Alternative Approaches to AMT Reform

Criteria For Evaluation and Preliminary Assessments

The Subcommittee on Select Revenue Measures of the House Ways and Means Committee recently held hearings on the Alternative Minimum Tax, and Subcommittee Chairman Richard Neal has said he is developing a proposal for permanent, revenue-neutral AMT reform. According to news accounts, the proposal will take the form of an AMT exclusion for households with incomes below a certain level (which would remove all such households from the AMT), likely paid for with an increase in taxes on high-income taxpayers.[1]

Senate Finance Committee Chair Max Baucus, meanwhile, has suggested that he intends to address the AMT issue by providing a two-year extension of the AMT “patch.”[2] The AMT patch is the temporary AMT relief measure that has kept the number of AMT taxpayers from rising rapidly over the past few years and that expired at the end of 2006.

This analysis sets out three tests by which to judge different approaches to AMT reform.[3] It also offers some preliminary thoughts on how the AMT patch and the emerging House proposal might fare on these tests.

1. AMT Reform Should Be Paid For

The first and most fundamental test of any AMT reform proposal is whether its costs are fully offset. The AMT relief provided in 2001-2006 was not paid for and, as a result, has already added more than $100 billion to deficits. Moreover, the costs of AMT relief rise sharply each year. Thus, if Congress were to continue the strategy of patching the AMT without paying for it, this approach would add almost $800 billion to deficits over the next ten years (2008-2017), if the 2001 and 2003 tax cuts expire, and about $1.3 trillion to deficits if the tax cuts are extended. (The 2001 and 2003 tax cuts push millions of additional taxpayers onto the AMT and dramatically increase the cost of providing AMT relief.[4])

Paying for AMT reform is required under the Pay-As-You-Go (PAYGO) budget rules reintroduced in the House in January and included in the Senate budget resolution. Given the nation’s bleak long-term fiscal outlook, adhering to the PAYGO rules is essential. With the federal government facing escalating budget deficits in future decades, it would be irresponsible to add to these deficits the cost of a massive, unpaid-for AMT fix. The added deficits that would result from unpaid-for changes to the AMT would have negative economic consequences over time.[5] In addition, since the nation’s long-term budget shortfall must eventually be addressed, adding to that shortfall now will force deeper program cuts or steeper tax increases later.

Fortunately, paying for AMT reform is feasible. The Urban Institute-Brookings Institution Tax Policy Center recently published a menu of options for offsetting the cost of reform. The possibilities range from modest increases in ordinary income tax rates to reforms to the AMT itself.[6]

Both the Senate and House budget resolutions and statements by Representative Neal and Ways and Means Committee Chairman Charles Rangel reflect a commitment to paying for AMT reform. If Congress adheres to that plan, this will be a major advance over the previous two Congresses’ approach to the AMT issue.

2. AMT Reform Should Be Well-Targeted

A paid-for AMT fix is still costly: it consumes offsets that could be used to pay for other national priorities, ranging from improvements in health care and education to deficit reduction. Policymakers can conserve these scarce offsets by ensuring that the tax benefits provided by AMT reform proposals are carefully targeted toward addressing the core concern motivating current AMT reform efforts: stemming the growth in the number of middle-income households who are subject to the AMT. A proposal that protects the middle class from the AMT at a lower cost leaves more resources available to address the nation’s many other important needs.

The AMT “Patch” Is Not Especially Well Targeted

Since 2001, Congress has kept the number of AMT taxpayers from rising rapidly with a series of AMT “patches.” These AMT patches have increased the AMT exemption level: the amount of a household’s income that is exempt from tax under the AMT.[7] Increases in the AMT exemption reduce some households’ taxable income under the AMT to zero, automatically pushing them off the AMT. For other households, increases in the AMT exemption lower AMT taxable income and thereby tentative AMT liability below regular income tax liability; these households, as well, are pushed off the AMT. Finally, increases in the AMT exemption level also benefit many households that remain on the AMT, since they owe less in AMT taxes than they would with a lower exemption level.

The AMT exemption phases out for higher income households but is fully phased out only at quite high income levels. As a result, increases in the AMT exemption level deliver a significant share of their benefits to households with very substantial incomes. For example, the 2006 AMT patch (which increased the AMT exemption to $62,550 for married couples and $42,550 for singles) benefited married couples with AMT income of up to $400,000 (and single filers with AMT income of up to $300,000). The Tax Policy Center estimates that about one third of the benefits of the 2006 AMT patch went to households with cash income above $200,000.[8]

Meanwhile, the Joint Committee on Taxation estimates that 1.6 million households with adjusted gross income below $200,000 and 300,000 households with adjusted gross income below $100,000, remained on the AMT in 2006 even with the patch. Whether a given household is removed from the AMT by an increase in the AMT exemption level depends not only on the household’s income but also on how many of the deductions and exemptions that the household claims under the regular income tax are disallowed under the AMT.

Continuing the AMT patch would be very expensive. Extending the patch (adjusted for inflation) just through 2007 would cost about $45 billion, according to Tax Policy Center estimates; continuing the patch for two years, through 2008, would cost about $100 billion.

An AMT “Exclusion” Could Be Better Targeted — Depending on the Income Level Chosen

The House is reportedly considering an alternative approach that would simply exclude all households with incomes below a given level from paying the AMT. In effect, the AMT would be repealed for households with incomes below the threshold amount: they would not owe AMT even if they claimed many exemptions and deductions. These households would be subject to only one income tax system, the regular income tax. The AMT would remain in place as a backstop tax system for higher-income households.

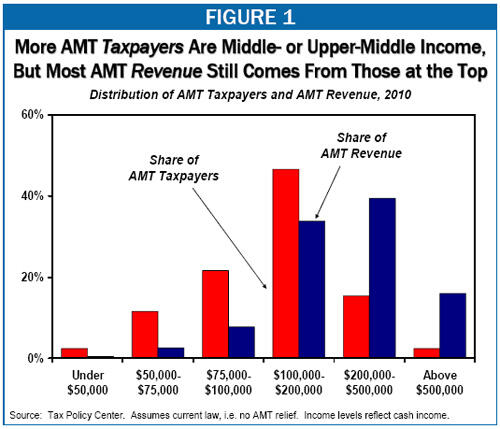

The exclusion approach has the potential to be better targeted than the patch if it takes full advantage of a key fact about the AMT. Under current law, a growing number of AMT taxpayers will be middle- or upper-middle income households. But the bulk of AMT revenue will continue to come from high-income households. (See Figure 1.) Thus, an exclusion could eliminate the AMT for the vast majority of AMT taxpayers while retaining the majority of AMT revenue. In contrast, an exclusion that also eliminated the AMT for very high-income households would lose considerably more revenue, with the additional cost going toward large tax cuts for these high-income households.

How costly — and how well targeted — an exclusion proposal is will thus depend crucially on the income level chosen for the exclusion. In thinking about what might represent an appropriate income level, it is informative to consider the effects of a few potential thresholds. The limits specified in Table 1 below are for married couples; limits for singles are assumed to be half those for married filers.

- With an exclusion of $150,000 of adjusted gross income ($75,000 for singles), 92 percent of U.S. households would be automatically exempt from the AMT. Moreover, only some of the 8 percent of households with incomes above the exclusion level would actually owe AMT. Thus, the Tax Policy Center estimates show that (if the AMT were left otherwise unchanged), 7.8 million households nationwide, or 5.2 percent of all U.S. households, would actually pay AMT.

- (Under current law in 2007, the Tax Policy Center estimates that 23 million households, or 16 percent of all U.S. households, would owe AMT.)

- With an exclusion of $200,000 of adjusted gross income ($100,000 for singles), 96 percent of households would be automatically exempt from the AMT. Only 2.9 percent of households, or 4.3 million households, would actually pay AMT.

- With an exclusion of $250,000 of adjusted gross income ($125,00 for singles), 97 percent of U.S. households would be automatically exempt from the AMT. Only 1.9 percent of households, or 2.8 million households nationwide, would owe AMT.

| Table 1: | |||

| Exclusion Level* | Percent of Households Automatically Exempt | Number of Households Paying AMT (Millions) | Percent of Households Paying AMT |

|---|---|---|---|

| $150,000 | 92% | 7.8 | 5.2% |

| $200,000 | 96% | 4.3 | 2.9% |

| $250,000 | 97% | 2.8 | 1.9% |

| Source: CBPP calculations based on Tax Policy Center data. *Exclusion levels specified are for married filers; thresholds for single filers are assumed to be half those for married couples. | |||

Many have noted that the effects of a given AMT exclusion will vary by state; at any given threshold, a smaller percentage of households in wealthier states will be automatically exempt from the AMT. IRS data show, however, that if a $200,000 exclusion ($100,000 for singles) had been in place in 2004 (the latest year for which these IRS data are available), at least 94 percent of tax filers in every state (and 92 percent in the District of Columbia) would have been automatically exempt from the AMT (see Appendix Table 1). In 40 states, at least 97 percent of taxpayers would have been automatically exempt.[9]

Costs Rise at Higher Exclusion Levels

Since the average amount of tax owed under the AMT increases with household income, the cost of any reform plan will rise steeply as households at higher and higher income levels are removed from the AMT. Tax Policy Center estimates show that the direct cost of excluding married couples with adjusted gross incomes below $150,000 from the AMT (singles with AGI below $75,000) in 2007 would be about $21 billion. If the exclusion level were increased from $150,000 to $200,000, the direct cost would increase to $32 billion. If the exclusion were increased to $250,000, the direct cost would rise to $40 billion.

| Table 2: | |

| Increase in the Exclusion Level | Approx. Cost Per Household Removed from AMT |

|---|---|

| $150,000-$200,000 | $3,000 |

| $200,000-$250,000 | $5,500 |

| Source: CBPP calculations based on Tax Policy Center data. | |

Further, as Table 2 shows, the cost per additional household removed from the AMT also would climb. Increasing the exclusion level from $150,000 to $200,000 costs $3,000 per household in the $150,000 to $200,000 range that is removed from the AMT. Increasing the exclusion level from $200,000 to $250,000 costs $5,500 per additional household removed from the AMT.

It is important to recognize that, in reality, the cost of any exclusion proposal would be somewhat higher than the “direct costs” listed above, since it would not be possible — or desirable — to simply exclude households with incomes below a given threshold from the AMT, with no other changes. Doing so would create steep “cliff effects:” that is, situations in which a $1 increase in a taxpayer’s income (for instance, an increase in AGI from $150,000 to $150,001, if $150,000 were the selected exclusion level) could result in thousands of dollars of additional tax liability. This could occur because, at an income level of $150,000, the taxpayer would be automatically exempt from the AMT, but at an income level of $150,001, she would become liable for her full AMT tax bill.

To avoid such cliff effects, some graduated AMT relief would need to be provided to taxpayers with incomes above the exclusion (so that the exclusion would in essence be phased out). But even with the added costs of such relief taken into account, it still would almost certainly be possible to design an AMT reform that was more effective than the patch at protecting middle-income households from the AMT, and at a lower cost.

3. AMT Reforms Should Be Permanent

Assuming that both are paid for, a permanent AMT reform has significant advantages over another temporary fix. As a matter of both responsible budgeting and responsible tax policy, it would be far better to figure out what sort of AMT fix the nation can afford over the longer term than to provide a generous temporary fix but defer the questions of whether the cost of that fix is sustainable and how the AMT issue should ultimately be resolved.

- Even if the cost of a temporary AMT fix were offset, when it expired it would leave the nation facing the same costly AMT problem it faces today. And there is no guarantee that the next AMT fix — and the one after that — would be paid for. Many in Congress have consistently favored extending expiring provisions such as the AMT patch without offsetting the costs. In addition, many members of Congress continue to oppose applying the Pay-As-You-Go rules to tax cuts, and there is no assurance that PAYGO will endure over the years. At some point, Congress may allow the PAYGO rules to lapse, or may choose to waive those rules when extending expiring tax provisions because it proves difficult politically to secure agreement on revenue-raising measures that could serve as offsets. This seems a particularly serious risk given that, if Congress enacts another temporary AMT fix, it is likely to pay for it with permanent offsets; that is, Congress may pay for a one- or two-year AMT fix with offsets that recoup the revenue over five or ten years. If this occurs, it will not be possible to simply extend those offsets to pay for an extension of the AMT fix. The full savings from the offsets would already have been used up to pay for the one- or two-year patch. In addition, the supply of permanent offset measures will have been depleted: there will be fewer politically viable offsets left on the table. This may make it more likely that Congress would choose to deficit finance the continuation of AMT relief after the one- or two-year patch expired.

- Another disadvantage of a temporary fix is that it leaves taxpayers in the same position of uncertainty they are in today. A permanent reform would offer middle-income households permanent protection from the AMT and make the tax code more predictable for all taxpayers. It would represent a welcome departure from Congress’s practice of the past several years, during which Congress has routinely enacted expensive tax cuts and then sunset them to mask their true costs. This has created uncertainty for taxpayers and also introduced considerable uncertainty into the nation’s finances.

Despite the disadvantages of a temporary fix, and the advantages of permanent reform, some policymakers have argued that Congress should pass a temporary AMT fix this year so that the larger AMT issue can be dealt with as part of a comprehensive overhaul of the tax code. Virtually all tax policy experts agree that the ideal tax system would have a broad tax base with few special exemptions, exclusions, or deductions and would therefore have no need for an AMT. Thus if lawmakers at some point reform the U.S. tax code to bring it closer to that ideal, they may be able to significantly scale back, or even dispense with, the AMT as part of that reform.

But comprehensive tax reform is nowhere on the immediate horizon. Moreover, reforming the AMT now would not prevent Congress from returning to the issue if at some point it does engage in a major tax reform effort. The fact that Congress may engage in more significant tax reform at some future date is no reason not to reform this aspect of the tax code this year, in a fiscally responsible manner.

| APPENDIX TABLE 1: | |

| State | |

|---|---|

| Alabama | 98% |

| Alaska | 97% |

| Arizona | 97% |

| Arkansas | 98% |

| California | 95% |

| Colorado | 96% |

| Connecticut | 94% |

| Delaware | 97% |

| D.C. | 92% |

| Florida | 97% |

| Georgia | 97% |

| Hawaii | 97% |

| Idaho | 98% |

| Illinois | 96% |

| Indiana | 98% |

| Iowa | 98% |

| Kansas | 98% |

| Kentucky | 98% |

| Louisiana | 98% |

| Maine | 98% |

| Maryland | 95% |

| Massachusetts | 95% |

| Michigan | 97% |

| Minnesota | 97% |

| Mississippi | 99% |

| Missouri | 98% |

| Montana | 98% |

| Nebraska | 98% |

| Nevada | 96% |

| New Hampshire | 97% |

| New Jersey | 94% |

| New Mexico | 98% |

| New York | 95% |

| North Carolina | 98% |

| North Dakota | 98% |

| Ohio | 98% |

| Oklahoma | 98% |

| Oregon | 97% |

| Pennsylvania | 97% |

| Rhode Island | 97% |

| South Carolina | 98% |

| South Dakota | 98% |

| Tennessee | 98% |

| Texas | 97% |

| Utah | 98% |

| Vermont | 98% |

| Virginia | 96% |

| Washington | 97% |

| West Virginia | 99% |

| Wisconsin | 98% |

| Wyoming | 98% |

| United States | 97% |

| Source: CBPP calculations based on Internal Revenue Service data. Due to the effects of inflation and real income growth, the percentages of households automatically exempt likely would be slightly, but not significantly, lower if the $200,000 exclusion were implemented in 2007. For example, the Tax Policy Center estimates that, nationwide, 96 percent (rather than 97 percent) of households would be automatically exempt under a $200,000 exclusion in 2007. | |

End Notes

[1] Lori Montgomery Democrats Craft New Tax Rules, New Image: Plan Tries to Shield Middle Class from Paying High Rates,” Washington Post, April 23, 2007.

[2] Alan K. Ota, “Top Democrats Back Two-Year Tax Patch,” CQ Today, March 2, 2007.

[3] These tests are not the only considerations that should be taken into account in assessing AMT reforms. They are, however, three especially important criteria.

[4] See Aviva Aron-Dine, “Myths and Realities About the Alternative Minimum Tax,” Center on Budget and Policy Priorities, February 14, 2007.

[5] See Aviva Aron-Dine and Robert Greenstein, “The Economic Effects of the Pay-As-You-Go Rule,” Center on Budget and Policy Priorities, March 19, 2007.

[6] Leonard E. Burman, William G. Gale, Gregory Leiserson, and Jeffrey Rohaly, “Options to Fix the AMT,” Tax Policy Center, January 19, 2007, http://www.taxpolicycenter.org/publications/template.cfm?PubID=411408.

[7] The AMT patches have also allowed households to claim certain tax credits (e.g. education tax credits) under the AMT. The cost of allowing taxpayers to claim these credits under the AMT in 2006 was $2.8 billion, according to Joint Committee on Taxation estimates, which is less than a tenth the cost of the increase in the AMT exemption level.

[8] Cash income is a more inclusive measure of income than adjusted gross income or AMT income; for example, it includes non-taxable pension income and contributions to tax-deferred retirement saving accounts. Thus, more households have cash income above $200,000 than have AGI or AMT income above $200,000. The Tax Policy Center issues distributional estimates based on cash income because it provides a more comprehensive measure of the income that households have available to them and thus is generally a more accurate measure of economic status.

[9] Due to the effects of inflation and real income growth, the percentages of households automatically exempt likely would be slightly, but not significantly, lower if the $200,000 exclusion were implemented in 2007.

More from the Authors