Employer-Based Health Coverage Declined Sharply Over Past Decade

Highlights Need for Successful Implementation of Health Reform Law

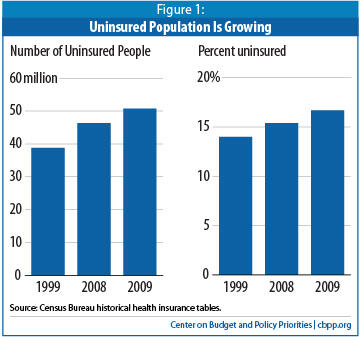

In September, the Census Bureau released data showing that the number and percentage of Americans without health insurance rose at a record pace in 2009, continuing a decade-long increase. This trend reflects the decline in private health coverage, primarily in employer-sponsored coverage. Although the severe economic downturn and corresponding job losses have accelerated the erosion of employer coverage, increasing health costs appear to be the primary catalyst of the decade-long decline in the share of Americans enrolled in health coverage through their employers.

Medicaid and the Children’s Health Insurance Program (CHIP) ensured that many of those losing employer-based coverage over the last decade — particularly children — did not become uninsured. In particular, both programs expanded to cover the swelling ranks of Americans lacking employer-based health insurance due to the 2001 and the current economic downturns. Federal policies enacted in response to the downturns were particularly critical: in both cases, Congress temporarily raised the share of Medicaid costs borne by the federal government to allow states to maintain their Medicaid programs despite large budget deficits resulting from depressed revenues.

If implemented successfully, the health reform law will reverse these trends of eroding employer-based coverage and a growing share of Americans without health coverage. The law’s expansion of Medicaid will provide a coverage option to poor adults, a population uninsured at an increasingly high rate. Small businesses will receive financial support to offer coverage to their workers, larger employers will pay a penalty if they do not offer affordable coverage to their workers, and more employees will be encouraged to take up offers of employer-sponsored insurance under the individual mandate — which will strengthen the employer-based insurance market. In addition, the new health insurance exchanges will make available more high-quality, affordable coverage options to individuals and small businesses, with premium and cost-sharing subsidies for low- and moderate-income individuals and families. Had health reform been in place in 2009, the number of people without health insurance would have increased by a much smaller amount.[1]

Ranks of Uninsured Swelled in 2009 and Over Past Decade

The share of the population without health coverage continues to grow across the country and across most segments of the population. For example, between 2008 and 2009, the uninsured rate grew among both workers and non-workers, among single individuals and those in families, among people in all regions of the country, among men and women, among those at all income levels, and among all major racial and ethnic groups other than Asians. Over a ten-year time frame (1999-2009), the increase in the uninsured rate is still greater in magnitude and broader in scope. Notably, however, Hispanics and poor children did not experience significant increases in the uninsured rate from 1999 to 2009. Medicaid, CHIP, and other publicly financed programs have generally stabilized insurance coverage among these groups. (See Appendix Table 1 for changes in the uninsured rate for different population groups.)

The uninsured rate is particularly high among certain populations. Nearly one of every three individuals living below the poverty line lacked insurance in 2009, as did more than one in four individuals with incomes between one and two times the poverty line. The uninsured rates were substantially higher in the South (19.7 percent) and West (18.3 percent) than in other regions. Nearly one of every three Hispanics was uninsured, a rate more than two and a half times greater than that for non-Hispanic whites. And, 19.7 percent of those living in inner cities were uninsured in 2009. These groups traditionally have suffered a high incidence of uninsurance, and 2009 was no exception.

American Community Survey Also Reveals Growing Uninsured Population

Subsequent to releasing results from the Current Population Survey, the Census Bureau released results from the American Community Survey (ACS) that also showed a significant increase in the uninsured population between 2008 and 2009. The ACS estimate is that 45.7 million people were uninsured in 2009 — 15.1 percent of the total population. This is an increase from the 43.6 million people reported uninsured in 2008 (14.6 percent of the total population). ACS data also show that in 2009, the uninsured rate was much lower among children (8.6 percent) than non-elderly adults (20.6 percent).[1]

The ACS is a nationally representative sample of the population that provides population and housing information annually by detailed geographic area. For the second year in 2009, the ACS survey includes estimates of respondents’ health insurance coverage status. These data will be available at the national, state, and congressional-district levels. They will also be available for geographic areas of at least 65,000 people, such as counties, cities, and metropolitan areas. The ACS data are particularly valuable for calculating single-year estimates at the sub-national level and for evaluating single-year trends at the sub-national level from 2008 to 2009.

Although a weak economy has contributed to the growth in the uninsured rate, research suggests that a return to economic growth and low unemployment will not reverse this trend by itself, as explained later in this report. On the other hand, the health reform law’s coverage expansions will change these figures dramatically when those expansions take effect in 2014.

Growth in Uninsured Reflects Erosion of Employer-Sponsored Coverage

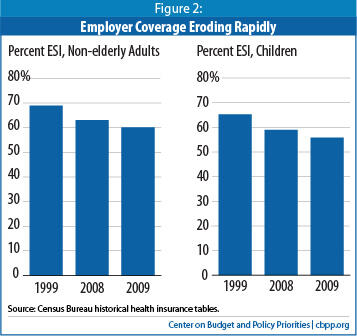

Employer coverage rates declined precipitously for both children and working-age adults. Only 55.8 percent of children had employer coverage in 2009, down 3.1 percentage points from 2008 and 9.3 percentage points from 1999. Likewise, only 60.1 percent of working-age adults had employer coverage in 2009, down 2.9 percentage points from 2008 and 8.8 percentage points from 1999. These historically low rates reflect both the large job losses resulting from the recession and the increasing difficulty that employers and workers are having in financing health care coverage as costs rise.

Job Losses Not Primary Cause of Eroding Employer Coverage

During the last decade, job losses were an important contributor to declining rates of employer-sponsored coverage. But they were not the primary factor, accounting for only 30-40 percent of the loss of employer coverage over one- and ten-year time frames.

The nation experienced two recessions between 1999 and 2009. The economic recovery from the March-November 2001 recession was among the weakest since World War II.[3] Many termed it a “jobless recovery,” as the total number of jobs did not exceed pre-recession levels until nearly four years after the end of the recession. During the 2007-2009 “Great Recession” that followed, by many measures the worst downturn since the Great Depression, the unemployment rate more than doubled from 4.6 percent in 2007 to 9.4 percent in 2009. [4] And because employers are the primary source of health insurance coverage, many workers who lost their jobs also lost their health coverage.

| TABLE 1: Employer Coverage Declines by Working Status | |||

| WORKING STATUS (adults, 18-64) | ESI Rate, 2009 | % Point Change from 2008 | % Point Change from 1999 |

| TOTAL | 60.1% | -2.9% | -8.8% |

| Full-time, year round | 77.2% | -1.0% | -3.8% |

| Less than full-time, year round | 50.6% | -2.7% | -9.2% |

| Did not work | 34.6% | -2.5% | -8.9% |

| Share of total change due to employment loss | 40% | 31% | |

| Source: CBPP analysis of Census Bureau data. | |||

However, the share of individuals with employer-sponsored coverage has dropped significantly among workers as well as those who are not working. Table 1 shows that in 2009, employer-sponsored coverage rates were significantly lower than in 2008 and 1999 for all groups in the labor force: those working full-time year-round, those working lesser hours, and those not working. While employment loss explains a portion of declining employer-sponsored coverage rates, there are other factors as well. Shifts in the labor market to more part-time work, a decline in the share of small businesses offering coverage, and increasing employee cost burdens all play a significant part.

Health Care Costs Rising and Employees Bearing Increasing Share of Costs

| TABLE 2: Family Coverage Premiums Rise Sharply | |||

| 1999 | 2009 | 2010 | |

| FAMILY COVERAGE PREMIUM | $5,791 | $13,375 | $13,770 |

| Employer Share | $4,247 | $9,860 | $9,773 |

| Employee Share | $1,543 | $3,515 | $3,997 |

| Growth Since Previous Year | n/a | 5.5% | 3.0% |

| Employer Share | n/a | 5.7% | -0.9% |

| Employee Share | n/a | 4.8% | 13.7% |

| Growth Since 1999 | n/a | 131.0% | 137.8% |

| Employer Share | n/a | 132.2% | 130.1% |

| Employee Share | n/a | 127.8% | 159.0% |

| Source: CBPP analysis of Kaiser Family Foundation/Health Research Education and Trust survey data. | |||

Results of an annual survey of employers show that health insurance premiums continue to rise, making coverage increasingly difficult to afford. In 2010, the average annual premium for single coverage was $5,049 — an increase of nearly 130 percent over the comparable 1999 estimate. The average premium for family coverage increased more than 140 percent over the same period, to $13,770.[5] Cumulative inflation from 1999 to 2010 is projected at only 32 percent, and the increase in nominal GDP from 1999 to 2009 at 48 percent. [6] Thus, each year insurance premiums have been consuming an ever-larger share of businesses’ budgets.

| TABLE 3: Single Coverage Premiums Rise Sharply | |||

| 1999 | 2009 | 2010 | |

| SINGLE COVERAGE PREMIUM | $2,196 | $4,824 | $5,049 |

| Employer Share | $1,878 | $4,045 | $4,150 |

| Employee Share | $318 | $779 | $899 |

| Growth Since Previous Year | n/a | 2.6% | 4.7% |

| Employer Share | n/a | 1.6% | 2.6% |

| Employee Share | n/a | 8.0% | 15.4% |

| Growth Since 1999 | n/a | 119.7% | 129.9% |

| Employer Share | n/a | 115.4% | 121.0% |

| Employee Share | n/a | 145.0% | 182.7% |

| Source: CBPP analysis of Kaiser Family Foundation/Health Research Education and Trust survey data. | |||

Survey data further reveal that businesses are passing along a greater share of these costs to their employees. In 2010, employees paid on average roughly $900 in premiums for single coverage (18 percent of the total) and roughly $4,000 in premiums for family coverage (29 percent of the total). Employees’ share of the cost is at a historically high level, as their premium payments have risen more than 180 percent for single coverage, and nearly 160 percent for family coverage, since 1999.[7] Meanwhile, median household incomes among non-elderly households have remained relatively stagnant since 1999, rising 19.3 percent in nominal terms and actually declining in real terms. [8] Thus, insurance premiums are consuming an ever-larger share of families’ budgets.

The transfer of premium costs from employers to their employees was particularly significant in 2010, as employees bore the entire increase in average premiums for family coverage from the prior year. Previously, employees had never been responsible for as much as half of the total premium increase in any given year. Although the premium increase for single coverage was shared more equally between employers and employees, employees’ 53 percent share of that increase was still a historical high. The result was that employees’ premium costs rose by 15.4 percent for single coverage and 13.7 percent for family coverage in 2010.[9]

| TABLE 4: Health Care Costs Rising for Workers | |||

| EMPLOYEES' OUT-OF-POCKET COSTS | 2001 | 2006 | Annual % Point Change |

| TOTAL, paid by employee | $2,875 | $3,842 | 6.0% |

| Premiums, paid by employee | $1,617 | $2,287 | 7.2% |

| Cost-sharing, paid by employee | $1,259 | $1,555 | 4.3% |

| Total As Share of Family Income | 3.8% | 5.0% | n/a |

| % of Employees with "High-Cost Burden" | 12.3% | 18.4% | n/a |

| Source: Commonwealth Fund. | |||

Researchers from the Commonwealth Fund found that premium cost increases are only a fragment of the full picture of rising health care costs. Using the most recent survey data available, they evaluated overall out-of-pocket health care costs — both premiums and cost sharing — as a percentage of families’ income. They found that the overall cost burden on families with employer-sponsored coverage rose from 3.8 percent to 5 percent of family income between 2001 and 2006. The share of families that bear a “high-cost burden” — defined as health care costs at 10 percent or more of family income — increased from 12.3 percent of all families with employer coverage to 18.4 percent of these families over the same period. [10] Notably, the analysts argue that the cost increases would have been even higher if insured families had not lowered their costs by making fewer visits to physicians, making better use of generic pharmaceutical options, and other steps. [11] Research by the RAND Corporation indicates that beneficiaries often respond to cost-sharing by forgoing needed as well as unneeded care.[12]

Rising Costs Weaken Participation in Employer-Sponsored Insurance

Certain types of businesses are much less likely to offer coverage than others. Small businesses in particular have a significantly lower offer rate (68 percent in 2010) than large businesses (99 percent). In the Northeast, 78 percent of firms offer coverage, compared to 70 percent in the West, 67 percent in the South, and 63 percent in the Midwest. Likewise, firms in the transportation and communications industries are much more likely to offer coverage than firms in the retail and health care industries.[13] The majority of firms not offering coverage report the high cost of health care as the most important reason for their decision. In many instances, these firms do not have the capital to provide coverage or cannot benefit from economies of scale due to their small work force.

Significant cost increases do appear to be taking a toll on employees’ participation in available plans. Since 1999, the percentage of workers in small firms who take up available coverage has declined from 83 percent to 77 percent. Even in large firms, often assumed to be relatively insulated from cost increases, employees’ participation declined from 86 percent to 82 percent over the same period. [14] Rising health care costs and relatively flat wages make it increasingly challenging for employees to purchase coverage when it is available.

Health care costs continue to grow at a rate that suggests a return to economic growth and low unemployment will not necessarily be enough to reverse the erosion of employer-sponsored coverage. As noted below, certain elements of the health reform law will take steps toward controlling costs. Moreover, individuals will have to be insured or pay a penalty, which should encourage more individuals to take advantage of offers of employer-sponsored insurance. Firms whose workers don’t have access to affordable coverage and purchase subsidized coverage through the new health insurance exchanges will be charged a penalty. Firms of fewer than 25 employees that employ a relatively low-wage work force can receive tax credits to help them offer coverage to their workers, and will be able to purchase coverage through the new health insurance exchanges, which should provide a greater choice of high-quality, affordable plans. These provisions collectively will serve as a counterbalance against rising costs and should maintain employers’ significant role in offering coverage to their workers.

Federal Government Subsidizing Coverage for the Unemployed

The Consolidated Omnibus Budget Reconciliation Act of 1986 (COBRA) requires most group health plans to provide a temporary continuation of group health coverage that otherwise might be terminated upon loss of employment. Employees who lose their jobs can remain in their employer-based health insurance plan if they pay the full cost of coverage, including administrative expenses. While the coverage generally proves to be less expensive and more comprehensive than coverage options available in the individual market, participation in COBRA is relatively low because of the high cost to former employees of coverage through COBRA.

During the recent recession, the federal government provided temporary financial support to workers who lost their jobs and were attempting to retain coverage from their former employer through COBRA. The 2009 Recovery Act included a provision to subsidize the purchase of COBRA coverage, and subsequent legislation extended this benefit. Any individual who was involuntarily terminated from employment between September 1, 2008 and May 31, 2010 was eligible for a tax credit equal to 65 percent of the cost of COBRA coverage for themselves and their family. These subsidies were available for 15 months after the worker’s termination date. In 2009, the subsidy reduced the average premium for single coverage through COBRA from $4,704 to $1,646 and for family coverage from $12,680 to $4,438. The remaining expenditures borne by the employee remained high, however — more than 10 percent of family income, on average; as a result, coverage through COBRA remained unaffordable for many families.

The temporary COBRA tax credit has now expired. Employees who lost their jobs after May 31, 2010 receive no assistance with their COBRA premiums and are at significant risk of ending up uninsured. Those terminated on or before May 31, 2010 could still receive a COBRA subsidy through August 2011.

Medicaid Helped Offset Decline in Employer Coverage, But Primarily for Children

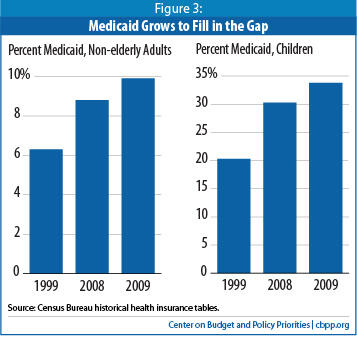

Age differences in the insurance data highlight the importance of Medicaid’s role in offsetting some of the erosion in private coverage. In 2009, despite the severe recession, the number and percentage of children who were uninsured did not rise: Medicaid coverage for children grew by 3.5 percentage points to offset a 3.1 percentage-point decline in employer coverage for children. In contrast, non-elderly adults experienced a large increase in uninsurance, with 4.1 million more of them being uninsured in 2009 than in 2008.

Many Young Adults Are Uninsured

The uninsured rate among young adults — those under 26 — continues to grow. In 2009, 9.6 million adults aged 18 through 25 were without coverage, or 32.7 percent of adults in this age group. This represents a 2 percentage-point increase in the uninsured rate from 2008 and a 4 percentage point increase from 1999.

As with the adult population as a whole, a decline in the rate of employer-sponsored coverage has precipitated this trend. The problem is particularly acute for young adults, as they historically have been in employment situations where coverage is more tenuous. Young adults are more likely to have unsteady employment, to be ineligible for available coverage, or to be unable to afford available coverage.

Provisions in the health reform law will provide multiple new avenues to coverage for this vulnerable population. Young adults under age 26 can enroll in employer-sponsored coverage available through their parents’ employer regardless of whether they live at home. In addition, the establishment of state health insurance exchanges will be of particular benefit to young adults with severe health conditions, who previously were often able to buy coverage only in a dysfunctional individual insurance market that charged exorbitant prices — if it made coverage available at all — to people with serious health problems.

The role that Medicaid and CHIP play in stabilizing children’s insurance coverage is even more apparent over time. Despite an eroding private health insurance market, the share of children without health coverage declined markedly from 12.5 percent in 1999 to 10 percent in 2009. This is entirely because coverage rates for children under Medicaid or the Children’s Health Insurance Program increased from 20.3 percent of all children to 33.8 percent over this period, an increase of 10.6 million children.

Medicaid Coverage More Expansive for Children Than Adults

The primary reason for the disparate fortunes of children and non-elderly adults is that income eligibility limits for Medicaid and CHIP are substantially higher for children than for adults. In the median state, children are currently eligible for Medicaid or CHIP up to about 240 percent of the poverty line. In contrast, working parents are eligible for Medicaid only up to 64 percent of the poverty line in the median state. Moreover, unemployed parents are typically eligible only up to 38 percent of the poverty line, and childless adults are not covered by Medicaid at all (except in a handful of states).

In nearly half of the states, the uninsured rate among children declined significantly between 1999 and 2009. In contrast, the uninsured rate among non-elderly adults rose in 35 states between 1999 and 2009. The District of Columbia, Massachusetts, and New York stand out as states in which uninsurance fell by a statistically significant amount among both children and non-elderly adults. Not coincidentally, these three states adopted eligibility expansions for adults in their Medicaid programs, and in the case of Massachusetts, established a private insurance exchange to expand the availability of high-quality, affordable health coverage. Appendix Table 2 and Appendix Table 3 look at the uninsured rate among both children and non-elderly adults in individual states over time.

Federal Government Provides Extra Medicaid Support During Downturns

Medicaid and CHIP are jointly financed by the federal government and the states. While the federal government supports the majority of the cost — on average, 57 percent of the total in Medicaid and 70 percent of the total in CHIP — the state share represents a significant component of states’ overall budgets. During a recession, the need for Medicaid and CHIP services increases while available revenues typically decline. This can make it extremely challenging for states to continue to operate strong programs.

As part of the 2009 Recovery Act, Congress increased the federal share of total Medicaid costs through December 31, 2010. In exchange, the federal government required states to maintain their eligibility levels and not make their enrollment procedures more restrictive than those as of July 1, 2008. The funding increase helped shore up state Medicaid programs so they could serve millions more individuals as people lost their jobs and private health coverage. Congress also temporarily increased the federal Medicaid matching rate in 2003, when states were still recovering from the 2001 recession and considering damaging Medicaid cuts. Without these temporary measures, the number of uninsured would undoubtedly have been even higher, because a number of state Medicaid programs would have cut their eligibility and/or made it more difficult to enroll.

Demand for Medicaid Will Remain High in Near Future

State officials anticipate continued high demand for Medicaid services as state economies slowly emerge from the severe economic downturn. In a recent survey, Medicaid directors estimated overall Medicaid spending growth of 7.4 percent in state fiscal year 2011, and over two-thirds of these directors expect that growth may exceed this level. This follows growth in state fiscal year 2010 of 8.8 percent, the highest single-year growth rate since the previous recession.[15]

This recent spending growth is almost entirely a result of increasing enrollment associated with the erosion of employer-sponsored coverage. Medicaid enrollment grew by 8.5 percent in state fiscal year 2010 and is projected to grow an additional 6.1 percent in state fiscal year 2011. States are attempting to control costs: 48 states implemented at least one cost-cutting measure in 2010 and 46 states plan to in 2011. The Recovery Act’s matching rate increase (as well as the health reform law) ensures that states cannot make cuts to eligibility, so states have focused primarily on reducing provider rates or, to a lesser extent, changing benefits.[16]

In August 2010, legislators extended a modified version of the Recovery Act provision to apply to Medicaid expenditures made in the first six months of calendar year 2011. States are projected to receive an additional $16.1 billion in matching funds during this period, which will be critical to maintaining their programs. Without an extension, state Medicaid expenditures were projected to rise 25 percent in state fiscal year 2011, an increase that likely could not be met given that state revenues have only recently begun to show modest growth.

The six-month extension of the federal fiscal relief was enacted after nearly all states had passed their 2011 budgets; about half the states had assumed this extension when formulating their budgets. States that did not assume the extension can revisit their 2011 budgets in light of it. To this point, a majority of states have used the Recovery Act funds to avert Medicaid cuts, close general fund shortfalls, and/or help cover the cost of Medicaid enrollment increases.[17]

Health Reform Law Will Help Reverse Long-Term Declines in Coverage

Finally, both the deterioration of the private health insurance market and the protective role that Medicaid has played illustrate the importance of implementing the health reform law. The Congressional Budget Office estimates that by 2019, the law will result in coverage for 32 million people who otherwise would be uninsured. The share of the population without coverage will decrease to roughly 6 percent.

Under the Affordable Care Act, starting in 2014, health coverage will be made available through the Medicaid program to low-income adults with incomes up to 133 percent of the poverty line (roughly $29,000 for a family of four in 2010). In addition, health insurance exchanges will be established in all states to make affordable private health insurance available to individuals and small businesses; people who don’t have an offer of affordable employer coverage and have incomes too high to qualify for Medicaid and CHIP — but below 400 percent of the poverty line — will qualify for subsidies to help them afford coverage in the exchanges.

In all states, the great majority of those uninsured will be eligible either for expanded Medicaid coverage or for subsidized insurance through the state-based exchange. Thus, health reform will sharply reduce the number of uninsured. (Appendix Table 4 provides state-level data.) Had these provisions already been in effect in 2009, the increase in the number of Americans without insurance would have been a modest fraction of what it was.

| APPENDIX TABLE 1: People without Health Insurance Coverage by Selected Characteristics | |||||||||||

| CHARACTERISTIC | UNINSURED RATES | COMPARE TO 2009 | |||||||||

| 1999 | 2007 | 2008 | 2009 | 1999 | 2007 | 2008 | |||||

| TOTAL | 14.0% | 15.3% | 15.4% | 16.6% | -2.6% | * | -1.3% | * | -1.2% | * | |

| AGE | |||||||||||

| Under 18 Years | 12.5% | 11.0% | 9.9% | 10.0% | 2.5% | * | 1.0% | * | -0.1% | ||

| 18 to 24 Years | 26.9% | 28.1% | 28.6% | 30.4% | -3.5% | * | -2.3% | * | -1.8% | * | |

| 25 to 34 Years | 21.8% | 25.7% | 26.5% | 29.1% | -7.3% | * | -3.4% | * | -2.6% | * | |

| 35 to 44 Years | 14.8% | 18.3% | 19.4% | 21.7% | -6.9% | * | -3.4% | * | -2.3% | * | |

| 45 to 64 Years | 11.9% | 14.0% | 14.4% | 16.1% | -4.2% | * | -2.1% | * | -1.7% | * | |

| 65 Years Older | 0.8% | 1.9% | 1.7% | 1.8% | -1.0% | * | 0.1% | -0.1% | |||

| RACE/ETHNICITY | |||||||||||

| White | 12.7% | 14.3% | 14.5% | 15.8% | -3.1% | * | -1.5% | * | -1.3% | * | |

| White, not Hispanic | 9.2% | 10.4% | 10.8% | 12.0% | -2.8% | * | -1.6% | * | -1.2% | * | |

| Black | 19.4% | 19.5% | 19.1% | 21.0% | -1.6% | * | -1.5% | * | -1.9% | * | |

| Asian | 18.4% | 16.8% | 17.6% | 17.2% | 1.2% | -0.4% | 0.4% | ||||

| Hispanic | 32.6% | 32.1% | 30.7% | 32.4% | 0.2% | -0.3% | -1.7% | * | |||

| WORKING (18-64) | |||||||||||

| All Workers | 15.8% | 18.1% | 18.7% | 20.2% | -4.4% | * | -2.1% | * | -1.5% | * | |

| Full Time, Year Round | 12.6% | 14.9% | 14.6% | 15.2% | -2.6% | * | -0.3% | -0.6% | |||

| Less Than Full Time | 23.0% | 25.7% | 27.3% | 29.7% | -6.7% | * | -4.0% | * | -2.4% | * | |

| No Work | 23.5% | 25.4% | 26.0% | 29.1% | -5.6% | * | -3.7% | * | -3.1% | * | |

| NATIVITY | |||||||||||

| Native | 11.8% | 12.7% | 12.9% | 14.1% | -2.3% | * | -1.4% | * | -1.2% | * | |

| Foreign born | 32.2% | 33.2% | 33.5% | 34.5% | -2.3% | * | -1.3% | * | -1.0% | * | |

| Naturalized | 16.3% | 17.6% | 18.0% | 19.0% | -2.7% | * | -1.4% | * | -1.0% | ||

| Non-citizen | 41.6% | 43.8% | 44.7% | 46.0% | -4.4% | * | -2.2% | * | -1.3% | * | |

| REGION | |||||||||||

| Northeast | 11.3% | 11.4% | 11.6% | 12.4% | -1.1% | * | -1.0% | * | -0.8% | * | |

| Midwest | 9.6% | 11.4% | 11.6% | 13.3% | -3.7% | * | -1.9% | * | -1.7% | * | |

| South | 16.0% | 18.4% | 18.2% | 19.7% | -3.7% | * | -1.3% | * | -1.5% | * | |

| West | 17.7% | 16.9% | 17.4% | 18.3% | -0.6% | * | -1.4% | * | -0.9% | * | |

| GENDER | |||||||||||

| Men | 15.2% | 16.7% | 17.0% | 18.4% | -3.2% | * | -1.7% | * | -1.4% | * | |

| Women | 12.9% | 13.9% | 13.8% | 15.0% | -2.1% | * | -1.1% | * | -1.2% | * | |

| INCOME | |||||||||||

| Under 100% FPL | 31.0% | 30.8% | 30.3% | 31.7% | -0.7% | -0.9% | * | -1.4% | * | ||

| 100%-199% FPL | 23.4% | 24.7% | 24.3% | 26.2% | -2.8% | * | -1.5% | * | -1.9% | * | |

| 200%-399% FPL | 12.3% | 14.6% | 14.7% | 15.3% | -3.0% | * | -0.7% | * | -0.6% | * | |

| 400% FPL + | 5.4% | 6.3% | 6.0% | 6.8% | -1.4% | * | -0.6% | * | -0.9% | * | |

| Source: Census Bureau historical tables. Note, a ‘*’ indicates that the difference between 2009 and the given year for a particular estimate is statistically significant at the 90 percent confidence level. | |||||||||||

| APPENDIX TABLE 2: Children Gain Ground | |||||||||||||||

| STATE | UNINSURED RATES | CHANGE | |||||||||||||

| Period 1: 1999/2000 | Period 2: 2006/2007 | Period 3: 2008/2009 | Period 2 to Period 3 | Period 1 to Period 3 | |||||||||||

| NATION | 12.5% | 11.0% | 10.0% | -1.0% | * | -2.5% | * | ||||||||

| Alabama | 9.3% | 7.4% | 5.8% | -1.6% | -3.6% | * | |||||||||

| Alaska | 15.4% | 10.9% | 12.2% | 1.4% | -3.2% | ||||||||||

| Arizona | 16.4% | 15.4% | 14.7% | -0.7% | -1.7% | ||||||||||

| Arkansas | 11.3% | 7.8% | 10.4% | 2.6% | * | -0.9% | |||||||||

| California | 16.0% | 11.8% | 10.6% | -1.2% | * | -5.4% | * | ||||||||

| Colorado | 14.6% | 13.8% | 11.0% | -2.9% | -3.7% | * | |||||||||

| Connecticut | 7.7% | 5.6% | 6.6% | 1.0% | -1.1% | ||||||||||

| Delaware | 6.3% | 9.6% | 9.0% | -0.7% | 2.7% | ||||||||||

| DC | 12.3% | 7.5% | 7.2% | -0.3% | -5.1% | * | |||||||||

| Florida | 16.3% | 19.1% | 17.3% | -1.8% | 1.0% | ||||||||||

| Georgia | 10.5% | 12.2% | 10.9% | -1.3% | 0.4% | ||||||||||

| Hawaii | 7.9% | 5.6% | 4.5% | -1.1% | -3.5% | * | |||||||||

| Idaho | 17.3% | 12.0% | 9.6% | -2.5% | -7.7% | * | |||||||||

| Illinois | 10.6% | 8.1% | 7.8% | -0.3% | -2.9% | * | |||||||||

| Indiana | 9.3% | 6.5% | 7.3% | 0.8% | -2.0% | ||||||||||

| Iowa | 6.1% | 5.6% | 5.6% | 0.1% | -0.5% | ||||||||||

| Kansas | 11.2% | 7.5% | 9.6% | 2.1% | -1.7% | ||||||||||

| Kentucky | 10.1% | 8.9% | 9.1% | 0.3% | -1.0% | ||||||||||

| Louisiana | 19.3% | 14.2% | 9.9% | -4.4% | * | -9.5% | * | ||||||||

| Maine | 7.6% | 5.8% | 4.9% | -0.9% | -2.7% | ||||||||||

| Maryland | 8.2% | 10.2% | 6.5% | -3.7% | * | -1.7% | |||||||||

| Massachusetts | 6.9% | 5.0% | 3.2% | -1.9% | * | -3.7% | * | ||||||||

| Michigan | 6.8% | 5.5% | 5.2% | -0.3% | -1.6% | * | |||||||||

| Minnesota | 6.0% | 7.4% | 6.1% | -1.3% | 0.0% | ||||||||||

| Mississippi | 11.7% | 15.5% | 12.2% | -3.4% | * | 0.5% | |||||||||

| Missouri | 5.2% | 9.8% | 8.3% | -1.5% | 3.1% | * | |||||||||

| Montana | 16.6% | 13.6% | 10.5% | -3.1% | -6.1% | * | |||||||||

| Nebraska | 7.7% | 10.1% | 8.4% | -1.7% | 0.7% | ||||||||||

| Nevada | 17.5% | 16.6% | 16.2% | -0.4% | -1.3% | ||||||||||

| New Hampshire | 6.1% | 7.0% | 3.7% | -3.3% | * | -2.4% | * | ||||||||

| New Jersey | 8.0% | 13.1% | 10.3% | -2.9% | * | 2.3% | * | ||||||||

| New Mexico | 21.9% | 16.7% | 15.1% | -1.7% | -6.9% | * | |||||||||

| New York | 10.4% | 8.7% | 7.3% | -1.4% | * | -3.1% | * | ||||||||

| North Carolina | 10.6% | 13.1% | 10.6% | -2.5% | * | 0.0% | |||||||||

| North Dakota | 10.2% | 9.1% | 6.9% | -2.2% | -3.3% | * | |||||||||

| Ohio | 9.0% | 7.2% | 7.3% | 0.1% | -1.7% | ||||||||||

| Oklahoma | 16.2% | 12.6% | 9.9% | -2.7% | -6.3% | * | |||||||||

| Oregon | 11.4% | 11.9% | 11.8% | -0.1% | 0.4% | ||||||||||

| Pennsylvania | 6.5% | 7.4% | 6.8% | -0.6% | 0.3% | ||||||||||

| Rhode Island | 4.7% | 6.5% | 7.0% | 0.5% | 2.3% | ||||||||||

| South Carolina | 12.6% | 12.5% | 12.6% | 0.1% | 0.0% | ||||||||||

| South Dakota | 8.4% | 8.6% | 9.2% | 0.6% | 0.8% | ||||||||||

| Tennessee | 7.3% | 7.8% | 8.0% | 0.3% | 0.7% | ||||||||||

| Texas | 22.7% | 21.3% | 17.2% | -4.1% | * | -5.5% | * | ||||||||

| Utah | 9.0% | 12.7% | 10.4% | -2.3% | 1.4% | ||||||||||

| Vermont | 5.1% | 8.7% | 4.7% | -4.0% | * | -0.4% | |||||||||

| Virginia | 11.2% | 10.2% | 7.2% | -3.0% | * | -4.0% | * | ||||||||

| Washington | 9.8% | 6.9% | 5.8% | -1.1% | -4.0% | * | |||||||||

| West Virginia | 11.2% | 6.6% | 6.3% | -0.3% | -4.9% | * | |||||||||

| Wisconsin | 6.5% | 5.4% | 5.3% | -0.1% | -1.3% | ||||||||||

| Wyoming | 13.0% | 8.9% | 9.2% | 0.3% | -3.8% | * | |||||||||

| Source: Census Bureau historical tables. Note, a ‘*’ indicates that the difference between 2008/2009 and the given year for a particular estimate is statistically significant at the 90 percent confidence level. | |||||||||||||||

| APPENDIX TABLE 3: Adults Lose Ground | |||||||

| STATE | UNINSURED RATES | CHANGE | |||||

| Period 1: 1999/2000 | Period 2: 2006/2007 | Period 3: 2008/2009 | Period 2 to Period 3 | Period 1 to Period 3 | |||

| NATION | 17.2% | 19.6% | 22.3% | 2.7% | * | 5.1% | * |

| Alabama | 16.7% | 18.6% | 21.0% | 2.5% | * | 4.3% | * |

| Alaska | 21.3% | 21.6% | 23.4% | 1.8% | 2.2% | ||

| Arizona | 21.7% | 24.5% | 24.5% | 0.0% | 2.8% | * | |

| Arkansas | 18.0% | 24.8% | 25.6% | 0.8% | 7.6% | * | |

| California | 22.5% | 23.9% | 25.7% | 1.8% | * | 3.2% | * |

| Colorado | 16.5% | 20.2% | 19.8% | -0.4% | 3.3% | * | |

| Connecticut | 11.4% | 12.6% | 14.8% | 2.3% | * | 3.4% | * |

| Delaware | 12.1% | 14.8% | 15.8% | 1.1% | 3.7% | * | |

| DC | 16.7% | 12.7% | 13.8% | 1.1% | -3.0% | * | |

| Florida | 22.6% | 26.3% | 28.0% | 1.8% | * | 5.5% | * |

| Georgia | 18.0% | 22.0% | 24.9% | 2.9% | * | 7.0% | * |

| Hawaii | 11.8% | 10.6% | 11.0% | 0.5% | -0.8% | ||

| Idaho | 19.4% | 18.8% | 21.0% | 2.2% | 1.7% | ||

| Illinois | 16.2% | 18.0% | 18.5% | 0.5% | 2.3% | * | |

| Indiana | 12.1% | 15.6% | 18.4% | 2.8% | * | 6.3% | * |

| Iowa | 10.0% | 13.7% | 14.2% | 0.5% | 4.1% | * | |

| Kansas | 13.0% | 17.0% | 16.4% | -0.6% | 3.4% | * | |

| Kentucky | 15.9% | 19.3% | 21.8% | 2.5% | * | 5.9% | * |

| Louisiana | 22.6% | 26.8% | 24.8% | -2.0% | 2.2% | ||

| Maine | 14.0% | 12.2% | 14.5% | 2.4% | * | 0.5% | |

| Maryland | 12.7% | 17.4% | 17.5% | 0.1% | 4.8% | * | |

| Massachusetts | 11.0% | 10.3% | 6.6% | -3.7% | * | -4.3% | * |

| Michigan | 11.6% | 15.2% | 17.9% | 2.8% | * | 6.3% | * |

| Minnesota | 8.6% | 10.8% | 11.4% | 0.6% | 2.8% | * | |

| Mississippi | 18.1% | 24.9% | 23.9% | -1.0% | 5.7% | * | |

| Missouri | 10.2% | 16.8% | 18.9% | 2.2% | * | 8.7% | * |

| Montana | 20.3% | 20.3% | 21.3% | 0.9% | 0.9% | ||

| Nebraska | 11.0% | 16.1% | 15.3% | -0.7% | 4.3% | * | |

| Nevada | 20.1% | 22.5% | 24.4% | 1.9% | 4.3% | * | |

| New Hampshire | 10.9% | 14.3% | 14.4% | 0.1% | 3.5% | * | |

| New Jersey | 15.4% | 19.3% | 19.3% | 0.0% | 3.9% | * | |

| New Mexico | 29.5% | 29.4% | 30.0% | 0.6% | 0.5% | ||

| New York | 20.6% | 18.0% | 19.4% | 1.5% | * | -1.1% | * |

| North Carolina | 16.8% | 21.8% | 22.2% | 0.4% | 5.4% | * | |

| North Dakota | 13.4% | 14.0% | 14.8% | 0.9% | 1.4% | ||

| Ohio | 12.7% | 14.4% | 17.7% | 3.3% | * | 4.9% | * |

| Oklahoma | 21.2% | 24.6% | 22.1% | -2.5% | 0.9% | ||

| Oregon | 15.6% | 22.4% | 22.4% | 0.0% | 6.7% | * | |

| Pennsylvania | 10.2% | 12.7% | 14.4% | 1.7% | * | 4.2% | * |

| Rhode Island | 9.1% | 12.5% | 15.8% | 3.3% | * | 6.8% | * |

| South Carolina | 16.5% | 20.9% | 21.6% | 0.8% | 5.2% | * | |

| South Dakota | 13.4% | 14.4% | 17.6% | 3.2% | * | 4.2% | * |

| Tennessee | 12.6% | 19.5% | 21.3% | 1.9% | 8.8% | * | |

| Texas | 25.6% | 30.2% | 33.0% | 2.8% | * | 7.5% | * |

| Utah | 15.4% | 18.2% | 17.8% | -0.4% | 2.4% | * | |

| Vermont | 12.5% | 13.4% | 12.9% | -0.5% | 0.4% | ||

| Virginia | 13.5% | 17.6% | 16.9% | -0.6% | 3.4% | * | |

| Washington | 16.9% | 15.0% | 17.1% | 2.0% | * | 0.2% | |

| West Virginia | 19.3% | 19.0% | 21.0% | 2.0% | 1.7% | ||

| Wisconsin | 10.7% | 11.2% | 13.1% | 1.9% | * | 2.5% | * |

| Wyoming | 18.2% | 18.9% | 19.8% | 0.9% | 1.6% | ||

| Source: Census Bureau historical tables. Note, a ‘*’ indicates that the difference between 2008/2009 and the given year for a particular estimate is statistically significant at the 90 percent confidence level. | |||||||

| APPENDIX TABLE 4: Most of the Uninsured Will Be Eligible for Medicaid or Premium Subsidies | |||||||||

| STATE | OF UNINSURED | NON-ELDERLY UNINSURED (in 1,000’s) | |||||||

| Share | 134% to 400% of Poverty | ||||||||

| Total | Adults | Kids | Total | Adults | Kids | Total | Adults | Kids | |

| NATION | 85% | 85% | 91% | 19,688 | 15,614 | 4,074 | 20,755 | 18,052 | 3,307 |

| Alabama | 82% | 87% | 96% | 308 | 260 | 48 | 240 | 260 | 27 |

| Alaska | 86% | 79% | 85% | 41 | 33 | 9 | 67 | 48 | 12 |

| Arizona | 90% | 84% | 96% | 576 | 416 | 160 | 540 | 404 | 100 |

| Arkansas | 91% | 91% | 94% | 232 | 202 | 30 | 241 | 195 | 46 |

| California | 85% | 85% | 91% | 2,919 | 2,349 | 570 | 3,013 | 2,656 | 437 |

| Colorado | 84% | 82% | 93% | 313 | 234 | 79 | 324 | 273 | 56 |

| Connecticut | 75% | 77% | 81% | 121 | 96 | 25 | 163 | 151 | 21 |

| Delaware | 73% | 82% | 88% | 39 | 27 | 11 | 37 | 41 | 7 |

| DC | 80% | 84% | 91% | 27 | 22 | 4 | 25 | 25 | 3 |

| Florida | 85% | 85% | 91% | 1,615 | 1,227 | 388 | 1,626 | 1,365 | 294 |

| Georgia | 84% | 88% | 92% | 892 | 720 | 171 | 638 | 605 | 113 |

| Hawaii | 80% | 77% | 92% | 39 | 33 | 6 | 39 | 31 | 7 |

| Idaho | 86% | 90% | 92% | 100 | 78 | 22 | 101 | 93 | 17 |

| Illinois | 84% | 83% | 94% | 685 | 541 | 145 | 774 | 680 | 112 |

| Indiana | 84% | 86% | 90% | 327 | 271 | 55 | 365 | 327 | 62 |

| Iowa | 80% | 85% | 93% | 117 | 94 | 23 | 129 | 131 | 18 |

| Kansas | 85% | 89% | 94% | 174 | 130 | 44 | 120 | 111 | 24 |

| Kentucky | 89% | 90% | 92% | 329 | 281 | 48 | 275 | 237 | 48 |

| Louisiana | 90% | 87% | 95% | 360 | 287 | 73 | 340 | 285 | 44 |

| Maine | 79% | 80% | 87% | 37 | 33 | 5 | 67 | 62 | 9 |

| Maryland | 79% | 82% | 87% | 251 | 210 | 42 | 316 | 299 | 42 |

| Massachusetts | 83% | 73% | 77% | 103 | 83 | 20 | 160 | 112 | 19 |

| Michigan | 83% | 84% | 89% | 514 | 437 | 77 | 513 | 482 | 47 |

| Minnesota | 84% | 83% | 93% | 154 | 115 | 38 | 221 | 190 | 36 |

| Mississippi | 93% | 90% | 91% | 241 | 193 | 49 | 225 | 167 | 43 |

| Missouri | 86% | 87% | 91% | 355 | 287 | 68 | 351 | 317 | 49 |

| Montana | 87% | 82% | 96% | 55 | 45 | 11 | 78 | 61 | 14 |

| Nebraska | 85% | 88% | 91% | 81 | 63 | 19 | 94 | 84 | 17 |

| Nevada | 82% | 82% | 91% | 191 | 132 | 59 | 224 | 190 | 48 |

| New Hampshire | 74% | 75% | 73% | 38 | 35 | 3 | 61 | 57 | 6 |

| New Jersey | 77% | 79% | 89% | 430 | 331 | 99 | 539 | 493 | 100 |

| New Mexico | 88% | 86% | 93% | 218 | 167 | 51 | 169 | 137 | 26 |

| New York | 80% | 78% | 87% | 906 | 733 | 173 | 1,267 | 1,099 | 133 |

| North Carolina | 89% | 90% | 93% | 708 | 565 | 143 | 651 | 570 | 104 |

| North Dakota | 87% | 82% | 94% | 25 | 21 | 3 | 37 | 27 | 7 |

| Ohio | 83% | 86% | 94% | 598 | 486 | 112 | 620 | 595 | 89 |

| Oklahoma | 80% | 89% | 93% | 219 | 186 | 33 | 237 | 232 | 59 |

| Oregon | 86% | 88% | 91% | 274 | 221 | 53 | 277 | 249 | 45 |

| Pennsylvania | 78% | 78% | 89% | 435 | 339 | 95 | 572 | 500 | 99 |

| Rhode Island | 81% | 80% | 90% | 46 | 36 | 10 | 53 | 48 | 6 |

| South Carolina | 87% | 85% | 91% | 321 | 253 | 68 | 317 | 245 | 66 |

| South Dakota | 88% | 86% | 94% | 48 | 37 | 11 | 43 | 34 | 8 |

| Tennessee | 93% | 90% | 94% | 448 | 380 | 69 | 422 | 350 | 51 |

| Texas | 88% | 88% | 91% | 2,689 | 2,031 | 659 | 2,724 | 2,244 | 526 |

| Utah | 79% | 80% | 87% | 126 | 82 | 44 | 177 | 146 | 42 |

| Vermont | 76% | 75% | 96% | 15 | 11 | 3 | 29 | 27 | 3 |

| Virginia | 78% | 82% | 85% | 359 | 293 | 67 | 398 | 383 | 58 |

| Washington | 87% | 85% | 92% | 272 | 236 | 36 | 446 | 384 | 56 |

| West Virginia | 90% | 84% | 82% | 108 | 100 | 8 | 125 | 96 | 13 |

| Wisconsin | 84% | 84% | 89% | 184 | 151 | 33 | 254 | 228 | 33 |

| Wyoming | 77% | 81% | 88% | 26 | 21 | 5 | 34 | 32 | 7 |

| Note: Analysis accounts for the five percent income disregard to be used in the Medicaid eligibility determination process. Thus, effectively the income categories are under 139 percent of poverty, and 139 percent to 405 percent of poverty. Children are those aged 0 through 18. Non-elderly adults are those aged 19 through 64. Based on CBPP analysis of Census Bureau data. | |||||||||

End Notes

[1] Arloc Sherman, Danilo Trisi, Robert Greenstein, and Matt Broaddus, “Census Data Show Large Jumps in Poverty and the Ranks of the Uninsured in 2009,” September 17, 2010.

[2] Unless otherwise noted, all estimates are based on Center on Budget and Policy Priorities’ analysis of Census Bureau publications or Census Bureau survey data from the Annual Social and Economic Characteristics’ supplement to the 2010, 2009, 2008, 2001, and 2000 Current Population Surveys. These surveys report on individuals’ health insurance status for the prior year.

[3] Aviva Aron-Dine, Richard Kogan and Chad Stone, “How Robust Was the 2001-2007 Economic Expansion?” Center on Budget and Policy Priorities, updated August 29,2008.

[4] The Center on Budget and Policy Priorities generates annual averages using monthly unemployment rate data from the Bureau of Labor Statistics.

[5] The Kaiser Family Foundation and Health Research and Educational Trust, “Employer Health Benefits: 2010 Annual Survey,” September 2010.

[6] Estimates by the Center on Budget and Policy Priorities based on data from the Bureau of Labor Statistics.

[7] Kaiser Family Foundation, op cit.

[8] Based on analysis of the Census Bureau’s historical series of income data generated from the Current Population Survey.

[9] Kaiser Family Foundation, op cit.

[10] As mentioned, these figures are for those with employer-sponsored coverage. Comparable figures for all non-elderly families, irrespective of health insurance coverage, are as follows: the overall cost burden rose from 4.0 percent to 5.1 percent of family income between 2001 and 2006, and the share of families bearing a “high-cost burden” increased from 14.4 percent to 19.1 percent.

[11] Peter Cunningham, “The Growing Financial Burden of Health Care: National and State Trends, 2001-2006,” Health Affairs, May 2010.

[12] R Brook, et al., “The Effect of Co-insurance on the Health of Adults: Results from the RAND Health Insurance Experiment,” RAND Corporation, 1984.

[13] Kaiser Family Foundation, op cit. Offer rates in 2010 were higher than in 2009, despite the economic downturn. The authors of the survey suggest that this is because a disproportionate share of the firms that closed between 2009 and 2010 didn’t offer health insurance coverage. Generally, the offer rate comparisons by firm size and region have changed little since these data first were gathered in 2007, but the comparisons by industry do not hold in all years of comparable survey data.

[14] Kaiser Family Foundation, op cit.

[15] Health Management Associates and the Kaiser Family Foundation, “Hoping for Economic Recovery, Preparing for Health Reform: A Look at Medicaid Spending, Coverage and Policy Trends,” September 2010.

[16] Health Management Associates, op cit.

[17] Health Management Associates, op cit.

More from the Authors