Impact of Estate Tax on Small Businesses and Farms Is Minimal

Almost No Small Business and Farm Estates Owe the Tax; Those That Do Owe Only Modest Amounts

Congress is expected to debate permanent changes in the estate tax in coming months. A key issue in that policy debate is likely to be the effect of the estate tax on estates containing small businesses and family-owned farms.[1] Some proponents of repealing or weakening the estate tax beyond its current form claim that doing is so is necessary because of the impact of the tax on small business and farm estates.[2] Yet if the 2009 estate tax parameters were made permanent, almost no small business and farm estates would owe any estate tax: just 140 such estates in the entire nation would be taxable in 2011, and virtually none of them would have to be liquidated to pay the tax.

Almost no small farms and businesses owe any estate tax

The vast majority of small business and small farm estates already escape the estate tax.

-

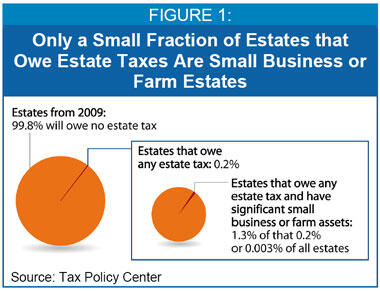

The Tax Policy Center estimates that fewer than 0.2 percent of all estates — two of every 1,000 — will be subject to tax in 2009.[3]

-

Moreover, only about 1.3 percent of the tiny fraction of estates that are taxable are small business or farm estates — that is, estates in which a small business or farm that is valued at up to $5 million makes up the majority of the estate (see Figure 1).

-

This means that only 0.003 percent of all estates — that is, the estates of three out of every 100,000 people who die this year — will be small business or farm estates that owe any estate tax.

The tiny number of small farms and business estates that owe any estate tax owe a modest amount.

The tiny number small farms and small-business estates that do owe estate tax generally owe a very small percentage of the estate’s value in tax.

-

The very few small farm and small-business estates that will owe any estate tax from deaths in 2009 will face a tax that, on average, equals only one seventh (14.3 percent) of the value of the estate.[4]

-

This is below the average for all taxable estates. Taxable estates as a whole will owe tax equal to an average of 19.4 percent of the value of the estate, still less than one fifth of an estate’s value.

-

There are several reasons why those few small businesses and farm estates that are taxable pay such low effective tax rates. First, the fact that the first $3.5 million of any estate is entirely exempt from estate tax — $7 million for a couple — generally protects a large share of the value of small-business and small farm estates.[5] Second, the law contains a number of special estate tax provisions that are targeted to small business and small farms estates and allow them to reduce significantly the amount of tax they owe.[6] (See the box on page 4 below)

There is no evidence that the tiny number of small farms and business estates that owe any estate tax face liquidity constraints.

Proponents of repealing or eviscerating the estate tax often claim that it causes small businesses and farms to be liquidated. This claim is groundless.

-

Opponents of the estate tax have not been able to produce a single case in which a family farm had to be sold to pay the tax. In 2001, the American Farm Bureau Federation acknowledged to the New York Times that it could not cite a single example of a farm having to be sold to pay estate taxes, and this was before the estate tax exemption level was more than tripled and the top rate was reduced.[7]

-

Furthermore, a Congressional Budget Office study of the estate tax exploded the myth that small businesses and farms have to be liquidated to pay the tax. CBO found that of the very few farms estates that would owe any tax under the 2009 parameters, all but a handful would have sufficient liquid assets on hand (such as bank accounts, stocks, and bonds) to pay the tax without having to touch the farm or business.[8]

-

CBO further noted that it may have overestimated the number of small businesses and farm estates with any seeming liquidity constraints, because CBO was unable to include certain assets held in trusts — such as life insurance trusts — in calculating the liquid assets available to estates to help pay the tax.[9] And, those few small businesses and farm estates that might conceivably face a liquidity problem would have other options available to them — such as spreading their estate tax payments over a 14-year period — that would allow them to pay the tax without having to sell off any of the business or farm assets. (See box on page 4 below)

Additional preferences for small farm and business estates are unnecessary and may even harm farm and small business owners

Despite the fact that only a tiny number of small business and farm estates face the estate tax, and despite the lack of evidence that those estates face serious liquidity constraints, proposals are likely to emerge in Congress this year to expand the current, generous estate tax preferences for small businesses and farms. Such measures may be portrayed by their sponsors as being both modest and necessary. Yet such proposals could be extremely costly, because they could create lucrative opportunities for wealthy individuals who are not small business or farm proprietors to shift large amounts of their assets late in life to businesses or farm property in order to escape the estate tax.[10]

Such proposals thus could end up being exploited by clever tax attorneys and accountants at the expense of the federal Treasury, open up large, unintended loopholes, and even harm farm and small business owners. The dangers of such proposals are illustrated by a recent Tax Policy Center analysis of a proposed measure to exempt farmland from the estate tax:[11]

Farm and small business estates enjoy existing protections

Under current estate tax law, farm estates benefit from four forms of targeted estate tax relief.

- Special use valuation. This year’s $7 million per-couple estate tax exemption really amounts to a nearly $9 million exemption for farm couples. Each member of a farm couple is allowed to reduce the value of farmland and certain other assets in their estate by up to $960,000 in 2008 (indexed for inflation) through a provision that allows farmers to value these assets based on their current use (farming) rather than on their most profitable use. According to a leading study of this matter conducted by USDA economists during the Bush administration, special use valuation can reduce the value assigned to the component of farm estates that consists of real property (as distinguished from the part that consists of financial assets) by 40 to 70 percent of the market value of those assets.*

- Payment of tax extended over 14 years. Farm and small business estates are generally eligible to defer payment of estate tax (paying only interest) for five years and then may pay the tax in up to ten annual installments.** The first $1.33 million in estate tax is subject to an interest rate of only 2 percent. In addition, the interest rate on the remainder owed is still only 45 percent of the rate generally levied on late tax payments. This provision prevents farmers with large estates but few liquid assets from having to sell their farms to pay the estate tax.

- Conservation easements. Farmers may deduct from the value of the estate up to 40 percent of the value of land subject to a qualified conservation easement. (A conservation easement is essentially an enforceable promise not to develop the land for uses other than farming; typically, conservation easements are donated to environmental groups or municipalities.)

- Minority interests and marketability discounts. Estate tax law allows a lower valuation for property that is held by multiple heirs, each of whom has a minority interest, or that is otherwise difficult to sell. Farm and small business estates are especially likely to qualify for these discounts. According to the Congressional Budget Office, minority discounts reduced the taxable value of undeveloped land and farmland for which these discounts were claimed by an average of 51 percent in 2000.***

* Ron Durst, James Monke and Douglas Maxwell, “How Will the Phaseout of Federal Estate Taxes Affect Farmers?” USDA Agriculture Information Bulletin No. 751-02, February 2002. http://www.ers.usda.gov/publications/aib751/aib751-02/aib751-02.pdf.

** Generally estates that are required to file a return must do so within nine months of the death; this provision allows qualifying estates to spread payment of any tax owing over an additional 14 years.

*** Congressional Budget Office, “Effects of the Federal Estate Tax on Farms and Small Businesses.”

-

The Tax Policy Center concluded that "an unlimited exemption for farm assets could create a giant loophole from the estate tax" because wealthy individuals who expect to owe estate tax could use much or all of their wealth to buy farms before they died. A special preference such as this would "make the estate tax essentially voluntary for the very wealthy," because "the wealthiest people would have a strong incentive to convert most of their assets into qualifying farms, and thus skirt the estate tax."

-

TPC also noted that, “Ironically, this could endanger many existing small farms, as wealthy people would bid up the price of such properties to claim their tax benefits. (How much of Iowa could Bill Gates buy with his fortune?).”

-

In addition, TPC pointed out that such preferences can have adverse economic consequences because, “it is unlikely that a billionaire’s heirs holding tens of thousands of acres of farmland for tax purposes would manage the resources as effectively as the professional farmers they would displace….and how committed would the heirs be to continuing to farm the land (rather than develop it) after the required holding period expires?"

-

Finally, the Tax Policy Center warned that although some versions of this proposal include measures intended to limit the limit the potential for estate-tax avoidance, it is unclear that such measures would be effective.

These risks are avoidable because additional measures to enlarge special estate-tax preference for farms and other small businesses are not needed. As the foregoing discussion illustrates and the data cited above demonstrate, small business and farm estates already are very well protected under the 2009 estate-tax parameters and the current estate-tax preferences for small businesses and farms.

Conclusion

The effect of the estate tax on small businesses and farms does not justify weakening the estate tax beyond its current form or creating additional preferences for small business and farm estates. Only a tiny number of small business and farm estates currently face the estate tax, those that do generally face a low effective tax rate, and there is no evidence that those estates face liquidity constraints. Moreover, further special preferences for such estates could open up loopholes that would drain the Treasury and possibly even harm small businesses and farms.

End Notes:

[1] We follow the Tax Policy Center definition of a small business or small farm estate. TPC defines such an estate as one in which more than half of the value of the estate is in a farm or business and the farm or business assets are valued at less than $5 million.

[2] For a detailed discussion on why repealing the estate tax or weakening it beyond its current form would be unnecessary and fiscally responsible, see Chye-Ching Huang, “Congress Should Not Weaken Estate Tax Beyond its 2009 Parameters", Center on Budget and Policy Priorities, January 27, 2009.

[3] Leonard E. Burman, Katherine Lim, and Jeffrey Rohaly, “Back from the Grave: Revenue and Distributional Effects of Reforming the Federal Estate Tax,” Urban Brookings Tax Policy Center, October 20, 2008.

[4] Urban Institute and Brookings Institution Tax Policy Center estimates. The average effective tax rate falls far below the 45 percent top marginal estate tax rate, primarily because of the tax’s $3.5 million exemption (effectively $7 million per couple).

[5] Urban Institute and Brookings Institution Tax Policy Center

[6] The provisions targeted to small business and farm estates include the qualified family-owned business-interest deduction, valuation of assets based on current use, minority discounts, and the payment of estate taxes owed over 15 years.

[7] David Cay Johnston, “Talk of Lost Farms Reflects Muddle of Estate Tax Debate,” New York Times, April 8, 2001.

[8] Congressional Budget Office, “Effects of the Federal Estate Tax on Farms and Small Businesses,” July 2005.

[9] Congressional Budget Office, “Effects of the Federal Estate Tax on Farms and Small Businesses,” July 2005.

[10] Aviva Aron-Dine, "An Unlimited Estate Tax Exemption For Farmland Unnecessary, Open to Abuse, and Likely to Hurt, Rather than Help, Family Farmers," Center on Budget and Policy Priorities, October 1, 2007.

[11] Leonard E. Burman, Katherine Lim, and Jeff Rohaly, "Back from the Grave: Revenue and Distributional Effects of Reforming the Federal Estate Tax", Urban-Brookings Tax Policy Center, October 20, 2008, http://www.taxpolicycenter.org/UploadedPDF/411777_back_grave.pdf, pp 32-33.

End Notes

More from the Authors