Revisiting State Tax Preferences for Seniors

Summary

By the year 2030 one in five Americans will be over the age of 65 according to Census Bureau projections. Increasingly, state budgets will be stretched thin by the healthcare and other needs of the nation’s elderly. For example, states provide on average 47 percent of the funding for the Medicaid program, which pays for the vast majority of long-term care in this country and bears a portion of the prescription drug costs for low-income elderly people. States must finance pensions and health care for what will be a growing cadre of retired state employees. Elderly-related costs borne by state and local governments for a range of other programs ranging from special transportation to social services will also be increasing.

While these government costs will be rising, the revenue collections needed to cover the costs will be depressed in many states as the proportion of elderly in the population increases. This is because states provide a wide variety of income and property tax breaks to all elderly residents — regardless of their income. The cost of these special tax preferences will rise along with the increase in the elderly population. These preferences are widespread.

- Some 28 states completely exempt social security income from the income tax.

- Pension income is fully or partially exempt from taxation in 33 states.

- Nine out of ten states offer added income tax exemptions, standard deductions, or credits based on age.

- In addition, many states assist local governments with the costs of age-based property tax reduction programs. Some 26 states offer homestead exemptions or credits targeted to the elderly.

Data on the cost of at least some of these preferences is available for 22 states. Currently, the cost exceeds three percent of the state’s general fund budget in nearly one-third of these states (Illinois, Kentucky, Michigan, Mississippi, New York, North Carolina, and Pennsylvania). By 2030, the cost will grow to exceed three percent of the budget in three-fifths of these states. (The additional six states are Delaware, Idaho, Iowa, Missouri, Oklahoma, and Oregon.)[1] In four of the 22 states, the costs would exceed seven percent of the budget.

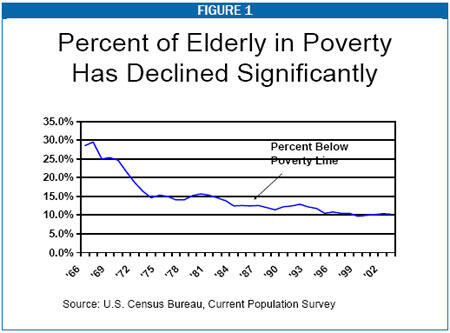

Decades ago, when many of these preferences were first established, elder poverty was much more widespread in the United States than today. In 1970, some 25 percent of the over-65 population had below-poverty income. It seemed reasonable at that time for states to attempt to relieve the tax burden on the elderly. Today, however, only 10 percent of the elderly are poor. (See Figure 1.) As a result, many state tax preferences for seniors that have long been in state tax codes now benefit taxpayers who have similar or better ability to pay taxes as other segments of the population. This raises questions about whether these tax preferences for the elderly make sense in the current context.

Moreover, in many states the special tax preferences do not help the lowest-income seniors. In states that generally do not tax people with incomes below or slightly above the poverty line, most of the special tax preferences for seniors are used only by somewhat higher income taxpayers. In states that levy their income tax with multiple rates that increase with income, it is the highest income seniors who benefit most from the preferences.

By better targeting income and property tax reductions on low-income seniors, states can free resources to pay for the growing needs of senior citizens while still assisting poor elder residents.

AARP’s Policy Director Addresses Issue of Non-targeted Breaks for Seniors

John Rother, AARP's Director of Policy and Strategy, made the following statement, “While surveys reveal many Americans feel they are overtaxed, US tax burdens are lower today than their average for the past several decades, and significantly lower than those in most developed countries. Tax relief is warranted for people who confront difficulties in meeting living expenses, but it is difficult to justify preferential treatment on age grounds alone or on the basis of receiving pension income. Property taxes are the least popular form of tax, especially in light of their recent escalation, and can pose significant problems for older persons wishing to remain in their homes.

“With the population aging and more people needing services, younger people, many of whom are struggling financially, will not be able to fill the revenue gap. Older Americans, who are the beneficiaries of so much of what government provides, understand this and the need to do their part.”

AARP is a nonprofit, nonpartisan membership organization of over 35 million people age 50 and older.

- More states could tax a portion of social security benefits when the recipient’s total income exceeds a specified amount — as the federal government does — rather than completely exempting social security income from taxation. Currently 12 states use the same income limits as the federal government for determining whether to tax social security benefits.

- States that offer exemptions for public or private pensions could phase them out at a specific income level or only offer them to taxpayers with incomes below a certain level. For example, as a part of a large tax package adopted in 2004, Virginia scaled back its preferential treatment of pension income by allowing the exemption to phase out for taxpayers at higher income levels.

- States could convert their age-based additional personal exemptions to a higher standard deduction, comparable to the one the federal government offers. This would target these preferences more to lower and middle income taxpayers.

- Additional states could rely more on means-tested property tax credits rather than homestead exemptions or credits. For example, under the provisions of credits known as “circuit-breakers” taxpayers receive a credit if their income is below a defined level and their property taxes exceed a specified percentage of their income. Currently, 34 states offer property tax circuit breaker programs; many of these are very limited programs, however, and some of the same states also offer homestead exemptions or credits that are not means-tested.

- States could raise the eligibility age for their age-based credits and exemptions in order to target them on the seniors who have less ability to pay. The percent of people 75 years old and older in poverty is higher than the percent of those between 65 and 75 in poverty (although the rates are still considerably below senior poverty rates of the past).

As states prepare for the spending challenges that the aging of the population will bring they should consider the revenue challenges as well. The time for states to reconsider their senior tax preferences is now, before the baby boom generation retires and the cost of the preferences begins to rise rapidly and it therefore becomes even more politically difficult to modify them.

Designing Change to Improve Chances of Adoption

A key question is whether it is politically possible to modify senior preferences in ways suggested in this report. Policymakers are aware that older Americans vote in disproportionate numbers, and that they are vocal in making their needs known. Nevertheless, it will become increasingly difficult for states to meet those needs if some of the preferences described here are not modified before the bulge of the baby boomers becomes qualified to take advantage of them. The following are some suggestions of ways to improve the political chances of enacting the needed changes.

- Include the changes in senior preferences in a larger tax reform package that may include other changes that seniors view favorably. Such offsetting changes might include taking the sales tax off food and/or pharmaceuticals or enacting an income-targeted credit to offset the sales tax on those items, or increasing another tax to fund specific services important to seniors. In addition, if the tax preferences for some other groups are also being changed, seniors may feel less singled out. The recent change in senior tax preferences in Virginia was made in the context of a larger tax reform.

- It may be possible to sit down with organizations representing seniors in the state and discuss their priorities. They may have priorities they consider more important than preferences for higher-income seniors, and may be open to using the revenue from curtailing the preferences or other revenue to fulfill those priorities.

- When proposing a change from a non-targeted preference to a targeted preference for seniors, it may be possible to set the income ceiling for the preference at a level that will encompass between a third and a half of all seniors in the state. This could help deflect opposition.

- It might be possible to make the preference more generous than it currently is for the lowest-income seniors, while eliminating it for seniors at higher incomes. This could garner support for the change.

- Many people at age 65 today do not consider themselves “old,” and few are poor. Poverty is higher at age 75 and higher still at age 85. It may be possible to re-target the senior preferences on an older cohort, rather than using age 65 as the qualifying age. Perhaps in combination with some of the other strategies above, this could improve the chances of support for the change.

- Retaining the tax preference for those already receiving it — grandfathering — could make the changes more acceptable because no one would lose a benefit that they are already receiving. In addition, phasing in the change rather than eliminating a benefit all at once could make it more palatable.

(21pp.)

End Notes

[1] There is little information collected on a regular basis on the cost of senior tax preferences to states. These estimates in are based on the costs of income tax preferences using information from state tax expenditure reports.

More from the Authors