House Child Tax Credit Bill Leaves Behind Millions of Low-Income Working Families

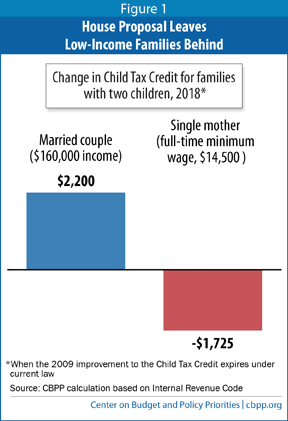

The bill permanently alters the CTC by extending it higher up the income scale so that more families with six-figure incomes can benefit from it, while failing to make permanent a key CTC improvement for working-poor and near-poor families that is slated to expire at the end of 2017. As a result, a married couple with two children making $160,000 a year would receive a new tax cut of $2,200 in 2018 under the bill. But a single mother with two children who works full time throughout the year at the minimum wage of $7.25 an hour (which House leaders oppose raising) and earns just $14,500 would lose $1,725. Her CTC would disappear altogether (see Figure 1).

The bill also indexes the current maximum credit of $1,000 per child to inflation, but that would benefit only those with incomes high enough to receive the maximum credit amount.

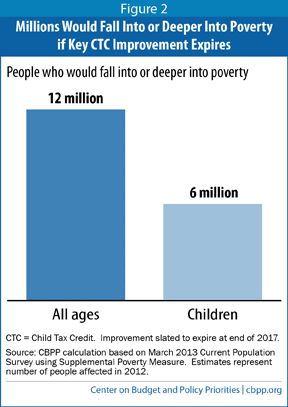

Middle-income families with children would get a small benefit from the bill’s indexing provision. But the big winners would be the more-affluent families who would become newly eligible for the CTC. The losers would be millions of low-income families who are doing exactly what policymakers often say they want these people to do — working, even at low-wage jobs. Census data show that letting the Child Tax Credit improvement for low-income working families expire after 2017 would push 12 million people — including 6 million children — into or deeper into poverty.

The bill’s CTC expansions would cost $115 billion over ten years.[1]

Bill Ignores Critical Child Tax Credit Improvement Set to Expire After 2017

Policymakers established the CTC on a bipartisan basis in 1997 to help defray the high costs of raising children and substantially expanded the credit in 2001 as part of the Bush tax cuts. Yet the Child Tax Credit, as established by those pieces of legislation, had a large hole — most working-poor families with children were either ineligible for the credit altogether or received only a partial credit, because their wages were too low for them to qualify for the full credit. The very working families that most needed the credit to help with the costs of raising their children were partially or entirely shut out.

Policymakers made substantial progress in addressing this flaw in 2009. They did so by lowering the level of family earnings at which the CTC begins to phase in to $3,000, so that families with very low earnings could get a partial credit, and so a family with two children could start to receive the full credit when its earnings reached $16,333 (rather than a considerably higher level). This enabled the CTC to reach more working-poor families while boosting the credit for many near-poor working families that had been receiving only a partial credit. The 2009 law also increased the Earned Income Tax Credit (EITC) for families raising three or more children and provided more marriage-penalty relief in the EITC.

In 2010, policymakers extended these CTC and EITC improvements, along with the Bush tax cuts, and they thus were scheduled to expire together at the end of 2012. As their price for agreeing to extend the CTC and EITC improvements for working families in 2010, however, Republican negotiators secured a hefty increase in the amount that the heirs of the wealthiest estates could inherit tax free. This change benefited the heirs of the estates of the wealthiest one-third of 1 percent of Americans who die.[2] The 2012 “fiscal cliff” deal then made this generous tax cut for the biggest estates permanent (along with the bulk of the Bush tax cuts), even as it extended the CTC and EITC improvements for low- and moderate-income working families only through 2017.

The Bill’s Misguided Priorities

The CTC legislation coming to the House floor has three notable features:

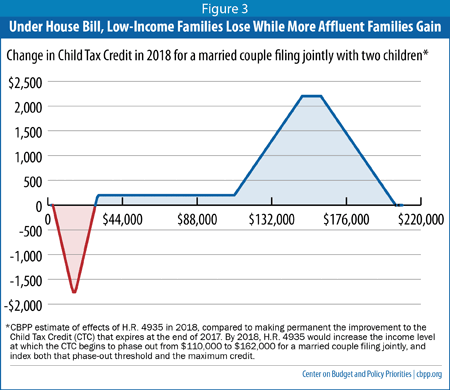

- It permanently extends the Child Tax Credit higher up the income scale so more families with six-figure incomes will benefit. It raises the income levels at which the CTC begins to phase out and indexes those thresholds to inflation. Couples with two children making between $150,000 and $205,000 would become newly eligible for the credit; a family making $160,000, for example, would receive a new tax cut of $2,200 in 2018.

- It fails to make permanent the 2009 reduction in the CTC’s earnings threshold, set to expire at the end of 2017. If this provision expires, a single mother with two children who works full time throughout the year at the minimum wage and earns $14,500 would lose her full CTC of $1,725 in 2018.

- It indexes the current maximum credit of $1,000 per child to inflation. This provision would not help most working families with low or moderate incomes, because it benefits only those with incomes high enough to receive the maximum credit. If the credit’s $3,000 earnings threshold (the level of family earnings at which the credit starts to phase in) is allowed to expire at the end of 2017, the threshold will nearly quintuple — and families making less than about $14,500 will lose their CTC altogether. In addition, many working families with incomes somewhat above $14,500 will have their CTC cut substantially and no longer receive the maximum credit, which will make the inflation adjustment meaningless for them. Under the House bill, indexing would not benefit a family with two children in 2018 until the family has earnings of at least $28,050 — nearly double full-time work at the minimum wage.

In sum, the bill’s big losers would be lower-income working families with children, even as its big winners are more affluent families, as Figure 3 shows.

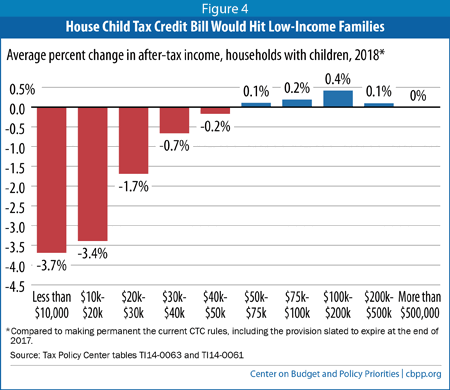

On average, families with children that have incomes between $100,000 and $200,000 would gain nearly $550 apiece in 2018, while families with incomes below $40,000 would be worse off, according to the Urban-Brookings Tax Policy Center (TPC). The TPC analysis also shows that, under the bill, after-tax incomes in 2018 would fall by an average of more than 3 percent among households earning less than $20,000, while rising among households with incomes between $100,000 and $200,000 (see Figure 4).

End Notes

[1] Joint Committee on Taxation (JCT) score of H.R. 4935 as voted on and passed by House Ways and Means Committee, https://www.jct.gov/publications.html?func=startdown&id=4625. The bill the House is scheduled to consider adds an offset, not yet scored by JCT, which would decrease the net cost of the bill.

[2] Robert Greenstein, “Disparate Treatment: Permanent, Million-Dollar Estate-Tax Breaks for Wealthy Heirs Vs. Temporary Tax Credit Improvements for Low-Income Working Families,” Off the Charts blog, January 4, 2013, http://www.offthechartsblog.org/disparate-treatment-permanent-million-dollar-estate-tax-breaks-for-wealthy-heirs-vs-temporary-tax-credit-improvements-for-low-income-working-families/

[3] CBPP calculation using the March 2013 Current Population Survey using the Supplemental Poverty Measure. Estimates represent number of people affected in 2012.

[4] CBPP estimate of veteran and active-duty families as a share of total families with children that would lose out if the CTC improvement expires (3.75 percent), based on the March 2013 Current Population Survey, applied to Tax Policy Center estimate of total families with children who would lose if these benefits expire (TPC table T14-0010).

[5] CBPP estimate of veteran and active-duty families as a share of total families with children that would lose out if the CTC and EITC improvements expire (5.9 percent), based on the March 2013 Current Population Survey, applied to Tax Policy Center estimate of total families with children who would lose if these benefits expire (TPC table T14-0033).

More from the Authors

Areas of Expertise