Rebuilding the Unemployment Insurance System: A Deficit-Neutral Plan That Limits Tax Increases and Maintains Benefits

The systems for financing unemployment insurance (UI) in many states are broken and, without major reforms, they will remain broken through this decade and beyond, requiring years of high federal taxes on employers and threatening the system’s role as a key economic stabilizer during recessions. By enacting the plan outlined in this paper, however, federal policymakers would give states a framework to restore the long-term health of their UI systems, avoid significant tax increases on employers while the economy remains weak, and prevent damaging cuts in UI eligibility and benefits for jobless workers — all without increasing the federal deficit.

Currently, states levy taxes on employers to finance regular UI benefits for unemployed workers, generally up to 26 weeks. The federal government also levies a UI tax on employers, under the Federal Unemployment Tax Act (FUTA), to finance the administration of state UI programs. Since state UI trust funds may run dry when unemployment remains high for long periods, states can borrow from the federal UI trust fund and repay these loans in later years from employer taxes. If a state does not fully repay its loan within two years, the federal government is required to recoup it by raising federal UI taxes on employers in the state.

At the moment, 30 states have exhausted their UI trust funds in the face of high unemployment and are borrowing from the federal government. Total outstanding loans, which reached an estimated $41 billion at the end of 2010, will climb to a record $65 billion in 2013, the U.S. Labor Department projects.

To repay the principal on these loans, federal UI taxes on employers will increase automatically in a number of states this year or in early 2012 and rise to very high levels over the next few years. Employers in borrowing states will pay $5 billion to $7 billion in higher federal UI taxes before the end of 2013, and $16 billion to $24 billion in higher federal UI taxes over the next five years. Employers will continue to pay these higher federal UI taxes until the loan principal is paid off.

These automatic tax increases will not cover the interest due on these loans. Interest payments must be made separately, and are due in September of each year that a state is borrowing. To make these interest payments, states often enact special assessments on employers. So, in addition to paying higher federal UI taxes in the years ahead, employers also will face higher state UI taxes starting this year, as states enact special assessments to pay interest due on their loans by September 2011. States will pay $1.4 billion in interest in federal fiscal year 2011 and another $2.2 billion in 2012, the Labor Department projects.

These near-term tax increases will occur even though the economy will not likely regain its pre-recession strength for several years, and even though federal policymakers cut business taxes in December to encourage investment and hiring. [1] Meanwhile, with states facing large loan repayments and interest costs over the next several years, state policymakers will face considerable pressure to substantially cut UI eligibility and benefits, as states did the last time trust funds were severely depleted. As it is, only about a third of jobless workers receive state UI benefits, and large cuts on the benefit side would undermine the UI system’s ability to avert a collapse in jobless families’ purchasing power and help the economy during recessions.

The plan outlined in this report has five central elements:

- The federal government would gradually raise the amount of a worker’s wages subject to the federal UI tax (i.e., the FUTA taxable wage base), which has remained at the first $7,000 of a worker’s wages for nearly three decades, with no adjustment for wage growth or even for inflation. This would automatically raise the floor for the taxable wage bases in the states which by law cannot be lower than the federal wage base, helping states rebuild their trust funds by taxing a more adequate share of wages. The federal UI tax rate would fall, however, so that overall federal UI taxes did not go up.

- The federal government would provide a moratorium, until 2013, on state interest payments on their UI loans. That would reduce the adverse economic impact of business tax increases that most states would likely impose to finance those payments, delaying them until the economy is stronger.

- The federal government would also postpone, for two years, the FUTA tax increases required to recoup the loan principal in borrowing states. This, too, would delay business tax increases until the economy is stronger.

- The federal government would excuse a state from repaying part of its loan if the state (a) enters a flexible contractual agreement with the U.S. Labor Department to rebuild its trust fund to an appropriate level over a reasonable number of years, and (b) agrees to maintain UI eligibility, benefit levels, and an appropriate tax rate over the loan-reduction period. The amount of the loan that the federal government would excuse could vary by state, based on the severity of the recession in the state.

- The federal government would offer immediate rewards and future incentives for states that currently have and continue to maintain adequate trust fund levels. That would help address one cause of the current situation: many states failed to amass adequate trust funds when the economy was strong, largely because they had no incentive to do so; employers often push for low UI taxes even though that can lead to inadequate trust fund balances. Moreover, with some states maintaining very low taxes, employers in states that did build adequate trust funds were left feeling they were at a competitive disadvantage. One potential incentive for states would be a lower FUTA tax rate. The federal government could also pay a higher interest rate on assets in the state’s UI trust fund, and give states needed flexibility to use additional interest for purposes such as administration of state UI programs. (All states hold their major UI trust fund assets in the federal treasury.)

This plan would produce the following benefits:

- Employers would not pay higher federal UI taxes until the beginning of 2014, saving them $5 billion to $7 billion while the economy remains weak and $10 billion to $18 billion over the next five years, compared to current policy. Also, employers would pay no additional assessments to cover interest payments in 2011 or 2012, saving them $3.6 billion.

- In addition, partial loan forgiveness that comes from a state’s commitment to build adequate trust funds would save employers about $37 billion by the end of the decade. Counting the interest payments on this principal as well, employers could save as much as $50 billion.

- All or nearly all states would assume a path to permanent solvency; no state would find itself in a permanent cycle of borrowing, in which it cannot repay the loans it incurred in one recession before the next one strikes. This should sharply reduce state borrowing from the federal UI trust fund in future recessions.

- Employers in forward-looking states would receive concrete rewards and a more level playing field between the states.

- Adequate trust funds would stabilize UI tax rates over time, avoiding the roller-coaster tax rates common in many states — very low during healthy economic times, rising rapidly during recessions — that harm businesses and the economy.

- States would maintain current UI benefit and eligibility levels.

- The federal deficit would not rise as a result of these policies. By itself, the plan’s federal loan forgiveness component would increase the deficit by reducing future FUTA tax payments. But to qualify for partial loan forgiveness, states would have to build up their trust funds and – since state trust funds are held in a federal account – the increase in the trust funds would offset the revenue loss from the lower FUTA tax payments.

Unemployment Insurance Taxes – the Basics

Unemployment Insurance provides payments to eligible workers who are unemployed through no fault of their own and meet other eligibility requirements of state law. In part because states restrict who qualifies for unemployment insurance benefits, only about one in three unemployed workers receives them. Benefits average about $300 a week across the states, replacing just under half of an average worker’s wage. [2]

State UI Taxes

The states levy taxes on employers to cover “regular” UI payments for workers. Regular payments generally provide a maximum of 26 weeks of payments.

In all but three states, regular state UI taxes are collected entirely from employers. [3] The remaining three states also require minimal employee contributions. The amount of tax an employer pays for each of its employees is determined by the taxable wage base and the tax rate. Individual employers’ tax rates are determined by a combination of “experience rating,” which means that a business’ tax rate depends on its history of laying off workers. Businesses that lay off a lot of workers face a higher UI tax rate and thereby contribute more to the program that supports these workers than businesses that lay off few if any people. On average across states in 2009, employers contributed $293 per worker to state UI programs (less than 0.7 percent of total wages paid), but that amount varies greatly across states and across employers within states.

The state UI tax is not levied on the entire payroll of a firm, but rather on the first amount of dollars each employee earns; this amount is called the taxable wage base. The minimum taxable wage base that a state can use is $7,000 per employee. This minimum taxable base is by law the same as the taxable wage base for the federal UI tax (see below) and has not been increased since 1983. [4] The median state taxable wage base in 2011 is $12,000 (see Appendix A for state taxable wage bases in 2011).

Federal Unemployment Tax

The federal government, under the Federal Unemployment Tax Act [FUTA], also levies an unemployment insurance tax on employers. The taxable wage base of the federal tax is $7,000 per employee, and the effective tax rate is 0.8 percent of this base. [5] This amounts to $56 per year for most workers, although less for workers with less than $7,000 in annual earnings.

The federal tax pays for the administration of state UI programs; the federal government makes grants to states for this purpose. This tax also supports the account that has been used to pay for extended weeks of benefits during most recessions, and the fund from which states can borrow when necessary to pay regular state UI benefits. In this recession, however, states’ borrowing for their UI programs has far exceeded the available federal UI trust fund reserves, and the federal trust fund is borrowing, in turn, from the U.S. Treasury to make the loans to the states.

Without Major Reform, Most States Will be Unprepared for the Next Recession

At the end of 2010, some 30 state unemployment trust funds were insolvent and borrowing from the federal government to pay the regular 26 weeks of benefits to laid-off workers. Moreover, total state debt is likely to continue growing over the next two or three years. The U.S. Department of Labor projects that the total loans outstanding stood at $41 billion at the end of 2010 and will climb to $65 billion by 2013. [6]

Current law requires that the federal government recoup loans to state UI trust funds by raising federal UI taxes (known as FUTA taxes) on employers in the states that have borrowed. While the federal government ultimately will be repaid through this process, that will not restore the country’s UI system to health.

More specifically, states have roughly two years after borrowing to pay back loans that they take from the federal government to make regular UI payments. If a state does not pay back these loans in full by the deadline, the federal government will raise the FUTA tax by $21 per employee on businesses in the state and apply the resulting revenue toward reducing the loan principal balance. [7] If, by the following year, the state still has not paid back the loan, the FUTA tax will increase by another $21 per employee, so that the total increase reaches $42 per employee. The tax continues to increase by $21 increments in subsequent years until the loan is paid.

Businesses in Michigan, for example, saw their FUTA taxes increase by $21 per employee last year. This year, the tax is increasing to $42 per employee (above what employers would normally pay in FUTA taxes). In two additional states — Indiana and South Carolina — businesses are seeing their first FUTA tax increases this year. In about 21 additional states, FUTA taxes on businesses will increase early next year.

Even as the federal government increases FUTA taxes to recoup the loans, states will need to raise their own UI taxes to build their trust funds adequately for the next recession. However, if the combination of federal and state UI taxes rises too sharply, especially during a time when the economy remains weak, some businesses could be discouraged from hiring additional workers.

Under current and reasonably projected patterns of state UI tax collections and benefit payments, states in aggregate will not begin to move from repaying their federal loans to building their UI reserves until 2018. [8] Some 10-15 states will remain insolvent ten years from now. While no one knows when the next recession will occur, there is a reasonable likelihood that there will be one within the next 10 years, before these states can climb out of debt.[9]

When the next recession does hit, states that have not repaid their debt from this recession will have to borrow additional funds and be forced to go even deeper into debt in order to pay basic UI benefit payments to their unemployed residents. States in this position may need to borrow indefinitely from the federal government to pay regular payments, caught in a cycle of borrowing they cannot repay between recessions, unless they reform the financing of their trust funds.

In addition, many other state UI trust funds will still be weak when the next recession hits, even if another recession does not hit for another decade. Only about 12 states are projected to have reserves at the end of 2020 that meet the standard the Department of Labor suggests, which is enough to make one year of benefit payments at the level these payments reached in the average of the previous three recessions (called an Average High Cost Multiple, or AHCM, of 1.0).[10] Another eight states are projected to have reserves at the end of 2020 that equal at least half of the Department of Labor’s standard (measured as an AHCM of 0.5). The rest of the states — 30 of them — likely will be unprepared to make basic payments for their workers in the next recession without borrowing — or borrowing more — from the federal government, even if that recession does not strike for another ten years.

| TABLE 1: Under current law, most states still will be unprepared for a recession in 2020. The proposed UI State Solvency Plan results in many more states being prepared. | ||||||||

| State | Current law, projection for 2020 | UI State Solvency Plan, projection for 2020 | ||||||

| Out of debt | Halfway to adequacy^ | Adequate trust fund^ | Out of debt | Halfway to adequacy^ | Adequate trust fund^ | |||

| AK | Yes | No | No | Yes | No | No | ||

| AL | Yes | No | No | Yes | Yes | Yes | ||

| AR | Yes | Yes | No | Yes | Yes | Yes | ||

| AZ | No | No | No | Yes | No | No | ||

| CA | No | No | No | Yes | Yes | Yes | ||

| CO | Yes | Yes | Yes | Yes | Yes | Yes | ||

| CT | No | No | No | Yes | No | No | ||

| DE | No | No | No | Yes | No | No | ||

| FL | No | No | No | Yes | Yes | Yes | ||

| GA | Maybe | No | No | Yes | Yes | Yes | ||

| HI | Yes | Yes | No | Yes | Yes | No | ||

| IA | Yes | Yes | Yes | Yes | Yes | Yes | ||

| ID | Yes* | Yes | No | Yes | Yes | No | ||

| IL | No | No | No | Yes | No | No | ||

| IN | Yes | Yes | No | Yes | Yes | Yes | ||

| KS | Yes | Yes | Yes | Yes | Yes | Yes | ||

| KY | Yes | No | No | Yes | Yes | Yes | ||

| LA | Yes | No | No | Yes | Yes | Yes | ||

| MA | Yes | No | No | Yes | Yes | No | ||

| MD | Yes | Yes | Yes | Yes | Yes | Yes | ||

| ME | Yes | No | No | Yes | Yes | No | ||

| MI | No | No | No | Yes | Yes | Yes | ||

| MN | Yes | Yes | Yes | Yes | Yes | Yes | ||

| MO | Yes | Yes | No | Yes | Yes | Yes | ||

| MS | Yes | Yes | No | Yes | Yes | Yes | ||

| MT | Yes | No | No | Yes | No | No | ||

| NC | No | No | No | Maybe | No | No | ||

| ND | Yes | Yes | Yes | Yes | Yes | Yes | ||

| NE | Yes | Yes | Yes | Yes | Yes | Yes | ||

| NH | Yes | Yes | Yes | Yes | Yes | Yes | ||

| NJ | Yes | No | No | Yes | No | No | ||

| NM | Yes | No | No | Yes | No | No | ||

| NV | Yes | No | No | Yes | No | No | ||

| NY | Yes | No | No | Yes | Yes | Yes | ||

| OH | Maybe | No | No | Yes | Yes | Yes | ||

| OK | Yes | No | No | Yes | No | No | ||

| OR | Yes | Yes | No | Yes | Yes | No | ||

| PA | No | No | No | Yes | Yes | Yes | ||

| RI | Maybe | No | No | Maybe | No | No | ||

| SC | Yes | No | No | Yes | Yes | No | ||

| SD | Yes | Yes | Yes | Yes | Yes | Yes | ||

| TN | Yes | Yes | Yes | Yes | Yes | Yes | ||

| TX | Yes* | No | No | Yes | Yes | Yes | ||

| UT | Yes | Yes | No | Yes | Yes | No | ||

| VA | No | No | No | Yes | Yes | Yes | ||

| VT | Yes | No | No | Yes | Yes | No | ||

| WA | Yes | Yes | Yes | Yes | Yes | Yes | ||

| WI | Yes | No | No | Yes | Yes | Yes | ||

| WV | Yes | No | No | Yes | No | No | ||

| WY | Yes | Yes | Yes | Yes | Yes | Yes | ||

| Total "yes" | 37-40 | 20 | 12 | 48-50 | 37 | 29 | ||

| * Texas issued bonds to pay off its loan debt in December 2010. Idaho’s governor said in a speech in January 2011 that the state intends to issue bonds to pay off its loan debt. The model employed to generate this table projected Idaho to be solvent by 2020 even without issuing bonds. The model projected Texas to remain insolvent in 2020 without the bond issuance. | ||||||||

Why This Has Happened

Some states prepared for the recession by building balances that were adequate, based on their experiences in previous recessions. In the last quarter of 2007, when the recession hit, some 17 states had balances higher than the Department of Labor’s standard for measuring trust fund adequacy (an AHCM of at least 1.0). All but four of these 17 states have avoided insolvency. Three of the four states that had the recommended balances but nevertheless are borrowing now from the federal UI trust fund were hit exceptionally hard by the bursting of the housing bubble and the economic downturn — Nevada, Arizona, and Florida. (The fourth state is Vermont.)

The remaining states were not adequately prepared. Their trust funds contained amounts insufficient to weather even a relatively modest recession.

A major reason such a large number of states were unprepared is that many states rejected the fundamental historic premise of UI financing — “forward funding.” As the unemployment insurance system in this country is designed, states are supposed to levy taxes on employers to build up balances in their UI trust funds during periods of healthy economic growth, and then draw down those balances to pay up to 26 weeks of payments to unemployed workers during local or national economic downturns and recessions. Forward funding assures that when recessions hit, unemployment payments will sustain laid-off workers and their families, whose spending in turn will support the economy at a time when consumer demand is weak.

More than a decade ago, the bi-partisan, blue-ribbon Advisory Council on Unemployment Compensation (ACUC), appointed by the President and Congressional leaders and headed by former Bureau of Labor Statistics Commissioner Janet Norwood, urged states to return to forward financing. In its recommendations, the council wrote:

During the past decade, many states with low or negative trust fund reserves have found themselves in the position of either having to increase taxes on employers in the midst of an economic downturn, or having to take measures to restrict eligibility and benefits for the unemployed. . . . The Council believes that it would be in the interest of the nation to begin to restore the forward-funding nature of the Unemployment Insurance system, resulting in a building up of reserves during good economic times and a drawing down of reserves during recessions. [11]

Rather than forward fund their programs, however, many states continued to use a “pay-as-you-go” approach that held taxes artificially low in the good years before the current recession hit. When they should have been preparing for the recession, many states allowed their tax rates to fall below levels that would be needed to build adequate trust fund reserves. Many states reduced their UI tax rates to historically low levels. In inflation-adjusted dollars, average UI taxes were $274 per employee in 2008, less than they had been in 1994 ($350), and far less than they were in 1984 ($515). The U.S. Department of Labor found that 28 states made significant legislative reductions of UI taxes between 1995 and 2001. [12]

In theory, states that used the pay-as-you-go approach planned to raise their UI taxes on employers as unemployment, and thus benefit payments to workers, rose in the next recession. In practice, however, most people agreed that the midst of a recession is the worst time to raise employer taxes, so scheduled tax increases were repealed or postponed and taxes did not rise to meet the demand. In a state where they did rise, Nebraska, employers absorbed a 140 percent one-year increase in taxes because of the “pay-as-you-go” rules. Not surprisingly, most states did not raise taxes and borrowed large amounts from the federal government.

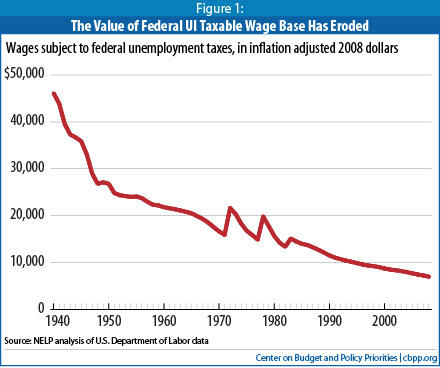

In addition to inadequate tax rates, many states base their UI taxes on a small and diminishing portion of wages. The taxable wage base for the federal FUTA tax establishes the minimum wage base for UI taxes in the states. The federal government has allowed this minimum to remain at $7,000 per worker since the early 1980s, nearly 30 years ago, without any adjustment for overall wage growth. Most states have maintained their taxable wage base at an amount that is only modestly above the $7,000 minimum; the median state taxable wage base in 2011 is $12,000 (see Appendix A). Since most states, like the federal government, do not increase their wage bases each year to keep up with overall wage growth, the share of wages that is subject to UI taxes declines each year.

The combination of declining state UI tax rates and low taxable wage bases left states more unprepared for the current economic downturn than they were before past recessions. In December 2007, when the current downturn began, state UI trust fund reserves were equal to 0.8 percent of total wages. By contrast, prior to the 2001 recession, state reserves were nearly double their level heading into the current downturn, a much greater 1.5 percent of wages. Before the 1990-91 recession, state reserves were even higher, at 1.9 percent of wages. Given the relative inadequacy of their reserves, states were especially unprepared for an unusually deep and protracted recession. This downturn has been longer and deeper than the past three recessions, and local sources of economic stress, such as foreclosures, have created particularly difficult conditions in some states. The unemployment rate — 9.0 percent as of January 2011 — has remained over 8 percent since February 2009, nearly two years ago.

In sum, most states allowed their taxable wage bases and tax rates to reach historically low levels in the good years before the recession hit, leaving their reserves vulnerable. Then they were clobbered by an unusually severe recession.

At this point, the imprudence of rejecting forwarding funding for “pay-as-you-go” has become clear. “Pay-as-you-go” systems require tax rates to go up when trust funds run low in recessions. But once the recession hit, states were caught between cancelling the planned tax rate increases (and borrowing more from the federal government) and increasing tax rates sharply during a recession or its aftermath when the economy remained weak and thereby slowing job growth at a crucial time for the economic recovery.

Goals for an Effective Policy Solution

There could be various ways to restore sustainable financing to the nation’s unemployment insurance system. The UI State Solvency Plan, presented here, is one that can meet a number of goals: (1) to put states on a course to rebuild adequate trust funds for future recessions; (2) to limit the necessary tax increases for businesses, especially in the near term while the economy remains weak; (3) to protect UI payments for workers and their families; and, (4) to avoid increasing the federal deficit.

1) Putting States on a Course to Rebuild Adequate Trust Funds for Future Recessions

As discussed above, the primary reason why 30 state UI trust funds are insolvent today is that most did not raise enough tax revenue during better economic times to prepare properly for a recession; that is, they did not forward fund their UI systems. To move to an appropriate level of forward funding of their trust funds, states will have to both establish adequate wage bases and maintain adequate, stable tax rates over time.

Improving UI financing in insolvent and barely solvent states would provide certain important advantages for businesses. For example, restoring adequate trust funds in all states will help employers in states that already operate forward funded UI systems by eliminating any competitive advantage enjoyed by employers in states with poorly funded, “pay-as-you-go” systems.

In addition, rebuilding adequate, sustainable trust funds will save businesses from paying unnecessary, additional taxes to cover the interest charges associated with state loans following the next recession. The U.S. Department of Labor estimates that under current law, insolvent states will pay more than $11 billion over the next five years in interest charges on UI trust fund debt, payments that are likely to come largely from additional tax assessments on business.[13]

In addition, restoring adequate trust funds will eliminate the roller coaster tax rates of recent years. In a sustainable, forward funded system, there’s no need for tax rates to fluctuate wildly, because they are set by reasonable expectations of benefit costs based on past experience. In an unsustainable “pay-as-you-go” system, by contrast, rates are set artificially low during good times. When a recession hits, states are forced to either sharply increase taxes to cover the surge in payments or borrow from the federal government, which will subsequently raise FUTA taxes on employers in the state to recoup the loans. Either way, employers cannot be sure when the artificially low tax rates of economic good times will suddenly surge, producing an unpredictable roller coaster ride for the businesses paying both UI taxes and the additional costs associated with paying the interest on the loans.

2) Limiting the Necessary Tax Increases for Businesses, Especially in the Near Future when the Economy will Remain Weak

Under current law, states will begin paying the interest on their outstanding loans in 2011, and businesses in most states that have borrowed will begin paying higher federal FUTA taxes to reduce the principal loan balance in early 2012 — a time when the unemployment rate is expected still to be well above pre-recession levels. (The Congressional Budget Office projects that the unemployment rate will remain above 8 percent throughout 2012.) In addition, to fund existing UI claims and prepare for the next recession, states will need to raise and maintain high UI taxes well into the future and in some cases indefinitely. Postponing the beginning of interest payments and additional FUTA taxes for two years would delay these tax increases until the economy is somewhat stronger.

3) Protect Payments for Unemployed Workers and Their Families

The last time that states faced significant UI trust fund debt — in the early 1980s — 44 states reduced benefits or eligibility to their programs, making it harder for workers to sustain their families when they are laid off. The share of unemployed workers getting UI payments fell from 45 percent in 1980 to 30 percent in 1984.[14]

State UI systems still have not recovered from the early 1980s cuts. Today, while temporarily expanded federal programs are covering more of the unemployed, only about one in three receive regular UI payments.

In most states, the UI benefits that workers receive are modest (and in some cases meager). The average weekly benefit nationally replaces less than half of an average worker’s wage.

Further restricting access or cutting benefit payments would undermine the unemployment insurance system’s basic purposes: to help the families of workers who have been laid off through no fault of their own, and to boost the economy during recessions by sustaining the spending power of unemployed workers. Unemployment payments are one of the most effective countercyclical tools available to policymakers, generating about $1.60 in economic activity during recessions for every dollar of payments provided. [15]

4) Avoid Adding to the Federal Deficit

Given the country’s troublesome longer-term federal deficit, an effective policy proposal for rebuilding sustainable state UI trust funds should not add to the federal deficit. To understand the impact of our proposal on federal deficits and debt, some background is necessary.

State UI trust funds are held in a federal account. As a result, changes in state trust fund balances affect the federal deficit. For example, raising state UI taxes would increase the revenue flowing into these accounts, thereby reducing the federal deficit. Cutting state UI taxes, on the other hand, enlarges the federal deficit. Loan forgiveness offered by the federal government also would, by itself, increase the deficit, because it would reduce future FUTA and state tax payments. Employing the right balance of the various policy levers — providing partial loan forgiveness in return for a state’s commitment to build adequate state trust funds (i.e., to build trust fund reserves to higher levels than they otherwise would reach) — can restore sustainability to the UI system without increasing the federal deficit.

The UI State Solvency Plan

The UI State Solvency Plan would meet these goals by implementing the following interrelated set of policies, which would prepare states for future recessions while limiting the necessary tax increases for businesses and protecting payments for workers — and without increasing the federal deficit.

- Beginning in two years, raise the federal taxable wage base gradually over several years. Since states must set their taxable wage base at least as high as the federal wage base, raising the federal taxable wage base will have the immediate effect of requiring states that have lower taxable bases to raise their own taxable wage bases. This will broaden the base of taxation and help states reach the goal of building adequate trust funds. If the federal wage base still equaled 40 percent of the average annual wage nationally, as it did when it was established in 1983, it would be about $18,000 today. [16]

There are many ways to structure a gradual increase in the federal taxable wage base. This paper modeled an approach that would gradually increase the base to $16,000 over five years, from 2013 to 2017. This plan could begin with an increase in the federal taxable wage base in 2013 from $7,000 to $10,000. More than half of states would be unaffected by that increase because their taxable wage base already is $10,000 or higher. In most of the remaining 18 states, the increase would be limited; fifteen of these states already have wage bases that exceed $7,000 .Table 2:

Federal Taxable Wage Base Under the UI State Solvency Plan2009 No change 2010 No change 2011 No change 2012 No change 2013 $10,000 2014 $11,000 2015 $12,000 2016 $14,000 2017 $16,000 2018 Indexed for wage inflation 2019 Indexed for wage inflation 2020 Indexed for wage inflation

In the 2014-17 period, when the economy is expected to be on a stronger footing, the wage base could increase gradually from $10,000 to $16,000. For example, it could increase to $11,000 in 2014, $12,000 in 2015, $14,000 in 2016, and $16,000 in 2017. About 17 states still would be unaffected even in 2017 when the wage base would reach $16,000, because their bases are already over that level.

Regardless of how the wage base is gradually increased, it should be set to adjust annually so it keeps up with overall wage growth, helping to maintain the system’s health over time. In the scenario described above, the base would be adjusted annually in accordance with the rate of growth in total national wages, beginning in 2018.

The point of increasing the federal taxable wage base is to raise the wage bases in the states, fixing one of the major problems with today’s UI financing system — namely, that states are not applying their tax rates to a large enough proportion of total wages. There is no need to raise federal FUTA taxes substantially; for this reason, we recommend reducing the FUTA tax rate to offset the effect of the increase in the wage base — thereby holding constant the effective tax rate. Currently, employers pay 0.8 percent of federal taxable wages — $56 per employee — in FUTA taxes. If the federal taxable wage base increased to $16,000, adjusting the current 0.8 percent rate to 0.35 percent would produce the same $56 tax per employee. In other words, employers would see no increase in their FUTA taxes. We propose that as the federal taxable wage base increases, the FUTA tax rate should decline so that most or all of the federal tax increase is eliminated. [17] Overall, the UI State Solvency Plan would be deficit neutral for the federal budget, with a federal rate reduction that offsets the increased federal wage base. - Delay loan interest payments. The 30 states currently borrowing must pay the interest that will accumulate on their loans in 2011, through September 30. [18] The U.S. Department of Labor projects that states will pay $1.4 billion in interest in federal fiscal year 2011 and another $2.2 billion in federal fiscal year 2012. [19]

This interest cannot be paid out of regular UI tax collections. As a result, most states are likely to impose a special assessment on businesses. Some states may take the revenue out of their General Funds, reducing the funding available to schools, health care, and other public necessities, or find some other revenue source. Regardless, the steps states take are likely to reduce economic activity at a time when the economy remains fragile. Providing a moratorium on interest payments until 2013 will lessen the adverse effects on the economy. - Postpone for two years the FUTA tax increases required to recoup the loan principal in borrowing states. The FUTA tax increases imposed on borrowing states to force loan repayment would be postponed for two years. This would help employers that are still suffering from the aftermath of the recession. In particular, it could help avoid a tax increase on employers in a state at a time when the unemployment rate is expected to remain quite high. Since the FUTA tax increase is imposed across-the-board on all businesses in a state, regardless of their experience rating, employers who have maintained or expanded their workforces in recent years — or are currently adding jobs — would avoid seeing their tax increased in the next couple of years to repay loans for benefits that went primarily to the former employees of other companies.

The UI State Solvency Plan envisions no FUTA tax increases in 2011 and 2012, with the increases resuming in 2013, beginning at a first-year cost of $21 per worker in 2013 (with the first payments due in January, 2014). - Reward states that already have, or build, adequate trust funds. The plan also rewards those states which entered this recession with strong trust funds and did not borrow much or at all from the federal government. They may perceive a policy of forgiving some of the loan debt accumulated by less forward-looking states as inequitable if no reward is offered to states that properly financed their UI programs.

One potential method to aid the forward-looking states (that is, the employers therein) would be a reduction in the FUTA tax rate for states that meet solvency standards. For example, employers in states whose trust funds meet the Department of Labor’s standard for adequacy (measured as an AHCM of 1.0) could receive a FUTA tax reduction of $14 per employee. This policy to reward forward-looking states would cost the federal government roughly $300 million on average annually from 2012 to 2020. Even with this provision, the overall policy proposal is deficit neutral.

The federal government could also reward solvent states by paying a higher interest rate on the UI funds that these states hold in federal accounts, where all states hold their UI trust funds. Solvent states could be given the option to appropriate these additional payments to help cover administrative costs. This option likely would be attractive to the many state agencies struggling to meet the program’s administrative demands with antiquated computer systems and an overworked staff. Businesses in many states also could benefit from this option, since the additional funding could reduce the state UI taxes that businesses pay to help cover state administrative costs.

- Limit tax increases in future years by forgiving a portion of the debt in states that have borrowed but that enter into a contract committing them to rebuilding adequate trust funds (without benefit cuts) . The federal government would excuse a portion of each state’s outstanding loans in return for the state’s entering into a contractual agreement with the Department of Labor to rebuild its trust funds to reach the U.S. Department of Labor’s standard for trust fund adequacy (an AHCM of 1.0) within a reasonable period of time, depending on the severity of the state’s insolvency problem.

The amount excused could vary by state, based on the severity of the recession in the state, in order to reduce the “moral hazard” of helping states in which the need to borrow stemmed more from the failure to build the state’s trust fund prior to the recession than from the severity of the recession in the state. The severity of the recession could be measured by the increase in the state’s unemployment rate over its base unemployment rate prior to the recession.[20]

For example, the amount excused could equal 60 percent of the end-of-calendar-year loan balance (as of a recent date prior to the passage of the legislation) for the hardest-hit states. Other states hit less hard by the recession could be placed in two lower tiers in which the amount forgiven would be smaller — perhaps equaling 40 percent of the loan balance for states hit somewhat hard by the recession and 20 percent for states hit less hard.

Because in many states the total amount borrowed from the federal government is expected to rise substantially over the next few years as unemployment remains at high levels, basing the amounts to be forgiven on states’ outstanding loan balances shortly before the legislation is enacted would mean that, even in the hardest-hit states, less than 60 percent of total loans would be forgiven. Under the UI State Solvency Plan, states would receive roughly $37 billion in loan forgiveness out of $70 billion in total loans projected by 2012. [21]

The partial loan forgiveness would be distributed to states in equal payments over a number of years, to encourage and assure continued adherence to the contract. For the purposes of costing out this proposal, it is assumed that the federal government will offer $37 billion in forgiveness and that states – in the aggregate – will receive this amount in equal $5.3 billion installments over a seven-year period.

- Require states accepting loan forgiveness to maintain current tax rates, payments, and eligibility standards. The agreement that states would make with the Department of Labor to have a portion of their loans forgiven should require that the state maintain at least its current UI tax rates on employers for the full period of the agreement, in order to assure that states use the incentive payments and (in some states) higher taxable bases to rebuild their trust funds. Specifically, states under such a contract should not be able to cut their average tax rate on total covered wages. Nor should they be able to repeal any tax increases already scheduled to take place during the agreement period. States achieving an adequate reserve balance during the agreement period could be allowed to lower their tax rates as long as they maintained an adequate reserve balance.

The agreement should also require that the state maintain its current benefit levels and eligibility standards. In the aftermath of the recession in the early 1980s, which was the last time that states borrowed a substantial amount from the federal UI trust fund to pay benefits, only modest relief from repayment was provided. States returned their trust funds to solvency in substantial part by cutting the benefit amounts that unemployed workers receive and by scaling back their eligibility rules to provide benefits to fewer unemployed workers. In the aftermath of that recession, more than 40 states enacted more restrictive benefit or eligibility standards or stricter disqualification standards. Between 1980 and 1984, the share of unemployed workers receiving UI payments fell from 45 percent to 30 percent, as many states sharply restricted access to their programs. The maintenance-of-effort suggested here would prevent a repeat of that scenario, from which the UI system still has not adequately recovered.

Within the bounds of these maintenance-of-effort requirements, states should be given the authority to determine how they will reach the Department of Labor’s standard for adequacy (measured as an AHCM of 1.0) While the goal of the plan is for states to reach this adequacy standard by 2020, the Department of Labor would be given authority to approve a plan that has a longer time frame in states with a severe financing crisis. [22]

Benefits of the UI State Solvency Plan

The UI State Solvency Plan, which incorporates the above provisions, would restore the health of the nation’s UI system while limiting tax increases (especially in the near term) and protecting UI benefits. Moreover, it would accomplish these goals without increasing the federal deficit.

A Major Improvement Over the Status Quo

This plan is a significant improvement over what is likely to happen if current policy conditions are allowed to play out (the “baseline” scenario). Using reasonably projected patterns of tax collections and benefit payments (see Appendix B for methodological details), the baseline scenario produces the following:

- Employers in a number of states will see their federal UI taxes rise this year or in early 2012 and climb to very high levels over the next few years. Employers in these borrowing states will pay between $5 billion and $7 billion in increased federal UI taxes before the end of 2013. Over the next five years, employers in more than half of all states will pay between $16 billion and $24 billion in increased federal UI taxes.

- Employers also will see their state UI taxes increased starting this year, as states enact special assessments to pay $1.4 billion in interest payments due by September 2011 on loans they have already taken from the federal UI trust fund. Next year, employers will see more special assessments to pay approximately $2.2 billion in additional interest payments that will be due by September 2012.

- These near-term tax increases are scheduled to occur even though the economy is not expected to regain its pre-recession strength for a number of years (and even though federal policymakers reduced business taxes as part of the December 2010 compromise legislation to encourage investment and hiring).[23]

- In addition, substantial pressure will mount for benefit and eligibility cuts this year and over the next several years as UI systems face large loan repayments and interest costs. Yet substantial cuts in eligibility and benefits would undermine the basic purpose of the UI program and weaken the recovery in the period ahead while it remains weak. UI payments generate about $1.60 in economic activity for every dollar of benefits provided, a significantly greater bang-for-the-buck than other policies intended to promote growth and jobs in a weak economy.

- States will continue to have few, if any, incentives to build and maintain adequate trust funds; as a result, employer pressures for lower UI taxes will be difficult to resist, even when state trust fund balances are low.

Under the UI State Solvency Plan, by contrast:

- The nation’s UI system would return to health. The fundamental historic premise of UI financing — forward funding to build up trust funds in good economic times for use during recessions — would be restored.

- All or nearly all states would be on a path to permanent solvency. No state would be caught in a permanent cycle of borrowing.

- Employers would not pay higher federal UI taxes until the beginning of 2014, saving them $5 billion to $7 billion while the economy remains weak and $10 billion to $18 billion over the next five years, compared to current policy. Also, employers would pay no additional assessments to cover interest payments in 2011 or 2012, saving them $3.6 billion.

- Partial loan forgiveness that comes from a state’s commitment to build adequate trust funds would save employers about $37 billion by the end of the decade. Counting the interest payments on this principal as well, employers could save as much as $50 billion.

- Adequate state trust fund balances ultimately would stabilize UI tax rates over time, avoiding the roller-coaster rates common in many states — very low during healthy economic times and rising rapidly during recessions — that harm businesses and the economy.

- The federal deficit would not increase.

- Current benefit and eligibility levels would be maintained.

- States maintaining adequate trust funds would receive financial rewards from the federal government, including additional funding that these states could use to help cover their administrative costs.

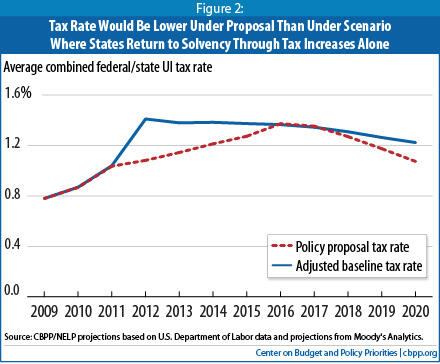

In achieving this much improved policy environment, the UI State Solvency Plan would slightly lower UI tax rates next year when the economy remains relatively weak, and then increase them modestly above the baseline. The average combined federal and state UI tax rate would reach about 1.4 percent of total wages in 2016, compared to about 1.1 percent of wages under the baseline scenario. After 2016, when trust funds are beginning to properly fill, the average combined tax rate would decline, reaching about 1.0 percent of wages in 2020, similar to where rates would be under the baseline scenario. Even at their peak in 2016, these average tax rates would be similar to historical UI tax rates from the 1980s.

Holds Taxes Down Compared To a “Tax Only” Scenario

States could attempt to restore the adequacy of their trust funds under current law through tax increases alone. Without the provisions in the UI State Solvency Plan for limiting tax increases (delaying when federal UI taxes increase to recoup the loans, delaying interest payments, and partial loan forgiveness), however, that approach would require sharp tax increases beginning while the economy remains weak. Compared to a hypothetical scenario (referred to here as an “adjusted baseline” scenario), in which all or nearly all states do achieve solvency by 2020 by raising state UI taxes, even as employers continue to pay increased FUTA taxes to repay the loans, the UI State Solvency Plan produces significantly lower average employer tax rates nationally. That is, raising the combined federal and state UI tax rate enough for nearly all states to achieve an AHCM of 1.0 by 2020 would produce significantly higher tax rates than would be required under the UI State Solvency Plan, especially in the next several years when the economy likely will remain weak (see Figure 2).

Appendix A

| State Taxable Wage Bases in 2011 | |||

| Alabama | $8,000 | Montana* | $26,300 |

| Alaska* | $34,600 | Nebraska | $9,000 |

| Arizona | $7,000 | Nevada* | $26,600 |

| Arkansas | $12,000 | New Hampshire | $12,000 |

| California | $7,000 | New Jersey* | $29,600 |

| Colorado | $10,000 | New Mexico* | $21,900 |

| Connecticut | $15,000 | New York | $8,500 |

| Delaware | $10,500 | North Carolina* | $19,700 |

| Florida | $7,000 | North Dakota* | $25,500 |

| Georgia | $8,500 | Ohio | $9,000 |

| Hawaii* | $34,200 | Oklahoma* | $18,600 |

| Idaho* | $33,300 | Oregon* | $32,300 |

| Illinois* | $12,740 | Pennsylvania | $8,000 |

| Indiana | $9,500 | Rhode Island | $19,000 |

| Iowa* | $24,700 | South Carolina | $10,000 |

| Kansas | $8,000 | South Dakota | $11,000 |

| Kentucky | $8,000 | Tennessee* | $9,000 |

| Louisiana* | $7,700 | Texas | $9,000 |

| Maine | $12,000 | Utah* | $28,600 |

| Maryland | $8,500 | Vermont | $13,000 |

| Massachusetts | $14,000 | Virginia | $8,000 |

| Michigan | $9,000 | Washington* | $37,300 |

| Minnesota* | $27,000 | West Virginia* | $12,000 |

| Mississippi | $14,000 | Wisconsin | $12,000 |

| Missouri* | $13,000 | Wyoming* | $22,300 |

| *Taxable wage base is adjusted automatically, typically on an annual basis. Source: Department of Labor Employment and Training Administration and the American Payroll Association. | |||

Appendix B: Methodology

Staff at the Center on Budget and Policy Priorities and the National Employment Law Project developed a model to project trends in state UI trust funds under current policy conditions and under the improved policy environment that would be created by the UI State Solvency Plan.

This modeling began with historical data contained in the U.S. Department of Labor’s (DOL)’s Unemployment Insurance Financial Data Handbook, which includes annual, state-by-state data for a wide variety of UI variables. These data were supplemented with more recent, comparable data on state UI programs from other DOL sources and the U.S. Department of the Treasury, and with historical data on employment and wages from the Bureau of Labor Statistics and the Bureau of Economic Analysis, respectively. [24] Finally, state-by-state projections of wages and unemployment, as well as national projections of the average employer tax rate were added to the model.

The model was then used to project payments, contributions, and other key UI financing variables for each state through 2020. Below is a brief summary of how projections of the key variables were calculated. [25]

The future costs of UI payments were estimated based on the historical relationship between state unemployment rates and benefits (expressed as a share of wages).

Contributions under base scenario were estimated based on DOL projections of the average employer tax rate nationally in future years. States whose reserves remained low in 2014 or later were required to diverge from the national pattern of declining rates at that point and maintain relatively high tax rates. States achieving adequate levels of reserves were set to reduce their rates more deeply than the national pattern would have allowed.

Contributions under proposed policy scenario were estimated by first converting the base scenario tax rates from rates based on total wages to rates based on taxable wages. The conversion was based on ratios of taxable to total wages in each state in 2008, and a model of how those ratios would change if the taxable wage base were increased. [26] Adjustments were made to reflect that these ratios will decline over time in states with a taxable wage base that is not indexed for inflation. When the conversion was completed, the converted rates were adjusted to reflect the impact of the taxable wage base increases proposed by the UI State Solvency Plan. Finally, the new rates were applied to a taxable wage base adjusted to reflect the changes proposed by the plan, producing a contributions estimate for each state through 2020.

Interest credited to state trust funds was calculated based on the historical relationship between UI trust fund interest and 10-year Treasury yields (10-year Treasury notes are one of the instruments used to determine the interest rate states earn on their UI trust funds). This historic ratio was applied to Congressional Budget Office projections of 10-year Treasury yields through 2020.

FUTA credit reductions and interest payments on loans – The model mimics the legal specifications of FUTA credit reductions and interest payments on loans. For instance, the FUTA credit reduction is generally equal to 0.3 percent of federally taxable wages (the first $7,000 of each covered worker’s earnings). The model’s employment projections for each state were used to project covered employment, allowing for a projection of federally taxable wages, which then allowed for a projection of the FUTA credit reduction in states that had been borrowing for the requisite period of time.

The amount of loan forgiveness each state would receive under the UI State Solvency Plan was estimated based on the increase in unemployment in the state in recent years, and each state's projected loan balance at the end of 2011. Each state was put into categories modeled on the unemployment "tiers" used in the formula for distributing additional Medicaid assistance to states under the American Recovery and Reinvestment Act (also known as the “enhanced FMAP”). Then, each state's loan forgiveness amount was calculated using the following criteria:

- 60 percent of state's net loan balance in 2011 if the unemployment rate in 2011 at least 3.5 percent higher than in the base period (the three-consecutive month period of the lowest average unemployment rate beginning in January 2006)

- 40 percent of net loan balance in 2011 if unemployment rate between 2.5 and 3.5 percent higher than in the base period

- 20 percent of net loan balance in 2011 if unemployment rate between 1.5 and 2.5 percent higher than in the base period

- No payment if unemployment rate less than 1.5 percent higher than in the base period

For the purposes of illustrating the impact of the UI State Solvency Plan in this report, the payments were spread over 7 years (i.e. states were assumed to receive one-seventh of their total loan each year from 2012 through 2018).

Reward to forward-looking states – To illustrate the impact of the UI State Solvency Plan, states with an AHCM of 1.0 or higher were provided an additional FUTA credit reduction equal to $14 for every covered employee.

End Notes

[1] Congress temporarily provided certain investment incentives under S.A. 4753, the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (the tax cut extension bill President Obama negotiated with Congressional Republicans in December 2010).

[2] In 2007, the most recent year for which data are available, the average worker collecting UI received benefits equal to about 47 percent of lost earnings.

[3] However, see text box “Who Pays Unemployment Insurance Taxes” on p. 5.

[4] Technically, states may set their taxable wage bases below the $7,000 federal taxable wage base, but the law requires the federal government to sharply increase federal UI taxes on employers in states that fail to meet this minimum. As a result, no state sets their taxable wage base below $7,000.

[5] The stated tax rate is 6.2 percent, but employers in states that are compliant with federal UI regulations receive a 5.4 percent credit against their tax, resulting in a 0.8 percent effective rate. Of the 0.8 percent, 0.2 percent is a surtax that was enacted as a temporary measure in 1976 and has been repeatedly renewed since then. The current surtax is scheduled to expire in June, 2011.

[6] U.S. Department of Labor, “UI Data Summary FY 2011 Budget Mid-session Review,” available at http://ows.doleta.gov/unemploy/content/midsession_review.asp.

[7] The FUTA tax increase is technically imposed by reducing a credit against FUTA taxes employers would otherwise receive. The stated FUTA tax rate is 6.2 percent, but employers in states that are compliant with federal UI regulations receive a 5.4 percent credit against their tax, resulting in a 0.8 percent effective rate. To recoup the loans, the federal government reduces gradually the size of the credit. Generally the credit is reduced by 0.3 percent each year until the loan is repaid. Since the FUTA taxable wage base is $7,000 per employee, a 0.3 percent credit reduction is equivalent to a $21 per employee tax increase.

[8] See the Appendix for information on the methodology we used to project state trust fund balances over the next several years.

[9] If the current period of economic growth lasts as long as the last three periods of economic growth, it will end in a recession that starts in about 2017. At that point, some 11-13 states are projected to remain insolvent, similar to the projection for 2020.

[10] The Average High Cost Multiple (AHCM) is calculated by dividing a state's calendar year reserve ratio by their three year average high cost rate. The reserve ratio for a state is the trust fund balance as a percent of estimated wages for the most recent 12 months. The three year average high cost rate is the average of the three highest “benefit cost rates” — benefits paid as a share of total wages in taxable employment — in the last 20 years (or a period including three recessions, if that is longer than 20 years).

[11] Advisory Council on Unemployment Compensation, Report and Recommendations. February 1994.

[12] “National UI Issues Conference: State UI Taxes and Trust Fund Solvency,” Presentation by Ronald Wilus, U.S. Department of Labor, June 22, 2010.

[13] The money to pay this interest cannot come from regular UI collections, and so must come from special assessments on business, state general funds, or other sources. Twelve of the 30 borrowing states require automatic special assessments on business to pay off this kind of interest charge. Given that 46 states face shortfalls in their general fund budgets in the current fiscal year, with shortfalls continuing in most states in the next fiscal year, finding general funds to pay off the interest charges will be difficult in most states.

[14] National Employment Law Project, Understanding the Unemployment Trust Fund Crisis of 2010, April 2010, p. 8.

[15] Mark Zandi, “U.S. Macro Outlook: Compromise Boosts Stimulus,” Moody’s Analytics, December 8, 2010. Other analysts find that unemployment payments generate as much as $2 in economic activity during recessions for every dollar of payment provided. See The Role of Unemployment as an Automatic Stabilizer During a Recession, Impaq/Urban Institute for the U.S. Department of Labor, available at http://www.dol.gov/opa/media/press/eta/eta20101615fs.htm

[16] The median state taxable wage base in 2011 is $12,000.

[17] If some higher revenues are retained, they could be reserved to make up for the chronic shortfall in funding for states to administer the UI program.

[18] The 2011 interest accumulated through September 30, 2011 is due on that date -- September 30, 2011.

[19] U.S. Department of Labor, “UI Data Summary FY 2011 Budget Mid-session Review,” p. 14, available at http://ows.doleta.gov/unemploy/content/midsession_review.asp.

[20] This was the method used to determine the three tiers of enhanced Medicaid assistance to states under ARRA.

[21] The Department of Labor projects outstanding loans will peak at $65 billion at the end of federal fiscal year 2013. We estimate loans will peak at about $70 billion at the end of calendar year 2012 and stand at about $67 billion at the end of calendar year 2013. The primary reason why our estimates are higher than DOL's is the difference between the end of the federal fiscal year and the end of the calendar year. Loan balances tend to increase in the last three months of the year, between the end of the federal fiscal year (on September 30) and the end of the calendar year. During this time of year, states typically receive relatively little in revenue to cover the cost of payments because employers pay taxes for employees from the beginning of the calendar year until the taxable wage base is reached for each employee.

[22] A state looking for a model of how it could satisfy its agreement with the Department of Labor could look to South Carolina’s Act no. 234 of 2010. This law creates a long-term plan to reach the average high cost multiple of 1.0 by increasing tax rates and the state’s taxable wage base.

[23] Congress temporarily provided certain investment incentives under S.A. 4753, the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (the tax cut extension bill President Obama negotiated with Congressional Republicans in December 2010).

[24] The handbook data are available from the Department of Labor at http://workforcesecurity.doleta.gov/unemploy/hb394.asp. Because the site was not functioning when we attempted to access the data, we received the data by email from the Department of Labor.

[25] A more detailed methodological description is available upon request.

[26] The 2008 ratios were supplied by Wayne Vroman of the Urban Institute

More from the Authors

Areas of Expertise

Areas of Expertise