A Common-Sense Strategy for Fixing State Pension Problems in Tough Economic Times

Restoring underfunded state and local workers’ pension programs to full fiscal health is a long-term goal for state policymakers that should be accomplished with moderate, common-sense steps, rather than drastic measures that could imperil states’ economic recoveries.

Today’s pension shortfalls were caused in substantial part by the 2001 recession and the recent Great Recession. Those recessions reduced the value of assets in pension trust funds and made it difficult for some jurisdictions to find sufficient revenues to make required deposits into the trust funds. As a result, the average state pension fund is considered “underfunded,” meaning that there are not enough assets in the fund to pay 100 percent of the future retirement benefits that current state employees have earned, even taking into account the future investment earnings on those assets.

It would be extremely difficult, as well as unnecessary, for states to immediately begin fully funding their pension shortfalls. State economies and budgets continue to struggle because of shrunken revenues and rising needs. The long-term pension shortfalls are not the cause of the current state fiscal problems, and addressing them need not overwhelm state and local budgets now or reduce states’ ability to recruit and retain a high-quality workforce.

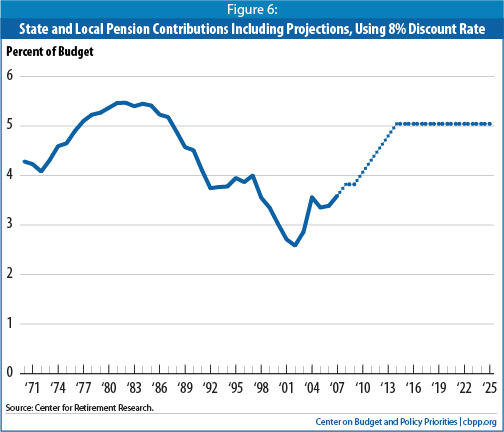

Instead, states should act now to make a few relatively straightforward legislative changes —increases in plan contributions, increases in employee contributions, and sensible changes to pension eligibility rules and benefit levels — that can remedy underfunding over time. If states and localities over the next five years boost their pension contributions to roughly 5 percent of their budgets on average (compared with the present level of 3.8 percent), they can make major progress in restoring plans to full health; if benefits are reduced or employee contributions increased, the increases in state contribution can be smaller than would otherwise be necessary.[1] In this way, states can avoid undermining either the retirement security of their employees or their ability to fund education, health care, infrastructure, and other public services necessary to maintain strong economies in both the short and long term.

States should:

- Act now to craft a plan to restore pension trust funds to solvency gradually. The long-term nature of the problem means that most state and local governments can fashion a plan that postpones significant additional pressure on state budgets for a few years until revenues have recovered from the current downturn.

- Move carefully to change, as necessary, their methods for determining needed contributions. Requiring much larger contributions right now, while state budgets are still in crisis, would mean that states and localities would have to take even more money away from other areas of spending at a time when they are already cutting important services and investments deeply.

- Immediately change pension rules to reduce the potential for uncommon but damaging abuses such as “double-dipping” (where, for example, a person claims a public pension while continuing to draw a government salary) and “spiking” (where employees artificially inflate their final year’s earnings in order to boost their pensions).

- Gradually, over the next several years, move to boost contributions to pension funds by governments and/or employees and modestly scale back benefits, while continuing to use reasonably strong pension benefits as a way to attract a high-quality workforce that otherwise might be dissuaded from public jobs by the sector’s comparatively low wages. Adequate pay and benefits are critical to states’ and localities’ ability to attract and keep high-quality teachers, nurses, police, and other employees.

- Continue to offer defined-benefit plans, since to do otherwise would actually make it harder for states to restore fund balance, as explained below.

These are general principles. Any reform strategy must reflect an individual state’s circumstances, with radical changes reserved for states whose pension plans are the most severely underfunded. (A few states have grossly underfunded their pensions in past years and/or granted retroactive benefits without funding them, including Illinois, New Jersey, Colorado, Kentucky, Kansas, and Rhode Island.)

Many states have begun to address their funding problems. Last year alone, 11 states increased employee contributions toward their future pension costs; 16 states made changes that will reduce benefits, such as changing the formula used to set pension levels. (Several states fall into both categories.) In addition, a number of states have reduced or eliminated cost-of-living increases in pension payments. Other states have made changes that will facilitate more consistent and adequate funding for pensions in the future, such as requiring at least a minimum contribution every year.

This report begins with a short primer on how public-sector pension funds operate, their current funding status, and their relationship to states’ general operating budgets. It then identifies a set of strategies that, taken together, should enable pension funds to return to fiscal health with the least amount of harm, especially in the short term, to a state and its economy.

I. How Retirement Benefits for State and Local Employees Are Funded

To understand how states and localities should solve their pension problems, it is important to understand the nature of those problems — and, more basically, why states and localities have pension funds to begin with.

The Basics: Why States Have Pension Funds

Like most workers in the United States, the people who work for state and local governments — teachers, police officers, firefighters, nurses, and many others — receive most of their compensation in the form of salaries and wages and a smaller part in benefits, including retirement benefits. Some 90 percent of state and local governments provide some form of retirement income for their employees. This is larger than the 70 percent rate for private-sector employers but comparable to the 85 percent rate for large private-sector employers (those with more than 500 workers).

Public defined-benefit plans are pre-paid — that is, state and local governments have established dedicated trust funds where money is deposited annually to cover future pension liabilities (i.e., the anticipated costs of pensions for current and past employees). Pension payments to retirees are an expense of the trust fund, not of the state’s annual operating budget.

Payments into trust funds come from employers and (usually) employees. (The state’s employer contributions are a part of its annual operating budget.) The money is invested and earns interest and dividends.

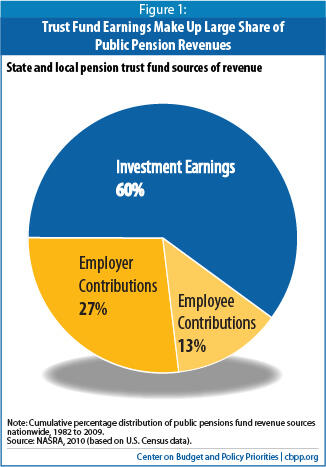

There are several good policy reasons to have pre-paid pension trust funds. Setting aside money in advance allows state and local governments to earn interest, which means less money has to be collected from taxpayers. On average over the last 17 years, investment earnings made up 60 percent of pension trust fund revenues; employer contributions made up 27 percent and employee contributions made up 13 percent. (See Figure 1.) This practice also means that if employer contributions are set at appropriate levels, state and local budgets reflect the full cost of an employee during the years that he or she is employed, so the taxpayers who benefit from the services provided by government employees pay the full cost of those services at that time. This promotes intergenerational equity — that is, it averts the practice of pushing costs on to the next generation. It also results in more realistic budget trade-offs between the cost of providing additional benefits to workers and, say, expanding existing programs or adding new ones. But as the next section discusses, the question of exactly how much money should be in those pension funds at any time is not always clear.

Public Pension Funds: Underfunded but with a “Solid Foundation”

Public pension funds at the end of 2010 held almost $3 trillion in assets.[3] That is a very large number. (The total valuation of all the companies listed on the entire New York Stock Exchange is $15 trillion.) It is also a huge improvement from 30 years ago. For much of the 20th century, pension trust funds were uncommon, and pension benefits were paid directly from operating funds instead. But the attention paid to pension funding as a result of the passage of ERISA (the federal law regulating private pensions) prompted most states and localities to establish and begin to fill pension trust funds in the 1970s and 1980s.

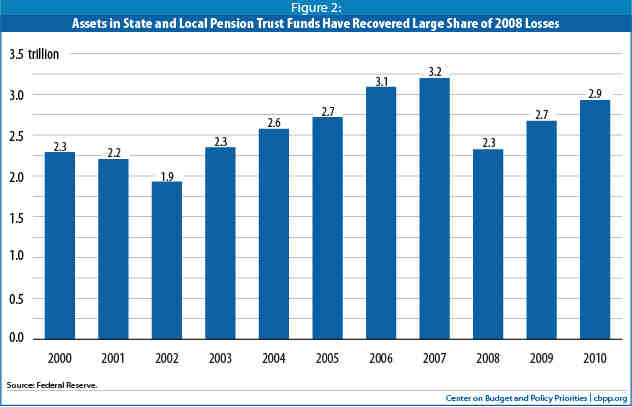

By making annual contributions of around 4 to 5 percent of their budgets — and with the assistance of a growing stock market — states and localities built up their trust funds to some $2.3 trillion by 2000, as Figure 2 shows. After temporarily declining due to the 2001 recession, pension assets grew to $3.2 trillion in 2007. The massive collapse of the financial markets in 2008 caused an even larger decline in 2008, but since then the funds have grown again and are nearly back at the $3 trillion mark. The funds have recouped two-thirds of the $0.9 trillion they lost in the 2008 market.

Because the trust funds are so large, pension expert Professor Alicia Munnell of Boston College points out, they “have a solid foundation in place. . . . [E]ven after the worst market crash in decades, state and local plans do not face an immediate liquidity crisis.” [4]

Of course, the amount of money in the funds does not by itself tell whether the funds are strong enough. Even as a fund builds up assets in the form of cash, equities, bonds, and so on, it also builds up liabilities in the form of obligations to pay future pension benefits to the workforce. If the assets are less than the liabilities, the trust fund is considered “underfunded.” The larger the underfunding, the greater the amount of money that states must put into those pension funds over time to restore them to full funding.

The size of assets is one part of the comparison. Most public pension funds use “asset smoothing” to phase in the effect of big stock market changes on the value of the fund’s assets, thereby minimizing year-to-year changes in the amount of money that the state must deposit in the fund. If the market rises (or falls) significantly more or less than the fund projected in one year, a state that uses a five-year smoothing path will recognize one-fifth of the difference in valuing its assets in the first year, two-fifths of the difference in the subsequent year, and so on. This smoothed (or actuarial value) of assets is then compared to the fund’s liabilities.

The other part of the comparison is the size of the liabilities. How to value those liabilities is complicated and controversial. The first step in calculating a pension fund’s liabilities is estimating the cost of the promised benefits in the future years when they will be paid, based on how many current workers are likely to stay on the job until retirement age, what their retirement benefits will be, and so on. The second step is estimating the cost of the promised future benefits in today’s dollars — that is, the “present value” of those future costs.

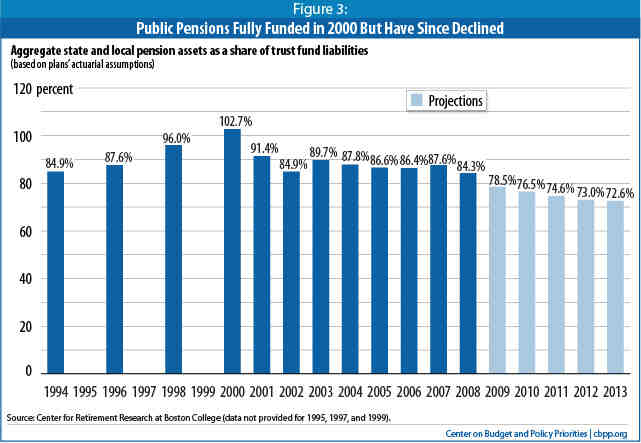

For example, as of 2009, the assets of state and local pension trust funds were valued at $2.7 trillion. The present value of their pension obligations, according to the funds’ calculations, totaled $3.4 trillion. This meant that, based on the funds’ calculations and assumptions (which are the subject of some debate), the trust funds were “underfunded” by $700 billion or 21.1 percent. To put it another way, the funding level of the average pension plan (based on the plans’ calculations and assumptions) was 78.9 percent — that is, the plans’ holdings equaled 78.9 percent of the amount the plans estimated they needed to fully fund future obligations. Because the impact of the recession-induced decline in the value of assets is being phased in, pension plan funding (as a percentage of the amount needed to fully fund future obligations, under the plans’ calculations and assumptions) will continue to decline for a few years (see Figure 3), but the market recovery of 2009 and 2010 will likely result in improvements after 2013.

Using a lower discount rate such as a riskless rate substantially raises a pension fund’s unfunded liabilities. As a result, proponents of using a riskless rate as the discount rate maintain that public pension funds are much less well funded than the funds report. They estimate a shortfall of $3 trillion rather than the $700 billion reported under the longstanding method, which commonly uses a discount rate of about 8 percent.

It also should be noted that economists are not necessarily arguing that state and local pension funds should change their investment practices, liquidate their equity portfolios, and invest solely in bonds.

A key point to understand is that the issues of: 1) how states and localities should value their pension liabilities; and 2) how much they should contribute to their pension funds each year to meet their pension obligations are two separate issues, although they obviously are related.[6]

The estimate of more than $3 trillion in unfunded liabilities that results from use of a “riskless rate” does not mean states and localities need to contribute that amount to their pension funds, since the pension funds may well earn higher rates of return over time than the Treasury bond rate. In other words, states may be able to achieve pension fund balances adequate to meet future obligations without adding the full $3 trillion to the funds.

While it may make sense to reconsider whether the typical 8 percent discount rate is the right one going forward, simply basing annual state contribution amounts to pension funds on the return to riskless investments appears to go farther than is necessary for a number of reasons:

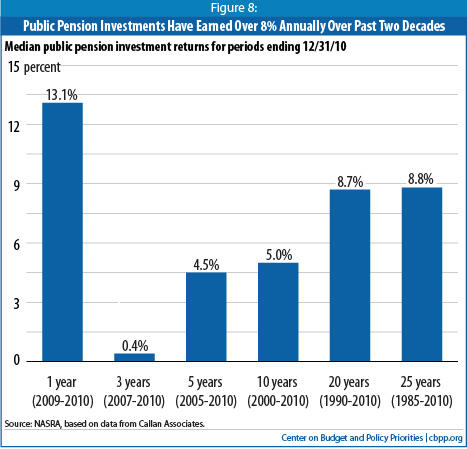

- Pension funds invest for the long term, so a few years of below-average returns can be averaged out with years of higher returns. As noted, the 8 percent discount rate that most states assume reflects the experience of the trust funds over the last 20 years (including the 2008 stock market decline); median returns for the last 25 years were even higher, at 9.3 percent. While the rates of return on investments were much lower in the recent recession, it is generally assumed that they will rise in the future even if they do not return to the very high rates of the late 1980s.

- A business may be sold or go out of business at any time, so it is important to keep its pension plan 100 percent funded at all times for benefits earned to date.[7] Governments, in contrast, will be in continuing existence, so a small amount of underfunding in some years does not put their pensioners or taxpayers at significant risk.

- The stated concern of some that basing required contributions on actual rates of return will lead pension managers to put funds in risky investments appears overblown. Pension funds have a long history of generally having invested prudently, except in rare situations. Most states have effective barriers to overly risky investing in place (although these could be strengthened), including oversight boards, reporting requirements, and regular actuarial reviews.

- If, as a result of use of a very low discount rate in determining state contribution amounts, a state puts money into its pension fund that exceeds what the fund turn out to need, the state will have made less effective use of the resources than if the excess contributions had been used to support important public services, resupply reserve (or “rainy day”) funds, invest in infrastructure, or return funds to taxpayers in the form of tax reductions.

- Finally, if a pension fund assumes a 4 or 5 percent discount rate when determining annual contribution levels but actually gets higher returns on its investments, funds will build up in the trust fund. When pension trusts have been overfunded in the past, this has sometimes led to problems such as employee demands for increases in pension benefits that later proved unsustainable. Overfunding also has led some jurisdictions to skip payments that they subsequently found difficult to resume, because they used the amounts freed up by skipping the pension contribution to fund programs or cut taxes in ways that they cannot easily undo. The 2008 GAO report noted that experts have said: “… it can be politically unwise for a plan to be overfunded; that is, to have a funded ratio over 100 percent. The contributions made to funds with ‘excess’ assets can become a target for lawmakers with other priorities or for those wishing to increase retiree benefits.” [8]

At Present, Pension Contributions Are a Small Part of State and Local Budgets

| TABLE 1: State and Local Pension Contributions as Share of Spending | |

| State | Percent of Spending |

| United States | 3.8% |

| Alabama | 3.8% |

| Alaska | 3.1% |

| Arizona | 3.5% |

| Arkansas | 3.8% |

| California | 5.2% |

| Colorado | 3.0% |

| Connecticut | 4.9% |

| Delaware | 1.9% |

| DC | 1.8% |

| Florida | 3.2% |

| Georgia | 2.8% |

| Hawaii | 4.4% |

| Idaho | 3.2% |

| Illinois | 4.5% |

| Indiana | 3.5% |

| Iowa | 2.2% |

| Kansas | 2.5% |

| Kentucky | 3.2% |

| Louisiana | 4.2% |

| Maine | 3.2% |

| Maryland | 3.4% |

| Massachusetts | 4.2% |

| Michigan | 3.1% |

| Minnesota | 2.1% |

| Mississippi | 3.5% |

| Missouri | 4.2% |

| Montana | 2.9% |

| Nebraska | 2.1% |

| Nevada | 7.6% |

| New Hampshire | 2.4% |

| New Jersey | 3.5% |

| New Mexico | 3.8% |

| New York | 5.3% |

| North Carolina | 1.2% |

| North Dakota | 1.8% |

| Ohio | 3.8% |

| Oklahoma | 4.7% |

| Oregon | 3.5% |

| Pennsylvania | 2.1% |

| Rhode Island | 5.7% |

| South Carolina | 3.0% |

| South Dakota | 2.3% |

| Tennessee | 3.0% |

| Texas | 2.7% |

| Utah | 3.7% |

| Vermont | 1.2% |

| Virginia | 4.8% |

| Washington | 2.2% |

| West Virginia | 4.7% |

| Wisconsin | 3.6% |

| Wyoming | 1.8% |

| Source: CBPP calculations of U.S. Bureau of the Census Government Finances, Finances of State and Local Retirement Systems Note: WI adjusted to include state payment of fee contribution; CT adjusted to remove deposit of $2 billion proceeds from pension bond. | |

The regular deposits to pension trust funds are paid by employers (from their annual budgets) and by employees (as a reduction in their take-home pay). As part of the annual budget process, the state estimates the amount needed to cover the pension costs accrued for employees. [9] This amount, known as the “normal cost,” is based on factors such as current employees’ expected years of service, future salary increases, and longevity once retired. As noted above, the state needs to deposit an amount that will grow over time to the amount required to make pension payments when they come due.

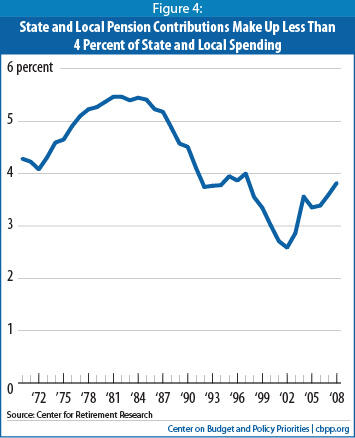

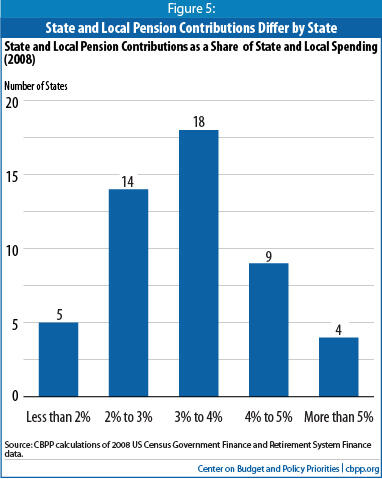

Since states must balance their budgets each year, and since state budgets also must pay for the salaries of current state workers in areas like education, health care, and human services and the costs for private sector providers of health care for their poor, elderly, and disabled residents and other services, as well as other costs, it is important that pension contributions remain reasonable and stable. Fortunately, pension contributions — the combination of normal costs and “catch-up payments” (which are described below) — represent a modest share of state budgets, typically between 2 percent and 5 percent of state and local spending, averaging 3.8 percent. (See Figure 5 and Table 1.)

One reason contributions vary among states is that a significant portion of state and local workers are not covered by Social Security. These jurisdictions generally provided more generous retirement benefits. The higher contributions these benefits require from the employer and employees are partially offset by the fact that no payroll deductions are made for Social Security. (See box.)

If the forecasts of costs and interest rates were always totally accurate, the state made the full deposit each year, and it enacted no benefit improvements that are retroactive to prior years for which the contributions have already been made, the state would have no pension costs each year beyond the “normal cost.” But given the long time horizon involved, some of the forecasts inevitably will prove wrong. A severe stock market decline can reduce the return on the assets deposited, salaries can grow faster than expected, or the state can fail to make the full deposit each year because of budget constraints.[10] As a result, states generally face a second annual pension cost: catch-up payments to help make up for future costs that previous deposits do not fully cover.

How best to finance those catch-up payments, and how to build assets and reduce liabilities so that future “normal costs” and catch-up payments are kept to a reasonable level, are addressed in the next section.

II. A Strategy for Fixing State Pension Problems in Tough Economic Times

States face a daunting fiscal challenge: the worst recession since the 1930s has caused the steepest decline in state tax receipts on record. State tax collections are 11 percent below pre-recession levels,[11] adjusted for inflation, while the need for state-funded services has not declined. As a result, even after instituting very deep spending cuts over the last several years, states continue to face large budget gaps. To date, 44 states and the District of Columbia are projecting budget shortfalls for fiscal year 2012, which begins July 1, 2011 in most states. These come on top of the large shortfalls that states closed in fiscal years 2009 through 2011. States will continue to struggle to find the revenue needed to support critical public services for a number of years.

This is the difficult context in which states must begin to address their pension funding problems. States must proceed cautiously, but unlike the shortfalls in their operating funds — which must be closed each year — states have a longer period in which to address their unfunded liabilities.

States’ options are somewhat constrained. Key provisions of current pension promises are legally guaranteed in most states. In addition, changes to public employees’ compensation will affect the ability of states and localities to attract and retain workers. States that slash benefits deeply for new workers (and current workers in states where that is allowed) run the risk of dissuading a substantial number of the best young workers from entering careers in education, health care, public safety, and other areas that are important for a state’s long-term economic future.

Many State and Local Workers Are Not Covered by Social Security

When considering changes to state and local pension plans, it is important to take into account the fact that many state and local workers are not covered by Social Security. Nationally, virtually all private sector workers are covered by Social Security. In contrast, some 27 percent of state and local workers are not covered.a This includes approximately 40 percent of all teachers and a majority of public safety workers. For these workers, a public pension is a critical part of their retirement security.

In states and localities that are not part of the Social Security system, pension benefits tend to be higher and contributions are larger.

In addition to police and firefighters in many states, some of the larger groups of public employees not covered by Social Security are state and local workers in Ohio, Massachusetts, Nevada, Louisiana, and Colorado and teachers in California, Georgia, Illinois, Kentucky, Missouri, and Texas.

a Social Security Administration: Management Oversight Needed to Ensure Accurate Treatment of State and Local Government Employees, GAO-10-938, September 2010.

Nevertheless, states can address public pension issues effectively within the current legal, fiscal, and economic framework without throwing their budgets out of whack or harming their economies. They should:

- Act now to craft a plan to restore pension trust funds to solvency gradually.Image

- Move deliberately to make changes, to the degree needed, in their methods for determining future costs and needed contributions. In particular, the assumptions concerning the discount rate for computing liabilities — and the amount of annual contributions needed to the funds — merit close examination. However, rather than moving abruptly to new ways of estimating annual contribution amounts, states should make adjustments over time as needed.

- Immediately change pension rules to address abuses such as “double-dipping” and “spiking.”

- Gradually address underfunded pensions with a balanced combination of adequate contributions to pension funds by governments and employees (in states where employees are not already contributing adequately) and reductions in benefits as appropriate to offset the costs of restoring trust funds.

- Avoid abandoning defined-benefit plans altogether, which would actually make it harder for states to restore fund balance.

- Adapt any reform strategy to an individual state’s circumstances, with radical changes reserved for states whose pension plans are the most severely underfunded.

Many states are already adopting elements of this strategy, illustrating that problems in state pension funds — far from the massive challenge that they are sometimes depicted to be — can be addressed without imperiling workers’ retirement security, a state’s ability to attract and retain a good workforce, or its ability to finance public services. The rest of this report examines each of the above elements in turn.

A. Rebuild Trust Funds Over Time — Not All at Once

The misconception that state pension funding is in crisis often stems from confusion between states’ long-term funding needs and their immediate costs. As noted above, many state pension funds do not contain enough assets to pay 100 percent of promised benefits. [12] It would constitute a very large drain on their budgets if state and local governments had to fill their entire shortfalls immediately. But the Governmental Accounting Standards Board — the arbiter of the accounting rules that state and local pension plans follow — quite reasonably allows states to pay off these shortfalls over up to 30 years, since the underlying liabilities are long term in nature.

Such an increase would be significant but not enough to require drastic solutions (such as the elimination of defined-benefit pensions). Because of the long time horizon, state and local governments can safely take two or three years to ramp up to the higher contributions (to allow more time for state economies, and revenues, to recover) that will be needed to put them on a path to paying off unfunded liabilities. The recovery in state revenues that appears to be starting will make this more affordable. The key is to make and stick to a clear plan that leads to full contributions each year, rather than haphazardly skipping payments or making less than the full payment — as the more substantially underfunded states have done.

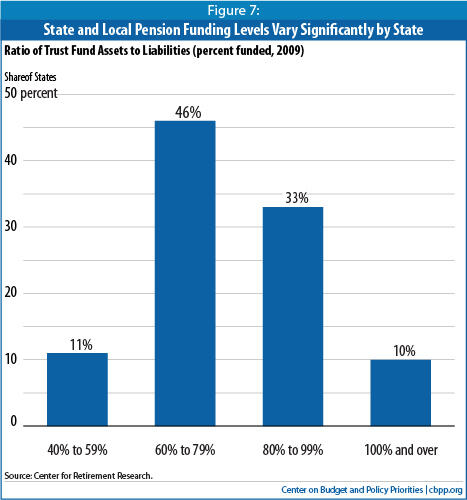

According to the most recent data available (Figure 7), some 43 percent of major public pension funds were funded at 80 percent or above in 2009, using the plan’s calculations and assumptions for determining liabilities. One option is to use an 80 percent threshold for a few years until the economy recovers and state tax revenues return to pre-recession levels as a share of the economy. Aiming for a target of 80 percent funding reduces the amount that needs to be contributed each year. Over the longer term, however, a goal of 100 percent is required in order to ensure that an adequate level of funding is maintained.

B. Re-Examine Assumptions Concerning Liabilities and Contribution Rates

As noted, states and localities determine the amount they must set aside each year to fund future pension costs by summing two elements: the “normal cost” (the amount needed this year to cover the future cost of retirement benefits for current employees) and an amount to pay down any accrued unfunded liabilities.[14]

The discount rate used to determine the present value of pension benefits that have been promised can have a dramatic effect on the size of the set-aside needed each year. The appropriate rate to use has been the subject of much debate.

Some favor continuing to use the actuarial method that has been recommended by the Governmental Accounting Standards Board (GASB), which is to use the historical average return on funds’ assets — about 8 percent. (Note: GASB is reconsidering this recommendation; see footnote 5.) State pension trust funds invest their assets in a diverse mix of stocks, bonds, and other instruments until they are needed to pay for benefits. Others (especially economists) argue that because pension obligations are guaranteed (rather than being subject to risk), the discount rate should also be based a riskless rate, such as that on Treasury bonds — around 4 percent.

Even if state and local pension liabilities are valued at the riskless rate — producing an unfunded liability generally estimated at $3 trillion — that would not mean that states and localities must necessarily pay an extra $3 trillion to their pension funds. Rather, to fund future pension costs and to pay down unfunded liabilities, states and localities need to set aside an amount that will be sufficient, after years of investment growth, to pay pension costs in the future. A key point, as noted above, is that how states and localities should value their pension liabilities and how much they should contribute to their pension funds each year to meet their pension obligations are two distinct issues, although they obviously are related. Ultimately the amount states and localities must contribute will be determined by the actual return on those investments (rather than by the rate of return assumed in selecting a discount rate to use in estimating liabilities).

While some states and localities are reconsidering whether an 8 percent discount rate is appropriate for estimating liabilities, simply switching to a riskless rate for purposes of calculating pension contributions goes farther than necessary, as discussed above. [16]

Other factors besides the discount rate affect the amount of annual contributions needed, and states should carefully consider changes to other methods used to determine funding needs. For example, most public pension funds use “asset smoothing” to phase in the effect of big stock market changes. The typical period used is five years. If the market rises (or falls) significantly relative to the state’s assumption in one year, a state that uses a five-year smoothing path will recognize one-fifth of the difference in valuing its assets in the first year, two-fifths of the difference in the subsequent year, and so on. States that do not use asset-smoothing or use a relatively short period could reduce volatility by extending the number of years over which differences are recognized.

The number of years over which liabilities are paid off, or “amortized,” also affects the size of the annual payments needed. Current accounting rules recommend an amortization period of no more than 30 years; this is the most common period states use, but there is considerable variation. In the past, some states adopted a shorter period (such as 15 years) in order to pay down their unfunded liabilities more quickly; a state that is using an unusually short period may want to extend it now in order to reduce the annual payments required during the current difficult fiscal times.

One way states can reduce the potential for large pension cost increases is to recognize the full extent of new liabilities incurred when they enhance pension benefits (such as when a state raises the percentage by which an employee’s years of service are multiplied to calculate the benefit amount). If a change applies only to new hires or only to pensions accrued after the date of the change, it can be paid for by future contributions. [17] Often, however, these changes create a new liability that past contributions for the normal costs of current employees did not take into account. Because any enhancement of pension benefits is in the control of the employer — in contrast to an unfunded liability that results from an unanticipated decline in the stock market — states and localities should be required to fully fund any retroactive cost they incur at the time they enact the enhancement. This allows for more accurate budget trade-offs.

C. Adopt Reforms That Will Reduce the Potential for Abuse

A number of states have made or are considering changes to help ensure that no retirees receive overly large pensions. Two of the best-known problems are “double-dipping” and “pension spiking.”

Double-dipping occurs when an employee retires from a job and begins to draw a pension but at the same time returns to work for the same employer, receiving pay and building up an additional pension. Some state and local governments are ending this practice by disallowing the payment of a pension at the same time an employee is drawing a salary from the same government entity. For example, Maryland enacted restrictions last year that limit earnings for all retirees who return to work except those with lower incomes; Georgia suspends pension payments for retirees who return to work; and in Michigan, retirees who return to work lose their current pension payments if their salary is more than one-third of their previous salary.

Pension spiking occurs when an individual greatly increases the amount of pension he or she can receive by artificially increasing his or her final year of pay (a prominent part of the pension benefit calculation in many jurisdictions). This can be accomplished by receiving a short-term promotion at the end of a career, by working an unusually large number of overtime hours, and in other ways. Public employers such as Arizona, Colorado, Michigan, and Virginia have partially addressed this problem by increasing the number of years used as the average in determining the amount of the pension (see below). Other states are responding by disallowing the use of accrued sick leave or vacation in determining the pension amount, limiting the amount of overtime that can be counted, and capping the level of salary used to determine the pension amount. For example, for New York State workers hired after 1976, any salary that is more than 10 percent above the average of the prior two years’ salary is excluded.

Despite the media attention they receive, double-dipping and pension spiking are not widespread, so reforming them will not result in great cost savings for most states and localities. Such reforms are, however, an important part of any pension restructuring plan. Not only do they make the system fairer to other public employees, but these kinds of abuses lead to the mistaken impression that the majority of public pensions are bloated and undeserved.

D. Address Underfunding Through Larger Contributions and Benefit Reductions

Changes in state and local pension plans’ policies are needed to address the toll taken by the last two recessions and to prepare for the impact of demographic changes in the future. States and localities can address their pension problems with a multi-pronged strategy that includes a balanced combination of adequate contributions to pension funds by both governments and employees and a restructuring of benefits to reduce costs as appropriate.

| TABLE 2: Summary of Major State Pension Actions in 2010 | |||||||||

| State Plan | Major Change (any type) | Contributions | Normal Retirement Age Increased | Anti Abuse Measures - Anti-Spiking or Re-employment Restrictions | Benefit Formula | Vesting period | COLA | ||

| Employee | Employer | Years in Final Average Salary | Benefit Multiplier | ||||||

| Arizona | Y | Y | up | ||||||

| California - state | Y | up | up | Y | up | down | |||

| Colorado | Y | up | down | Y | Y | down | |||

| Georgia | Y | Y | |||||||

| Hawaii | Y | Y | |||||||

| Illinois – non teachers | Y | Y | up | down | |||||

| Illinois - teachers | Y | down | Y | up | down | ||||

| Iowa - public employees | Y | up | up | Y | Y | up | |||

| Louisiana - state ees and teachers | Y | Y | up for teachers | no change for most | |||||

| Louisiana - other school ees | Y | up | Y | ||||||

| Michigan | Y | down | |||||||

| Michigan - school | Y | Y | up | down | |||||

| Minnesota - state | Y | up | down | ||||||

| Minnesota - local | Y | up | up | up | down | ||||

| Minnesota – teachers | Y | up | up | ||||||

| Mississippi | Y | up | Y | ||||||

| Missouri | Y | up | Y | up | |||||

| New Jersey - state, local, teachers | Y | up | up | down | |||||

| New Mexico | Y | down | Y | ||||||

| Pennsylvania – state | Y | up | Y | down/ or same with higher ee contribution | up | ||||

| Pennsylvania – teachers | Y | up | Y | down/ or same with higher ee contribution | up | ||||

| Rhode Island | Y | down | |||||||

| South Dakota | Y | Y | down | ||||||

| Utah | Y | Y | down | ||||||

| Vermont - municipal | Y | up | |||||||

| Vermont – teachers | Y | up | Y | cap on salary | up aft 20yrs | ||||

| Virginia | Y | up | down | Y | up | down | |||

| Wyoming | Y | up | up | ||||||

| Totals | 21 | 11 | up - 5 down - 4 | 12 | 7 | 8 | 3 | 3 | 8 |

| Source: National Conference of State Legislatures Plan Enactment Summary, state reports. “Ee” = employee. | |||||||||

Even before the recession began in 2007, many states recognized the need to address future pension funding issues. Between 2005 and 2010, 30 states made one or more major changes such as increasing employee contributions or paring back benefits, according to a survey by the National Conference of State Legislatures. The pace of these changes accelerated over that period and remains high; 21 states acted in 2010, and NCSL has identified 31 states considering proposals so far this year, including increasing and stabilizing revenues going into pension trust funds, reducing benefits, and more fundamental changes to the way that state and local pensions are run.

Increasing Employer Contributions

Academic studies[18]as well as states’ experience suggest that the best way to maintain the fiscal health of a pension fund is to make regular contributions at the full required level. There is always a temptation — especially during economic downturns — to make inadequate contributions because of the short-term benefit to a state’s annual budget, as some states have done in recent years. To change this practice, politicians and the public must recognize that the short-term benefit of skipping or postponing payments may be outweighed by the longer-term problems this creates for pension funding — problems that will increase future costs.

Many states and localities recognize these trade-offs and have been increasing their pension contributions. Between 2008 and 2009 (the most recent period for which Census data are available), employer contributions increased in three-fourths of major state and local pension plans; in about half of these plans, the increase was more than 5 percent.

Some pension underfunding has occurred when states reduced their contributions in good economic times because their plans appeared fully funded or investment returns were exceeding their assumptions. Total state and local pension payments as a share of budgets steadily declined starting in 1997 and reached a low of 2.6 percent in 2002.[19] Some plans reduced their pension contributions after the stock market boom of the late 1990s boosted the value of trust fund assets. For example, employer contributions to California’s main public employee retirement funds were just $321 million in fiscal year 2001, compared to $4 to $5 billion a year in the 1990s. While these reductions may have seemed justified at the time, this failure to build up assets further in good times has contributed significantly to the current underfunding problems.

Unfortunately, states have incentives in both good times and bad to make low payments to pension trust funds: when investments are growing, the trust fund does not appear to need as much employer funding, and when a slow economy has depressed state revenues, other demands compete for scarce resources. One way to address this problem would be to set a statutory floor on annual employer contributions, say, 7.5 percent of payroll or some multiple of the normal costs.

Some states are constrained by legal restrictions on the size of their pension payments. For example, a 2006 study found that most of the 55 plans that did not make their annual required contributions to cover normal costs and unfunded liabilities that year had a legally imposed cap on the contribution allowed. [20] States can improve their future funding by removing or restructuring these caps. At the least, states without such caps should be careful to avoid creating new problems by imposing them as part of efforts to address the pension funding problem. Caps are particularly problematic if they are set so low that the state cannot cover its normal costs or ever achieve full funding.

Increasing Employee Contributions

Employees in almost all states contribute a share of their own pay toward future pension benefits. In 2008, employee contributions totaled $37 billion. A survey of 87 large state plans found that only six of them (7 percent) required no employee contribution. [21]

Unlike employer contributions, employee contributions generally do not vary with the economy and remain a steady share of payroll, averaging about 4 percent of payroll in the 1980s and increasing gradually to 4.6 percent on average in 2008.[22] Thus, employee contributions have remained at a much more consistent level as a share of state and local budgets, lending stability to the system.

One way to strengthen the fiscal health of pension plans is to examine the level of employee payments and to increase them if needed. A number of states have increased employee contributions in recent years; 11 states, including California, Louisiana, Mississippi, and Vermont, took this step in 2010.

Increases to employee contributions should be considered in the context of the total compensation of a government’s employees. State and local employees generally receive lower wages than their private-sector counterparts and employee benefits such as pensions make up only part of the difference.[23] If employees pick up a larger share of the cost of these pensions, the benefit becomes less valuable and current wages may need to increase so that the public sector can continue to attract high-quality employees.

Restructuring Benefits to Reduce Costs

Many states are scrutinizing the formulas that determine pension benefit payments for both new hires and existing employees. Changes to provisions for existing employees are much more difficult for legal, political, and practical reasons, but some states are considering them. And most states are considering changes for new hires.

Rather than simply reducing benefits in order to reduce costs, states and localities should apply some commonsense principles drawn from analysis of public and private retirement systems, including:[24]

- Pension systems should provide adequate income in retirement but not encourage healthy and productive workers to exit the workforce too soon. Unnecessarily early retirements are costly in terms of both state and local budgets and lost contributions to the economy.

- Retirees’ pension payments should not be overly dependent on the level of their salaries in at the very end of their career.

- Public pensions should be sufficient to provide retirement security as one part of a multi-faceted system that includes savings as well as Social Security (in the states and localities where employees are a part of the Social Security system).

- The pension system should balance some employees’ desire for portable pension benefits with the need for an experienced and stable workforce.

Two areas of special importance concern the retirement age and the formula used to compute pension payments, as explained below.

Retirement Age

Generally, the rules that determine when an employee can retire and receive a full pension factor in the employee’s age and number of years worked. For example, an employee might receive a full pension at age 60 if he or she has worked at least ten years for the state, or at age 55 after working for at least 30 years. If an employee retires early — that is, at a younger age or with fewer years of service — most states and localities provide a reduced benefit.

Many states and localities are following the lead of the Social Security system and raising the age when an employee qualifies for a full pension to reflect the fact that people are staying healthier longer and living longer than in the past. For example, last year alone, 12 states upped their retirement ages, including Illinois (to 67), Pennsylvania and Vermont (to 65), and Virginia (to match Social Security’s full retirement age). In almost all states and localities, police, firefighters, and employees in other physically demanding jobs are allowed to retire with full pensions at a younger age than other employees.

States and localities are also examining the calculation used to reduce benefits for early retirees. The goal should be to provide them with benefits that are no more than “actuarially equivalent” to those for workers who wait until the retirement age — i.e., benefits for both sets of workers should be roughly the same over the workers’ lifetimes. Where this is not already the case, such a change would both reduce costs and remove an incentive for early retirement. Last year, Minnesota and Louisiana made changes in this area. In addition, a number of states raised the age at which employees become eligible for early retirement.

Computing Pension Payments

The general formula used to determine the payments to retired employees is: Retirement Annuity = (Years Worked x Formula Multiplier) x Average Salary.

For example, employees who retire after working 30 years in a state with a formula multiplier of 2.0 would receive an annual pension equal to 60 percent [30 x 2.0] of their average salary over a set number of years. A formula of this type determines the amount of the full pension, for which only employees who reach a minimum age and/or years of service would qualify. In addition, workers must have a minimum number of years of service (generally between five and ten) to be eligible for any pension at all; this is called the vesting period.

One element of this calculation that has received a considerable amount of attention is the number of years used in determining the average salary of an employee eligible for retirement. Different states and localities use different numbers, ranging from just one year (i.e., the last year of work) to five years; three years is the most common.

Increasing the number of years used in this average can result in a pension that better represents an employee’s full career, such as by muting the effect of a promotion received at the end of a career (thereby helping prevent pension spiking). Increasing the number of years generally would also reduce the size of the pension — and thus the employer’s costs — because salaries typically go up annually. Alternatively, states could go further and base pension payments on employees’ inflation-adjusted earnings over their full career.[25]

The other important element of the benefit calculation is the formula multiplier. In states where employees are covered by Social Security, the average multiplier was 1.94 in 2008; multipliers are generally higher in states where employees are not covered by Social Security. (See the box on page 11 for information on states and local employees who are not covered by Social Security.) A multiplier of 2.0 results in a pension that replaces 60 percent of the final average salary of an employee who has worked 30 years. Whether this is a sufficient replacement ratio depends on many considerations, including access to Social Security and ability to save for retirement. A number of states, including California and New Jersey, have lowered the multiplier. The main motivation for these reductions appears to be to lower costs, although some states are acting to bring their plan closer to the national average or better meet a chosen replacement ratio. Pennsylvania now gives new employees a choice of making higher contributions to retain the current multiplier or accepting a lower multiplier with no increase in contributions.

Once an employee has retired, most state pension plans increase the amount of the pension each year to account for increases in the cost of living. This type of provision, often referred to as a cost-of-living adjustment (COLA), serves an important purpose. Without any such increase, the value of a pension slowly erodes over time, making it increasingly difficult for retirees to make ends meet.

Nonetheless, some states are eliminating or capping their COLAs in order to cut costs. Colorado, Minnesota, and South Dakota recently reduced COLAs for current members of the retirement system — a change that is being challenged in the courts. Such changes are problematic not only from a legal standpoint but also because they reduce retirees’ income after they have made their retirement plans on the assumption that their pension would keep pace with inflation. Other states, including Illinois, Michigan, Rhode Island, and Virginia, have taken the less drastic step of reducing the COLAs that will affect new hires once they retire. In some cases these changes are being made to bring COLAs more in line with expected inflation by eliminating “floors” (minimum annual percentage increases); in others, it is purely a cost-saving measure. Any state considering changing its COLA should weigh the cost savings against the impact on the retirement security of current and future retirees.

Another way to reduce costs is to increase the vesting period, which currently averages five years. The trend since the mid 1980s had been towards shorter vesting periods, but this has reversed in the last couple of years. States such as Minnesota, Missouri, and Pennsylvania have recently increased vesting requirements.

E. Avoid Abandoning Defined-Benefit Plans

Some states are considering more fundamental pension changes, such as converting to plans that combine elements of defined-benefit and defined-contribution plans. (A defined-benefit plan provides employees with specified pension payments, generally based on the employee’s age at retirement, number of years worked, and pre-retirement earnings. A defined-contribution plan, such as a 401(k), does not guarantee payments of a specified level; rather, employer contributions are set aside in an account for each individual employee and benefits are based on the amount of funds in that employee’s account at the time of retirement.) These discussions often start with a proposal to convert a defined-benefit plan into a defined-contribution plan for future hires only. But there are a number of reasons why these conversions do not make sense from either a fiscal or retirement security perspective.

First, closing a defined-benefit plan to new hires has no effect on a state’s current unfunded liability, so it does not address the major funding problem most public pension systems currently face. On the contrary, it can raise annual costs by making it harder for a state to pay down those existing liabilities, because the plan will include fewer employees and fewer contributions going forward. [26]

In addition, a defined-contribution plan is a more expensive way to provide a given level of retirement income to employees because it lacks the benefits of improved investment returns that result from a pension trust fund’s pooled investments, professional money managers, and shared administrative costs.[27]

One advantage of defined-contribution plans often cited by proponents is that they reduce risk for the employer, who faces no future liability once the contributions are made. This reduction in risk, however, is a major disadvantage from the point of view of individual employees, who now face the risks of inadequate retirement income or outliving their retirement savings.

Another argument for defined-contribution plans is that younger employees are less likely to remain in one job for many years and are attracted by the portability of individual retirement accounts. This desire for flexibility, however, may not be enough to offset the shift in risk from the employer to the employee, as well as other problems with defined-contribution plans. In addition, the experience of states that offer employers a choice between defined-benefit and defined-contribution plans shows that, when given a choice, most public employees prefer defined-benefit plans. [28]

Some states have tried to get the best of both the defined-contribution and defined-benefit approaches by creating a hybrid that provides a reduced defined-benefit plan in addition to a defined-contribution plan. Michigan (in its teachers’ plan) and Utah recently adopted this approach, and other states are considering it. (Utah gives employees the option to go completely to a defined-contribution plan.) This reduces the risk for employees somewhat. Another way to mitigate some of the risk of defined-contribution plans is to include provisions like automatic enrollment, matching employer contributions, and access to investment managers. None of these provisions, however, give employees participating in a defined-contribution plan the same level of retirement security as those in a defined-benefit plan.

State and local governments considering defined-contribution or hybrid plans solely for the purpose of saving money would be well advised to look carefully at the experience of other states. For example, Utah’s employer contribution under its new plan (10 percent of payroll) is higher than the contributions that a number of states typically make to their defined-benefit plans. In addition, Nevada decided against putting new hires in a defined-contribution plan when projections showed that the state’s total pension costs would increase, since the state would have to increase its contributions to offset the loss of these new employees to the state’s defined-benefit plan.[29] Similarly, Kentucky found that conversion to a defined-contribution plan would increase the state’s costs for close to 20 years. [30]

F. Adopt a Reform Strategy That Matches the State’s Particular Circumstances

Many media reports on state pension issues lose sight of the fact that pension funding problems are localized, not universal, and result from some individual governments not following basic funding rules. On average across all states, funding is very close to the recommended level, which is 80 percent of discounted future liabilities (as those liabilities are now estimated by the plans, generally using about an 8 percent discount rate). Funding exceeds 80 percent in 43 percent of state plans and is below 60 percent in 11 percent of plans. In most states, a package of sensible changes like those outlined above should be sufficient to restore the health of the pension system.

The states making news for having inadequately funded plans — Illinois and New Jersey, for example — either failed to make regular contributions to their future pension costs even in good economic times or increased benefits retroactively without funding those increases. In these states, more drastic measures will likely be needed, such as significantly increased contributions in the near future or significant reductions in pension benefits.

Conclusion

Pension costs didn’t cause the current state fiscal crisis. And even eliminating defined-benefit pensions — with all the problems that would entail — wouldn’t have much impact on current state budget shortfalls. Rather, pension funding is one of several key structural budget problems that states must address. Most states have generally been responsible in funding pensions, and a large number are already starting to address pension fund shortfalls.

State and local governments need to provide adequate pay and benefits to attract and retain high-quality teachers, nurses, police, and other employees. Currently, the pay of public-sector employees is somewhat below that of their private-sector counterparts: “apples-to-apples” studies find that public workers are paid 4 to 11 percent less than private-sector workers with similar education, job tenure, and other characteristics. [31]

In some cases public employees have foregone wage increases and received benefit enhancements instead. But while benefits are more generous and secure for public employees than for most private-sector workers, factoring in the value of these benefits does not entirely eliminate the gap between the compensation of state and local employees and their private counterparts in comparable jobs. [32]

State and local governments thus should use all the tools at their disposal to solve their pension problems without severely reducing public pensions, which would be an overreaction to current funding issues and hinder states’ and localities’ efforts to attract and keep the workers that teach our children and protect our lives and homes.

End Notes

[1] Current contribution data are for 2008, the most recent year available from Census.

[2] As explained below, the typical alternative to a defined-benefit plan is a “defined-contribution plan” such as a 401(k), which does not guarantee payments of a specified level. Rather, employer contributions are set aside in an account for each individual employee; these funds are invested and benefits are based on the amount of funds in that employee’s account at the time of retirement.

[3] These figures are the market value of the equities, bonds, cash, and other assets held by the pension fund at a given point in time. They differ from the actuarial value of the trust fund’s assets. Most public pension funds use “asset smoothing” to phase in the effect of big stock market changes, as described later in this report.

[4] Alicia Munnell, Jean-Pierre Aubry, and Laura Quinby, Public Pension Funding Standards in Practice. Center for Retirement Research at Boston College, paper prepared for NBER State and Local Pension Conference, August 19 and 20, 2010, p. 14.

[5] The GASB draft of its revised standards for state and local pension funds, due to be issued in final form in 2012, concludes that use of a riskless rate is not “… consistent with the view … that the present value of projected benefit payments should reflect an expectation of the employer’s projected sacrifice of resources, reduced by the expected rate of return on investments.” The overall discount rate that the GASB draft recommends using to report on a pension fund’s liability would be based on a blend of the expected rate of return on a fund’s existing and expected assets and the rate of return on high-quality municipal bonds, which would be applied to the portion of liabilities for which future assets cannot be identified. The precise blend would depend on various factors related to the funding status of the pension fund.

[6] A Congressional Budget Office issue brief released in May 2011, The Underfunding of State and Local Pension Plans, makes this point, saying, “Decisions about how to address the underfunding can be informed by the choice between those two measurement approaches [the GASB method and a fair-value approach using a much lower discount rate], but there is no necessary connection between the information provided by the two approaches and decisions about how much a plan’s sponsor should contribute each year.”

[7] See discussion in National Conference on Public Employee Retirement Systems, The Advantages of Using Conventional Actuarial Approaches for Valuing Public Pension Plans, November 2008, http://www.ncpers.org/News/PageText/documents/ResearchSeriesIII.pdf .

[8] GAO-08-223.

[9] Most states and localities allocate a portion of an employee’s career pension costs to a given year using a method called Entry Age Normal (EAN). This evens out the contributions needed over the career of the employee. The normal cost for any employee for any given year is equal to the amount that would need to be deposited — in today’s dollars — to meet the full expected pension for that employee, divided by the number of years the employee is expected to work. This differs from the “classic” definition of normal costs or service cost for each year, which equals the present value of the cost of future pension payment earned that year without any averaging over the career of the employee. Using this classic method, pension costs would be lower at the beginning of an employee’s career and rise as the employee got closer to retirement.

[10] In the late 1990s when the stock market was booming, asset growth that exceeded projections resulted in overfunding in a number of states. Some states responded to these surpluses by reducing contributions or increasing benefits retroactively. When the economy subsequently declined and asset values dropped simultaneously, states found it hard to restore contributions.

[11] As of the third quarter of 2010. CBPP analysis of Rockefeller Institute, Census Bureau, and Bureau of Labor Statistics data.

[12] Alicia Munnell, Jean-Pierre Aubry, and Laura Quinby, The Funding of State & Local Pensions: 2009-2013, Center for Retirement Research at Boston College, April 2010.

[13] U.S. Government Accountability Office, “State and Local Government Retiree Benefits: Current Funded Status of Pension and Health Benefits,” GAO-08-223. The GAO report noted on p. 15, “Many experts and officials to whom we spoke consider a funded ratio of 80 percent to be sufficient for public plans….”

[14] In addition, a small amount is used to cover the cost of administering the pension system.

[15] For example, when discussing the implications of using a riskless rate in a June 2010 paper, Valuing Liabilities in State and Local Plans, Alicia Munnell states, “And a totally invalid implication is that the selection of the discount rate has any implications for the appropriate investments for public plans.”

[16] Additional discussion of the discount rate issue can be found on pages 6 through 9.

[17] For example, an employee’s pension could be calculated in two pieces, with one formula that applies to years worked before the increase and one that applies to years after the change.

[18] See, for example, Alicia Munnell, Kelly Haverstick, Jean-Pierre Aubry, and Alex Golub-Sass, Why Don’t Some States and Localities Pay Their Required Pension Contributions?, Center for Retirement Research at Boston College, May 2008, http://crr.bc.edu/images/stories/Briefs/slp_7.pdf; J. Fred Giertz and Leslie Papke, Public Pension Plans: Myths and Realities for State Budgets, National Tax Journal, June 2007.

[19] As a share of payroll, the pattern is the same. On average, employer contributions dropped from 9.6 percent of payroll in 1997 to 6.5 percent in 2002.

[20] Munnell, Haverstick, Aubry, and Golub-Sass.

[21] Daniel Schmidt, 2008 Comparative Study of Major Public Employee Retirement Systems, Wisconsin Legislative Council, revised May 2010.

[22] Comparative Study of Major Public Employee Retirement Systems, Wisconsin Legislative Council, various years.

[23] As noted later in this report, studies find that state and local workers are paid 4 percent to 11 percent less than private-sector workers with similar education, job tenure, and other characteristics. The wage deficit is highest for higher-wage public workers..

[24] For example, see the following: Peter Diamond, Alicia Munnell, Gregory Leiserson, and Jean-Pierre Aubry,Problems with State-Local Final Pay Plans and Options for Reform, Center for Retirement Research at Boston College, August 2010,http://crr.bc.edu/images/stories/Briefs/slp_12.pdf; Richard Woodbury, State Population Aging and State Pensions in New England, New England Public Policy Center, Federal Reserve Bank of Boston, Report 10-1, June 2010; Beth Almeida and William Fornia, A Better Bang for the Buck, The Economic Efficiencies of Defined Benefit Pension Plans, National Institute on Retirement Security, August 2008.

[25] See Diamond and Munnell. As explained in this paper, in order to maintain retirement security, implementing this type of option would require some trade-offs such as an increase in benefit formula multipliers.

[26] This would become particularly problematic if GASB adopts proposed rules that would significantly reduce allowed amortization periods.

[27] Almeida and Fornica.

[28] Mark Olleman, “Public Plan DB/DC choices,” Milliman, January 2009.

[29] The Segal Group, Public Employees’ Retirement System of the State of Nevada, Analysis and Comparison of Defined Benefit and Defined Contribution Retirement Plans , December 14, 2010.

[30] “Actuarial Analysis of Senate Bill 2 GA,” letter to Mr. William A. Theilen, COO Kentucky Retirement Systems, February 25, 2011.

[31] See analysis of Current Population Survey data in Keith A. Bender and John S. Heywood, Out of Balance? Comparing Public and Private Sector Compensation over 20 Years, Center for State & Local Government Excellence, National Institute on Retirement Security, April 2010, page 7, http://www.slge.org/vertical/Sites/%7BA260E1DF-5AEE-459D-84C4-876EFE1E4032%7D/uploads/%7B03E820E8-F0F9-472F-98E2-F0AE1166D116%7D.PDF ; and John Schmitt, The Wage Penalty for State and Local Government Employees, Center for Economic and Policy Research (CEPR), March 2010, http://www.cepr.net/documents/publications/wage-penalty-2010-05.pdf .

[32] Bender and Heywood, pp. 14-15.

More from the Authors

Areas of Expertise