Repatriation Tax Holiday Would Increase Deficits and Push Investment Overseas

Proponents Are Distorting Joint Tax Committee Analysis

Despite proponents' claims to the contrary, a proposal to enact a second tax holiday for the profits that U.S.-based multinational corporations bring back to the United States from foreign accounts would cost tens of billions of dollars in federal revenue — boosting deficits and debt – while not achieving its proponents' promise of more jobs and higher investment in the United States.

Its cost is particularly troubling given the high expectation of failure. In recent days, leading private analysts have raised serious doubts about the proposal. Goldman Sachs concluded that, with a holiday, "we would not expect a significant change in corporate hiring or investment plans." [1] Fitch Ratings added that a holiday would not likely "support growth-oriented investment by U.S. firms."[2] A holiday also would violate the "do-no-harm" rule because it ultimately would encourage corporations to shift investment, profits, and jobs overseas.

Proponents, part of a massive lobbying campaign for the tax holiday, are distorting an analysis by the congressional Joint Committee on Taxation (JCT) on the proposal's budgetary impact. JCT found that the proposal would boost revenues initially, as companies took advantage of the holiday to repatriate some profits they otherwise would have kept overseas for a number of years. But, JCT explained, the proposal would also reduce revenues by giving companies a large tax break for those profits they would have repatriated anyway in the next few years, even without the holiday, and by giving companies a strong incentive to shift more profits overseas in the future, in anticipation of future tax holidays. JCT found that the net impact of these three different revenue effects would be to reduce revenues by $79 billion over ten years.

Proponents of the tax holiday, by focusing just on the proposal's short-term revenue gain and ignoring the larger revenue losses JCT identified, wrongly claim that the holiday would not increase deficits or indeed may even raise revenues. Some misleadingly argue that companies are willing to repatriate foreign income only under a holiday, so that all of the revenue derived from repatriations during a holiday represents a windfall to the Treasury. This is simply false: corporations have repatriated an average of $129 billion every year since the 2004 holiday (adjusted for inflation).

A second tax holiday would also reward and encourage corporate tax avoidance. The evidence indicates that a significant share of the profits that multinational corporations book in low-tax foreign jurisdictions is, in economic terms, attributable to domestic economic activity — that these "overseas profits" were, through complicated accounting maneuvers, shifted overseas on paper specifically to avoid U.S. corporate taxes. A valuable new report[3]from the Senate's Permanent Subcommittee on Investigations shows that, during the first repatriation holiday in 2004, seven of the nineteen surveyed corporations received over 90 percent of their repatriations from tax haven countries. A second holiday for repatriated profits would enable firms that have avoided U.S. taxes in this way to bring sheltered earnings back at a greatly reduced tax rate — encouraging them and other firms to shift more income earned from investments in the United States and other non-low-tax countries to offshore tax havens.

The mistaken belief that a tax holiday would generate a net increase in federal revenues has sparked proposals to pair it with investments in other priorities, most notably an infrastructure bank. While the United States badly needs infrastructure improvements, a repatriation tax holiday cannot finance such a bank — or anything else — for the simple reason that it costs money rather than raises it. Policymakers would have to cut other priorities, potentially including infrastructure funding itself, to pay for this revenue loss.

At a time when policymakers are focusing on reducing long-term deficits and scaling back tax loopholes — and when both the economy and the job market remain weak — it would be irresponsible to enact a tax holiday that increases deficits, rewards corporate tax avoidance, and ultimately shifts jobs and investments overseas.

Lobbying Campaign Misrepresents Joint Tax Committee Analysis

JCT, Congress' official scorekeeper on tax matters, recently analyzed the potential effects of a repatriation tax holiday on tax receipts and the economy.[4] The analysis drew on information from companies' current financial positions and recent behavior as well as extensive evidence from the 2004 American Jobs Creation Act, which established a one-year holiday similar to a number of the current proposals. JCT found that a second repatriation holiday would have three separate effects on revenues, compared to what would happen in absence of a holiday:

- It would encourage corporations to repatriate foreign earnings that they would otherwise have kept overseas over at least the medium term. This would increase revenues in the short term.

- It would give companies a large tax break for other foreign earnings that they would have repatriated even without a holiday. This would decrease revenues.

- It would increase incentives for companies to shift jobs, profits, and investments overseas in anticipation of future holidays. This, too, would decrease revenues.

The combined effect of these three factors is that a holiday would raise revenues initially but would cost the Treasury considerably more in later years — for a ten-year net revenue loss of $79 billion (see Figure 1).

Some proponents of the tax holiday argue that, contrary to JCT's findings, a repatriation holiday would "increase rather than reduce federal government revenues."[5] They reach that conclusion by focusing exclusively on the proposal's revenue- raising effect while ignoring the two much larger, revenue-losing effects that JCT identified. JCT's cost estimate reflects the net result of all three effects, making this policy a major loser of both revenue and domestic investment.

More broadly, a recent study[6] on which some proponents are relying — sponsored by the private New Democratic Network (NDN) — charges that JCT's methodology is "flawed conceptually." But, in fact, it's the analysis in the NDN study that does not withstand scrutiny. The NDN study alleges that JCT vastly underestimated the repatriations that occurred from fiscal 2004 to 2008 but, in doing so, the study grossly mischaracterizes both JCT's projection and the level of actual repatriations during those years. Moreover, NDN's revenue estimate ignores the crucial fact that a second repatriation holiday would encourage corporations to shift income and future investments overseas, thereby substantially draining future corporate tax revenues. (For a full analysis of the flaws in the NDN study, see the appendix.)

The following sections more closely examine each effect that, according to JCT, the proposal would have on revenues.

1) Holiday Would Raise Revenues Initially by Boosting Repatriated Profits

Although the profits of U.S.-based corporations' foreign affiliates are subject to the U.S. corporate tax, companies pay no taxes on this income until they "repatriate" it, or bring it back to the parent corporation from abroad. This structure allows such firms to defer payment of U.S. corporate income tax on their overseas profits indefinitely.

The deferral feature costs the federal government significant revenue: the Office of Management and Budget estimates it will cost $213 billion over the 2012-2016 period, making it one of the single largest corporate tax expenditures (i.e., targeted tax breaks) in the tax code. It also gives multinationals an incentive to shift economic activity — as well as their reported profits — overseas.

In response to this incentive, many companies have accumulated significant profits overseas, perhaps as much as $1.5 trillion. [7] Some critics have implied that the JCT's analysis rests on the false assumption that companies would repatriate the bulk of these profits at the regular tax rate if there were no holiday. But the JCT made no such assumption. Its estimate reflects the fact that, as companies' prior behavior clearly indicates, a portion — not most or all — of the profits repatriated under a holiday would be repatriated anyway (with the remainder of those profits remaining overseas).[8]

2) Holiday Would Lose Revenues by Giving Large Tax Break for Profits That Firms Would Have Repatriated Anyway

While a tax holiday would lead corporations to repatriate some profits that they would not have repatriated at the full statutory tax rate, it would also provide a large tax break on profits that corporations would have repatriated even without the tax break. The resulting revenue loss would likely offset most if not all of the revenue gain from increased repatriations.

A central theme of the lobbying campaign for the tax holiday is that companies are willing to repatriate overseas income only under a holiday. "[T]he money held overseas simply isn't coming back if tax rates for bringing back global earnings remain at the current levels," according to WINAmerica.[9]

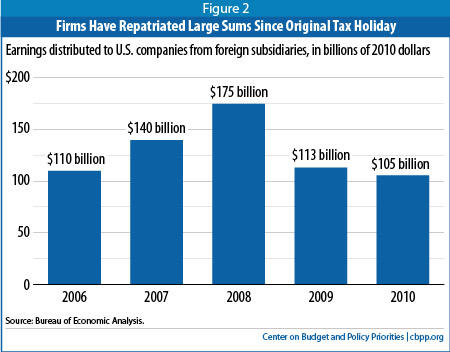

These claims, however, are difficult to square with the fact that foreign corporations have repatriated an average of $129 billion every year since the 2004 holiday (adjusted for inflation)[10], and have paid U.S. corporate income taxes on these repatriated profits.[11] Just last year — even as lobbyists were working to deliver a second tax holiday — U.S. multinationals brought home $105 billion in overseas profits (see Figure 2). Moreover, research suggests that a major reason why companies are not repatriating even higher amounts — and why they have built up so much foreign cash in the first place, as explained below — is that they believe Congress will enact a second repatriation holiday.

Providing very large tax breaks on those profits that companies would have repatriated anyway (the 2004 holiday allowed corporations to repatriate foreign profits at a low 3.7 percent effective tax rate[12]) can prove very costly. If the temporary rate offered under a second repatriation holiday is very generous, as under the first holiday, the policy would very likely reduce revenue and increase deficits overall even if the bulk of the money that companies repatriated would have remained abroad in the absence of a holiday.

In short, even if one believes — despite overpowering evidence to the contrary — that nearly all profits currently held overseas will remain there indefinitely if Congress doesn't provide a second tax holiday, it remains the case that any new holiday is likely to provide such generous terms that the Treasury will still lose money. (Moreover, as strong as this effect is, JCT concluded that a second revenue-losing effect — that a second repatriation holiday would encourage companies to shift still more income and investments overseas in the future — is even stronger; this effect is discussed in the next section of this paper.)

3) Holiday Would Encourage Firms to Shift More Profits and Investment Overseas, Worsening Revenue Losses

Currently, firms that shift income to foreign tax havens generally understand that, while they will be able to defer tax as long as they leave their profits abroad, they will generally have to pay U.S. corporate income taxes when the profits are repatriated. This knowledge acts as a restraint (albeit a weak one) on decisions to shift investments overseas primarily for tax reasons. If Congress enacts another tax holiday, however, rational corporate executives will almost certainly conclude that more tax holidays are likely in the future and will adjust investment and tax decisions accordingly. They will almost certainly move more investment and jobs overseas and book more profits abroad, and keep the profits there while they wait for another tax holiday in which the vast bulk of those profits will be exempt from tax.

In other words, the expectation of future tax holidays will make firms more inclined to shift income into tax havens and less likely to reinvest earnings in the United States — precisely the opposite of what lobbyists promote the measure as accomplishing.

The JCT singles out this factor as the biggest reason why a second holiday would lose substantial revenues: "Enactment of a [repatriation holiday] for a second time in seven-year period likely signals to taxpayers that something like [this holiday] will become periodic, if not a permanent, feature of the Code." As a result, it "encourages investment and/or earnings to be located overseas."

JCT is not alone in its predictions:

- A 2009 study by tax experts Lee Sheppard and Martin Sullivan found that, between 2003 and 2007, firms that had participated in the tax holidaydoubled the average annual increase in the amount of cash they held overseas, from $60 billion to $122 billion. [13] Their data, "show multinationals are loading up on unrepatriated earnings at a far greater rate than before the tax holiday legislated in 2004," Sheppard and Sullivan concluded.Image

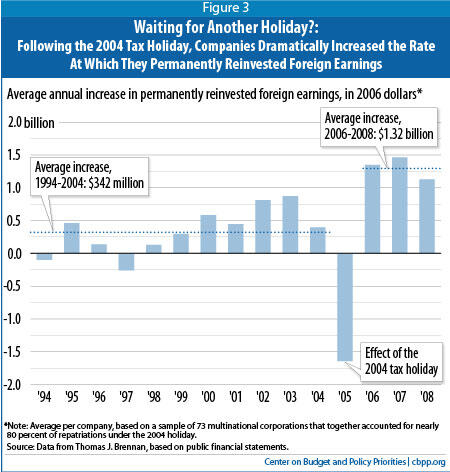

- A 2010 study by Northwestern University law professor Thomas J. Brennan strongly suggests that firms, anticipating a second holiday, have already aggressively shifted profits overseas. Analyzing the public records of a large group of U.S. multinationals that together accounted for 79 percent of the repatriations that occurred under the 2004 holiday, Brennan found that "since the holiday window, there has been a dramatic increase in the rate at which firms add to their stockpile of foreign earnings kept overseas."[14] In each of the three years following the 2004 tax holiday, these companies increased the amounts of new "permanently reinvested" foreign earnings by three times as much, on average, as they had in the each of the ten years before the holiday (see Figure 3).

- A new report from the Senate Permanent Subcommittee on Investigation's majority staff provides still more evidence, finding that, "Since the 2004 AJCA repatriation, the corporations that repatriated substantial sums have built up their offshore funds at a greater rate than before the AJCA, evidence that repatriation has encouraged the shifting of more corporate dollars and investments offshore." [15]

- Also in a new report, Goldman Sachs wrote, "Two 'one-time' holidays in less than a decade could change incentives going forward: Another 'one-time' holiday may condition US multinationals to never routinely repatriate any foreign profits because, eventually, Congress can be expected to pass another 'one-time' tax holiday. If so, this would constitute a significant structural change in US tax policy." [16]

Not surprisingly, lobbyists promoting a second holiday do not highlight the expectation that a second holiday would encourage multinationals to invest overseas instead of at home. As a result, many policymakers remain unaware of it.

First Tax Holiday Failed as Stimulus — and Second One Would, As Well

Proponents of a repatriation holiday often frame it as an economic stimulus measure, contending that corporations would use the repatriated profits to expand in the United States and thereby boost economic growth and create large numbers of jobs. This is the same pitch that proponents used to sell Congress on the 2004 tax holiday, and studies by the National Bureau for Economic Research, the Congressional Research Service, the Treasury Department, and numerous outside analysts have found no evidence that the 2004 holiday had any of the promised positive economic effects.

To the contrary, there is strong evidence that firms primarily used the repatriated earnings to benefit owners and shareholders, and that the restrictions Congress imposed on the use of the repatriated earnings — aiming to ensure that firms invested them in the United States — proved ineffective. In fact, many of the firms that repatriated large sums during the holiday actually laid off workers.

Before enactment of the 2004 holiday, President Bush's Council of Economic Advisers concluded that it "would not produce any substantial economic benefits."a A subsequent review by National Bureau of Economic Research (NBER) researchers found that the holiday "did not increase domestic investment, employment, or [research and development]."b Similarly, the Congressional Research Service (CRS) reported that the various studies "generally conclude that the reduction in the tax rate on repatriated earnings . . . did not increase domestic investment or employment."c The JCT reached the same conclusion: "the research has shown little macroeconomic benefit" from the 2004 holiday.

A second holiday would likely result in a similar policy failure. Goldman Sachs recently concluded that it "would not expect a significant change in corporate hiring or investment plans."d Fitch Ratings similarly concluded that, under a repatriation holiday, "most multinationals would likely return repatriated cash to shareholders through share repurchases and dividends rather than investing cash in U.S. growth projects or reduce debt."e

The reason is simple: when the economy is weak, the primary problem that firms face is a shortage of demand for their products, not a shortage of cash. Companies currently already have on hand over $2 trillion of domestic cash and liquid assetsf — cash that they are not investing because they have concluded that the investment opportunities do not exist. Adding to firms' vast domestic cash supply via a massive tax giveaway is unlikely to change this calculus or lead to significant new investment. As a recent Bank of America Merrill Lynch analysis concluded, "Today, businesses are investing slowly not because their tax burden is high but because demand for goods and services is soft. Supply-side measures such as a tax repatriation holiday will have limited effect in what remains a demand-deficient economy."g

Some argue that a tax holiday would strengthen the dollar as firms converted their foreign profits to dollars to repatriate them, marginally increasing the demand for dollars. However, the bulk of many firms' foreign profits is likely already in dollars.h Even if the demand for dollars did rise significantly, that would make American-made goods more expensive abroad and foreign imports cheaper in the United States — threatening U.S. jobs rather than creating them. As a result, CRS researcher Jane Gravelle has written, "U.S. exports would temporarily decline, further straining the economy and at least partially offsetting any stimulative effect of the repatriated earnings."

a "Letter to the Honorable Charles E. Grassley," October 4, 2004.

b Dhammika Dharmapala, Kristin J. Foley, and C. Fritz Forbes, "Watch What I Do, Not What I Say: The Unintended Consequences of the Homeland Investment Act," NBER Working Paper, June 2009.

c Donald J. Marples and Jane G. Gravelle, "Tax Cuts on Repatriation Earnings as Economic Stimulus: An Economic Analysis," Congressional Research Service, January 30, 2009.

d Goldman Sachs, U.S. Daily: Profit Repatriation Tax Holiday: Still an Uphill Climb, Alec Phillips, October 5, 2011.

e Fitch Ratings Press Release "Fitch: Proposed Repatriation Tax Relief Bill Unlikely to Drive U.S. Investment" October 6, 2011.

f See for example Ben Casselman and Justin LaHart, "Companies Shun Investment, Hoard Cash," Wall Street Journal, September 17, 2011, http://online.wsj.com/article/SB10001424053111903927204576574720017009568.html .

g Bank of America Merrill Lynch "Repatriation Games," Economic Commentary, July 7, 2011.

h This is because most US multinationals are U.S. dollar denominated public companies, and would be unlikely to want to risk huge fluctuations in their accounting profits by holding large amounts of liquid assets in anything other U.S. dollars.

Repatriation Holiday Would Reward and Encourage Tax Avoidance

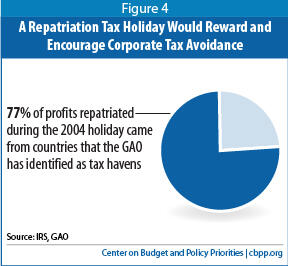

A repatriation tax holiday would encourage companies not only to invest more overseas, but also to shift income earned from investments within the United States to tax-haven countries. Evidence suggests that firms earned the bulk of the "overseas profits" for which they now seek a tax holiday in the United States and then shifted them overseas to avoid U.S. taxes. IRS data show that 77 percent of profits repatriated under the 2004 tax holiday came from subsidiaries incorporated in countries that the Government Accountability Office has identified as tax havens, including Bermuda, Switzerland, and the Cayman Islands (see Figure 4).[17]

As Edward Kleinbard, former staff director of Congress' Joint Committee on Taxation and a leading tax expert, has noted, "Much of these earnings overseas are reaped from an enormous shell game: Firms move their taxable income from the U.S. and other major economies — where their customers and key employees are in reality located — to tax havens."[18] Indeed, by funneling profits overseas on the hope that Congress would eventually grant a second repatriation holiday, companies have played a large role in creating the very problem from which they now seek relief.

Consider the following recent examples:

- Bloomberg News has reported that Cisco Systems has reduced its U.S. income taxes by $7 billion since the last repatriation holiday by shifting large amounts of profits to a foreign subsidiary.[19]Image

- Last April, Bloomberg News reported that Google had "cut its taxes by $3.1 billion in the last three years using a technique that moves most of its foreign profits through Ireland and the Netherlands to Bermuda." Through complex accounting maneuvers, the article noted, "The earnings wind up in island havens that levy no corporate income taxes at all."[20]

- More recently, the New York Times reported that General Electric had used "innovative accounting that enables it to concentrate its profits offshore" to eliminate its U.S. corporate tax liability in 2010, despite having reported profits of $14.2 billion. [21]

All three companies are members of the coalition that is lobbying Congress to enact a second repatriation holiday.

As Lee Sheppard and Martin Sullivan have written: "The principal effect of another repatriation holiday would be to reward multinationals for shifting income out of the United States to low-tax jurisdictions."[22] (Goldman Sachs analysts described the 2004 holiday as the "no lobbyist left behind" act.[23])

Holiday Would Also Make It Harder to Enact Corporate Tax Reform

Some proponents of a second repatriation holiday have argued that the net revenue losses JCT estimates that a holiday would produce starting in 2014 are irrelevant because Congress will enact corporate tax reform well before then. This argument does not withstand even cursory scrutiny.

Enacting a revenue-losing repatriation tax holiday would obviously result in a lower baseline of projected revenues. If, as the Administration favors, Congress subsequently enacted a revenue-neutral corporate tax reform package — one that raises the same amount of revenue as under existing law — such a package would not recoup the revenue loss from a repatriation holiday; instead, those revenue losses would be locked into the tax code permanently. Moreover, the business community prefers a corporate tax reform package that would generate lower revenues than under current law.

Holiday Could Not "Pay for" Infrastructure bank — or Anything Else

Some have proposed enacting a repatriation tax holiday and using the proceeds to pay for an infrastructure bank designed to help address the country's large infrastructure needs. As explained above, however, the holiday would cost money, not raise it. As Edward Kleinbard recently said, "You're starting $80 billion in the hole with repatriation . . . so there's no net money to go into an infrastructure bank or anywhere else." [24] Instead, a holiday would put even more budget pressure on infrastructure investments by adding to budget deficits.

Conclusion

The research organization e21, which includes a number of former officials in the George W. Bush Administration, has stated:

A special repatriation tax holiday is hardly good policy; it is likely to result in a substantial net reduction in revenue because of the expectation it creates for future holidays, and would lessen the pressure that would otherwise exist for fundamental tax reform. … In fact, it is not clear what public policy goals this proposal would advance — if done outside a broad based reform of the code — aside from the near term interests of a relatively small number of large firms that want to avoid paying corporate income taxes on foreign-sourced earnings. [25]

Futhermore, granting another holiday would induce companies to shift even more income and investment abroad, likely resulting in less domestic investment and fewer jobs. And it would increase deficits and debt.

The first tax holiday was an expensive mistake. The consequences of repeating it would be even more costly.

Appendix: Study Claiming That Tax Holiday Would Raise Revenue Is Deeply Flawed

The NDN study, discussed briefly on page 4, claims that JCT in 2004 "forecast total repatriations of $235 billion for the period FYs 2004-2008 by companies [participating in the tax holiday]" but that actual repatriations over that period were "nearly $687 billion," or $452 billion above the JCT estimate. There are several problems with this claim:

- First, JCT's $235 billion figure was not an estimate of total repatriations. It was, instead, JCT's estimate of the amount of repatriated dividends that would qualify for the tax holiday — a wholly different thing. [26]

- Second, JCT's $235 billion estimate applied not to the full 2004-2008 period, as the NDN study claims, but solely to the holiday period. (Companies could claim the tax benefit during any single tax year that began between October 2003 and October 2005; 86 percent of corporations chose 2005, the others chose 2004 or 2006.) The NDN study argues that the JCT "assumed negligible repatriations in the years following the expiration of the lower rate"—but JCT has never released its projection of repatriations over those subsequent years. In fact, this assertion is almost certainly incorrect. Moreover, the NDN study effectively assumed that JCT did not expect a single company to repatriate earnings of any sort once the holiday expired — an assumption JCT clearly would not have made because it would have contradicted the historical evidence.

- Third, NDN compares the JCT's estimate to what it calls "actual repatriations" between 2004 and 2008. But NDN's figure for "actual repatriations" — $687 billion — refers to the amount of repatriations of all dividends received from foreign corporations, not just those eligible for the tax holiday. The authors note this mischaracterization and admit that "our numbers do change" if they do not make the untenable assumption that 100 percent of received foreign dividends are distributed by affiliated corporations."[27]

According to the IRS, firms claimed $312 billion in dividends that qualified for the tax deduction, according to the IRS. While this is more than JCT had estimated, the difference ($77 billion) is only about one-sixth of the $452 billion difference that NDN alleges. And these IRS data cannot shed any light on the more important question: how much would companies have repatriated anyway in the absence of the holiday?

The NDN study's claim that repeating the tax holiday would raise federal revenues similarly is deeply flawed:

- The study fails to account for the crucial fact that a repatriation holiday would encourage corporations to shift income and future investments overseas, at substantial cost to future corporate tax revenues. Two independent studies of the effect of the 2004 holiday on investment decisions — by Thomas J. Brennan and by Lee Sheppard and Martin Sullivan — found strong evidence that firms responded by increasing the rate at which they shifted income and investments overseas. JCT lists this factor as the single largest driver of a second holiday's budget costs. The Congressional Research Service also identifies it as an important factor. In addition, as cited above, Goldman Sachs recently argued [28] that a second repatriation holiday "could change incentives going forward" by "condition[ing] US multinationals to never routinely repatriate any foreign profits" in anticipation of additional temporary tax holidays. The NDN study ignores this factor.

- The NDN study assumes that after a second holiday, repatriations would "return to their trend growth rate" — defined as the average between 1994 and 2003 (i.e., before the first tax holiday). The study justifies this highly dubious assumption by noting that repatriations in the years following the 2004 holiday increased rather than decreased. But, in light of the evidence that companies have shifted investments overseas in expectation of a second holiday, the increase in the level of repatriated dividends likely masks a decline in the percentage of foreign earnings that are being repatriated.

By boosting firms' expectation that future Congresses will enact still more tax holidays, a second tax holiday will likely prompt them to reduce the amounts of foreign earnings that they repatriate during non-holiday years, reducing tax revenues during those years. NDN's questionable assumption that this will not happen is not shared by neutral analysts like JCT, financial analysts, and the Congressional Research Service. - The NDN study assumes that the effective U.S. tax rate on earnings repatriated after another tax holiday will be 10.26 percent, but acknowledges that this "estimated tax rate may be too high." Indeed, it is likely too high, significantly skewing the study's revenue estimate. NDN derives its 10.26 percent figure from a study of repatriations that occurred between 1999 and 2004. However, the precedent of the 2004 holiday likely encouraged multinationals to repatriate, in non-holiday years, earnings that would require lower amounts of U.S. tax (because they could be offset with associated foreign tax credits),[29] while holding overseas, in anticipation of a future holiday, most income that would otherwise attract a relatively high amount of U.S. tax. That would reduce the effective U.S. tax rate on earnings repatriated in non-holiday years, thereby raising the budgetary cost of the holiday.

The estimates in the NDN study are highly sensitive to this estimated residual tax rate. In fact, the NDN study's finding — that a repatriation holiday will likely boost revenue — disappears if the 10.26 percent is too high by even one-half of one percentage point.

End Notes

[1] Goldman Sachs, U.S. Daily: Profit Repatriation Tax Holiday: Still an Uphill Climb, Alec Phillips, October 5, 2011.

[2] Fitch Ratings Press Release "Fitch: Proposed Repatriation Tax Relief Bill Unlikely to Drive U.S. Investment" October 6, 2011, http://www.marketwatch.com/story/fitch-proposed-repatriation-tax-relief-bill-unlikely-to-drive-us-investment-2011-10-06 .

[3] "Repatriating Offshore Funds: 2004 Tax Windfall for Select Multinationals." United States Senate Permanent Subcommittee on Investigations Majority Staff, October 11, 2011. http://levin.senate.gov/download/repatriating-offshore-funds.

[4] "Letter to Rep. Lloyd Doggett," April 15, 2011.

[5] WinAmerica Campaign website, accessed September 14, 2011, http://www.winamericacampaign.org/myth-vs-fact/.

[6] Robert J. Shapiro and Aparna Mathu, "The Revenue Implications of Temporary Tax Relief For Repatriated Foreign Earnings: An Analysis of the Joint Tax Committee's Revenue Estimates," http://ndn.org/paper/2011/revenue-implications-temporary-tax-relief-repatriated-foreign-earnings-analysis-joint-tax .

[7] Bank of America Merrill Lynch.

[8] JCT explains the effect here: "[Some] taxpayers would accelerate the repatriation of dividends to qualify for section 965 [the tax holiday]: some of these dividends … would not otherwise be repatriated in the budget period (nor perhaps for many years after that)."

[9] WinAmerica Campaign website, accessed September 14, 2011, http://www.winamericacampaign.org/myth-vs-fact/.

[10] U.S. International Transactions Accounts, Bureau of Economic Analysis.

[11] These data include repatriations from foreign corporations in which U.S. corporations have only minority ownership, which would not qualify for a second repatriation tax break.

[12] Section 965 of the Internal Revenue Code, which established the 2004 tax holiday, allowed multinational corporations to deduct 85 percent of qualifying dividends received from their controlled foreign corporations (CFCs). If companies paid the top corporate tax rate of 35 percent on the remaining 15 percent of their repatriated profits, the effective tax rate would have been 5.25 percent. But about 30 percent of even that reduced tax liability was eliminated by foreign tax credits. As a result, the effective rate was actually closer to 3.7 percent. See Edward D. Kleinbard and Patrick Driessen, "A Revenue Estimate Case Study: The Repatriation Holiday Revisited," Tax Notes Special Report, September 22, 2008.

[13] Lee A. Sheppard and Martin A. Sullivan, "Multinationals Accumulate to Repatriate," Tax Notes, January 19, 2009.

[14] Thomas J. Brennan, "What Happens After a Holiday?: Long-Term Effects of the Repatriation Provision of the AJCA," Northwestern Journal of Law and Social Policy, Spring 2010.

[15] U.S. Senate Permanent Subcommittee on Investigations majority staff report, Repatriating Offshore Funds: 2004 Tax Windfall for Select Multinational, October 11, 2011.

[16] Goldman Sachs, U.S. Daily: Profit Repatriation Tax Holiday: Still an Uphill Climb, Alec Phillips, October 5, 2011.

[17] List of tax haven countries taken from Government Accountability Office, "International Taxation: Large U.S. Corporations and Federal Contractors with Subsidiaries in Jurisdictions Listed as Tax Havens or Financial Privacy Jurisdictions", GAO-09-157, December 2008, http://www.gao.gov/new.items/d09157.pdf. Data on source of repatriated dividends are from Melissa Redmiles, "The One-Time Dividends-Received Deduction," Internal Revenue Service Statistics of Income Bulletin, Spring 2008, http://www.irs.ustreas.gov/pub/irs-soi/08codivdeductbul.pdf.

[18] Jesse Drucker, "Biggest Tax Avoiders Win Most Gaming $1 Trillion U.S. Tax Break," Bloomberg News, June 28, 2011, http://www.bloomberg.com/news/2011-06-28/biggest-tax-avoiders-win-most-gaming-1-trillion-u-s-tax-break.html .

[19] Ibid.

[20] Jesse Drucker, "Google 2.4% Rate Shows How $60 Billion Lost to Tax Loopholes," Bloomberg News, October 21, 2010, http://www.bloomberg.com/news/2010-10-21/google-2-4-rate-shows-how-60-billion-u-s-revenue-lost-to-tax-loopholes.html .

[21] David Kocieniewski, "G.E.'s Strategies Let It Avoid Taxes Altogether" New York Times, March 24, 2011, http://www.nytimes.com/2011/03/25/business/economy/25tax.html?pagewanted=all .

[22] Lee A. Sheppard and Martin A. Sullivan, "Repatriation Aid for the Financial Crisis?" Tax Notes, January 5, 2009.

[23] Elliot Blair Smith, "Tax breaks let firms repatriate profit", USA Today, http://www.usatoday.com/money/companies/2005-01-10-jobs-act_x.htm .

[24] Richard Rubin, "Bill Clinton Backs Tax Holiday on Foreign Profits, With Caveats," Bloomberg News, July 1, 2011, http://www.bloomberg.com/news/2011-07-01/bill-clinton-backs-tax-holiday-on-foreign-profits-with-caveats.html .

[25] e21 editorial, "Tax Reform: Repatriation's Siren Song," http://economics21.org/commentary/tax-reform-repatriations-siren-song .

[26] The tax benefit was available for "extraordinary dividends" (those in excess of a calculated average amount received from the foreign subsidiary over the previous five tax years), and the maximum amount of qualifying repatriated earnings equaled the greater of $500 million or the amount of earnings that the firms' most recent financial statement listed as being permanently reinvested abroad. In all, $50 billion of dividends that firms repatriated during the holiday did not qualify for the tax deduction.

[27] The authors justify their assumption by noting that repatriations from controlled foreign corporations (CFCs) accounted for the large majority of total repatriations in 2004 and 2006. But those years overlap with the first repatriation tax holiday—when CFC repatriations were subject to a large tax break and, therefore, constituted a higher than usual share of total repatriations.

[28] Goldman Sachs, U.S. Daily: Profit Repatriation Tax Holiday: Still an Uphill Climb, Alec Phillips, October 5, 2011.

[29] The U.S. corporate tax code allows companies to use tax credits for foreign taxes paid in one jurisdiction to reduce U.S. taxes paid on income derived from another foreign jurisdiction. In the absence of a holiday, many companies time their repatriations from high-tax countries (which generate foreign tax credits) to offset repatriations from lower-taxed countries (which generate less in offsetting foreign tax credits), a practice known as cross-crediting or "filling the base." But as Kleinbard and Dreissen point out, during the 2004 holiday, "taxpayers no longer needed to use those high-taxed foreign-source dividends to shelter from tax any such low-tax foreign-source dividends" (or to shelter other foreign income). As a result, it is likely that taxpayers will in non-holiday years repatriate a greater proportion of income from high-tax jurisdictions (thereby generating offsetting tax credits) than they would either in holiday years, or than they would have in the non-holiday years prior to the first dividend repatriation tax holiday. This would lower the effective US rate of tax on repatriations in non-holiday years well below the effective rate reported for years before the first repatriation tax holiday. See Edward Kleinbard and Patrick Driessen, "A Revenue Estimate Case Study: The Repatriation Holiday Revisited" Tax Notes Special Report, September 22, 2008.

More from the Authors

Areas of Expertise

Areas of Expertise