GAO Study Again Confirms Health Savings Accounts Primarily Benefit High-Income Individuals

A new Government Accountability Office (GAO) report indicates that Health Savings Accounts are used disproportionately by affluent households. Its findings also suggest that HSAs are being used extensively as tax shelters.[1]

What Are Health Savings Accounts and Why Are They Attractive as Tax Shelters?

Established by the 2003 Medicare drug legislation, Health Savings Accounts (HSAs) are accounts in which individuals with a high-deductible health insurance policy can save money to pay for out-of-pocket health expenses. In tax year 2008, someone who enrolls in a health plan with a deductible of at least $1,100 for individual coverage and $2,200 for family coverage may establish an HSA.

HSA contributions are tax deductible. In 2008, individuals may contribute up to $2,900 for individual coverage and $5,800 for family coverage. These tax-preferred contributions may be placed in stocks, bonds, or other investment vehicles, with the earnings accruing tax free. Withdrawals also are tax exempt if used for out-of-pocket medical costs.

HSAs thus have a unique tax structure. No other savings vehicle in the federal tax code offers both tax-deductible contributions and tax-free withdrawals, as HSAs do. Moreover, because the value of a tax deduction rises with an individual’s tax bracket, HSAs provide the largest tax benefits to high-income individuals. In addition, higher-income individuals generally can afford to contribute more money into HSAs each year than lower-income people. And since there are no income limits on HSA participation, very affluent individuals whose incomes who are too high for them to qualify for IRA tax breaks, or who have “maxed out” their 401(k) contributions, can use HSAs to shelter additional funds.

As a result, many health and tax policy analysts have warned that HSAs are likely to be used extensively as tax shelters by high-income individuals. The Bush Administration and other HSA proponents have repeatedly dismissed this concern and argued that HSAs will not have such effects.

What the GAO Report Shows About HSA Use

In 2006, the GAO issued a groundbreaking study analyzing, for the first time, data from the Internal Revenue Service on all Americans who made HSA contributions in tax year 2004.[2] The study also examined three large employers who offered HSA-eligible high deductible plans, as well as data on enrollment in HSA-eligible plans from several national surveys of employers. In that report, the GAO determined that tax filers who make contributions to HSAs were disproportionately high-income individuals, and that among HSA users, those with high incomes made the largest contributions and received the largest tax benefits. The GAO also found initial indications that HSAs are being used as tax shelters.[3]

The GAO’s new report on the use of Health Savings Accounts examines IRS data for tax year 2005, as well as employer surveys. The findings bolster those from the GAO’s earlier study.[4] The new report’s principal findings include:

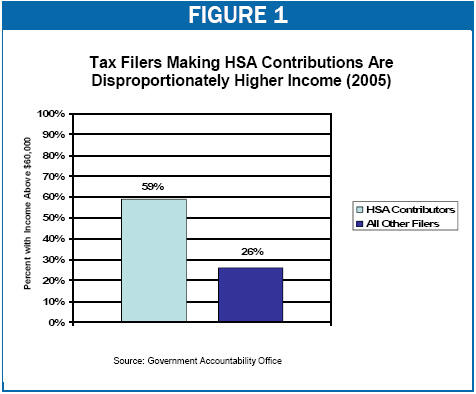

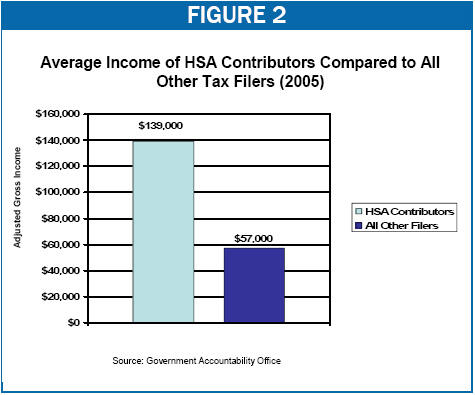

- HSA participants are disproportionately high-income. In tax year 2005, some 59 percent of tax filers making HSA contributions[5] had adjusted gross income of $60,000 or more, even though only 26 percent of all other adult tax filers under age 65 had incomes this large (see Figure 1). At the other end of the income scale, people with adjusted gross income of less than $30,000 made up 50 percent of all other tax filers in 2005 but only 15 percent of all HSA participants.[6] The average adjusted gross income of tax filers who made HSA contributions in 2005 was $139,000, as compared to $57,000 for all other tax filers under age 65 (see Figure 2).

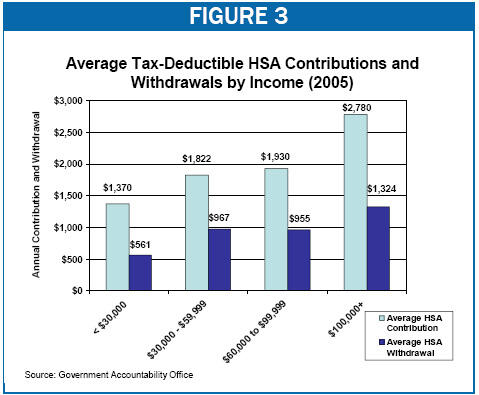

- Affluent HSA participants contribute much more to the accounts than other participants. HSA participants with incomes over $100,000 contributed an average of $2,780 to their accounts in 2005, as compared to an average contribution of $1,370 for HSA participants with incomes below $30,000 (see Figure 3). The fact that higher-income individuals not only are more likely to have HSAs but also contribute more to their accounts further skews the tax benefits of HSAs to high-income households, as does the fact that the higher one’s tax bracket, the greater the subsidy that HSAs provide.

-

Many HSA participants appear to be using their accounts purely or primarily as a tax shelter rather than paying for out-of-pocket health care costs. The GAO found that a stunning 41 percent of tax filers reporting HSA contributions in 2005 did not withdraw any funds from their accounts at any time during the year.[7] In recent Congressional testimony, the GAO stated that this was consistent with the view held by industry experts that many HSA users are people who primarily use their HSAs as a tax-advantaged savings vehicle.[8]

Overall, the average HSA contribution in 2005 was $2,100, more than double the average HSA withdrawal of $1,000. As one would expect, tax filers with incomes over $100,000 had the largest net contributions to their HSA contributions, contributing an average of $2,780 and withdrawing an average of $1,324 in 2005, for a net increase in their HSA balance of $1,456 (see Figure 3).

- Many employers offering high-deductible health insurance plans and HSAs did not contribute to their workers’ HSAs. The GAO reported that a series of employer surveys conducted in 2005, 2006 and 2007 found that more than one-third of large employers offering HSA-eligible plans made no contribution to their employees’ HSAs. GAO also cited another survey finding that nearly half of small and large employers offering high-deductible plans made no HSA contributions for their employees in 2007. This may mean that some lower-income workers who cannot make substantial HSA contributions on their own, and whose employers make no contributions on their behalf, may be unable to afford the high deductibles required under HSA-eligible plans when they or their families need health care.

Health and tax policy analysts have long warned that HSAs could be used extensively as tax shelters by high-income individuals. The GAO’s latest analysis of HSAs again lends strong credence to these concerns.

End Notes

[1] Government Accountability Office, “Health Savings Accounts: Participation Increased and Was More Common among Individuals with Higher Incomes,” April 1, 2008.

[2] Government Accountability Office, “Consumer-Directed Health Plans: Early Enrollee Experiences with Health Savings Accounts and Eligible Health Plans,” August 8, 2006.

[3] See Government Accountability Office (2006), op cit and Edwin Park and Robert Greenstein, “GAO Study Confirms Health Savings Accounts Primarily Benefit High-Income Taxpayers,” Center on Budget and Policy Priorities, September 20, 2006.

[4] Government Accountability Office (2008), op cit.

[5] Contributions include those made by individual tax filers as well as those made by employers or other individuals on their behalf, but do not include funds transferred from Medical Savings Accounts, precursors to Health Savings Accounts that are established as part of a demonstration project in 1996.

[6] It is likely that there are a number of individuals in this income range who may be enrolled in HSA-eligible high-deductible health plans but have not established or contributed to a HSA. According to GAO’s examination of employer surveys, more than 40 percent of individuals enrolled in a high-deductible health insurance plan eligible for a HSA did not open an HSA. Reasons cited by survey respondents included lack of information, lack of need and a belief that they could not afford to put money in the accounts. Government Accountability Office (2008), op cit.

[7] Health policy analysts and economists have expressed significant concern that high-deductible plans attached to HSAs risk “adverse selection.” Adverse selection occurs when healthy and less-healthy individuals separate into different health insurance arrangements, and the average cost of insurance for the less-healthy group rises significantly, because these people are no longer being pooled with healthier individuals who are less expensive to insure. When that occurs, premium costs for the less-healthy can rise sufficiently high that those individuals are put at risk of becoming uninsured or underinsured.

High deductible plans attached to HSAs are likely to be disproportionately attractive to healthier individuals who do not need much health care and thus are less concerned about the higher out-of-pocket costs that can result under a high-deductible plan in comparison to a more traditional lower-deductible plan. If healthier individuals move to HSA-eligible plans in large numbers over time while less healthy individuals remain in traditional plans, that could drive up health insurance premiums for the more traditional plans and make them increasingly unaffordable over time. The fact that a large proportion of individuals contributing to HSAs make no withdrawals may indicate not only that these individuals are using HSAs as tax shelters but also that they may be healthier, on average, and therefore have less utilization of health care services. This deepens the concern over adverse selection. For a discussion of why Health Savings Accounts may spur adverse selection, see Edwin Park and Robert Greenstein, “Latest Enrollment Data Still Fail to Dispel Concerns About Health Savings Accounts,” Center on Budget and Policy Priorities, Revised January 30, 2006.

[8] John Dicken, “Health Savings Accounts: Participation Grew, and Many HSA-Eligible Plan Enrollees Did Not Open HSAs while Individuals Who Did Had Higher Incomes,” Testimony before the Subcommittee on Health, House Ways and Means Committee, Government Accountability Office, May 14, 2008. The GAO also noted that only 22 percent of tax filers making HSA contributions withdrew as much or more than their reported contributions. According to the GAO, industry experts viewed this minority population as consistent with HSA account holders who are “spenders” and who actually use these accounts to pay for out-of-pocket health care costs, rather than as a tax-preferred savings vehicle.

More from the Authors