Making Higher Education Tax Credits More Available To Low- And Moderate-Income Students: How and Why

Senate Finance Committee Chairman Max Baucus has indicated that his committee will soon mark up education tax incentives. In addressing this issue, the Finance Committee should start by considering how to improve the existing tax credits for higher education. In particular, it should consider reforms that would address these credits’ single greatest failing: the fact that most low-income, and many moderate-income, students cannot benefit from them.

Several members of the Finance Committee have introduced legislation that would enhance these students’ access to the credits, while other Committee members have introduced a bill that would overhaul the existing credits without remedying their most significant defect (see box below). This analysis discusses the reforms needed to make the credits more available to low- and moderate-income students and the importance of making these changes if the credits are to fulfill their basic purpose of enabling more students to go to college.

The Existing Tax Credits and Low- and Moderate-Income Students

There are two existing federal tax credits for higher education expenses: the Hope Credit and the Lifetime Learning Credit. The Hope Credit is a tax credit of up to $1,650 for tuition and fees incurred by students in their first two years of postsecondary school education. The Lifetime Learning Credit is a tax credit of up to $2,000 for tuition and fees incurred by students at any stage of their postsecondary school education. (In addition, the deduction for qualified tuition and related expenses provides a deduction of up to $4,000 for tuition and fees incurred by students at any stage of their postsecondary school education. For a more detailed description of the credits and a brief discussion of other federal tax benefits for higher education, see the box below.)

Low- and moderate-income students face two major obstacles in trying to claim the education tax credits.

Non-Refundability of the Credits Blocks Access

The most basic reason the education tax credits are unavailable to most low-income students — and many moderate-income students as well — is that these credits are nonrefundable. If a credit is nonrefundable, it is available only to the extent that it can be applied against positive income tax liability. A nonrefundable credit thus has no value for households whose incomes are not high enough to owe federal income taxes. In contrast, if a credit is refundable, a taxpayer can receive a tax refund for the amount by which the credit exceeds his or her income tax liability. Thus, refundable credits offer the same benefits to low- and moderate income taxpayers as to middle- and upper-income taxpayers, but nonrefundable credits do not.[1]

In 2007, a married couple with one child in college and another child under age 17 would need an income of at least $24,300 to benefit at all from either of the education tax credits; it would need an income of $42,850 to benefit in full from the nonrefundable Lifetime Learning Credit (for which the maximum credit is $2,000) or an income of $40,515 to benefit in full from the nonrefundable Hope Credit (for which the maximum credit is $1,650). A non-traditional-age part-time student with no children would need an income of $8,750 to benefit at all from the Lifetime Learning Credit, and an income of $24,690 — more than twice full-time minimum wage earnings — to benefit from it in full (see Table 1).

Indeed, about a third of all households — and almost half of all families with children — have no federal income tax liability.[2] Very few of these households are able to benefit in full from either the Hope or the Lifetime Learning Credit, and many are not able to benefit at all.[3] As a result, the education tax credits do the least for the very students that need them most and that are most likely to fail to enroll in or complete higher education because they have difficulty affording it. Moreover, other education tax benefits, particularly Section 529 plans and Coverdell education savings accounts, are more skewed, concentrating their assistance on those in the top tax brackets. (See the box below.)

| Table 1: | ||

|

| Income to Benefit at All | Income to Benefit in Full |

| Independent (e.g. non-traditional age) student with no children | $8,750 | $24,690 |

| Unmarried parent with one child in college and one child under age 17 | $18,050 | $35,115 |

| Married couple with one child in college and one child under age 17 | $24,300 | $42,850 |

| Source: CBPP calculations | ||

The Higher Education Tax Benefits

There are two federal tax credits for higher education expenses, both enacted in 1997.

The Hope Credit provides a nonrefundable credit against income taxes of up to $1,650 in 2007 (the credit amount is indexed for inflation). Taxpayers may claim a $1 credit for each dollar of qualifying tuition and fees up to $1,100 and a 50-cent credit for each dollar of qualifying expenses between $1,100 and $2,200. Thus, a filer must have at least $2,200 in qualifying expenses to receive the maximum credit in 2007. To qualify for the Hope Credit, students must be enrolled at least half-time in the first two years of a postsecondary education program leading to a recognized education credential. A household can claim the Hope Credit for each eligible student. Since the credit is largely unavailable to low-income households and phases out for upper-income households (it is fully phased out for married couples with incomes above $114,000 and single filers with incomes above $57,000 in 2007), its benefits are concentrated among middle- and upper-middle- income households.

The Lifetime Learning Credit provides a nonrefundable credit against income taxes of up to $2,000. Taxpayers may claim a 20-cent credit for each dollar of qualifying expenses up to $10,000; thus, a filer must have at least $10,000 in qualifying expenses to receive the maximum credit. The Lifetime Learning Credit is available for tuition and fees incurred by students enrolled in some form of higher education (including less than half-time students and students beyond their first two years of postsecondary education). A household may claim only one Lifetime Learning Credit per tax return and must choose between claiming the Hope Credit and claiming the Lifetime Learning Credit. Like the Hope Credit, the Lifetime Learning Credit is generally unavailable to low-income households and phases out for upper-income households, and so the distribution of its benefits is similar.

In addition to the education tax credits, the federal tax code includes other significant tax benefits for higher education, some of which are notably more skewed to upper-income students. The deduction for qualified tuition and related expenses, which was enacted in 2001 and is scheduled to expire at the end of 2007, provides an above-the-line deduction (that is, one available to taxpayers who do not itemize their deductions) of up to $4,000 for qualifying tuition and fees. Since deductions are worth more to taxpayers in higher tax brackets, and since taxpayers must choose between claiming the tuition deduction and claiming one of the credits, about half the benefits of the deduction go to households with incomes between $100,000 and $200,000 (the deduction phases out, but at higher income levels than the Hope and Lifetime Learning Credits).* In addition, the tax-preferred saving accounts for higher education, Section 529 plans and Coverdell education savings accounts — which were significantly expanded in 2001 and in last year’s pension bill — primarily benefit upper-income households.**

* Leonard E. Burman, Elaine Maag, Peter Orszag, Jeffrey Rohaly, and John O’Hare, “The Distributional Consequences of Federal Assistance for Higher Education: The Intersection of Tax and Spending Programs,” Urban Institute-Brookings Institution Tax Policy Center Discussion Paper No. 26, August 2005.

** Susan Dynarski, “Who Benefits from the Education Saving Incentives? Income, Educational Expectations, and the Value of the 529 and Coverdell,” National Tax Journal, June 2004.

Definition of Qualifying Expenses Is Also an Obstacle

Another key reason that many moderate-income students do not benefit from the education tax credits is their narrow definition of qualifying expenses. Under current law, students can only claim the credits for what they pay in tuition and fees, minus any governmental or institutional grants. They cannot count expenses incurred for room and board, books and supplies, or transportation.

In practice, this definition means that many low- and moderate-income students would not be eligible to receive the full benefits of the credits even if the credits were made refundable. To benefit in full from the Hope Credit in 2003-2004, a student needed $2,000 in claimable tuition and fees; for the full Lifetime Learning Credit, $10,000. Most low- and moderate-income students attend community colleges — where tuition and fees averaged $2,000 per full-time, full-year student in 2003-2004 — or public four-year colleges and universities — where tuition and fees averaged about $5,200 per full-time, full-year student, according to data from the National Center for Education Statistics of the U.S. Department of Education. After taking into account grants, about half of all community college and public university students from families with incomes below $32,000 had no net tuition expenses in 2003-2004, and most others paid relatively little out of pocket. [4]

But these same low- and moderate-income students had substantial non-tuition educational expenses not covered by governmental and institutional grants. Community college students from families with incomes below $20,000 had an average of $4,800 in uncovered non-tuition educational expenses, according to the NCES data. Those at four-year public colleges and universities faced average non-tuition costs of $7,800. None of these non-tuition expenses counted toward the federal higher education tax credits.

Strikingly, room and board and books and supplies are considered qualifying expenses for purposes of tax-preferred higher education saving accounts. That is, funds withdrawn tax free from Section 529 and Coverdell Education Saving Accounts can be used to defray non-tuition expenses. These higher education tax saving incentives primarily benefit high-income households (see the box above). Thus, books and supplies and room and board are considered qualifying higher education expenses for those higher education tax incentives that primarily benefit upper-income households, but not for the education tax credits that primarily benefit middle-income households.[5]

Reasons to Expand Access to the Credits

The higher education tax credits have two key rationales. First, they are intended to encourage and enable students who would not otherwise attend or complete college to do so. Second, they are supposed to ease the economic burden that higher education costs impose on students and their families. Each of these rationales for the credits represents a strong reason to enhance low- and moderate-income students’ access to these tax benefits.

Impact of Subsidies on College Enrollment Likely Greatest for Low-Income Students

Studies have found that price subsidies can significantly impact college enrollment decisions, and a number of studies have estimated that a $1,000 reduction in the cost of college can increase enrollment by 3 to 4 percentage points, a significant gain.[6] Yet a major study of the Hope and Lifetime Learning Credits by Harvard Professor Bridget Terry Long found no evidence that they had increased college enrollment. [7] Long commented that this result was perhaps unsurprising, since the credits were largely unavailable to “marginal” students: that is, students who are deciding whether or not to attend college.

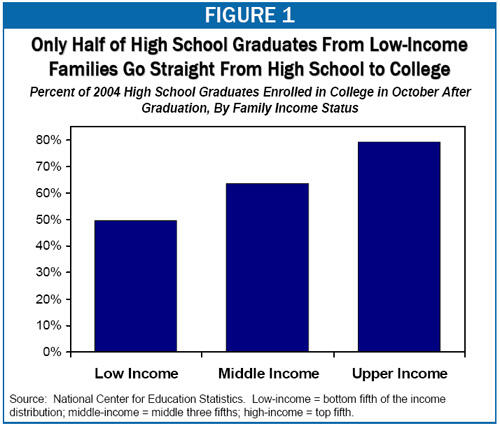

Common sense suggests that many of these “marginal” students come from low- or moderate-income families. Only about half of high-school graduates from families in the bottom fifth of the income scale went directly from high school to college in 2004, compared with more than 60 percent of those in the middle three fifths, and about 80 percent of those in the top fifth (see Figure 1). This suggests that low- and moderate-income students are more likely to be deciding whether or not to attend college, and that their decisions very likely are influenced by cost considerations.[8]

The available evidence supports the common-sense conclusion that subsidies will have the largest impact on the college enrollment decisions of low-income students. The Congressional Research Service has noted that studies consistently find that “lower-income students [are] more sensitive to changes in tuition and aid than students from middle- and upper-income families.” CRS commented, “These results suggest that the benefits of the education tax credits would be greater for lower-income students, though they are the least likely to be able to claim the credits.”[9] In other words, the unavailability of the higher education tax benefits to low-income students represents a significant missed opportunity for encouraging college enrollment.

It also represents a missed opportunity for encouraging and enabling low-income students to attend four-year colleges. The benefits of graduating from a four-year college significantly exceed those of graduating from a community college, but so do the costs. A study of the high school class of 1992 found that, even among students from low socioeconomic backgrounds with high standardized test scores at the end of junior high school, only 29 percent graduated from four-year institutions, compared with 47 percent of similarly scoring middle socioeconomic-status students and 74 percent of similarly scoring high socioeconomic-status students.[10] While high-achieving junior high students from low-income households also face other obstacles to completing high school and college, this discrepancy among high performers suggests that cost considerations likely play a significant role in barring qualified students from low-income families from four-year colleges.

Tax credits can make a notable difference in enabling qualified students to choose four-year institutions. In fact, Long’s study, which found no evidence that the education tax credits increased college enrollment, did find some evidence that they encouraged middle-income students to opt for four-year rather than two-year colleges. The existing credits cannot possibly have this effect for low-income students, however, since they are largely unavailable to these students.

Low-Income Students Have Substantial Unmet Financial Need

A second objective of the federal education tax credits is to help ease the burden of college costs, which have been increasing rapidly for the past several decades.

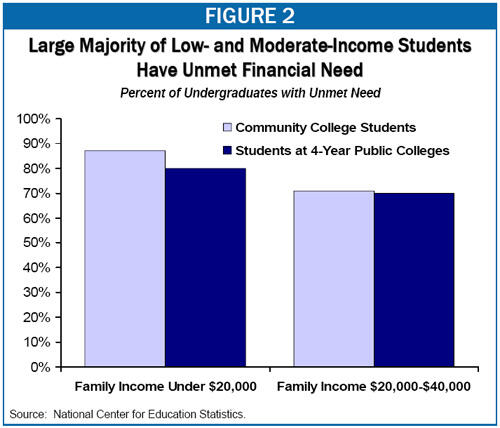

Some mistakenly believe that federal and school-based aid sufficiently insulates low-income students from high college costs and thus that they do not need the assistance provided by education tax benefits. In fact, the National Center for Education Statistics reports that — after taking into account governmental and institutional grants, subsidized loans, work study, and other aid — the large majority of low- and moderate-income undergraduates have significant unmet financial need.[11] Among community college students from families with incomes under $20,000, for instance, 87 percent had unmet financial need in 2003-2004, averaging $4,500 per student with unmet need. While the percentage of students with unmet need was slightly lower at four-year public institutions, the average amount of unmet need among those with need was even higher: $6,000 per student (see Figure 2 and Table 2). These are staggeringly high amounts for families with total annual income of less than $20,000. Very few of these families are able to use the existing education tax credits to defray any of these costs.

In addition, as Figure 1 and Table 2 show, considerable unmet need also exists among students with family income between $20,000 and $40,000. Many of these families are unable to benefit in full from the education tax credits. (Significantly lower percentages of students at higher income levels have unmet financial need, and most of these students are able to benefit in full from the education tax credits.)

| Table 2: | ||||

|

| Percent of Students With Unmet Need | Average Unmet Need Among Those With Unmet Need | ||

| Students From Families With Incomes Below $20,000 Attending: | ||||

| Community College | 87% |

| $4,500 | |

| Public Four-Year College or University | 80% |

| $6,000 | |

| Students From Families With Incomes Between $20,000 & $40,000 Attending: | ||||

| Community College | 71% |

| $3,500 |

|

| Public Four-Year College or University | 70% |

| $5,500 | |

| Source: Center for Education Statistics Figures are for dependent students, classified according to their parents' income. Figures for low-income independent students are similar. | ||||

Some have suggested that the problem of unmet need among low-income students is becoming worse. There is evidence that in recent years both public and private colleges and universities have retargeted some of their resources away from students with the greatest financial need and toward “merit-based” aid intended to attract high-performing students and thereby improve their colleges’ reputations.[12] To the extent this is occurring, it is an additional reason to make the higher education tax credits available to the students most in need of assistance.

Tax Credits and Pell Grants

It should be noted that making the education tax credits more available to low-income students is not a substitute for expanding and improving Pell Grants, the most important source of federal higher-education assistance for these students. But Pell grants, by themselves, are far from adequate. Since 2003, the value of the maximum Pell Grant has fallen in real terms, even as average tuition at public four-year institutions has increased by more than 15 percent.[13]

Education Tax Credit Legislation Introduced by Members of the Finance Committee

Several members of the Senate Finance Committee have introduced legislation that would reform the education tax credits in ways that would make them more available to low- and moderate-income students.

- S. 360, cosponsored by Senators Bingaman (D-NM) and Smith (R-OR), who are members of the Finance Committee, and Senators Murray (D-WA) and Sanders (I-VT), would make both credits refundable and expand the definition of expenses for the Hope Credit to cover room and board, books, supplies, and equipment.

- S. 97, introduced by Senator Kerry (D-MA), a member of the Finance Committee, would simplify and consolidate the credits and make them partially refundable.

- S. 3902, introduced by Senate Finance Committee Chairman Baucus (D-MT) in the previous Congress, would consolidate the credits, make them refundable and expand the definition of expenses to cover books and supplies.

In contrast, legislation (S. 851) cosponsored by Senators Schumer (D-NY), Stabenow (D-MI), Cantwell (D-WA), and Salazar (D-CO), members of the Finance Committee, and six other Senators would simplify and consolidate the credits but would not make them refundable. (It would modestly expand the definition of expenses to cover half the cost of books up to a total of $250.) As a result, the credits would remain unavailable to most low-income and many moderate-income students.

Moreover, even if needed improvements in the Pell Grant Program are made, low- and moderate-income students still will face significant higher education costs. For the 2007-2008 school year, the maximum amount a student can receive from a Pell Grant is $4,310. Even if the level of the Pell Grant were increased significantly, it still would not fully cover need for many low-income students; compare a $1,000 increase in the maximum Pell Grant — almost twice what President Bush proposed in his fiscal year 2008 budget — with the levels of unmet need shown in Table 2. Among students with unmet need from families with incomes below $20,000, even those attending community colleges had unmet need averaging $4,500.

This is a particular concern for students contemplating attending flagship state universities. Tuition and fees at the University of Maryland, for example, come to about $8,000 this year for in-state students; for in-state students living away from home, room and board adds another $8,000 to costs. Even if the maximum Pell Grant were increased by $1,000, it would cover only about two thirds of the cost of tuition and fees, and only about one third of cost including room and board (and these figures leave out the cost of books and other expenses). Giving low-income students access to educational assistance provided through the tax code, as well as Pell Grants, would help make it possible for qualified low-income students to choose to attend the stronger public universities in their states.

Conclusion: Making the Credits Available to Low- and Moderate-Income Students

Making federal tax credits for higher education available to low- and moderate-income students is important to achieving the credits’ fundamental goal of promoting college enrollment. It is also a matter of equity: low- and moderate-income students struggle with significant college expenses — after accounting for governmental and school-based aid — and should be able to avail themselves of the assistance Congress has chosen to provide through the tax code.

Other Possible Reforms to the Credits

Some have raised additional concerns about the education tax credits. One criticism is that the credits are complicated. In particular, many have criticized the fact that there are two credits, each with its own set of rules. (The higher education deduction, which is set to expire at the end of 2007, adds to the complexity by adding another set of rules.) Credit take-up rates among eligible students are relatively low (about 66 percent, according to a study by the Urban Institute-Brookings Institution Tax Policy Center), and complexity is probably one of the causes.* Several members of Congress have introduced proposals that would simplify the credits by consolidating them into one. This approach deserves serious consideration.

Another concern is that the benefits of the credits are not available until after the student's family files its tax return and, thus, are not available at the time that college costs have to be paid. This may pose a serious problem for low-income students, who are more likely than middle- or upper-income students to have trouble coming up with the needed funds while waiting for tax season. To address this issue, some have suggested that the credits could be made “advanceable:” that is, available at the time of enrollment. Eligibility could be based on prior-year income.

While it may not be feasible for Congress to address this concern about the credits this year, it might consider establishing a small-scale demonstration project, so as to better evaluate the feasibility of making the credits advanceable and the impact of doing so on enrollment.**

* Leonard E. Burman, Elaine Maag, Peter Orszag, Jeffrey Rohaly, and John O’Hare, “The Distributional Consequences of Federal Assistance for Higher Education: The Intersection of Tax and Spending Programs,” Urban Institute-Brookings Institution Tax Policy Center Discussion Paper No. 26, August 2005.

** Over the longer term, it would also be worth thinking about more comprehensive reforms. For example, in a recent Hamilton Project paper, Susan Dynarski and Judith Scott-Clayton propose fully integrating and radically simplifying Pell Grants and the higher-education tax credits. See Susan Dynarski and Judith Scott-Clayton, “College Grants on a Postcard: A Proposal for Simple and Predictable Federal Student Aid,” Hamilton Project Discussion Paper, February 2007, http://www.brookings.edu/views/papers/200702dynarski-scott-clayton.htm.

Making the credits available to low-income students requires, at a minimum, making them refundable so they can benefit those with incomes too low to owe income taxes (or too low to owe $1,650 or $2,000 in income taxes, the amounts necessary to receive the maximum Hope Credit or Lifetime Learning Credit respectively). The goal would also be furthered by expanding the definition of qualifying expenses to match the broader definition already in place for higher-education tax benefits targeted at upper-income households.

Several members of the Senate Finance Committee have sponsored legislation that would make either or both of these changes to the credits (see box above). The Finance Committee should incorporate these improvements into the legislation it develops over the coming weeks.

End Notes

[1] Deductions, such as the higher education deduction, are similar to nonrefundable credits in that they are generally of no value to low-income households. But deductions also are of greater value to upper-income than to middle-income households, since their value depends on the taxpayer’s marginal tax bracket. For example, a $1,000 deduction is worth $150 to a taxpayer in the 15 percent tax bracket but $350 to a taxpayer in the 35 percent tax bracket.

[2] Lily L. Badchelder, Fred T. Goldberg, Jr., and Peter R. Orszag, “Reforming Tax Incentives Into Uniform Refundable Credits,” Brookings Institution Policy Brief No. 156, August 2006.

[3] Households with no federal income tax liability can sometimes benefit from a nonrefundable credit if they have pre-credit tax liability (i.e. positive income tax liability before the child tax credit and the Earned Income Tax Credit). However, few of these families would have sufficient pre-credit tax liability to receive the full benefits of either the Hope or the Lifetime Learning Credit.

[4] Data are from the 2003-2004 National Postsecondary Student Aid Study. Figures here are for undergraduate students who are dependents of their parents (and are classified into income groups based on their parents’ incomes), but the figures for low-income independent students (generally students who are over age 24, are married, or have dependents, or are enrolled in a graduate or professional program) are similar. See National Center for Education Statistics, “Student Financing of Undergraduate Education: 2003-2004,” U.S. Department of Education, August 2006, http://nces.gov/pubs 2006/2006186.pdf.

[5] For further discussion of these issues, see Susan Dynarski and Judith Scott-Clayton, “Simplify and Focus the Education Tax Incentives,” Tax Notes, June 12, 2006, http://www.americanprogress.org/kf/dynarski.pdf.

[6] Some 67 percent of all 2004 high school graduates enrolled in college the following year. A well-structured $1,000 subsidy could potentially boost that to 70 or 71 percent. For a review of this literature see Bridget Terry Long, “The Impact of Federal Tax Credits for Higher Education Expenses,” National Bureau of Economic Research Working Paper No. 9553, March 2003.

[7] Bridget Terry Long, “The Impact of Federal Tax Credits for Higher Education Expenses.”

[8] Note that a lower percentage of low-income students graduate from high school, so the discrepancies among all students, including non-high school graduates, are even greater. National Center for Education Statistics, “The Condition of Education 2006,” U.S. Department of Education, June 2006, http://www.nces.ed.gov/pubs2006/2006071.pdf.

[9] Pamela J. Jackson, “Higher Education Tax Credits: An Economic Analysis,” Congressional Research Service, updated February 20, 2007, http://opencrs.cdt.org/rpts/RL32507_20070220.pdf.

[10] National Center for Education Statistics, “Youth Indicators 2005: Trends in the Well-Being of America’s Youth,” U.S. Department of Education, July 2005, http://nces.ed.gov/pubs2005/2005050.pdf. Socioeconomic status was measured by a composite score giving weight to family income and parents’ educational attainment. Low socioeconomic-status students are those from families in the bottom quarter of the distribution, middle socioeconomic-status students are those in the middle half of the distribution, and upper socioeconomic-status students are those in the top quarter.

[11] NCES calculates unmet need by subtracting all forms of financial aid and the expected family contribution from the total price of attendance, including tuition and non-tuition costs.

[12] See for example Danette Gerald and Kati Haycock, “Engines of Inequality: Diminishing Equity in the Nation’s Premier Public Universities,” National Education Trust and Kevin Carey, “Colleges Giving More Financial Aid to Wealthy Students,” Education Sector, January 24, 2006.

[13] College Board, “Trends in College Pricing 2006,” http://www.collegeboard.com/prod_downloads/press/cost06/trends_college_pricing_06.pdf.

More from the Authors