What the 2011 Trustees' Report Shows About Social Security

On May 13, the Social Security Board of Trustees issued its annual report on the program’s financial status. [1] The trustees’ report shows some mild deterioration in the program’s short- and long-term outlook — a finding that was widely expected and well within the range of past revisions.

Several key points emerge from the new report:

- The trustees estimate that the combined Social Security trust funds will be exhausted in 2036 — a year earlier than they forecast in last year’s report.

- After 2036, Social Security could pay three-fourths of scheduled benefits using its annual tax income. Those who fear that Social Security won’t be around when today’s young workers retire misunderstand the trustees’ projections.

- The program’s shortfall is relatively modest, amounting to 0.8 percent of Gross Domestic Product (GDP) over the next 75 years (and 1.45 percent of GDP in 2085). A mix of tax increases and benefit modifications — carefully crafted to shield recipients of limited means and to give ample notice to all participants — could put the program on a sound footing indefinitely.

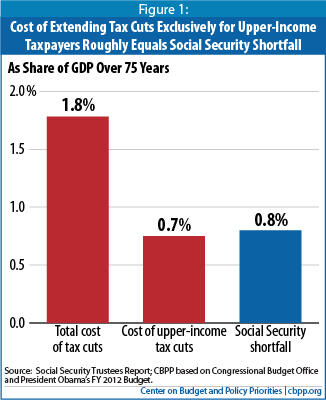

- The 75-year Social Security shortfall is only slightly larger than the cost, over that period, of extending the 2001 and 2003 tax cuts for the richest 2 percent of Americans (those with incomes above $250,000 a year). Members of Congress cannot simultaneously claim that the tax cuts for people at the top are affordable while the Social Security shortfall constitutes a dire fiscal threat. And the shortfall is well under half the cost over 75 years of making all of the 2001 and 2003 tax cuts permanent.

- Preserving and building upon the cost-control measures enacted in the 2010 health reform law will be important not only to Medicare, but — to a lesser degree — to Social Security as well.

Report Holds Few Surprises

The trustees’ report focuses on the outlook for the next 75 years — a horizon that spans the lifetime of just about everybody now old enough to work. The trustees expect the program’s tax income to remain near today’s levels, at about 13 percent of taxable payroll. [2] Meanwhile, the program’s costs are expected to climb to over 17 percent of taxable payroll — up from 12.5 percent today. Over the entire 75-year period, the trustees put the Social Security shortfall at 2.22 percent of taxable payroll; the shortfall is concentrated in the later years of the projection. Expressed as a share of the nation’s economy, the shortfall is 0.8 percent of GDP.

Both of these widely-cited figures include a buffer for a target trust-fund balance at the end of 2085. Without that buffer — which is set at 100 percent of the next year’s estimated Social Security outlays — the shortfall would be 2.1 percent of taxable payroll or 0.7 percent of GDP.

It’s no accident that the program will grow steadily over the next 25 years, peaking at 6.2 percent of GDP (up from 4.8 percent today) around 2035 and falling slightly after that. While Social Security provides a safety net to people in all age groups — to young children and their surviving parents who have lost a family breadwinner, to working-age adults who have suffered a disability, and to retired workers and elderly widows and widowers — about three-fourths of its benefits go to people age 65 or older. The share of the population that is 65 or older will climb steeply through 2035, from just under 13 percent today to 20 percent. Social Security’s increase in cost as a percentage of GDP roughly mirrors that pattern. This confirms that Social Security’s fundamental challenge is demographic, traceable to a rising number of beneficiaries rather than to escalating costs per beneficiary.[3]

The size of the shortfall over the next 75 years is similar to previous trustees’ forecasts (see Table 1) and represents a mild deterioration from last year’s report. Of the slippage in the new forecast — which equals 0.30 percent of taxable payroll over 75 years — the actuaries attribute half (0.14 percentage points) to revisions in demographic assumptions, specifically to slightly lower death rates and lower immigration. The actuaries ascribe another 0.05 percentage points of the slippage to the simple passage of another year (the 75-year valuation period now spans 2011 through 2085, rather than 2010 through 2084, and thus includes one less year in which the program’s finances were strong and one more year in which it will be running a significant deficit). Lingering economic weakness explains another 0.06 percentage points of the deterioration, and all other changes are minor. Changes of this magnitude are well within recent bounds and are not alarming.

Superficially, the new numbers return us to the deficits that the trustees projected in the late 1990s. In the reports for 1995 through 1998, the trustees similarly estimated a 75-year gap of about 2.2 percent of payroll. But in fact, the new estimates are somewhat more sanguine. The 1997 report, for example, spanned the period through 2071; this year’s report goes through 2085. In the meantime, we’ve moved more than a decade closer to the baby boomers’ retirement and the long-term aging of America’s population. The 1997 report projected trust fund depletion in 2029; the new estimate is 2036 — a reprieve of seven years.

| TABLE 1: Trustees’ Estimates Have Fluctuated But Tell a Consistent Story |

||||||

| Change in actuarial balance since previous report due to— | Actuarial balance | Year of exhaustion | ||||

| Legislation and regulations | Valuation period | All other | Total change | |||

| 1994 | 0.00 | -0.05 | -0.61 | -0.66 | -2.13 | 2029 |

| 1995 | 0.00 | -0.07 | 0.03 | -0.04 | -2.17 | 2030 |

| 1996 | 0.03 | -0.08 | 0.03 | -0.02 | -2.19 | 2029 |

| 1997 | 0.03 | -0.08 | 0.02 | -0.03 | -2.23 | 2029 |

| 1998 | 0.00 | -0.08 | 0.12 | 0.04 | -2.19 | 2032 |

| 1999 | 0.00 | -0.08 | 0.20 | 0.12 | -2.07 | 2034 |

| 2000 | 0.00 | -0.07 | 0.24 | 0.17 | -1.89 | 2037 |

| 2001 | 0.00 | -0.07 | 0.10 | 0.03 | -1.86 | 2038 |

| 2002 | 0.00 | -0.07 | 0.06 | -0.01 | -1.87 | 2041 |

| 2003 | 0.00 | -0.07 | 0.03 | -0.04 | -1.92 | 2042 |

| 2004 | 0.00 | -0.07 | 0.10 | 0.03 | -1.89 | 2042 |

| 2005 | 0.00 | -0.07 | 0.03 | -0.04 | -1.92 | 2041 |

| 2006 | 0.00 | -0.06 | -0.03 | -0.09 | -2.02 | 2040 |

| 2007 | 0.00 | -0.06 | 0.13 | 0.07 | -1.95 | 2041 |

| 2008 | 0.00 | -0.06 | 0.32 | 0.26 | -1.70 | 2041 |

| 2009 | 0.00 | -0.05 | -0.25 | -0.30 | -2.00 | 2037 |

| 2010 | 0.14 | -0.06 | 0.00 | 0.08 | -1.92 | 2037 |

| 2011 | 0.00 | -0.05 | -0.25 | -0.30 | -2.22 | 2036 |

| Source: Annual trustees’ reports. All figures (except year of exhaustion) are expressed as a percentage of taxable payroll. Details may not add to totals due to rounding. a “All other” changes include effects of economic, demographic, and disability assumptions and any changes in the actuaries’ methods and models. |

||||||

Last year’s trustees’ report showed a small but significant improvement in Social Security’s finances due to the new health-care reform law, which the actuaries expect will shift some employee compensation from (nontaxable) fringe benefits to (taxable) wages. That’s no longer new but is worth reiterating. Repealing health-reform would not only leave many millions of people uninsured and abandon various cost-saving measures in Medicare, but would also harm the Social Security outlook.

No significant legislation that altered the Social Security outlook has been enacted since last year’s report. The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 temporarily reduced the payroll-tax rate by 2 percentage points for employees and the self-employed. However, the revenue loss from that payroll-tax holiday — which lasts only through 2011 — is fully offset by a transfer from the Treasury’s general fund to the Social Security trust funds, estimated to total about $112 billion, leaving the trust funds unaffected.

Some commentators may focus on huge dollar figures that appear in the report, such as the estimated $6.5 trillion shortfall through 2085 (or even the $17.9 trillion shortfall through eternity, a figure whose validity many experts disparage[4]). Except over relatively short periods, however, it is not useful to express Social Security’s income, outgo, or funding gap in dollar terms, which conveys no sense of the economy’s ability to support the program. Expressing them in relation to taxable payroll or GDP, in contrast, puts them in proper perspective. Over the next 75 years, for example, taxable payroll — discounted to today’s dollars just as the $6.5 trillion shortfall figure is — will exceed $300 trillion, and GDP will be nearly $900 trillion. Thus, the shortfall over that period equals 2.1 percent of taxable payroll and 0.7 percent of GDP.[5]

Key Dates and What They Mean

2036 is the “headline date” in the new trustees’ report, because that is when the combined trust funds are expected to run out of Treasury bonds to cash in. At that point, if nothing else is done, benefits would have to be cut to match the program’s annual tax income. The program could then pay about 77 percent of scheduled benefits, a figure that would slip to 74 percent by 2085. Contrary to popular misconception, benefits would not stop.

Although the exhaustion date attracts keen attention, the trustees caution that their projections are uncertain. For example, while 2036 is their best estimate of when the trust funds will be depleted, they reckon there is an 80 percent probability that trust fund exhaustion will occur sometime between 2031 and 2042 — and a 95 percent chance that depletion will happen between 2030 and 2049. In short, all reasonable estimates show a long-run problem but not an immediate crisis.

Two other, earlier dates also receive attention but have little significance for Social Security financing:

- 2010 marked the first year since 1983 in which the program’s total expenses (for benefits and administrative costs) exceeded its tax income (from payroll taxes and income taxes that higher-income beneficiaries pay on a portion of their Social Security benefits). That so-called cash-flow imbalance — which equaled $49 billion in 2010 — results from the severe economic downturn and will shrink as the economy recovers, before widening again after 2015 as the retirement of the baby boom accelerates. Throughout that period, however, the trust funds will continue to grow, primarily because of the interest income the funds will receive on the Treasury bonds they hold. Even in 2010, for example, the trustees note that Social Security’s interest income of $118 billion more than offset its cash deficit of $49 billion, leading the trust funds to grow by $69 billion.[6]

- 2023 will be the first year in which the program’s expenses exceed its total income, including its interest income. At that point, the trust funds — after peaking at $3.7 trillion — will start to shrink as Social Security redeems its Treasury bonds to pay benefits.

Neither of these dates affects Social Security beneficiaries. Since the mid-1980s, Social Security has collected more in taxes each year than it pays out in benefits, has lent the excess revenue to the Treasury, and has received Treasury bonds in return. That accounts for the $2.6 trillion in Treasury bonds that the trust funds hold today.

The drafters of the 1983 Social Security legislation purposely designed program financing in this manner to help pre-fund some of the costs of the baby boomers’ retirement. The interest income that the Social Security trust funds earn on their bonds, as well as the proceeds the trust funds will subsequently receive when the bonds are redeemed, will enable Social Security to keep paying full benefits until 2036. Of course, policymakers should restore Social Security’s long-run solvency well before then. But they should not focus much on annual cash flows in a program that is meant to take a multi-decade perspective.

Automatic Adjustments Will Resume

The trustees project that in January 2012, for the first time since 2009, Social Security beneficiaries should expect a cost-of-living adjustment (COLA). The January 2009 COLA of 5.8 percent was based on a record high that the consumer price index for urban wage and clerical workers (CPI-W) set in summer 2008; the overall price level fell thereafter, and not until early 2011 did we pass that previous peak. The actual CPI-W for the July-September 2011 quarter — which will determine the upcoming COLA — will be known in mid-October. The trustees project an across-the-board increase in benefits of 0.7 percent, or about $7 a month for an average beneficiary. For many retirees, however, that increase will be entirely offset by an increase in Medicare premiums, which are deducted from Social Security checks.

An odd consequence of a zero COLA is that the maximum amount of an individual’s earnings that is subject to the Social Security payroll tax — currently $106,800 — stayed unchanged for three years in a row. (The same was true of the so-called retirement test, which reduces benefits for recipients who are under the full retirement age and whose earnings exceed certain dollar thresholds.) In the future, Congress should consider de-linking these measures from the COLA so they can continue rising with average wages as they normally do.[7] Because a COLA is now expected in 2012, wage-indexed features can also rise — from $106,800 to a projected $110,700 in the case of the taxable maximum. [8]

What Congress Should Do Soon

Most analyses of the trustees’ report — including this one — focus on the combined Old-Age and Survivors Insurance (OASI) and Disability Insurance (DI) trust funds, commonly known as the Social Security trust funds. But these two trust funds are in fact separate, and the DI trust fund faces exhaustion in 2018. (The much bigger OASI fund would last until 2038. Combined, the two funds would be depleted in 2036.)

Congress could address that simply by reallocating some payroll tax revenue between the two trust funds — as it has done several times in the past, in either direction — to shore up the DI trust fund. This would enable all parts of the program to pay full benefits until 2036. (For more on the disability program, see the text box below.)

Next year, Congress must decide whether to extend the Bush tax cuts that are scheduled to expire at the end of 2012. Those originally were slated to expire after 2010; in last December’s tax act, President Obama and lawmakers agreed to continue them for two years as part of a package that also aided the unemployed, granted a temporary payroll-tax holiday, and extended certain tax breaks for businesses. [10] The President has proposed to let the tax cuts expire for Americans making over $200,000 (single persons) or $250,000 (married couples) a year. If policymakers went further and let all the tax cuts expire — or paid for the tax-cut provisions they choose to continue — that step, at a single stroke, would nearly stabilize the ratio of federal debt to GDP (a key test of fiscal sustainability) for the next decade.[11]

The revenue loss over the next 75 years from making all of those tax cuts permanent would be two and one-half times the entire Social Security shortfall over that period. Indeed, the revenue loss just from extending the tax cuts for people making over $250,000 — the top 2 percent of Americans — would itself be almost as large as the Social Security shortfall over the 75-year period. (See Figure 1.) Members of Congress cannot simultaneously claim that the tax cuts are affordable while the Social Security shortfall constitutes a dire fiscal threat.

Conclusion

Because Social Security’s finances are fairly predictable, it is not difficult to craft revenue and benefit proposals that would place the program on a sound long-term footing. The best proposals would protect vulnerable workers and beneficiaries and give all participants ample warning of future changes so they can plan their work and savings accordingly.

Although Social Security faces no imminent crisis, policymakers should act sooner rather than later to restore its long-term solvency. As the Center’s President Robert Greenstein explained in a paper that he co-authored last fall with Charles Blahous, one of the two public trustees of Social Security, the sooner policymakers act, the more fairly they can spread out the needed adjustments in revenue and benefit formulas, and the more confidently people can plan their work, savings, and retirement.[12]

Acting sooner also helps the budget as a whole by modestly reducing federal borrowing in coming years. That will contribute to helping stabilize the ratio of debt to GDP and limit the overall interest costs that we must pay.

Nevertheless, policymakers need to get Social Security reform right. Nearly every American participates in Social Security, first as a worker and eventually as a beneficiary. The program’s benefits — though modest both in dollar terms (elderly beneficiaries receive an average benefit of about $14,000 a year) and in comparison with benefits in other countries (Social Security benefits replace a smaller share of pre-retirement earnings than comparable programs in most other western nations) — are the foundation of income security. [13]

Treating Social Security as just one component of a big deficit-reduction package could lead policymakers to reach for “off-the-shelf” options without sufficiently considering the program’s adequacy, equity, and relationship to other programs. Reforms need to be designed carefully so Social Security continues as the most effective and successful income-security program in the nation’s history

Disability Insurance Isn’t in Crisis

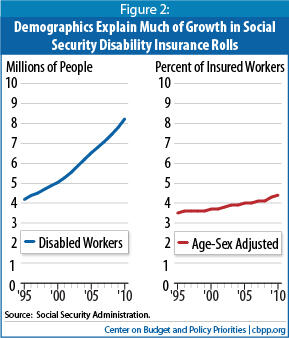

In December 2010, 8.2 million people received disabled-worker benefits from Social Security. (Payments also went to some of their family members: 160,000 spouses and 1.8 million children.) The number of disabled workers has doubled since 1995, while the working-age population — conventionally described as people age 20 through 64 — has increased by only about one-fifth. But that comparison is deceptive. Over that period:

- Baby boomers aged into their high-disability years. People are roughly twice as likely to be disabled at age 50 as at age 40, and twice as likely to be disabled at age 60 as at age 50. As the baby boomers (people born in 1946 through 1964) have grown inexorably older, the number of disability cases has risen.

- More women qualified for disability benefits. In general, workers with severe impairments can get disability benefits only if they’ve worked for at least one-fourth of their adult life and for five of the last ten years. Until the great influx of women into the workforce that occurred in the 1970s and 1980s, relatively few women met those tests; as recently as 1990, male disabled workers outnumbered women by nearly 2 to 1. Now that more women have worked long enough to qualify for disability benefits, the ratio has fallen to 1.1 to 1.

- Social Security’s full retirement age rose from 65 to 66. When disabled workers reach full retirement age, they begin receiving Social Security retirement benefits rather than disability benefits. The increase in the retirement age has delayed that conversion for many workers. In December 2010, nearly 340,000 people between 65 and 66 collected disability benefits; under the rules in place a decade ago, they would be receiving retirement benefits instead.Image

The Social Security actuaries express the number of people receiving disability benefits using an “age- and sex-adjusted disability prevalence rate” that controls for these factors. Over the 1995-2010 period, that rate rose from 3.5 percent of the working-age population to 4.4 percent. That’s certainly an increase, but not nearly as dramatic as some alarmists paint (see graph).

Not surprisingly, the rate crept upward during periods of economic distress. Anecdotally and statistically, we know that many workers with physical or other health conditions who can’t find jobs and who exhaust their unemployment benefits turn to disability insurance.

When lawmakers last redirected more of the 12.4 percent payroll tax from OASI to DI in 1994, they expected that step to keep DI solvent until 2016. Remarkably, despite fluctuations in the meantime, that projection still seems about right; the trustees now project exhaustion of the DI trust fund in 2018. Disability benefits are an integral part of Social Security, closely woven into its package of retirement and survivor protections. Policymakers should act well before 2018 to restore solvency to all of Social Security and make any necessary tax-rate reallocations between the two trust funds at that time.

End Notes

[1] The 2011Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds , May 2011, http://www.ssa.gov/OACT/TR/2011/index.html.

[2] Payroll taxes equal 12.4 percent of taxable payroll, while dedicated income taxes from higher-income beneficiaries contribute another 0.4 percent, which will rise to nearly 1 percent by 2085. See “Components of Income Rates” at http://www.ssa.gov/OACT/TR/2011/lr4b10.html.

[3] The scheduled rise in the full retirement age (FRA) from 66 to 67, to be phased in between 2017 and 2022, will mitigate the program’s cost growth. For an explanation, see Box 1, “Why Does Raising the Retirement Age Reduce Benefits?” in Kathy Ruffing and Paul N. Van de Water, “Bowles-Simpson Social Security Proposal Not a Good Starting Point for Reforms,” Center on Budget and Policy Priorities, February 17, 2011.

[4] See letter from the American Academy of Actuaries to the Trustees of the Social Security System and the Social Security Advisory Board, December 19, 2003, http://www.actuary.org/pdf/socialsecurity/tech_dec03.pdf.

[5] Trustees’ Report, Table IV.B6. As noted earlier, the more prominent figures — 2.22 percent of taxable payroll or 0.8 percent of GDP — include an extra margin for a target trust-fund balance at the end of 2085.

[6] Kathy A. Ruffing, “Social Security Does Not Need a ‘Bailout’: Alarmists’ Claims Are Unjustified, But Action Is Needed to Ensure Long-Term Solvency,” Center on Budget and Policy Priorities, August 24, 2010.

[7] Kathy A. Ruffing, “Case For a Social Security Cost-of-Living Adjustment in 2010 Is Weak: If Policymakers Feel a Need to Act, They Should Consider a One-Time Payment,” Center on Budget and Policy Priorities, October 15, 2009.

[8] Trustees’ Report , Table V.C1.

[9] “Bowles-Simpson Social Security Proposal Not a Good Starting Point,” op. cit.; Kathy Ruffing, “Plans Differ on Social Security Fix,” Center on Budget and Policy Priorities “Off the Charts” blog, November 23, 2010.

[10] Gillian Brunet and Chuck Marr, “Unpacking the Tax Cut-Unemployment Compromise,” Center on Budget and Policy Priorities, December 10, 2010.

[11] Kathy Ruffing and James R. Horney, “Economic Downturn and Bush Policies Continue to Drive Large Projected Deficits,” Center on Budget and Policy Priorities, May 10, 2011.

[12] Charles P. Blahous and Robert Greenstein, “Social Security Shortfall Warrants Action Soon,” Pew Economic Policy Group, November 2010.

[13] Kathy A. Ruffing and Paul N. Van de Water, “Social Security Benefits Are Modest,” Center on Budget and Policy Priorities, January 11, 2011; Kathy A. Ruffing, “We’re Number…30!” Off the Charts blog, May 11, 2011.

More from the Authors