act proposals.

I know there is a popular perception that the Recovery Act stimulus "failed" because the unemployment rate has exceeded even the rate the White House (and most other forecasters at the time) expected in the absence of any policy, much less the rate predicted if the policy was enacted. But what we have learned subsequent to those forecasts is that the underlying economy was deteriorating much more rapidly than those forecasts assumed. The recent revisions to GDP show that the economic decline in late 2008 and early 2009 was much sharper than was originally estimated. Others may produce different estimates of how much of an impact the Recovery Act had in preventing economic performance from being even worse than it was, but the comparison should be to a plausible counterfactual of what the economy would have looked like in the absence of the policy not to a baseline pre-policy forecast that in retrospect was much too rosy.

I believe the case for fiscal stimulus is compelling in an economy with substantial economic slack, a huge jobs deficit, and stubbornly high unemployment. Policies that are easy to implement, have high bang-for-the-buck, and relieve hardship should be top candidates. At a bare minimum, of course, the payroll tax cut and federal unemployment insurance should be extended for another year to prevent their scheduled expiration from imposing an additional drag on the recovery. But the President was right to go beyond merely treading water and propose additional measures like expanding the payroll tax cut, infrastructure investments, and aid to states to prevent layoffs of teachers and other essential workers.

Policies that will add the budget deficit without providing additional stimulus should not be part of a stimulus package. These include a repatriation holiday for foreign earnings of U.S. multinationals and other corporate tax cuts.

The False Promise of Expansionary Fiscal Austerity

Deficit reduction is critical to long-term growth, but reducing deficits too much or too fast in a weak economy is counterproductive. That mainstream economic view has been challenged recently by claims that immediate large reductions in government spending are necessary for successful deficit reduction and can be good for the economy even in the short run. Supporters of this claim point to empirical studies of major deficit-reduction initiatives by other countries.[5] These studies, they argue, show that programs composed largely of spending cuts are more likely to be successful at stabilizing deficits — and less harmful (and even beneficial) to the economy in the short run — than programs with a larger tax-increase component.

Recent research has cast serious doubt on these claims and on the relevance of this evidence to current economic and budget conditions in the United States. The International Monetary Fund, after correcting for potential biases in the way fiscal austerity episodes are usually identified in this literature, concludes, "The idea that fiscal austerity triggers faster growth in the short term finds little support in the data." [6] Konczal and Jayadev found that none of the episodes cited in one of the most prominent studies in this literature — by Harvard economists Alberto Alesina and Sylvia Ardagna [7] — took place in a country still feeling the effects of a large recession as the United States is now, with substantial economic slack, tepid economic growth, and high unemployment. [8] The Congressional Research Service's examination of the same literature concludes, "fiscal adjustments beginning in a slack economy (such as the current situation in the U.S.) appear to have a low probability of success." [9]

Advocates of spending-heavy deficit reduction argue that even if it is not expansionary in the short run, it is still preferable to tax-based deficit reduction because it is more likely to result in lasting results and does less harm to the economy in the short-term. This finding too has little relevance to current U.S. economic and budget conditions.

Successful, short-sharp fiscal contractions are usually accompanied by a rapid decline in interest rates, a moderation of wage growth, and an improvement in the trade balance. But U.S. interest rates are already low and the Fed does not have the option of lowering them much further in order to offset the contractionary effects of immediate deficit-reduction measures, whether tax- or spending-based. It would be very difficult for the United States to increase exports enough to offset those contractionary effects when other developed countries also are trying to reduce their budget deficits and get out of an economic slump by expanding their exports. And neither public nor private wages are growing faster than productivity.

In the latest summary of its findings, "Painful Medicine: Although advanced economies need medium-run fiscal consolidation, slamming on the brakes too quickly will hurt incomes and job prospects," the IMF flatly rejects the idea that deficit reduction would be expansionary in countries facing a weak recovery:

Will deficit reduction lead to stronger growth and job creation in the short run?

Recent IMF research provides an answer to this question. Evidence from data over the past 30 years shows that consolidation lowers incomes in the short term, with wage-earners taking more of a hit than others; it also raises unemployment, particularly long-term unemployment. [10]

The Congressional Research Service summarizes its examination of the austerity literature this way:

The findings in the Alesina and Ardagna study that successful debt reductions were associated with higher growth when spending cuts were used was based on 9 observations out of 107 instances of deficit reduction, or less than 10% of the sample. In addition, most of the countries where debt reductions were successful were at or close to full employment, while the United States remains well below full employment, raising questions as to whether this evidence is applicable to current U.S. conditions. Thus, both methodological questions and questions of applicability to current circumstances can be raised for the Alesina and Ardagna, and similar, studies.

Finally, Roberto Perotti, one of the leading researchers cited by supporters of spending-heavy deficit reduction, recently conducted detailed case studies of the four largest multi-year deficit-reduction efforts that researchers have commonly regarded as spending-based. He found that they were actually much smaller, and much less tilted toward spending cuts, than previous studies had assumed. [11]

The claim that government spending is crowding out productive private investment at a time when the economy has considerable economic slack goes as much against mainstream economic analysis as the arguments that deep budget cuts in a weak economy will trigger stronger growth and job creation. For government spending to crowd out private spending, the workers, factories, and machines needed to meet the demand generated by the government spending would have to be diverted from other productive activities. To be sure, that can occur in a high-employment economy with no economic slack. But the current situation is very different. For example, when the government provides additional unemployment insurance (UI) benefits to workers struggling to find a job, businesses are helped rather than harmed: the benefits increase consumer demand for goods and services and thereby enable businesses to put unemployed workers back to work and put idle capacity back into production (or to refrain from cutting workforces and production even further).

The crowding out argument would have more force if the economy today looked more like the economy in the 1990s expansion — the longest in our country's history and the last time we had a balanced budget. But in today's economy, weak demand, not competition for funds, is the much more plausible explanation for inadequate investment and job creation.

In summary, despite claims to the contrary, conventional economic wisdom still rings true: austerity and growth do not mix in the short term. Empirical support for the view that sharp, immediate cuts in government spending would be good for the U.S. economy was never strong, and it's getting weaker.

Principles for Long-Term Deficit Reduction

My discussion of the desirability of enacting policies to support the economic recovery and my critique of arguments for large immediate spending cuts should in no way be interpreted as minimizing the importance of meeting our long-term budget challenge. But we do have time to meet that challenge in a responsible way.

The Center on Budget and Policy Priorities laid out its principles for deficit reduction along with some cautions in March. [12] The overall objective should be to stabilize the debt as a share of GDP in a reasonable period of time, but as I have discussed in this testimony, not so quickly as to endanger the recovery. In pursuing this goal, policymakers should follow a series of principles that would make deficit-reduction efforts equitable and more likely to be effective and sustainable over time. At the same time, they should avoid a series of steps that not only would make deficit cutting harder to achieve and sustain but also would hurt the economy down the road.

As CBO Director Elmendorf testified before the Joint Select Committee on Deficit Reduction earlier this week, "The nation cannot continue to sustain the spending programs and policies of the past with the tax revenues it has been accustomed to paying. Citizens will either have to pay more for their government, accept less in government services and benefits, or both."

Recognizing that reality, CBPP believes that any deficit-reduction plan should be balanced and inclusive, affecting all parts of the budget and with the savings split about 50-50 over time between program reductions and revenue increases. A substantial share of the new revenues should come from scaling back "tax expenditures:" the more than $1 trillion a year in tax breaks that the tax code provides each year for particular taxpayers or groups of taxpayers. Policymakers should avoid misguided proposals such as those that would place a statutory cap on total annual federal spending or write a balanced budget requirement into the U.S. Constitution — either of which would diminish the government's ability to respond effectively to recessions (and, in fact, would make recessions worse) while largely or entirely shielding taxes from deficit-reduction efforts.

I want to particularly highlight one final principle. Policymakers should avoid making the problems of poverty and inequality, both of which are higher in the United States than in most other Western industrialized nations, still worse. Policymakers should adopt and adhere to the principle espoused in the Bowles-Simpson deficit-reduction plan to protect the disadvantaged. The major deficit-reduction packages of 1990, 1993, and 1997 all generally protected programs for low-income Americans; those packages, in fact, reduced poverty and inequality even as they reduced deficits.

The last point becomes even more crucial in light of the grim figures in this week's report from the Census Bureau on income, poverty, and health insurance in 2010, which showed that the share of all Americans and the share of children living in poverty, the number and share of people living in "deep poverty," and the number without health insurance all reached their highest level in many years — in some cases, in several decades — while median household income fell significantly after adjusting for inflation.

The extent and depth of poverty in coming years and decades will be strongly affected by whether the Joint Committee on Deficit Reduction, and Congress as a whole, adhere to a core principle that the commission chaired by Erskine Bowles and Alan Simpson set forth in its report and the Senate's "Gang of Six" sought to honor in its plan — that deficit reduction should be designed so that it does not increase poverty and should therefore shield low-income assistance programs from cuts — or whether the Joint Committee and Congress instead impose significant cuts in programs for those at the bottom of the income ladder.

Conclusion

The U.S. economy continues to struggle to recover from the severe 2007-2009 recession and subsequent protracted slump. We can take positive steps to give the recovery a boost without endangering efforts to stabilize our long-term debt. That will reduce the economic waste and human hardship that are evident in the current weak recovery. When we turn to the long-term budget challenge, we can and should protect the most vulnerable among us in order to reverse the recent history of poverty becoming wider and deeper.

End Notes

[1] Douglas W. Elmendorf, Director, Congressional Budget Office, "Confronting the Nation's Fiscal Policy Challenges," statement before the Joint Select Committee on Deficit Reduction, U.S. Congress, September 13, 2011. http://www.cbo.gov/doc.cfm?index=12413

[2] Ben S. Bernanke, Chairman, Federal Reserve Board, "The U.S. Economic Outlook," speech at the Economic Club of Minnesota Luncheon, September 8, 2011. http://www.federalreserve.gov/newsevents/speech/bernanke20110908a.htm

[3] See Alan S. Blinder and Mark Zandi, "How the Great Recession Was Brought to an End, "July 27, 2010. http://www.economy.com/mark-zandi/documents/End-of-Great-Recession.pdf

[4] Elmendorf, op. cit.

[5] Joint Economic Committee Republicans, "Spend Less, Owe Less, Grow the Economy," March 15, 2011: http://www.speaker.gov/UploadedFiles/JEC_Jobs_Study.pdf

[6] International Monetary Fund, "Will It Hurt?" Chapter 3 in World Economic Outlook, October 2010. http://www.imf.org/external/pubs/ft/weo/2010/02/pdf/c3.pdf

[7] Alberto F. Alesina and Sylvia Ardagna, Large Changes in Fiscal Policy: Taxes versus Spending, Working Paper 15438, National Bureau of Economic Research, October 2009. http://www.nber.org/papers/w15438.pdf?new_window=1

[8] Arjun Jayadev and Mike Konczal, ," The Boom Not The Slump: The Right Time For Austerity", The Roosevelt Institute, August 23, 2010, http://www.rooseveltinstitute.org/sites/all/files/not_the_time_for_austerity.pdf ?" http://www.bis.org/events/conf110623/perotti.pdf

[9] Jane G. Gravelle and Thomas L. Hungerford, "Can Contractionary Fiscal Policy Be Expansionary?" Congressional Research Service Report R41849, June 6, 2011.

[10] Lawrence Ball, Daniel Leigh, and Prakash Loungani, "Painful Medicine," Finance and Development, September 2011, p. 20.

[11] Roberto Perotti, "The Austerity Myth: Gain without Pain?" June 16, 2011. http://www.bis.org/events/conf110623/perotti.pdf

[12] Robert Greenstein, "A Framework for Deficit Reduction, Principles and Cautions," Center on Budget and Policy Priorities, March 24, 2011.

More from the Authors