Why The Cost of AMT Relief Should Be Included in Estimates of the Cost of Extending the President's Tax Cuts

The President’s budget estimates that extending the 2001 and 2003 tax cuts would cost $1.7 trillion over the next decade (2008-2017). (A figure of $1.6 trillion has been cited by a number of media outlets, but this number leaves out the increased outlays that will result from extending the refundable tax credit expansions enacted in 2001; the Administration’s estimate of the full costs of extending its tax cuts, including the tax credit expansions, is $1.7 trillion.)

The Administration’s figure, however, is deceptive. The Administration’s budget reflects the cost of only one year of relief (2007) from the Alternative Minimum Tax. In estimating the cost of extending the President’s tax cuts, the budget assumes that AMT relief then will end and that the AMT will mushroom after that and cancel out, for tens of millions of taxpayers, part of the very tax cuts the President proposes to extend, thereby lowering the tax cuts’ cost.

According to the Congressional Research Service, “absent congressional action, the AMT will ‘take back’ most of the tax relief granted through the regular income tax.” CRS calls attention to Congressional Budget Office estimates that show that “the total cost (both direct and indirect [i.e. including interest costs]) of extending the EGTRRA/JGTRRA tax cuts and reforming the AMT will be $3.5 trillion over the FY2008 through 2017 period.”[1]

An estimate that excludes the cost of continued AMT relief, as the Administration’s $1.7 trillion figure does, can not convey the true cost of the President’s tax policies for two basic reasons.

- First, it is extremely unlikely that lawmakers will allow AMT relief to expire and permit the AMT to hit upwards of 40 million households by 2013. The President’s budget includes AMT relief for 2007 in order to prevent the AMT from exploding and hitting about 20 million households this year. It is not plausible that AMT relief will be allowed to end after 2007 and ultimately affect more than 40 million taxpayers.

Furthermore, it clearly is not the Administration’s policy to allow the AMT to swell in this manner. Administration officials, like members of Congress of both parties, have said it is unacceptable for the AMT to expand dramatically in the years ahead, and no observer believes this will be allowed to occur. [2] Cost estimates based on the assumption that it will occur are highly unrealistic.

- Second, if AMT relief is allowed to expire, the AMT will cancel out a substantial portion of the very tax cuts the Administration says it wants to extend. This will happen because taxpayers owe the Alternative Minimum Tax whenever their tax liability, as calculated under the AMT, is higher than their tax liability under the regular income tax. The 2001 and 2003 tax cuts sharply reduce households’ tax liability under the regular income tax but do not change the structure of the AMT. As a result, with the tax cuts in place, AMT liability would exceed regular income tax liability for millions more households. These households would owe tax based on their AMT, rather than on their regular income-tax liability, and consequently would lose some or all of their tax cuts.

According to the Urban Institute-Brookings Institution Tax Policy Center, if AMT relief is allowed to expire, the AMT will take back more than a quarter of the President’s tax cuts by 2010. When the President urges that his tax cuts be made permanent, he presumably means all of the tax cuts, not just the less-than-three-fourths that will remain if AMT relief is not provided.

For these reasons, assuming that AMT relief expires yields an estimate of the President’s proposed policy that is artificially low, as it excludes the cost of the one-fourth of the tax cuts that would be cancelled out by the AMT. To avoid underestimating the cost of making the President’s tax cuts permanent, it is necessary to include the cost of AMT relief.

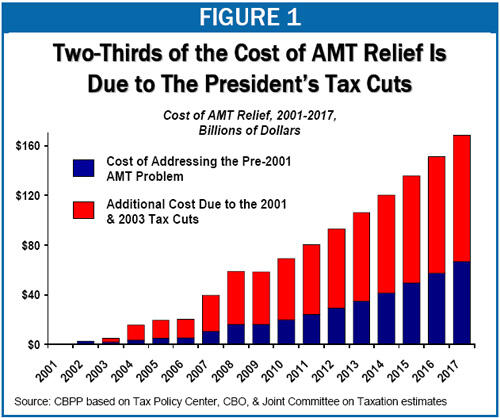

Including the cost of AMT relief is particularly warranted because the bulk of that cost simply reflects the cost of providing taxpayers with the full value of the 2001 and 2003 tax cuts. Estimates from the Tax Policy Center indicate that the cost of providing AMT relief through 2017, assuming the tax cuts are made permanent, will be about three times what it would have cost to provide relief from the AMT growth that would have occurred if the tax cuts had not been enacted.[3] In other words, about two thirds of the cost of AMT relief is due to the tax cuts.

As noted, CBO estimates that making the 2001 and 2003 tax cuts and AMT relief permanent would cost $3.5 trillion through 2017, including added interest costs. The Tax Policy Center estimates suggest that only about $400 billion of that cost represents the cost of addressing the preexisting AMT problem. The rest represents the direct costs of the 2001 and 2003 tax cuts plus the additional cost of AMT relief that is entirely a result of those tax cuts.

End Notes

[1] Gregg A. Esenwein, “Extending the 2001, 2003, and 2004 Tax Cuts,” Congressional Research Service, November 16, 2007. See also Aviva Aron-Dine, “Extending the President’s Tax Cuts and AMT Relief Would Cost $3.5 Trillion Through 2017,” Center on Budget and Policy Priorities, January 31, 2007, https://www.cbpp.org/1-31-07tax.htm.

[2] The Administration has said that the AMT should be reformed and that the reform should be paid for as part of a broader, deficit-neutral tax reform. But the Administration’s estimates of the cost of extending the tax cuts depend on the assumption that the AMT is left unchanged, grows dramatically, and cancels out a substantial portion of these tax cuts, reducing their cost. Moreover, the Administration has never actually proposed a broader, deficit-neutral tax reform.

[3] Estimates of the cost of addressing the pre-2001 AMT problem are based on Tax Policy Center estimates of the cost of indexing the 2000 AMT exemption level for inflation (and allowing non-refundable personal credits under the AMT), as of 2000.

More from the Authors