Florida’s “Amendment 4” Would Cause Tax Rate Increases and Deep Local Service Cuts, Likely Harming the State’s Economy

Amendment 4, which appears on the ballot in Florida in November, would lock a deeply flawed set of property tax changes into the state’s constitution, leading to tax increases for large numbers of Florida residents, a competitive disadvantage for new and emerging businesses, and significant cuts in local services — while producing little if any economic benefit.

The amendment would reduce the taxable value of certain types of property, mainly properties that are not primary residences (such as large corporations, other businesses, and part-time residences). To a lesser extent, it would also reduce the taxable value of homes owned by first-time homebuyers, and certain properties whose market value is decreasing. (While the property tax is a local tax, the state can restrict local governments’ ability to collect property taxes. Amendment 4 is an example of such a restriction).

Proponents claim that Amendment 4 would boost Florida’s economy and fix key flaws in the property tax system. These claims are off base. In reality, the amendment would:

- Raise taxes on many established, year-round residents. Property taxes in Florida are a key source of funding for local services such as fire and police protection, providing 60 percent of counties’ general fund revenues and 42 percent of cities’ revenues. [1] If Amendment 4 is adopted, local governments would have to raise property tax rates in order to preserve funding for these services. This in turn would increase property taxes on those who benefit least from the amendment — established, full-time homeowners not affected by the recapture rule — in order to pay for tax cuts for those who benefit most from the amendment, such as part-time residents, out-of-state corporations and first-time homebuyers.

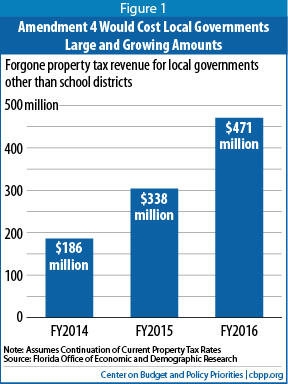

- Require local governments to make deep cuts in services. To the extent that local governments don’t respond to Amendment 4 by increasing property tax rates, it would take a large and growing bite out of funding for local services like police and fire protection. At current rates the local revenue loss from Amendment 4 would grow to $471 million by 2016[2] — the equivalent of 7,656 police officers at the state’s average annual police salary.[3] And the revenue loss would begin phasing in at a time when local government revenues are already down as a result of the recession.

Local governments would almost certainly respond to Amendment 4 with a combination of tax rate increases and service cuts. - Harm Florida’s economy. These tax increases and spending cuts mean that Amendment 4 is no free lunch for Florida taxpayers. As noted above, any tax cuts for non-residents and out-of-state corporations that result from the measure would require offsetting tax increases or cuts in local services. Either of these steps would remove demand from the economy, undermining Amendment 4’s potential to spur economic growth.

Supporters of Amendment 4 cite a study by Florida Tax Watch, a Florida research organization, as evidence that Amendment 4 would benefit Florida’s economy. But the study suffers from a crucial methodological flaw. While the study takes into account the economic benefit of the taxpayer savings that would result from the amendment, it ignores the tax increases or cuts to local services that local governments would need to enact to pay for the tax cut. It therefore gives a deeply misleading estimate of Amendment 4’s likely economic impact. - Send millions of dollars in tax benefits out of state. Much of the tax savings from Amendment 4 would be sent outside the state. This is because out-of-state shareholders in major corporations with Florida landholdings and owners of second homes who may spend much of their time and money in other places would get a large share of the benefit from Amendment 4.

As a result, the net effect would be to cost Florida jobs, not create them. - Hurt new and expanding businesses — important engines of job growth. Amendment 4 would ultimately place newer businesses at a competitive disadvantage by requiring them to pay more in property taxes than their more established competitors, even if the newer and more established businesses own identical properties. Tilting the playing field against newer businesses makes little economic sense. Important new research suggests that a small number of relatively new businesses create a disproportionate share of new jobs. Making those businesses pay more property taxes than their competitors will further harm the state’s economy.

Amendment 4 appears on the ballot alongside another measure that poses a serious threat to local services. Amendment 3 would place a severe limit on state revenue growth, and in so doing would very likely squeeze state aid to local governments. Because local governments get a substantial share of their funding from the state, such cuts could punch a large hole in local budgets, precipitating significant local service cuts and tax increases. Paired with the revenue loss from Amendment 4, the impact would be even more dramatic.

What Is Amendment 4?

Amendment 4, slated to appear on the ballot on November 6, would place three distinct property tax changes into Florida’s constitution. It would:

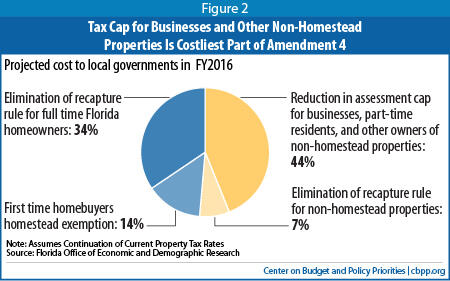

- Lower, from 10 percent to 5 percent, the cap on the annual growth in the assessed (taxable) value of “non-homestead” properties — that is, properties that are not owner-occupied, year-round residential properties, ranging from major corporate properties to the second homes of non-Floridians (increases in assessed value that result from improvements to a property are not subject to the cap).[4] This item is the biggest in the package, costing local governments $243 million, nearly half of the amendment’s total costs, by FY2016.

- Create a property tax exemption for first-time Florida homebuyers (full-time Florida homeowners who have not owned a home in Florida over the last three years). The exemption would initially be worth half of the property’s value, up to the county’s median home value, and would phase out over five years. This is probably the most politically popular item in the package, but it actually accounts for a small share of the dollars — just $78 million, or 14 percent of the amendment’s total tax reduction in FY2016.

- Permit the Florida legislature to eliminate Florida’s “recapture” rule, which allows a property’s assessed value to rise even if its market value declines if the assessed value is lower than the market value. (Florida caps the annual growth in a property’s assessed value. If a property’s market value is growing faster than the cap, a gap emerges between the home’s market value and its taxable value. If the property’s market value subsequently falls but remains above its taxable value, the recapture rule requires the taxable value to continue to increase until it catches up to the property’s market value). This provision would benefit not just year-round owner-occupied homes, but also corporate, rental, and other kinds of non-homestead properties. Repeal of the recapture rule for homestead properties would cost local governments and school districts $188.3 million in FY2016, or 34 percent of the amendment’s total costs. Repeal for non-homestead properties would cost local governments $41 million (7.5 percent of the amendment’s costs).

The first two changes would apply only to property taxes imposed by local governments other than school districts; the third applies to both school district and non-school district taxes

Amendment Would Require Deep Cuts in Services or Tax Increases for Many Year-Round Homeowners

Amendment 4 would force local governments to choose between raising taxes on large numbers of year-round Florida homeowners, making deep cuts to local services, or some combination of the two.

Florida Tax Watch Study Fails to Make the Economic Case for Amendment 4

Supporters of Amendment 4 frequently cite a study by Florida Tax Watch, a Florida research organization, as evidence that Amendment 4 would spur economic growth. But the study suffers from a crucial methodological flaw and therefore gives an extremely optimistic estimate of Amendment 4’s likely economic impact.

While the study takes into account the economic benefit of the taxpayer savings that would result from the amendment, it ignores the tax increases or cuts to local services that local governments would need to enact to pay for the tax cut. As noted above, those offsetting measures would wipe out the economic benefit of any tax savings that Amendment 4 provides.*

Florida Tax Watch’s omission of the negative economic impact of lost local government revenue is all the more perplexing because past Florida Tax Watch analyses of property tax cut proposals took this impact into account. For example, a 2007 Florida Tax Watch study found that property tax reductions would result in job losses. That 2007 study specifically noted: “The job losses [from the property tax cut] will be due to a reduction in local government spending.” **

Because Florida Tax Watch’s analysis of Amendment 4 ignores the impact of lost local revenue, the study’s findings — that the Amendment would create jobs and otherwise spur Florida’s economic recovery — are deeply misleading. Indeed, Amendment 4 would more likely kill jobs in Florida and damage the state’s economy because it would result in money that would otherwise be spent paying the salaries of Florida police officers, firefighters, and librarians and more generally funding local services, flowing outside the state.

* See “Analysis of the Fiscal and Economic Impact of Amendment 4” Florida Tax Watch, June 2012, available at http://www.floridataxwatch.org/resources/pdf/Amendment4FINAL.pdf . The analysis “assumes a net-zero fiscal impact for local government revenues.” (see pg.13).

** See “Model Predicts Florida Economy Will Gain By Property Tax Cut Without Changing Sales Tax,” Florida Tax Watch, May 2007, pg. 7.

Tax Increases

Property taxes are the single largest source of revenue for Florida’s local governments. Florida counties, for example, get 60 percent of their General Fund revenues from property taxes, while cities get 42 percent of their revenues from property taxes. [5] Aside from education, Florida property taxes pay for a range of local services, including jails, fire and emergency medical services, sheriffs’ and police departments, road maintenance, public transportation, parks, and libraries.

If Amendment 4 passes the only way that local governments could sustain funding for these services would be by increasing property tax rates. Doing so would mean raising taxes on everyone in a local jurisdiction, including large numbers of Florida property owners who do not benefit from the amendment — namely, established, year-round homeowners not affected by the recapture rule. These homeowners would essentially pay higher taxes to finance the tax cuts for the people who most benefit from the amendment: business owners and other owners of non-homestead properties, first-time homebuyers, and owners of properties subject to the recapture rule. As Orange County Property Appraiser Bill Donegan has said of Amendment 4, “The homeowners are going to pick up the tab.”[6]

Cuts to Services

Florida property tax collections are already deeply depressed. As a result of a previous round of large property tax cuts and the collapse of the Florida real estate market, non-school district property taxes have fallen sharply in recent years and are now 8 percent below 2005 levels, after adjusting for inflation.[9] And because the Florida real estate market has been slow to recover, property tax revenues are expected to see slow growth at best for the foreseeable future.

In response to falling revenues Florida local governments have been making deep cuts to services over the last several years. The city of Jacksonville, for example, laid off 48 police officers in 2011.[10] Pinellas County laid off 211 employees who worked on road repair, parks, and utilities among other areas in 2010.[11] Hillsborough County cut an afterschool program serving more than 1,800 children in 2011.[12] An additional revenue loss from Amendment 4 would likely lead to further cuts, and make it harder for local governments to restore services as the economy recovers.

Amendment 4 Is Unlikely to Boost Florida’s Economy

There are a number of reasons to doubt proponents’ claims that the amendment would help to revive Florida’s economy.

Amendment’s Tax Cuts Would Require Offsetting Tax Increases or Spending Cuts

As the preceding section points out, any tax cuts that result from Amendment 4 would require offsetting tax increases for those who benefit least from the amendment or cuts in local services. Either of these steps would undermine Amendment 4’s potential to spur economic growth.

To the extent that local governments raised taxes to offset the need for service cuts, this would simply shift tax liabilities from one group of taxpayers to another, doing little to boost overall demand.

Moreover, when local governments cut spending they lay off employees, cancel contracts with vendors, and eliminate or lower payments to businesses and non-profit organizations that provide direct services. In all of these circumstances, the companies and organizations that would have received the government payments have less money to spend on salaries and supplies, and individuals who would have received salaries have less money for consumption. This directly removes demand from the economy.

Amendment’s Tax Savings Are Poorly Targeted for Economic Growth

The majority of Amendment 4’s tax savings benefit large corporate-held properties, second homes, and other non-homestead properties. This results mostly from the reduction in the state’s assessment growth cap for non-homestead properties from 10 to 5 percent. Over time, this tighter cap — combined with the non-homestead portion of the recapture rule elimination — would produce over half of the tax savings from the amendment’s three provisions (see Figure 2), costing local governments over $284 million per year by FY2016.[13]

Amendment 3: Another Serious Threat to Local Services

Another question on the November ballot also poses a serious threat to local services like police and fire protection. Amendment 3 would limit annual state revenue growth to the combined rate of inflation and population growth, a formula that cannot keep pace with the normal costs of maintaining existing public services over time. In Colorado, the only state to have tried such a formula, it led to drastic cuts in public services. For example, between 1992, when Colorado’s limit was implemented, and 2001, Colorado fell from 35th to 49th in the country in K-12 spending as a percentage of personal income. In November, 2005, Colorado citizens voted to suspend the formula for five years, to stanch the deluge of harmful budget cuts.*

Florida’s police and fire departments and other local services depend on state support to operate. They get a fixed percentage of certain state revenue sources. Such shared state revenue is providing $4 billion for local governments (including school districts) in the current fiscal year.**

By forcing steep cuts in state revenues, Amendment 3 would almost certainly erode state aid for local governments, either automatically or through a vote of the legislature.

- If the state reduced tax rates to keep revenues within Amendment 3’s revenue cap, the amount of revenue shared with local governments would decline automatically because the state shares a fixed percentage of its revenue with localities.

- If the state kept rates unchanged, it would be required by Amendment 3 to deposit any revenue above Amendment 3’s revenue cap in a reserve fund and then use any additional money to reduce school district property taxes. Amendment 3 does not specify what would happen to revenue shared with local governments in this situation. Since overall state revenue collections and the percentage of revenue that goes to local governments would both be unchanged, the total amount of shared revenue that localities receive might be unchanged as well. But, given Amendment 3’s tight revenue cap, the state could avoid cutting local aid only by deeply cutting funding for state programs. It is highly likely that lawmakers would shrink the percentage of state revenues that go to localities in order to lessen the need for severe cuts to state services.

Whether cuts to local aid result automatically or through a vote of the legislature, they would damage local budgets, precipitating significant local service cuts or local tax increases, or both. Paired with the revenue loss from Amendment 4, their impact would be even more dramatic.

* See Iris J. Lav and Erica Williams, “A Formula for Decline: “Lessons from Colorado for States Considering TABOR,” Center on Budget and Policy Priorities, March 15, 2010, available at https://www.cbpp.org/cms/?fa=view&id=753 .

** See “Long Term Revenue Analysis FY1970-71 to 2020-21” Florida Revenue Estimating Conference, Fall, 2011. Available at http://edr.state.fl.us/Content/conferences/longtermrevenue/2011longtermrevenueanalysis.pdf.

A significant share of these savings will be spent outside the state. Many beneficiaries of the tighter assessment cap and the recapture rule will be the shareholders across the nation and around the world who own stock in large corporations, many with headquarters outside of Florida. Others are owners of second homes, who spend much of their time and money in other places.

Some supporters of Amendment 4 claim that the cap will speed Florida’s economic recovery by providing the tax reduction and certainty that businesses need to hire new workers and expand their operations. This claim is overstated.

Corporations typically decide to expand their operations based upon anticipated increases in demand for their goods or services. If they do not anticipate growing demand, they are unlikely to hire additional workers or invest in new plants or equipment, regardless of their future property tax liabilities. And the cap does not actually provide businesses with certainty about their future property tax bills. The property taxes that businesses pay could increase by more than five percent if local governments increase property tax rates.

Another claim from Amendment 4 supporters — that the cap will result in a flood of new investment in Florida — is also overstated. It would, for example, do little to attract businesses from other states. Businesses generally base their location decisions on factors like the skill of a state’s workforce and the proximity to markets and suppliers. A tighter property tax cap will not change those fundamentals. Total state and local taxes, including property taxes, are just 2.3 percent of overall expenses for the average corporation.[14] Moreover, businesses typically have strong economic and social ties to their current location, making relocation very costly and limiting the chances that any tax savings resulting from a tighter assessment cap would lure a large number of businesses to Florida.

Amendment 4 Would Put New and Expanding Businesses at a Competitive Disadvantage

Beyond failing to boost Florida’s economic recovery, Amendment 4 places newer and expanding businesses, key engines of job creation, at a competitive disadvantage.

This is a consequence of the amendment’s assessment cap for businesses and other non-homestead properties. Businesses that have just acquired property would initially get no benefit from the cap; instead, they would need to pay property taxes on the full market value of their property. The primary beneficiaries of the cap would be established businesses that see their property’s value grow by more than 5 percent for a number of years. For these businesses, the cap would hold their property’s taxable value below the price that the property would sell for on the open market. Over time, the tighter cap would make it more likely that newer businesses would pay more in property taxes than their more established competitors, even if the newer and more established businesses own identical properties.

Tilting the playing field against new and expanding businesses makes little economic sense. Much research suggests that newer companies create a disproportionate share of new jobs.[15] For example, firms that have just come into existence make up just three percent of total employment, but account for almost 20 percent of total job creation, according to a recent study by researchers at the University of Maryland and the Census Bureau. Newer firms have high rates of failure, but if they survive, these firms grow more rapidly than their more established peers.[16]

Amendment 4 would make it even more difficult for newer firms to survive by requiring them to pay higher property taxes than their more established competitors. The rapid job growth that dynamic new businesses have the potential to generate will be essential to putting Floridians back to work and growing the state’s economy over the longer term.

End Notes

[1] CBPP calculation using data from Florida’s Department of Financial Services' Bureau of Local Government. Local Fiscal Year 2009.

[2] Revenue loss for local governments other than school districts. CBPP calculation using the most recent estimates from Florida’s Revenue Estimating Conference.

[3] CBPP calculation using Bureau of Labor Statistics data, http://data.bls.gov/cgi-bin/dsrv. CBPP projection of average 2016 salary based on past salary growth.

[4] Assessment growth for year-round owner occupied residences is currently capped at the lesser of 3 percent or the rate of inflation.

[5] CBPP calculation using data from Florida’s Department of Financial Services' Bureau of Local Government

[6] Mary Shanklin, “Homeowners may pick up property tax slack if amendment passes in November,” Orlando Sentinal, June 21, 2012.

[7] CBPP calculation using data from Florida’s Department of Economic and Demographic Research and Department of Revenue.

[8] CBPP calculation using Bureau of Labor Statistics Data, http://data.bls.gov/cgi-bin/dsrv. CBPP projection of average 2016 salary based on past salary growth

[9] CBPP analysis of Florida Department of Revenue Data

[10] Jim Schoettler and Steve Patterson, “48 Jacksonville Cops Laid Off as Standoff Continues Between Sheriff, Union,”, The Florida Times-Union, October 5, 2011, http://jacksonville.com/news/crime/2011-10-04/story/48-jacksonville-cops-laid-standoff-continues-between-union-sheriff.

[11] David Decamp, “Pinellas to Lay Off 211 County Workers,” June 25, 2010, The Tampa Bay Times, http://www.tampabay.com/news/localgovernment/pinellas-to-lay-off-211-county-workers/1104668 .

[12] Mike Salinero, “Hillsborough Commissioners End After School Program,” The Tampa Tribune, July, 27, 2011, http://www2.tbo.com/news/news/2011/jul/27/4/hillsborough-commissioners-end-after-school-progra-ar-246688/.

[13] CBPP calculation using the latest estimates from Florida’s Revenue Estimating Conference.

[14] For a detailed discussion of this figure, see note 4 in Michael Mazerov and Mark Enriquez, “Vast Majority of Large Maryland Corporations Are Already Subject to “Combined Reporting” in Other States,” Center on Budget and Policy Priorities, November 9, 2010. Available at https://www.cbpp.org/sites/default/files/atoms/files/11-9-10sfp.pdf.

[15] See, for examply, Magnus Henrekson and Dan Johanson, “Gazelles as Job Creators: A Survey and Interpretation of the Evidence,” Journal of Small Business Economics, January 6, 2009, pp. 227-244.

[16] John Haltiwanger, Ron S. Jarmin, Javier Miranda, “What Creates Jobs? Small vs. Large vs. Young,” National Bureau of Economic Research, August 2011, available at http://www.nber.org/papers/w16300.pdf?new_window=1 .

More from the Authors