Maine’s “TABOR II” Repeats Mistakes of Colorado, Endangers Public Services and Business Climate

Summary

Maine’s 2009 ballot initiative, “An Act to Promote Tax Relief” (known as TABOR II), imposes tight restrictions on expenditures for the broad range of state and local services that help support Maine’s economy and quality of life. The spending growth permitted under TABOR does not allow for these services to continue at their current levels. Moreover, TABOR II is set to go into effect before the state is expected to recover from the recession, and so would lock in the cuts in services the state has had to impose because of the recent decline in revenue. TABOR II would undermine state and local services in Maine in much the same way that Colorado experienced under its TABOR. [1] (See appendix on page 12 for a comparison of Maine’s 2006 and 2009 initiatives and Colorado’s TABOR.)

TABOR II, which is almost identical to the TABOR proposal that Maine voters defeated in 2006, would force the state to devote fewer and fewer resources each year to providing public services. Maine would have to cut deeply into the full range of services that people have come to rely on — such as education, health care, prescription drugs, highway and bridge repairs, environmental protection, economic development, and safe streets — at a time when these and other services are needed to enhance the state’s competitive position and serve its aging population. As occurred in Colorado, Maine families might find themselves paying for educational activities, supplies, and even teachers the state could no longer support; more Mainers would likely become uninsured; the possibility of public health emergencies would increase; and companies would find Maine a less hospitable place to do business as infrastructure and education deteriorate.

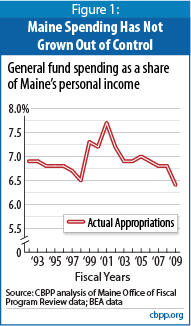

TABOR II proponents claim a rigid TABOR limit is needed to fix what they believe is the state’s tendency toward excessive spending. This claim ignores the state’s experience. For almost two decades, spending has been relatively stable as a share of Mainers’ incomes. And since the enactment in 2005 of “LD1” legislation, which imposes constraints on spending at the state, county, municipal and school district levels, growth in state spending has slowed.[2] In 2009, Maine’s General Fund expenditures equaled 6.4 percent of state personal income, down from 6.9 percent in 1992. Clearly the state has demonstrated fiscal discipline without the rigid restrictions that TABOR II would impose.

- TABOR II relies on the same flawed, rigid formula that Colorado’s TABOR employed, and the effect is likely to be same. Had TABOR II been in effect since 1992 (the year Colorado adopted its TABOR), Maine’s services would have experienced worsening deterioration over time. For example:

- In 2009 alone, the level of services in the General Fund would have been 17 percent lower than it actually was. Stated another way, in 2009 alone the state would have had to make $500 million in cuts beyond the cuts it put in place because of the recession. This amount is equivalent to more than half of the state’s general purpose aid to education in 2009.

- The reductions required by TABOR over the 1992-2009 period would have been equivalent to two years’ worth of Highway Fund spending. Such a reduction would have delayed much needed state efforts to upgrade roads and bridges to improve safety and the overall business environment.

- Under TABOR II, the recent cuts the state has had to make because of the recession would become permanent.

- Under the TABOR formula, if a state spends less than the formula permits in a given year, the following year’s spending growth is based on the state’s actual spending level, not the amount the state could have spent. Thus, as Maine continues to address the effects of the national recession, its 2011 spending level will be below the TABOR limit and therefore would become the basis for any future growth, locking in the reduced level of services.[3]

- Further, although federal stimulus funding under the American Recovery and Reinvestment Act of 2009 (ARRA) is mitigating the impact of the cuts on services, TABOR II does not count such federal funding in determining future spending limits; only the reduced level of state funding constitutes the base for future years. Going forward, Maine’s services would remain at the recession-reduced levels that would have prevailed had there been no federal stimulus to avert the worst of the cuts in services. Such a situation would jeopardize both Maine’s near-term economic recovery and its long-term competitiveness.

- The tax relief TABOR II promises is unlikely to materialize for some Maine residents, and for others it is likely to fall short of what they would lose from weaker public services. TABOR II specifies that the state refund “excess” revenues to income tax filers based on their number of exemptions (unless the legislature acts within a two-week window to specify another method). This would leave out some 60 percent of all seniors, who are not required to file tax returns in part because their Social Security income is exempt from taxation, as well as many other residents.

- Under TABOR II, municipalities, counties, and school districts would be hit by a particularly devastating combination of forces. As state expenditures are squeezed down each year, cuts in state services and assistance would be likely and residents would place increasing pressure on local governments to replace at least some of the needed services the state no longer provides. However, since municipalities and counties also would be subject to the TABOR II formula, localities would be struggling to maintain their own services and generally would not be able to replace reduced state services.[4]

Unlike LD 1, TABOR II would not allow municipal, city, and county revenues to grow in tandem with growth in a community’s tax base, particularly under circumstances when inflation is very low – such as currently – because it limits the LD 1 adjustment for new construction and improvements to the forecasted rate of inflation. Therefore, TABOR II’s greatest impact would be on communities experiencing new residential and commercial development. It would restrict their ability to meet the increased demands for services and infrastructure that such development generates, such as firefighting, public safety, and new streets. - TABOR II would limit the state’s options for maintaining sound fiscal management by allocating fewer resources than Maine currently devotes to rebuilding its budget stabilization fund. This would tie the state’s hands in restoring fiscal stability at a reasonable pace. As a result, the state would be less prepared to address any unforeseen emergency and more vulnerable to future economic shocks, which would add risk and uncertainty to Maine’s economic recovery and long-term stability.

A Solution in Search of a Problem: State Spending Already Falling as Share of Economy

Maine’s spending is not growing faster than the economy or residents’ incomes. Comparing state spending to residents’ personal incomes is the best indicator of a state’s “means” because it measures the ability of state residents and businesses to pay for government services. The cost of services has remained, on average, the same share of their income.[5]

In 1992, the year TABOR was introduced in Colorado, Maine’s spending from the General Fund was 6.9 percent of personal income. Spending has declined modestly over time; in 2009, because of LD 1 and recession-induced reductions, spending dropped to 6.4 percent of personal income. [6] Spending is expected to decline further over the next two years as a consequence of the recession and a moderate increase in incomes.

TABOR’s Flawed Population-Growth-Plus-Inflation Formula

TABOR II (like Maine’s earlier defeated TABOR proposal and Colorado’s TABOR) would allow a small growth in expenditures most years; expenditures could grow by the sum of a) the percentage growth in the state’s overall population averaged over three years and b) the percentage increase in general inflation.[7] Both elements of the formula, however, fail to reflect the cost of maintaining the same level of services year after year, and neither takes into consideration increased participation in existing programs or services caused by demographic shifts or economic circumstances.

The proven result of a TABOR is shrinking public services over time, as happened in Colorado. The deterioration in services so threatened Colorado’s economic climate that residents and businesses banded together to suspend TABOR for five years. (See box on page 6 for a summary of the impact of TABOR on Colorado’s services.) The population-growth-plus-inflation formula would cause similar problems in Maine.

Inflation Measure Does Not Accurately Reflect Government Costs

The measure of inflation in TABOR II is the annual national “Consumer Price Index-All Urban Consumers (CPI-U),” calculated by the U.S. Bureau of Labor Statistics. The CPI-U measures the change in the total cost of a “market basket” of goods and services purchased by a typical urban consumer. Since a typical urban consumer spends a majority of his or her income on housing, transportation, and food and beverages, those items are the primary drivers of the CPI-U.

By contrast, Maine’s state government spends its revenue primarily on education, health care, road and bridge repairs, and corrections. In short, its “market basket” of spending is entirely different.

Indeed, major items in Maine’s “basket of goods” — such as health care, education, and prescription drugs — have seen significantly greater cost increases in the past decade than the items in the basket of goods purchased by consumers, and this pattern is expected to continue. Many of these cost pressures, especially those related to health care, reflect national trends and there is little that Maine can do on its own to control them. Therefore, limiting growth in government spending to a formula based on the general inflation rate is not sufficient to address the normal rate of growth of government costs. A TABOR limitation will, therefore, affect the quantity and/or quality of public services the government is able to provide to its citizens.

The problems with the population-plus-inflation growth formula are described in more detail in a Center on Budget and Policy Priorities paper entitled The Flawed “Population Plus Inflation” Formula: Why TABOR’s Growth Formula Doesn’t Work.

Moreover, the CPI has been quite volatile recently. Volatility in the CPI may be caused by factors that do not much affect the cost of state and local government, such as weather-related changes in the prices of agricultural products or large swings in the price of oil. The consumer price index shot up 4.1 percent in 2007 but grew only 0.1 percent in 2008; forecasts suggest little or no growth for calendar years 2009 and 2010, in part because of the weak economy. Yet the cost of health care and other major components of state budgets will continue to rise for reasons unrelated to the low growth rate of the CPI.

Population Measure Does Not Account for Fast Growth Among Elderly Population

The second part of the population-growth-plus-inflation formula is also inherently flawed. Historically, not all segments of a state’s population increase at the same rate. Often, the segments that are increasing at a greater rate utilize public services more than other parts of the population, which makes a spending formula based on overall population growth even more restrictive. This is true in Maine.

Between 2000 and 2030, for example, Maine’s total population is projected to increase by 11 percent, but its senior population (65 and older) is projected to more than double.[8] As the elderly population increases, so will the cost of maintaining the current level of health care and a range of other services. TABOR II’s state spending limit would not accommodate this emerging need, since it measures growth using the much slower-growing total population figure.

Colorado Services Declined Sharply Under TABOR

A growing body of evidence shows that Colorado’s Taxpayer Bill of Rights, or TABOR, contributed to a significant decline in that state’s public services and business environment. Services had deteriorated to such an extent that Colorado voters chose to suspend TABOR for five years for fiscal years 2006 through 2010, in part to restore some of the service cuts induced by TABOR. Colorado voters also permanently repealed the “ratchet” feature of their TABOR. These developments in Colorado have serious implications for the residents of Maine, because TABOR II would lead to similar outcomes in Maine.

- Since its enactment in 1992, TABOR has contributed to declines in Colorado K-12 education funding. Under TABOR, Colorado declined from 35th to 49th in the nation in K-12 spending as a percentage of personal income, and even under the suspension of TABOR, is now only 48th. And Colorado’s average teacher salary compared to average pay in other occupations declined from 30th to 50th in the nation.

- TABOR has played a major role in the significant cuts made in higher education funding. Under TABOR, higher education funding per resident student dropped by 31 percent, after adjusting for inflation. College and university funding as a share of personal income declined from 35th to 48th in the nation. In 1992, Colorado spent close to the national average on higher education as a share of personal income; by 2004, it spent just 57 percent of the national average. This was particularly harmful to Colorado’s business climate. Bruce Alexander, President and CEO of Vectra Bank Colorado, commenting on a 2005 survey showing that 71 of 100 Colorado business leaders identified TABOR as their top concern said, “[K]ey businesspeople and community leaders tell us . . . [t]hey are looking at the broader issues that will shape the future of Colorado, from the well-being of our higher education centers to the availability of skilled workers as our economy improves.”

- TABOR has led to funding declines for public health programs. Under TABOR, Colorado declined from 23rd to 48th in the nation in the percentage of pregnant women receiving adequate access to prenatal care, as defined by the federal Centers for Disease Control and Prevention. Colorado plummeted from 24th to 50th in the nation in the share of children receiving their full vaccinations. Only by investing additional funds in immunization programs was Colorado able to improve its ranking to 43rd in 2004. At one point, from April 2001 to October 2002, funding was so low that the state suspended its requirement that school children be fully vaccinated against diphtheria, tetanus, and pertussis (whooping cough) because Colorado, unlike other states, could not afford to buy the vaccine.

- TABOR has hindered Colorado’s ability to address the lack of medical insurance coverage for many children and adults in the state. Under TABOR, the share of low-income children lacking health insurance has doubled in Colorado, even as it has fallen in the nation as a whole. Colorado now ranks last among the 50 states on this measure. TABOR has also affected health care for adults. Colorado has fallen from 20th to 48th in the percentage of low-income non-elderly adults covered under health insurance. In 2002, Colorado ranked 49 th in the nation in the percentage of both low-income, non-elderly adults and low-income children covered by Medicaid.

- The business community believes that TABOR harmed the business climate. As Denver Business Journal editor Neil Westergaard observed, “[Business leaders] have figured out that no business would survive if it were run like the TABOR faithful say Colorado should be run—with withering tax support for colleges and universities, under-funded public schools and a future of crumbling roads and bridges.”

Source: David Bradley and Karen Lyons, A Formula for Decline: Lessons from Colorado for States Considering TABOR, Center on Budget and Policy Priorities, October 2005; Aiming for the Middle: Benchmarks for Colorado’s Future, 2009 Updated Rankings, Colorado Fiscal Policy Institute.

Neither does TABOR II’s population growth component take into consideration the impact of changing economic conditions on the use of state services. During an economic downturn, such as the current one, participation can increase in a number of state services — job training, community colleges and state universities (as people who have lost jobs try to gain additional skills), and medical assistance. TABOR II’s spending formula effectively caps expenditures at the levels of participation that prevailed at the time it takes effect.[9] This would force Maine to reduce the quality and quantity of services it provides in future recessions.

TABOR II Would Reduce Wide Range of Services

TABOR II would apply to all state services — those funded out of the General Fund, the Highway Fund, and the Other Special Revenue Fund (OSRF). The annual spending growth limitations would apply separately to the General Fund and to the Highway Fund. Within the OSRF, which consists of a large number of specific dedicated revenue sources used for specific programs, the limitation would apply to each individual program.

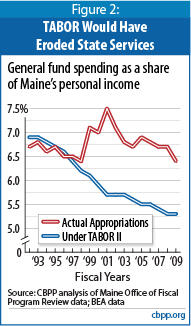

If Maine had enacted TABOR II in 1992, when Colorado adopted its TABOR, by 2009 Maine’s services would have experienced deterioration similar to that in Colorado. Because of the rigid growth formula, Maine would have had to cut general fund services by increasing amounts over the years. General state services would have declined more rapidly and to a greater extent than actually occurred without TABOR. As shown in Figure 2, General Fund expenditures constituted 6.9 percent of personal income in 1992; by 2009 they would have shrunk to just 5.3 percent of income. In 2009 alone, the state would have had to cut $500 million (17 percent) out of the General Fund budget beyond the cuts it actually made to cope with the effects the recession; these additional cuts are equivalent to more than half of the state’s general purpose aid to education.

Since TABOR II’s spending limit applies to the entire General Fund, if one service were to grow faster than the rate allowed under the limit (due to cost pressure, federal mandates, or increased participation, for example), spending for another General Fund service would have to grow slower than the TABOR rate. While TABOR II provides for statewide voter override of the limit or the approval of new taxes, such procedures are costly and cumbersome and generally cannot provide a timely response.

In addition, TABOR II’s limitation on the Highway Fund would devastate the state’s highway program. Had TABOR II been in effect since 1992, by 2009 Maine would have had to forgo the equivalent of more than two years’ worth of spending.[10] Since the Highway Fund is predominately focused on bridge and road maintenance, these programs would have had to absorb the reduction.

Many roads and bridges would have remained in need of resurfacing and repair. Even without TABOR II, Maine reported in 2006 that 36 percent of its major roads — comprising almost 60 percent of the state’s highway network — were rated either poor or critical; conditions would have been much worse if two years’ of spending had been removed from the program.[11] This clearly would have hampered efforts to improve highway safety and attract new development.

As noted above, the TABOR growth formula would apply to each individual program within the Other Special Revenue Fund. Many of these programs are funded by dedicated revenues from the constituency the program serves. They include a number of health-related programs, such as nursing facilities and medical services, and several environmental programs, among others.

TABOR II would limit spending growth of these special revenues according to the basic TABOR formula; no consideration would be given to a program’s growth characteristics or expenditure pattern. Even if dedicated revenues were sufficient to pay for the specified program, no expenditures could be made beyond what the rigid TABOR limit allowed. In addition, the state would have to refund any revenues that exceeded allowed expenditures by more than 10 percent; it could not keep these revenues to use in a future year.

The environmental funds demonstrate how dysfunctional it would be to apply the TABOR limit to each individual program in the OSRF. For example, the Bureau of Remediation and Waste Management receives revenues that in effect create an “insurance” pool enabling the state to respond to catastrophic environmental and health hazards. Expenses depend on the frequency of accidents, and monies remain in the fund until they are needed. Restricting growth to some annual growth rate based on the prior year’s expenditures, as TABOR II would require, would leave the state with insufficient resources when an accident does occur — since any one year with a low accident rate would create a base that restricted the size of the fund for all future years. Moreover, TABOR’s requirement that the state refund unexpended monies would prevent it from carrying over funds from years with few or no accidents. In short, TABOR II would make it impossible to maintain this type of environmental insurance pool.

“Ratchet” Would Lock in Effects of Recession

The problems associated with TABOR II’s rigid formula are compounded when the actual spending level for a given year is below the level the formula permits. Under TABOR II, annual spending growth would be based on the prior year’s actual spending level or the spending level permitted by the formula for that year, whichever is lower. Any time actual expenditures are lower than permitted expenditures, the lower actual level becomes the base for spending growth in future years. This is likely to occur during a recession, when the state has to cut its spending. As a result, under TABOR II Maine could never restore services to their pre-recession levels. Services would be permanently “ratcheted down” to a lower level.

As explained above, TABOR’s population-plus-inflation formula does not allow even the maintenance of the base level of services. But even if it did, the reduction of the base through the “ratchet effect” would mean a permanent reduction in services.

Colorado’s experience demonstrates the harmful impact of TABOR’s ratchet effect. The recession of the early 2000s necessitated a sharp reduction in services as revenues dropped. Colorado could not restore those services when its economy recovered because of the ratchet; TABOR would have permanently limited the state to recession-level services. Residents and businesses alike found that situation untenable, and in 2005 voters permanently eliminated the element of the TABOR formula that created the ratchet effect. They also suspended the TABOR formula for five years to allow services to recover as the economy recovered.

If Maine were to adopt TABOR II this year, during a recession, the ratchet would operate immediately and prevent recovery from the reduced service levels. The state adopted its biennium budget for 2010 and 2011 (this year and next) in the midst of the recession, and the budget imposes significant spending reductions in both years. In 2011, the first year TABOR II would be operational if voters approve it this fall, actual expenditures would be lower than expenditures permitted under TABOR II. The spending base for future years would therefore be ratcheted down to this lower level, preventing the state from reversing the cuts it had to make during the recession.

Moreover, while federal stimulus funding is mitigating the impact on services of Maine’s spending cuts for 2010 and 2011, the TABOR II formula does not take federal funding into account; the state’s future spending limits would be based on state spending alone. [12] This would impair both Maine’s near-term economic recovery and its long-run competitiveness.

TABOR Would Affect Municipalities, School Districts, and Counties

Under TABOR II, local services provided by municipalities, school districts, and counties would be hit by a combination of forces that would be particularly devastating. As state expenditures for services are squeezed down each year by the rigid formula, cuts in state assistance would be likely. In addition, pressure would increase at the local level to replace some of the reduced state services.

TABOR II proponents argue that the measure would not affect education. This is not accurate. Although TABOR II does not apply any spending limitations to school districts, it could have a big impact on state aid to education, which makes up half of schools’ funding for essential services.

In the current biennium, federal stimulus funds are mitigating the deep reductions the state had to make in education aid, but (as noted above) TABOR II would not count those federal funds in the base for future expenditure limits. Therefore, for purposes of TABOR II, state aid would be starting 10 percent below the prior year’s level of aid. Given the competition from other services funded through the General Fund, Maine would be highly unlikely to provide enough additional school aid under TABOR II to restore state funding to the pre-recession level. School districts would have difficulty replacing the reduced state aid with local funding.

Municipal and county governments would face additional limitations under TABOR II. The TABOR II formula restricts the growth of local expenditures to the increase in income plus forecasted inflation.[13] (The LD1 spending limit permits communities to benefit from growth attributed to new development or expansion. TABOR II would restrict the property growth factor to the rate of inflation.) Communities experiencing residential and commercial development would be particularly hard hit. It is unlikely, particularly in the current economic environment, that they would be able under TABOR II to address the increased demands for services and infrastructure, such as fire protection, public safety, and new streets.

TABOR II Would Force Irresponsible Fiscal Management

TABOR II’s supporters claim that it “creates a rainy day fund and forces the state and local governments to set aside a portion of surplus revenue in order to fund it.”[14] But Maine already has a budget stabilization fund (BSF) with a maximum funding level of 12 percent of revenues, the same level that TABOR II specifies. So TABOR II would not create anything new. In fact, TABOR II would make the stabilization fund less effective by restricting how quickly the state can replenish it.

The stabilization fund has been critical in helping Maine withstand sudden economic shocks. When the recession and ensuing state fiscal crisis hit in the early 2000s, Maine was able to draw on the fund to help support needed services. And since the state was able to partially restore those spent funds before the current recession hit, funds were available to ease the impact of the current economic downturn.

TABOR II, however, would permit the state to use only 20 percent of its revenues in excess of the spending limit to rebuild the fund. As a result, reserves would be built up at a much slower rate than under current law, which requires 35 percent of excess funds to go to the stabilization fund. [15] This would leave Maine less well equipped to deal with future shortfalls.

Tax Relief for Whom? Many Mainers Would Miss Tax Refunds

TABOR II’s tax relief program, under which 80 percent of the revenues above the spending limit would go to tax refunds, suffers from several serious problems.

First, the “excess” revenue must be refunded in all circumstances, even if the state is being forced to cut spending. For example, if revenues exceed the TABOR limit in one year but fall short of the limit in the next year — because the economy is in decline, an enacted tax cut cost more than expected, or for some other reason — Maine would have to send out tax refunds based on the prior year’s results even as it cut expenditures for the current year. This happened in Colorado. Such rigidity undermines prudent management of a state.

Second, TABOR II fails to distribute tax refunds fairly. The proposal sets out a very strict timeline for implementing tax refunds; if the legislature does not act between September 1 and September 15 to determine how the refunds would be made (given this limited window, it may not be able to act), refunds based on General Fund revenues would go to people who had filed Maine personal income tax returns for the previous year. Certain segments of the population are not required to file income tax returns, though, and thus would not benefit from any refunds. This is particularly true for senior citizens who are living largely on Social Security. More than 60 percent of senior households are not required to file and so would receive no tax relief.[16]

Moreover, many residents who do receive refunds may find that they are quite modest compared to the losses caused by cuts in state services, such as elimination of health coverage, additional school fees, or higher tuition. Many Colorado families experienced this under their state’s TABOR. So while proponents describe TABOR II as a “tax relief” measure, it would likely have a much broader impact on services than on tax relief.

Conclusion

Maine’s TABOR II proposal contains the core features of the proposal Mainers rejected in 2006 and of Colorado’s TABOR. Like Colorado, Maine would experience large declines in the quality and quantity of public services under TABOR II because of its strict population-growth-and-inflation limit combined with its “ratchet” feature.

Maine’s expenditures have declined over time relative to residents’ incomes even without TABOR, and LD1 — the limit already in place — will prevent high future growth. The rigid limit in TABOR II goes too far. It would prevent the state from restoring cuts made during the recession and from making adequate investments in education, health care, environmental quality, and infrastructure. The decline in services would hamper efforts to improve the state’s business climate and competitiveness, as Colorado experienced under its own TABOR. The impact would be even larger in Maine since TABOR II would take effect at the lowest point in state spending in a number of years.

| APPENDIX: | |||

|

| Maine TABOR (2006) | Maine TABOR II (2009) | Colorado TABOR, |

| Focus of growth limit | Appropriations | Appropriations | Revenues |

| Expenditures subject to limitations | General Fund, Highway Fund, Other Special Revenue Fund and Quasi-governmental agencies, for which separate limitations must be applied | General Fund, Highway Fund, Other Special Revenue Fund, by each program | General Fund |

| Base for growth for State expenditures | Lower of level imposed by limit or prior year’s appropriation | Lower of level imposed by limit or prior year’s appropriation | Lower of level imposed by limit or actual revenues |

| Formula | “Inflation adjustment factor” (increase in CPI for the most recent calendar year) PLUS “Population adjustment factor (increase or decrease in population for the preceding calendar year as determined by State Planning Office based on census) AND Any revenue increases approved by 2/3 vote of each House of the Legislature and approved by the voters | “Inflation adjustment factor” (increase in CPI for the most recent calendar year) PLUS “Population adjustment factor (average annual percentage increase in population for the three most recent years for which data is (sic) available as determined annually by the Executive Department, State Planning Office statewide based on federal census estimates) Inflation adjustment factor and Population adjustment factor would not be included if it were less than zero AND Any increases attributable to revenue increases approved by majority vote of each House of the Legislature and approved by the voters | Inflation measured by CPI for the Denver-Boulder-Greeley area PLUS Percentage change in State Population in the prior calendar year Also voter approved increases |

| Approvals for increases | Spending above the limit and any tax increase: 2/3 of all members of each house AND majority of voters | Spending above the limit and any tax increase: Majority of all members of each house AND majority of voters in next election | Majority of all members of each house AND majority of voters in next election |

| Use of excess revenues | 80% Tax Relief Fund 20% Budget Stabilization for General and Highway Funds For each agency that manages an Other Special Revenue Fund account, uncommitted revenues in excess of 10% of prior year’s expenditures, submit a plan to refund | 80% Tax Relief Fund 20% Budget Stabilization for General and Highway Funds For each agency that manages an Other Special Revenue Fund account, uncommitted revenues in excess of 10% of prior year’s expenditures, submit a plan to refund | Tax refunds |

| Cap on budget | 10% of Revenues | 12% of Revenues | Cap on budget |

| Tax refunds | If excess funds exceed $25 million, legislature shall provide refunds by October 15. | If excess funds exceed 1% of fund revenues, legislature shall provide refunds by September 15. If legislature does not act, refunds based on filing income tax returns by October 15 with refund based on number of exemptions claimed in income taxes filed for the previous tax year | Paid the following year |

| Tax increase | Any measure that results in a tax increase must be approved by AND Approval of the voters | Any measure that results in tax increase must be approved by majority vote of each House of the Legislature AND Approval of the voters | |

| Local Governments | |||

| Local governments included | Municipalities | Municipalities Counties | All local governments |

| Formula components | For Municipalities and Counties: OR Inflation plus Population, PLUS Student enrollment | 10 year average real personal income growth and forecasted inflation | Inflation PLUS Value of all real property PLUS Student enrollment |

| Override authority | Referendum election | Referendum election | Referendum election |

End Notes

[1] “An Act to Provide Tax Relief” has qualified for the November 2009 ballot. Unlike Colorado's TABOR, Maine's proposal is statutory rather than constitutional. Maine does not permit constitutional amendments by initiative. Nevertheless, while legislators have the power to override an initiated bill it is politically difficult and risky to do so. Moreover, the proponents of the TABOR initiative in Maine have declared clearly their intention to use the initiative as only the first step toward persuading the next legislature to adopt a constitutional provision.

[2] LD 1: An act to increase the State Share of Education Costs, Reduce Property Taxes and Reduce Government Spending at All Level (Public Law 2005, Chapter 2), is intended to lower Maine’s state and local tax burden by restricting growth in spending. For the state, the growth limit, applied to the General Fund appropriations, is the ten-year average personal income growth (but not more than 2.75%) plus the ten-year average annual growth rate of Maine’s population. An allowance is provided for additional funding of the state’s General Purpose Aid for Education, up to the point at which such aid covers 55% of covered costs. For the current biennium, FY 10 and FY 2011, the growth limitation for each year is 2.76% of prior year’s base amount. Under LD 1, each year’s limit is based on the previous year’s limit, adjusted for the permitted growth factor. This gives the state the opportunity to restore services to their prior level after a recession, but prevents growth beyond that prior level adjusted for population and personal income growth.

[3] Because of the continued effects of the national recession, the appropriation levels for the General Fund and Highway Fund for 2011 are below the 2010 levels in the adopted biennium budget for 2010 and 2011. Therefore, the lower 2011 levels would be the base for measuring future growth under TABOR II.

[4] The formula that would apply to local governments under TABOR II is different than the one that applies to the state. TABOR II would tighten the LD 1 formula, which uses a 10-year average of real personal income growth plus an allowance for new construction and improvements, by limiting the allowance for new construction and improvements to forecasted inflation.

[5] The size of the “economy” is typically measured by Gross Domestic Product for the U.S. as a whole or by total personal income for individual states. State personal income is the sum of wage and salaries, proprietors’ income, rental income, personal dividend income, personal interest income, and personal current transfer receipts received by all individuals residing in a state. The measure is computed quarterly and annually by the U.S. Bureau of Economic Analysis.

[6] A similar trend is seen with all state governmental fund expenditures, which equaled 9.9 percent of personal income in 1992 and 9.7 percent of personal income in 2008.

[7] The formula for state expenditures in TABOR II would not incorporate negative growth in inflation or growth less average population change.

[8] U.S. Census Bureau, State Interim Population Projections by Age and Sex: 2004-2030, Table 4. Available at http://www.census.gov/population/projections/PressTab4.xls.

[9] In the current recession, federal funds are paying for all or most of the increased participation in Medicaid and education. As explained below, however, these federal funds would not be counted in the base expenditures against which the TABOR formula is applied. In a future recession, state funds could not expand to meet increased need.

[10] The TABOR II formula was applied to the appropriation for Highway Fund from Fiscal Year 1992 through 2009. The level of funding under TABOR II was compared to actual appropriations, with the difference between the two being $631 million less under TABOR for the entire period. In as much as the average annual appropriation for the Highway Fund between 1992 and 2009 was $269 million, TABOR II would have resulted in reducing the funding the Highway Fund by more than 2 years’ funding.

[11] Maine Department of Transportation Highway Adequacy 2006 Interim Report, prepared by the Bureau of Planning, Maine DOT, August 2006.

[12] Maine used the federal stimulus funds as intended, to offset some of the state cuts. Despite those state cuts, therefore, state services in 2010 were about level with the prior year, and in 2011 Maine projects that services (funded from both state and federal stimulus sources) will be only about 2 percent below the pre-recession level.

[13] Under the current limitation, LD1, as long as the state’s state and local tax burden ranks in the highest 1/3 of all states, for municipal and county governments the growth of property tax levy limit is the income growth factor (statewide average 10-year real personal income growth) plus the increase in assessed valuation as a result of improvements to or expansion of the property or properties that are being taxed for the first time. TABOR II incorporates the same definition of income, but eliminated the growth attributed to new development and substitutes inflation.

[14] Becker, “TABOR Puts Taxpayers in Charge,” ibid.

[15] LD 1 provides that excess General Fund revenues, over the accepted estimates would be distributed in the following priority order: State contingency account, up to $350,000; Loan Insurance Reserve up to $1 million, to Maine Budget Stabilization Fund, 35 percent; to Retirement Allowance Fund, 20 percent; to Working Capital Reserve, 20 percent; Retiree Health Ins. Service Fund, 15 percent; Capital Construction and Improvement Reserve Fund, 10 percent.

[16] CBPP analysis of the Census Bureau's 2007 American Community Survey , identifying elderly tax filing units (where the would-be filer or spouse is age 65 or older), whose adjusted taxable income in 2007 was less than the $2,000 threshold for filing. Adjusted taxable income was calculated net of the appropriate standard deduction and personal exemptions, with income adjusted to exclude Social Security, SSI, and public assistance for the tax unit.

More from the Authors