Families’ Food Stamp Benefits Purchase Less Food Each Year

Food stamp benefits average only about one dollar per person per meal (to be precise, the figure is $1.05 in 2007). In addition, as a result of benefit cuts enacted as part of the 1996 welfare law, the purchasing power of most households’ food stamp benefits is eroding in value each year.

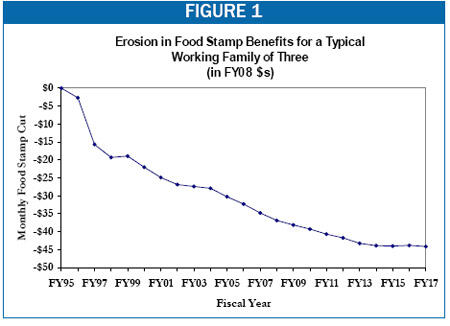

In 2008, food stamp benefits for a typical working parent with two children will be about $37 a month lower than they would have been without the across-the-board benefit cuts included in the 1996 law. By 2017, the average benefit reduction from those provisions will reach almost $45 a month in 2008 dollars. (See figure 1.) In fact, by 2017 a typical working parent of two will, over the course of a year, miss out on more than one and a half months-worth of food stamps, compared to the amount of benefits she or he would have received under the law in place prior to 1996. Under current rules, this lost ground will never be recovered.

What is Causing the Benefit Erosion?

The fact that food stamp benefits purchase less food is a legacy of two provisions of the 1996 welfare law. When the 1996 law was enacted, the Congressional Budget Office estimated it would cut the Food Stamp Program by $28 billion over six years. (Congress was using a six-year budget window at the time.) About 40 percent of these cuts came from two provisions: a permanent freeze in the food stamp standard deduction, which CBO said would result in $5 billion in benefit cuts over the 1997-2002 period, and a three percent reduction in the Food Stamp Program’s maximum benefit, which CBO estimated would produce a benefit reduction of $6.3 billion over six years (and which resulted in a benefit cut of more than three percent for most food stamp households).[1]

Standard Deduction Freeze

The food stamp benefit formula is based on the expectation that families will purchase food using both food stamp benefits and a portion of their income.[2] Households with lower incomes receive higher food stamp benefits because they have less money available to purchase food.

Similar to federal income tax rules, the rules under which the Food Stamp Program operates allow households to subtract a “standard deduction” from their income, to reflect the basic costs of housing, utilities, transportation, and other inescapable living expenses. The standard deduction represents a portion of household income that is not available to purchase food because it must be used for other necessities. In the 1977 Food Stamp Act, Congress consolidated a number of deductions for specific expenses into the standard deduction.[3]

Prior to 1996, the standard deduction was indexed each year to account for inflation, in recognition of the fact that basic living expenses rise with inflation. The 1996 welfare law, however, froze the standard deduction at $134 for all household sizes. If the standard deduction had continued to keep pace with inflation, it would be $184 this fiscal year, $205 by fiscal year 2012, and $229 by fiscal year 2017, using CBO’s inflation projections.

The 1996 cut to the standard deduction continues to deepen with each passing year for households with one, two, or three members, even though the budget window in effect at the time of the 1996 welfare law (fiscal years 1997 through 2002) is over. As discussed below, because of a provision of the 2002 farm bill, households with four or more members are no longer losing ground, although most of these households still continue to have their benefits calculated using a standard deduction that is lower than it would have been under the pre-1996 rules.[4]

Today, the standard deduction cut accounts for about two-thirds of the benefit cuts to which the typical food stamp household is subject as a result of the 1996 law. Because of the standard deduction freeze, a typical single parent with two children receives benefits that are about $24 a month lower in fiscal year 2008 than they would be if the standard deduction had kept pace with inflation. By 2017, such a household’s benefits will be about $32 a month lower (in 2008 dollars) because of the standard deduction freeze.[5]

Reduction in the Maximum Benefit Level

The 1996 welfare law also reduced the Food Stamp Program’s maximum benefit level from 103 percent of the cost of USDA’s “thrifty” food plan (TFP) to 100 percent of the TFP. The maximum benefit had been set at 103 percent of the cost of TFP to reflect the fact that there is a four-to-16 month lag between the month for which USDA estimates the cost of the TFP (June of each year) and the months for which the benefit levels based on that cost are in effect (the following October through September — i.e., the following fiscal year). Because this three percent adjustment was repealed in 1996, food stamp benefits are no longer sufficient to purchase the thrifty food plan in any given month, because food stamp benefit levels reflect the cost of food in the previous June rather than current food costs.[6]

The maximum food stamp benefit for a household of three is about $13 a month lower because of this reduction in the maximum benefit made by the 1996 law. In 2017, food stamp benefits will remain about $13 a month lower (in 2008 dollars[7])

In the 1996 to 2002 budget window, this cut reduced benefits by more than the cut in the standard deduction did. But because the standard deduction cut continues to grow deeper each year, it has now overtaken the maximum benefit cut in terms of the magnitude of the benefit reductions it causes.

The Impact of the 1996 Cuts Depends on Household Circumstances

These two across-the-board cuts have affected nearly all food stamp households. Households that qualify for the Food Stamp Program’s excess shelter deduction because of their high housing expenses are subject to the deepest reductions. This is because the formula for calculating the shelter deduction magnifies the effect of the standard deduction cut.[8]

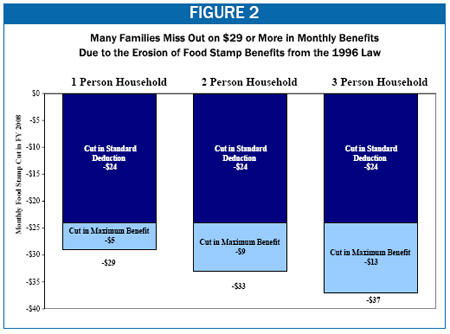

Figure 2 below shows the overall monthly benefit cut that typical households of one, two, and three persons will experience in fiscal year 2008 as a result of these cuts from the 1996 law. (The typical food stamp household has low income and high housing expenses and therefore qualifies for the excess shelter cost deduction.) About three-quarters of low-wage working families fall into this group.

Some households — those who do not qualify for the shelter deduction because they receive subsidized housing or otherwise have low housing expenses in relation to their income, and those whose shelter expenses are so high that they hit the cap on the shelter deduction — have been affected somewhat less by the cut in the standard deduction. These households, which account for about one-fifth of all food stamp households, have seen their food stamps cut about two-thirds as much as the typical household. In addition, two types of households are not affected by the changes in the standard deduction: those with very low or no income who receive the maximum food stamp benefit (they account for 30 percent of food stamp households) and households of one or two members who have relatively high incomes and low expenses and receive the $10 minimum food stamp benefit (about 5 percent of food stamp households). [9] See the appendix table at the end of this paper for the total amount of benefits lost to households in each state over the next ten years because of the freeze to the standard deduction.

The vast majority of households — 95 percent of them — are affected by the reduction in the maximum benefit, since the maximum benefit is the starting point for calculating food stamp amounts.[10] For households that already receive the maximum benefit (30 percent of food stamp households), the cut equals about 3 percent of their benefits. About two-thirds of households, however, are subject to a deeper cut in percentage terms. For a typical working-poor family of three (which has earnings equal to about 70 percent of the poverty line), the reduction in the maximum benefit enacted in 1996 lowers their monthly food stamp benefit by 4 percent. The percentage cut rises to almost 8 percent for a family of three with earnings at the poverty line.

Partial Fix in the 2002 Farm Bill

In the 2002 Farm Bill, Congress improved the standard deduction to help address the needs of larger households. The standard deduction is now set at 8.31 percent of the federal poverty income guidelines, which vary by household size, but at not less than the $134-a-month level that has been in effect since the mid-1990s. Varying the standard deduction by household size recognizes that larger families, which typically are families with children, incur greater expenses for necessities than smaller households do. Food stamp households with more members also typically fall farther below the poverty line than smaller households and experience a greater degree of hardship because they must stretch their limited incomes across more people.

The change in the standard deduction enacted in 2002 was beneficial to larger households. The standard deduction remains frozen at $134 a month, however, for households with three or fewer members. (The standard deduction now has risen above $134 a month for households of four or more; see Table 1.)

| Table 1: Current and Projected Standard Deduction Levels | |||

| Household Size | 2007 | Projected 2012 | Projected 2017 |

| 1 | $134 | $134 | $134 |

| 2 | 134 | 134 | 134 |

| 3 | 134 | 134 | 144 |

| 4 | 139 | 156 | 174 |

| 5 | 162 | 182 | 203 |

| 6 or more | 186 | 208 | 232 |

More than 75 percent of food stamp households have three or fewer members. Most households thus have yet to receive any relief from the standard deduction freeze enacted in 1996. Under current law, the standard deduction is scheduled to remain frozen at its current level of $134 until 2014 for three-person households, and until 2025 for two-person households.

As a result, the value of food stamp benefits will continue to erode for another seven years for households with three members and for another 18 years for households of two. For most one-person households, many of whom are elderly widows, the value of food stamp benefits will continue to erode for another 30 years, until 2038.

Congress’s decision in 2002 to set the standard deduction at 8.31 percent of the poverty line was driven by budgetary limitations in the 2002 Farm Bill process. In 2002, the Bush Administration (as well as senators from both parties, including Senators Lugar, Specter, and Kennedy) proposed setting the standard deduction at 10 percent of the poverty line.[11] The bill that the Senate subsequently passed was somewhat less generous than that, setting the standard deduction at a level that would have risen to 9 percent of the poverty line in 2010 and subsequent years. This Senate provision would have cost $2.2 billion over the ten-year budget window, however, and the Conference Committee ultimately provided only $1.5 billion for this purpose. As a result, the standard deduction level was scaled back in conference to 8.31 percent of the poverty line. (The House-passed bill took a different approach to the standard deduction at a cost or $1.4 billion.)

In other words, the level of 8.31 percent of the poverty line for the standard deduction was chosen so Congress could hit a particular budget target, rather than for substantive policy reasons. If the standard deduction had been set at 10 percent of the poverty line, households of three would no longer be facing further benefit erosion with each passing year, and for households of two, the freeze on the standard deduction would be lifted ten years earlier than under current law.

What Can be Done?

To restore the purchasing power of food stamp benefits, the standard deduction needs to be raised. To restore the standard deduction fully to its pre-1996 level for all household sizes, the standard deduction would be set at $188 in 2008 and annually adjusted for inflation. A typical household of three or fewer members would see its benefits increase by about $24 a month. This change would cost about $1.8 billion a year, or about $9 billion over five years. The Food Stamp Program would remain less effective in helping low-income families purchase a nutritionally adequate diet than it was prior to the 1996 law, due to the cut in the maximum benefit, but much of the lost ground would be recovered.

This level of resources, however, is not likely to be available in the 2007 farm bill. Accordingly, two other approaches are described below, which would partially restore the value of the standard deduction, at a substantially lower cost.

- End erosion of the standard deduction for households of three or fewer members. Under this approach, the standard deduction that households of one to three members receive would be adjusted annually for inflation, beginning in 2008. (Benefits for households of four or more would be unchanged; these are the households that benefited from the change in the standard deduction enacted in 2002, and the standard deduction for which they qualify already rises with inflation each year.) The cost of this improvement would be about $1.3 billion over five years.

The households that would be helped by this change would not regain any of the ground lost since 1996, but the real value of their food stamp benefits would stop deteriorating further with each passing year. Almost half of the benefits from this change (45 percent) would go to families with children. Slightly more than half would go to households with an elderly or disabled member.

- Improve on the 2002 Farm Bill Policy. An alternative is to improve the proposal enacted in 2002 and raise the standard deduction from 8.31 percent of the poverty line to 10 percent, as the Administration proposed in 2002. This would increase benefits right away for households of three (as well as larger households). Households of two would start to see an increase ten years earlier than under current law.

The cost of this proposal would be about $2 billion over five years.[12] Almost 60 percent of the benefits during this period would go to low-income working families, and virtually all of the benefits would go to families with children. (Over time, households of one and two would benefit as well.)

Because this provision helps larger as well as smaller families — and larger households tend to be poorer than smaller ones — this proposal is a more progressive change than the first option. Under this approach, however, households of two or fewer members would continue to experience a long delay before the erosion in their food stamp benefits ends. The 1996 benefit cut would continue to deepen until 2016 for households of two and until 2030 for households of one.

Conclusion

More than ten years after enactment of the 1996 law, the cuts in food stamp benefits contained in that law continue to deepen with each passing year and to affect most food stamp households, including most of the working poor and the elderly poor. Each year, food stamp households are able to purchase less food than the year before.

In the 2007 farm bill, Congress has the opportunity to take action to address this matter and to improve the adequacy of food stamp benefits for the nation’s neediest families.

End Notes

[1] The other 60 percent of the cuts came primarily from the termination of eligibility for certain legal immigrants and most unemployed childless adults, and from a number of other, smaller provisions. Part of the legal immigrant cut was subsequently reversed.

[2] Specifically, a household’s monthly food stamp benefits are equal to the maximum benefit for their household size (based on the cost of the thrifty food plan) minus 30 percent of the household’s net income (its gross income minus deductions).

[3] In addition to the standard deduction, current rules allow the following deductions: an earnings deduction for 20 percent of earnings, a dependent care deduction (which is capped), a child support deduction for amounts paid in child support, a medical expense deduction for out-of-pocket medical expenses above $35 a month that are incurred by household members who are elderly or have a disability, and an excess shelter deduction (which is capped) for shelter costs, including utilities, that exceed half of the household’s net income after all other deductions.

[4] Under current rules, the standard deduction for households of six or more is $2 a month higher than it would have been under the pre-1996 rules.

[5] In nominal terms (i.e., in 2017 dollars), the benefit cut from the standard deduction cut will be about $38 a month by 2017.

[6] The Food Stamp Act requires USDA to set the maximum food stamp benefit levels for each fiscal year based on the cost of the Thrifty Food Plan in June of the previous fiscal year.

[7] In 2017 dollars, the benefit reduction by 2017 from the maximum benefit cut will be about $15 a month for a household of three.

[8] A given household’s shelter deduction is equal to the amount by which its shelter expenses exceed half of its net income after other deductions, including the standard deduction. As a result, a cut in the standard deduction is counted one-and-a-half times for households that qualify for the shelter deduction.

[9] Eligible households with one of two members that qualify for a monthly benefit amount of less than $10 receive a $10 benefit.

[10] Only households that receive the $10 minimum benefit are not subject to a benefit cut because of the reduction in the maximum benefit.

[11] The poverty line is also the income eligibility limit for the Food Stamp Program: households generally must have net income (income after deductions are taken for certain expenses) at or below the poverty line.

[12] The estimated cost of the two alternatives over 10 years is the same: about $5 billion.

More from the Authors