Tax Foundation Estimates of State and Local Tax Burdens Are Not Reliable

Summary

In April 2005, the Tax Foundation released its annual report on "Tax Freedom Day," which it describes as the day when "Americans will finally have earned enough money to pay off their total tax bill for the [current] year." For each state, the report shows the Tax Foundation’s estimate of state and local taxes paid by residents of that state as a share of residents’ total incomes, the so-called "tax burden," and each state’s ranking by tax burden. The estimates are shown calculated to one-tenth of one percentage point.

The apparent timeliness and precision of the Tax Foundation’s estimates are likely to attract the attention of policymakers and the media, who may use the rankings to make claims about a given state’s tax burden. But what the Tax Foundation is unlikely to acknowledge prominently is that its state and local findings do not reflect actual tax collections for that year or for the previous year. Rather, they are based on a set of estimates and projections, largely derived from years-old data and from national samples that were never intended to be used for state-by-state estimates, and calculated using a methodology that has never been formally published or subject to outside review.

This report shows the degree to which their initial projections have been erroneous, and thus potentially misleading to policymakers.

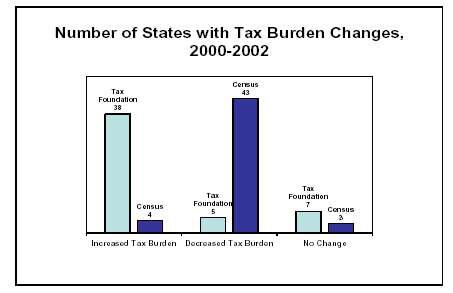

- For example, in their 2002 report the Tax Foundation claimed that tax burdens had risen since 2000 in 38 states. But three years later, it issued a revision that showed only eight states had higher tax burdens in 2002 than in 2000 — not the 38 states it had initially claimed. (Data from the Census Bureau shows that the tax burden had risen between 2000 and 2002 in only four states.)

- When the Tax Foundation initially reported figures for 2002 in April of that year, a number of states were debating whether to address their budget shortfalls with additional tax revenue or through budget cuts. Tax Foundation “information” that tax burdens already had been rising in a state over the past two years could have influenced the debate. But, as the Tax Foundation’s own revision showed, the initial “information” wasn’t true. So any policy implications that were drawn from the Tax Foundation’s report were unfounded.

The Tax Foundations ranking of state tax burdens was similarly flawed.

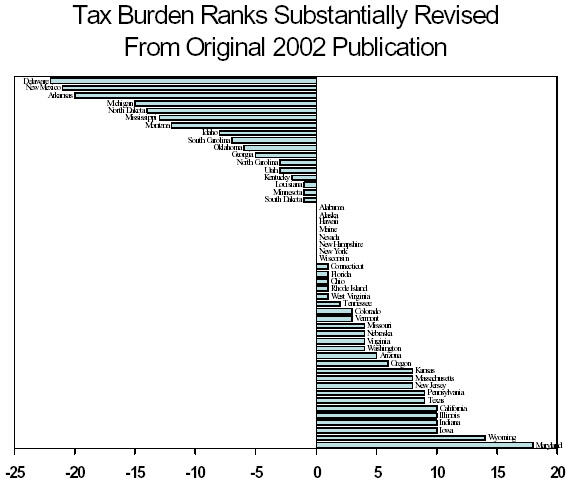

- The Tax Foundation reported in 2002 that Arkansas had the 7th highest state and local tax burden. In 2005, when the Tax Foundation released revised rankings for 2002, it reported Arkansas as having the 27th highest state and local tax burden, a revision of 20 places. New Mexico’s ranking was revised downward from 12th to 33rd, a drop of 21 places, and Delaware’s ranking fell 22 places.

- Other states also had their rankings revised. Between the 2002 Tax Foundation report and the 2005 revision, the ranking by state and local tax burden of 24 states changed by at least five places, and in 13 states the rankings changed by at least 10 places.

The estimates the Tax Foundation puts out every April often turn out to be misleading, because it is impossible to do what they claim they are doing; no one could accurately estimate the current year’s taxes relative to income for the numerous state and local units of government all over the country. In April, when the Tax Foundation releases its estimates, most taxes for the calendar year have not yet been collected. Nor is it possible to know what the path of income growth will be for the year. There is no way that the Tax Foundations numbers can be anything but speculative. Yet nowhere in its press material and reports does the Tax Foundation emphasize the instability of its estimates.

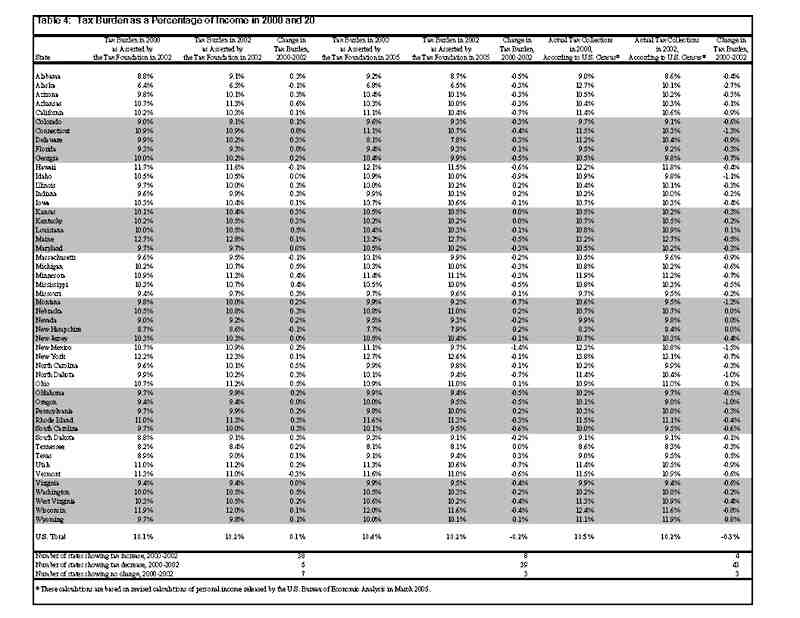

The only definitive information on state and local tax collections is compiled by the Census Bureau. But the Census Bureau takes time to compile data on actual state and local taxes; the report for a given year typically is released more than two years later. Once the Census data is completed it can be compared to the income information prepared by the Commerce Department — which also isn’t final for a substantial period of time — to determine “tax burden.”[1] For the 2002 data discussed above, final information was not available until August 2004.

It is worth noting that there are some conceptual differences between Tax Foundation and Census calculations of tax levels. For example, the Tax Foundation attempts to measure taxes by calendar year, while Census is based on fiscal year. More significantly, the Tax Foundation attempts to measure taxes paid by residents of each state, including taxes paid to other states, while the Census Bureau measures taxes collected by state and local governments within each state, including from non-residents. Thus the Tax Foundation measures the effect of the tax policies of all the states collectively on the residents of each state, while the Census measures the effect of the tax policies enacted in each state on its own residents. As a result, the Tax Foundation data is less useful for understanding the links between tax levels and state policy.

If the estimates the Tax Foundation released in 2002 are compared to the Census data for 2002, substantial discrepancies can be noted. For example, after adjusting the Tax Foundation data to account for the different way they measure taxes paid by residents, one finds that 27 states rank five or more places higher or lower in calculations based on Census data than in the Tax Foundation report. The rankings differ by at least ten places for seven states.

How Does the Tax Foundation Estimate State and Local “Tax Burdens”?

To understand why the Tax Foundation’s estimates are so shaky, it is worth remembering that there are thousands of units of state and local government in the United States that collect taxes. Those units operate under different accounting rules, different definitions of “taxes” (as opposed, say, to fees for services), and different fiscal years.

State Tax Freedom Day is Misleading

The Tax Foundation's reports include a list of the dates described as representing "Tax Freedom Day" for each state. In addition to the problem of unreliable estimates highlighted in this report, a number of other serious flaws mar the Tax Foundation's estimates total tax burdens on state residents.

About two-thirds of the tax burdens in the Tax Foundation calculations are federal tax burdens. The amount of federal taxes paid by the residents of a state thus has a large impact on that state’s “Tax Freedom Day.” But the Tax Foundation’s analysis of federal taxes is problematic. Its use of average taxes substantially overstates the federal tax burden of the vast majority of families; its estimates are at odds with more authoritative sources such as the Congressional Budget Office. In addition, its methodology is flawed because it counts taxes paid on capital gains but ignores the capital gains income on which these taxes are paid, and counts as taxes a number of non-tax items.* Because of these problems, the Tax-Freedom-Day figures for each state — which include the federal numbers — also substantially exaggerate the tax burdens of middle-class families.

Because the federal income tax system is progressive, states with relatively wealthy residents — those with higher-than-average per capita personal income — end up under the Tax Foundation’s methodology with a higher federal tax burden than other states. The fact that one state has higher-income residents than another state has nothing to do with the level of state and local taxes in a state. Yet by trumpeting state-level Tax Freedom Days that differ across the states, the Tax Foundation misleadingly implies that differences in burdens imposed by state and local taxes account for the differences across states in the Tax Foundation’s “average tax burden.”

As noted in this report, the Tax Foundation uses a procedure to allocate corporate and severance taxes based on the location of the consumers who purchase products that businesses sell (adjusted for taxes that tourists pay). This is likely to lead to further misimpressions about the role of a state’s tax policies on the tax burdens its residents are said to face. For example, when Alaska collects taxes from oil companies based on the amount of oil they produce in the state, the Tax Foundation does not count those taxes as part of Alaska’s revenue. Rather, they add those taxes to the tax burden in the states where oil is consumed. Maine residents consume a significant amount of fuel and so get allocated a large share of these Alaska taxes. Yet state legislators in Maine cannot have much impact on the level of taxes that Alaska or other oil-producing states levy on oil.

As a result, the Tax Foundation’s proclamations of state Tax Freedom Days are misleading and do little to inform legitimate debates over levels of state and local taxes and the services those taxes support.

* For a fuller description of the problems in computing the federal tax burden, see Joel Friedman, David Kamin, and Robert Greenstein, Tax Foundation Figures Do Not Represent Middle-Income Tax Burdens, Center on Budget and Policy Priorities, April 7, 2005.

The task of gathering and comparing data on tax collections from all those units of government falls to the U.S. Census Bureau’s Government Finances division. It typically takes several years of work by a team of Census experts to generate and publish their results for any given year. While the Census results are not perfect, they are widely recognized as the most reliable source of data on tax collections at the state and local level.

How, then, can the Tax Foundation purport to know what the tax burden is in each state in any given year, several years before the Census Bureau publishes its results? In fact, the Tax Foundation results are not hard data. Rather, they are forecasts generated by its “tax allocation model” to produce estimates and rankings of state and local tax burdens for the current year. And this model, in turn, is based on Census surveys from past years, a separate nationwide sampling that Census conducts of a small number of local governments, and other sources. (It is not possible to evaluate in detail the forecasting methodology and sources of forecasting error of the Tax Foundation model because they do not describe their model or methodology in a publicly available document.)

There is nothing improper about making forecasts, of course — as long as the inherent uncertainty is acknowledged. The Tax Foundation, however, does not warn readers that their data are only forecasts and thus may be inaccurate. They are presented as definitive. [2]

Judging the Accuracy of Tax Foundation Forecasts

There are two ways the accuracy of the Tax Foundation’s forecasts could be judged. One is to adhere to the Tax Foundation’s own methodology and analyze the degree to which they themselves revise their tax burdens and rankings once actual data on tax collections become available. The other way to judge is by comparing the Tax Foundation data to the Census data that is released two to three years after the initial report.

Revisions over Time

Using the Tax Foundation’s own methodology, the degree of revision is telling. Each year when the Tax Foundation releases its new information, it includes historical series of state “Tax Freedom” days. As actual data for particular years becomes available, the Tax Foundation is forced to replace its forecast estimates with actual data. Comparing the forecast to later revisions allows an assessment of just how much weight should be placed on its initial, same-year estimates.

In 2005, the Tax Foundation released new reports of tax burdens which included revised estimates of state and local tax burdens first reported in 2002.

- Comparing the 2002 report and the revision published in 2005, the ranking of 24 states changed by at least five places.

- In 13 states, the rankings changed by at least ten places.

One might argue that 2002 was a particularly difficult year in which to make accurate forecasts, since it was the first year of the recent state fiscal crisis. But the same-year data that the Tax Foundation has released in others years have been equally erroneous and misleading.

- Comparing the state tax burden rankings the Tax Foundation released in 1998 with revisions released in 2005, the rankings of 23 states changed by at least five places, while the rankings of 13 states changed by at least ten places.

- For the report the Tax Foundation released in 2000, the revisions resulted in 23 states changing ranking by at least five places, and ten states changing by at least 11 places.

The Tax Foundation does not in its published report explain why these revisions occur, or emphasize that their more recent rankings, too, will be revised.

The Tax Foundation has been particularly inaccurate in its determination of the direction in which tax burdens are moving.

- The 2002 report said that taxes had risen since 2000 in some 38 states, while five states had lower tax burdens and seven had no change. But the Tax Foundation’s revisions issued three years after the fact told the opposite story. By 2005, the Tax Foundation asserted that only eight states had higher tax burdens in 2002 than in 2000, while thirty-nine had lower tax burdens and three had no change.

- Calculations from the actual Census collections data released later in 2004 confirm the inaccuracy of the initial report: from 2000 to 2002, only four states’ tax collections rose relative to income; taxes fell in 43 states and were unchanged in three.

Comparison to Census Data

The most recent Tax Foundation report on state and local tax burdens that can be compared to actual state and local tax collections is the report published in April 2002. In August 2004, the Census Bureau produced its tally of actual 2002 tax collections.

Comparing the Tax Foundation’s original forecasts to the measure that most economists use to assess state tax burdens — the Census Bureau’s tally divided by state personal income — gives a sense of the magnitude of the Tax Foundation’s forecasting errors.

- Ten states rank at least five places higher in calculations based on Census data than in the Tax Foundation calculations, while 11 rank at least five places lower. Six states rank at least ten places lower and four states rank at least ten places higher.

- For example, in 2002, Idaho, Michigan, and Washington were all judged by the Tax Foundation to have had above-average taxes in that year, but the calculations from Census data show that those states had below-average taxes in 2002.

- Other states where the Tax Foundation overstated the state’s ranking, relative to the Census-based calculations, by more than 10 places include Arkansas, Connecticut.

The Tax Foundation’s assessment of how each state’s ranking of state tax burdens was changing over time also differed substantially from the Census data.

- The Tax Foundation reported in 2002 that 21 states moved up in ranking between 2000 and 2002, signifying that their tax burden relative to other states had increased. Calculations based on Census Bureau data, however, found that seven of the 21 actually moved down in ranking or had no change in ranking between 2000 and 2002.

The Tax Foundation’s “Incidence Adjustments”

One methodological adjustment that the Tax Foundation makes explicit in their report pertains to state and local tax incidence. Census tax data for a given state reflect the state and local taxes collected by governmental units in that state. Most economists describe this measure divided by state personal income as the state’s “tax burden,” while recognizing that in actuality out-of-state residents pay some share of those taxes. The Tax Foundation attempts actually to assign a share of the taxes collected in each state to residents of other states. Each state, then, becomes a net “exporter” or a net “importer” of taxes.

But this basic difference in approach does not explain why the Tax Foundation’s numbers for 2002 were so far off from what the Census found to be the actual case. It is possible to factor out the Tax Foundation’s adjustment for tax exporting and importing, using data provided in the report released in 2002 for tax year 2002. Even after accounting for this adjustment, the Tax Foundation’s numbers for tax year 2002 are different from calculations based on Census Bureau data.[3] A total of 27 states rank five or more places higher in one ranking than in the other, while seven states' rankings differ by ten or more places.

The incidence adjustments themselves are somewhat problematic. For instance, the Tax Foundation exports tourism taxes, severance taxes, and business taxes, but not property taxes.

States with high levels of out-of-state property ownership, such as Maine, thus are not well served by the Tax Foundation methodology. Moreover, the incidence adjustments probably make the tax data less useful, not more useful, to policymakers, because they cause a state’s “tax burden” in any state to reflect in part policies that are beyond the purview of that state’s lawmakers.

Conclusion

No one should draw any policy conclusions from the same-year state tax burden data released each April by the Tax Foundation. The data are forecasts based on scant evidence that frequently are proven wrong once actual information becomes available.

| Table 1: | |||

| State | Tax Burden Rank in 2002,as Asserted by the Tax Foundation in 2002 | Tax Burden Rank in 2002,as Asserted by the Tax Foundation in 2005 | Absolute Difference in Rank |

| Alabama | 46 | 46 | 0 |

| Alaska | 50 | 50 | 0 |

| Arizona | 28 | 23 | 5 |

| Arkansas | 7 | 27 | 20 |

| California | 24 | 14 | 10 |

| Colorado | 45 | 42 | 3 |

| Connecticut | 11 | 10 | 1 |

| Delaware | 27 | 49 | 22 |

| Florida | 42 | 41 | 1 |

| Georgia | 25 | 30 | 5 |

| Hawaii | 4 | 4 | 0 |

| Idaho | 17 | 25 | 8 |

| Illinois | 31 | 21 | 10 |

| Indiana | 34 | 24 | 10 |

| Iowa | 22 | 12 | 10 |

| Kansas | 21 | 13 | 8 |

| Kentucky | 18 | 20 | 2 |

| Louisiana | 16 | 17 | 1 |

| Maine | 1 | 1 | 0 |

| Maryland | 37 | 19 | 18 |

| Massachusetts | 39 | 31 | 8 |

| Michigan | 14 | 29 | 15 |

| Minnesota | 5 | 6 | 1 |

| Mississippi | 15 | 28 | 13 |

| Missouri | 38 | 34 | 4 |

| Montana | 32 | 44 | 12 |

| Nebraska | 13 | 9 | 4 |

| Nevada | 43 | 43 | 0 |

| New Hampshire | 48 | 48 | 0 |

| New Jersey | 23 | 15 | 8 |

| New Mexico | 12 | 33 | 21 |

| New York | 2 | 2 | 0 |

| North Carolina | 29 | 32 | 3 |

| North Dakota | 26 | 40 | 14 |

| Ohio | 9 | 8 | 1 |

| Oklahoma | 33 | 39 | 6 |

| Oregon | 41 | 35 | 6 |

| Pennsylvania | 35 | 26 | 9 |

| Rhode Island | 6 | 5 | 1 |

| South Carolina | 30 | 37 | 7 |

| South Dakota | 44 | 45 | 1 |

| Tennessee | 49 | 47 | 2 |

| Texas | 47 | 38 | 9 |

| Utah | 8 | 11 | 3 |

| Vermont | 10 | 7 | 3 |

| Virginia | 40 | 36 | 4 |

| Washington | 20 | 16 | 4 |

| West Virginia | 19 | 18 | 1 |

| Wisconsin | 3 | 3 | 0 |

| Wyoming | 36 | 22 | 14 |

| Number of states that changed ranking by five or more places: 24 Number of states that changed ranking by ten or more places: 13 | |||

| Table 2: | |||

| State | Tax Burden Rank in 2002, as Asserted by the Tax foundation in 2002 | Rank Based on Actual Tax Collection in 2002, According to U.S. Census* | Absolute Difference in Rank |

| Alabama | 46 | 48 | 2 |

| Alaska | 50 | 29 | 21 |

| Arizona | 28 | 25 | 3 |

| Arkansas | 7 | 21 | 14 |

| California | 24 | 14 | 10 |

| Colorado | 45 | 45 | 0 |

| Connecticut | 11 | 22 | 11 |

| Delaware | 27 | 18 | 9 |

| Florida | 42 | 44 | 2 |

| Georgia | 25 | 34 | 9 |

| Hawaii | 4 | 4 | 0 |

| Idaho | 17 | 36 | 19 |

| Illinois | 31 | 28 | 3 |

| Indiana | 34 | 30 | 4 |

| Iowa | 22 | 20 | 2 |

| Kansas | 21 | 24 | 3 |

| Kentucky | 18 | 16 | 2 |

| Louisiana | 16 | 10 | 6 |

| Maine | 1 | 2 | 1 |

| Maryland | 37 | 27 | 10 |

| Massachusetts | 39 | 38 | 1 |

| Michigan | 14 | 26 | 12 |

| Minnesota | 5 | 6 | 1 |

| Mississippi | 15 | 23 | 8 |

| Missouri | 38 | 39 | 1 |

| Montana | 32 | 40 | 8 |

| Nebraska | 13 | 13 | 0 |

| Nevada | 43 | 35 | 8 |

| New Hampshire | 48 | 49 | 1 |

| New Jersey | 23 | 19 | 4 |

| New Mexico | 12 | 12 | 0 |

| New York | 2 | 1 | 1 |

| North Carolina | 29 | 33 | 4 |

| North Dakota | 26 | 17 | 9 |

| Ohio | 9 | 8 | 1 |

| Oklahoma | 33 | 37 | 4 |

| Oregon | 41 | 47 | 6 |

| Pennsylvania | 35 | 31 | 4 |

| Rhode Island | 6 | 7 | 1 |

| South Carolina | 30 | 42 | 12 |

| South Dakota | 44 | 46 | 2 |

| Tennessee | 49 | 50 | 1 |

| Texas | 47 | 41 | 6 |

| Utah | 8 | 15 | 7 |

| Vermont | 10 | 9 | 1 |

| Virginia | 40 | 43 | 3 |

| Washington | 20 | 32 | 12 |

| West Virginia | 19 | 11 | 8 |

| Wisconsin | 3 | 5 | 2 |

| Wyoming | 36 | 3 | 33 |

| Number of states that changed ranking by five or more places Number of states that changed ranking by ten or more places | 21 10 | ||

| * These rankings are based on revised calculations of personal income released by the U.S. Bureau of Economic Analysis in March 2005. Rankings based on earlier estimates of personal income differ from these rankings by up to eight places in Alaska, Iowa, New Mexico, Oklahoma, and Pennsylvania, but by five places or less in all other states. | |||

| Table 3: | |||

| State | Tax Burden Rank in 2002, as Asserted by the Tax Foundation in 2002, Factoring Out the Tax Foundation’s Adjustment for Tax importing and Importing | Rank Based on Actual Tax Collections in 2002, According to U.S. Census* | Absolute Difference in Rank |

| Alabama | 45 | 48 | 3 |

| Alaska | 21 | 29 | 8 |

| Arizona | 31 | 25 | 6 |

| Arkansas | 7 | 21 | 14 |

| California | 23 | 14 | 9 |

| Colorado | 47 | 45 | 2 |

| Connecticut | 17 | 22 | 5 |

| Delaware | 19 | 18 | 1 |

| Florida | 44 | 44 | 0 |

| Georgia | 33 | 34 | 1 |

| Hawaii | 5 | 4 | 1 |

| Idaho | 24 | 36 | 12 |

| Illinois | 29 | 28 | 1 |

| Indiana | 35 | 30 | 5 |

| Iowa | 28 | 20 | 8 |

| Kansas | 26 | 24 | 2 |

| Kentucky | 22 | 16 | 6 |

| Louisiana | 20 | 10 | 10 |

| Maine | 1 | 2 | 1 |

| Maryland | 40 | 27 | 13 |

| Massachusetts | 39 | 38 | 1 |

| Michigan | 11 | 26 | 15 |

| Minnesota | 6 | 6 | 0 |

| Mississippi | 15 | 23 | 8 |

| Missouri | 42 | 39 | 3 |

| Montana | 27 | 40 | 13 |

| Nebraska | 18 | 13 | 5 |

| Nevada | 38 | 35 | 3 |

| New Hampshire | 46 | 49 | 3 |

| New Jersey | 25 | 19 | 6 |

| New Mexico | 4 | 12 | 8 |

| New York | 2 | 1 | 1 |

| North Carolina | 34 | 33 | 1 |

| North Dakota | 9 | 17 | 8 |

| Ohio | 13 | 8 | 5 |

| Oklahoma | 30 | 37 | 7 |

| Oregon | 41 | 47 | 6 |

| Pennsylvania | 36 | 31 | 5 |

| Rhode Island | 10 | 7 | 3 |

| South Carolina | 37 | 42 | 5 |

| South Dakota | 48 | 46 | 2 |

| Tennessee | 50 | 50 | 0 |

| Texas | 49 | 41 | 8 |

| Utah | 8 | 15 | 7 |

| Vermont | 16 | 9 | 7 |

| Virginia | 43 | 43 | 0 |

| Washington | 32 | 32 | 0 |

| West Virginia | 12 | 11 | 1 |

| Wisconsin | 3 | 5 | 2 |

| Wyoming | 14 | 3 | 11 |

| Number of states that changed ranking by five or more places 27

| |||

| * These rankings are based on revised calculations of personal income released by the U.S. Bureau of Economic Analysis in March 2005. Rankings based on earlier estimates of personal income differ from these rankings by up to eight places in Alaska, Iowa, New Mexico, Oklahoma, and Pennsylvania, but by five places or less in all other states. | |||

End Notes

End Notes::

[1] Note that the Census Bureau definition of tax burden, taxes as a percent of personal income, shares with the Tax Foundation one of the flaws described in the box on page 4. It counts taxes paid on capital gains income, but does not count the capital gains income on which those taxes were paid. This is because the Commerce Department’s National Income and Product Accounts — from which the measure of personal income as well as the income measure used by the Tax Foundation are derived — do not include capital gains income.

[2] It is good practice for organizations that forecast information to be upfront about the uncertainty in those forecasts. For example, the Congressional Budget Office recently released a report entitled, The Uncertainty of Budget Projections: A Discussion of Data and Methods: The Budget and Economic Outlook, it also highlights the uncertainty, and provides detailed information about how and why its forecasts have changed.

[3] It should be noted that the Tax Foundation reports tax burdens on a calendar year basis, while Census data on state and local government revenue are available by fiscal year. While the time periods of the data may not coincide, state revenue collections are greatest during the first and second quarters of the calendar year, which fall in the same calendar and fiscal year in most states.

More from the Authors

Areas of Expertise