Emergency Unemployment Insurance Benefits Remain Critical for the Economy

Although the unemployment rate is stuck at more than 9½ percent, jobless workers will see unemployment insurance (UI) benefits slashed to pre-recession levels unless Congress acts before the end of this month. That would deliver a harsh blow to most of the 5 million workers now receiving federal emergency UI benefits — which would end prematurely — as well as to the several hundred thousand more unemployed workers each month over the coming year who would get no emergency federal benefits when their basic unemployment benefits run out before they can find a job. It also would deliver a sharp blow to the weak economy. Unemployed workers and their families would have less money to spend and would cut back on their purchases of goods and services; the resulting weaker sales would hurt businesses and cost jobs.

A congressional failure to act under these circumstances would be unprecedented. Congress has enacted a temporary program to provide additional weeks of federally funded UI benefits in every major recession since the 1950s, and has always continued providing those benefits until the economy was back on track and job prospects were improving. Today, the unemployment rate is 9.6 percent, job opportunities are scarce, and forecasters see little improvement over the coming year. In weak economies over the past six decades, the highest unemployment rate at which federal unemployment benefits have been cut off was 7.2 percent — nearly two-and-a-half percentage points lower than it is today.

Policymakers have legitimate concerns about the nation’s unsustainable long-term budget deficit. But continuing federal emergency UI benefits until the job market is stronger will have a negligible impact on the long-term deficit. And allowing them to expire prematurely (or requiring Congress to offset the costs of any extension by cutting other current spending) will endanger a fragile economic recovery while harming millions of unemployed workers, their families, and the businesses where they shop.

Ending these benefits would be counterproductive as a response to the huge jobs deficit that is the legacy of the worst recession since the 1930s and ineffective and largely irrelevant as a way to address the nation’s long-term budget problems. In fact, restoring a healthy economy is a critical first step toward restoring a sound fiscal future, and continuing to provide emergency unemployment insurance benefits through next year is critical to restoring a healthy economy in the period immediately ahead.

What’s at Stake for the Unemployed

Under current law, people who exhaust their 26 weeks of regular state-funded UI benefits are eligible for additional weeks of federally funded benefits under the Emergency Unemployment Compensation (EUC) program enacted in 2008 and expanded in 2009 under the American Recovery and Reinvestment Act (ARRA). In addition, the Recovery Act provided for full federal funding of the permanently authorized Extended Benefits (EB) program that provides additional weeks of UI benefits to exhaustees in high-unemployment states and is normally half federal- and half state-financed. Full federal funding encouraged many states to change their laws so they could provide EB under current economic conditions, as long as those benefits were fully federally funded. [1]

Both the EUC program and full federal funding of EB are scheduled to expire on November 30. After that date, no new exhaustees will be eligible for EUC. Although the number of exhaustees has come down from its peak level, it remains very high; 455,000 unemployed workers exhausted their 26 weeks of regular UI benefits in September without finding a job, and several hundred thousand more unemployed workers will exhaust their regular benefits each month over the coming year. People receiving EUC on November 30 will be able to complete their current “tier” of benefits but will not be allowed to move on to the next tier.[2] In addition, people receiving unemployment benefits under the EB program will have their benefits cut off immediately in many states when those benefits are no longer fully federally funded.

The National Employment Law Project (NELP) estimates that if Congress fails to take action, 2 million workers now receiving unemployment benefits will lose those benefits in December.[3] Large additional numbers of unemployed workers will lose benefits each month in the coming year. (Of the 2 million workers whose benefits will be cut off in December, 800,000 will face a cut-off of their EB benefits, another 800,000 will face a premature cutoff of EUC benefits, and 400,000 will exhaust their regular UI benefits with no access to any benefits after that.) EB benefits will still be available in 10 states. But in all other states unemployed workers who exhaust their 26 weeks of regular benefits without having found a job will receive no further benefits.[4] The appendix at the end of this paper shows how many weeks of benefits would be available in each state if the federal emergency UI benefits expire, as well as NELP’s estimate of the number of unemployed workers in each state who will lose benefits in December.

Basic economics tells us that this is not the time to cut off emergency UI benefits. The economy is still in the early stages of recovery from its worst economic crisis by far since the 1930s. The need for financial assistance among unemployed workers and their families remains substantial, and the importance of UI to the weak economy has not diminished. That said, it is important to stress that this is a temporary program. As the economy improves and the unemployment rate comes down, expenditures for UI diminish automatically as the number of unemployed falls. As job prospects improve and the pace of job creation picks up, many more people will find jobs before exhausting all their available unemployment insurance benefits. As that begins to happen in earnest, the emergency benefits program can and should be phased out, as it has been after every previous economic downturn.

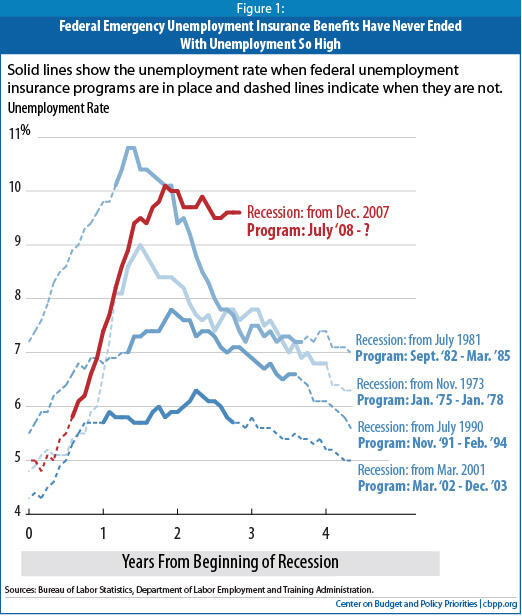

We now are nowhere near the conditions in which federal emergency UI benefits have ended in the past (see Figure 1). The unemployment rate is stuck at 9.6 percent; it is not 6 or 7 percent and falling. The highest unemployment rate at which any previous federal emergency unemployment benefits program ended was 7.2 percent in March 1985.[5]

Opponents of continuing emergency UI benefits often assert that UI discourages people from looking for work and that ending the program would speed the return to full employment. Certainly, U.S. policymakers have decided that 26 weeks of benefits is the right balance between providing temporary assistance to unemployed workers and preserving appropriate incentives to find work when the labor market is functioning properly. But arguments that emergency UI benefits are an important contributor to high unemployment in today’s economy have cause and effect backwards. We have a temporary federal program because unemployment is so high and jobs are so hard to find (see the box below, “Unemployment Remains Stubbornly High”). When there are five times as many unemployed workers as there are job openings, it is hard to see how sharply curtailing the duration of unemployment insurance benefits would increase the pace of job creation.

To be sure, there is research from earlier periods showing that additional weeks of unemployment insurance have an impact in lengthening unemployment spells. One of the most well-known of such studies is by Harvard economist Lawrence Katz. In recent Congressional testimony, however, Katz put that research in perspective and discussed more recent findings. He concluded that “the most compelling evidence” suggests that providing additional weeks of unemployment insurance has “only modest impacts” on how long UI recipients remain unemployed. According to Katz, earlier, somewhat larger estimates of the impact of additional weeks of UI on the duration of unemployment were based on data from the 1970s and early 1980s, when U.S. labor markets were quite different from today. In particular, Katz explained that during that period, firms and industries were prone to tie temporary layoffs and the timing of recalls to the duration of UI benefits, while “this layoff-recall process is much less important today.” Katz also observed that traditional estimates of the relationship between UI and the length of unemployment spells ignore other effects such as “the macroeconomic stimulus impacts of increased consumption expenditures by the unemployed …as well as the gains from keeping more of the long-term unemployed attached to the labor market rather than moving onto disability programs.”[6]

Unemployment Remains Stubbornly High

Figure 1 shows, the recession that began in December 2007 and ended in June 2009 looks a lot like the deep 1973-75 and 1981-82 recessions in terms of the initial sharp increase in unemployment to a high level, but it looks more like the shallower 1990-91 and 2001 recessions in terms of the subsequent “jobless” recoveries when excess unemployment lingered and job creation was sluggish long after the recession was officially over. This time, however, the jobs deficit created by the recession is much larger, and the economy remains mired in a much deeper economic slump, as evidenced by the following:*

Unprecedented post-World War II jobs deficit . Job losses were much larger and have persisted much longer into the recovery than in other post-World War II recessions. With help from the American Reinvestment and Recovery Act (ARRA) of 2009, the massive job losses of late 2008 and early 2009 were staunched, and the private sector has created jobs every month so far in 2010 (1.1 million through October). Unfortunately, the jobs deficit remains massive. There were 7.5 million fewer jobs on nonfarm payrolls in October 2010 than when the recession started; overall job creation has been blunted by losses in government jobs, especially those in state and local governments. Job creation of 100,000 or so per month is not even sufficient to keep up with a growing population, much less to bring down the employment rate.

Severely depressed employment-population ratio. The percentage of the population aged 16 and over with a job, which had topped 64 percent in the 1990s boom, plunged in the 2007-09 recession as the labor force shrank in the face of diminished job prospects and unemployment climbed. At 58.3 percent, the employment-population ratio is back to levels last seen in the mid-1980s.

Historically high long-term unemployment. Emergency UI kicks in after a worker exhausts his or her regular UI benefits — typically after 26 weeks.** During the recession, the share of the labor force unemployed for more than 26 weeks rose to its highest level in the 60 years for which we have data. Long-term unemployment remains a very serious concern: over two-fifths (41.8 percent) of the 14.8 million people who were unemployed in October 2010 had been looking for a job for 27 weeks or longer. The previous post World War II high occurred in June 1983, when 26 percent of the unemployed had been out of work for 27 weeks or longer.

Record-high labor market slack. In October 2009, the Labor Department’s most comprehensive alternative unemployment rate measure — which includes people who want to work but are discouraged from looking and people working part time because they can’t find full-time jobs — was 17.4 percent. That is the highest level ever recorded with data going back to 1994. In October 2010, this rate was almost as high, at 17.0 percent.

Many more job seekers than job openings. At one point at the beginning of the recovery, there were 6 people looking for work for every job opening. The ratio remains very high. In September 2010, almost 15 million workers were unemployed, but there were only 3 million job openings — or five unemployed workers for each available job. In other words, even if every available job were filled by an unemployed individual, 4 out of 5 unemployed workers would still be looking for work.

* See Center on Budget and Policy Priorities, “Chart Book: The Legacy of the Great Recession,” updated regularly, https://www.cbpp.org/cms/index.cfm?fa=view&id=3252.

** While most states provide a maximum of 26 weeks of regular UI, Massachusetts provides 30 weeks and Montana provides 28 weeks. Fewer weeks are available for workers with more limited work experience.

Moreover, important recent research by Harvard economist Raj Chetty finds that in normal times, additional weeks of UI benefits have two distinct effects on the duration of unemployment spells. On the one hand, unemployment insurance has the beneficial effect of allowing an otherwise financially strapped unemployed worker to search more efficiently for an appropriate job (rather than having to accept the first job offered whether or not it is a good match for his or her skills). On the other hand, UI creates minor disincentives to look hard for a job. He found that the former beneficial effect was much more significant than the latter harmful effect in explaining the duration of unemployment spells. [7] Chetty also concludes that the benefits of UI are likely to be even larger in the current deep jobs slump — and the work disincentive effects smaller, due to the lack of job opportunities — so that, “Weighing costs against benefits, extending benefits further in the current economy would significantly increase economic welfare.”[8]

What’s at Stake for the Economy

High rates of unemployment are bad not only for workers but also for the economy. As Federal Reserve Chairman Bernanke said in a recent speech,

That prospect [that the unemployment rate will decline only slowly] is of central concern to economic policymakers, because high rates of unemployment — especially longer-term unemployment — impose a very heavy burden on the unemployed and their families. More broadly, prolonged high unemployment would pose a risk to consumer spending and hence to the sustainability of the recovery.[9]

Fortunately, the policy that helps unemployed workers and their families is also one of the best policies available to reduce the risk to consumer spending and the strength and sustainability of the recovery.

UI Is a Highly Effective Tool for Reviving a Weak Economy

Among 11 measures analyzed by the Congressional Budget Office (CBO) for increasing economic growth and employment in the next year or two, aid to the unemployed stands at the top of the list.[10] According to CBO, “Households receiving unemployment benefits tend to spend the additional benefits quickly, making this option both timely and cost-effective in spurring economic activity and employment.” CBO estimates that providing additional unemployment insurance benefits would boost economic output by as much as $1.90 per dollar of budgetary cost and increase employment by as many as 19,000 jobs per billion dollars of budgetary cost. [11]

CBO’s estimate of the relative importance and bang-for-the-buck of UI is similar to that of most other forecasters. Mark Zandi of Moody’s Economy.com estimates, for example, that UI generates $1.64 of GDP per dollar spent in the first year, a bang-for-the-buck that is exceeded in his calculations only by the $1.73 generated by an increase in food stamp benefits.

Federal emergency UI benefits provide a significant boost to the economy and job creation. To illustrate, in September roughly 5 million people were receiving additional weeks of federally funded emergency UI benefits with an average weekly benefit of roughly $300. That translates into about $6.5 billion a month pumped into the economy, or $75 to $80 billion over the course of a year. That’s likely to mean one million or more additional jobs, based on CBO’s estimates.[12]

Put the other way around, failure to provide federal emergency UI benefits for another year could drain as much as $75 to $80 billion of purchasing power from the economy and hold down job creation over the coming year, costing one million or more jobs. [13] With forecasters becoming more pessimistic about economic growth and job creation over the coming year, that’s a loss we cannot afford. And, as the Federal Reserve concluded this week, the case for further policy to boost the economy is strong.

Economic Forecasters Becoming More Pessimistic

Economic activity as measured by real (inflation-adjusted) gross domestic product (GDP) was contracting sharply when policymakers enacted the financial stabilization bill (TARP) in late 2008 and the Recovery Act in early 2009. According to the Congressional Budget Office and leading private forecasters, these measures played an important role in boosting economic activity and stemming job losses in 2009. [14] As expected, however, the economy-boosting effects of the Recovery Act measures had their peak impact in 2009 and are now waning, while the economic headwinds that blow especially strong in the wake of recessions precipitated by financial crises [15] are severely inhibiting economic growth and job creation.

CBO expects—as do most private forecasters—that the economic recovery will proceed at a modest pace during the next few years. In its projections released in August, CBO forecast that, under current laws governing federal spending and revenues, real (inflation-adjusted) gross domestic product (GDP) would increase by 2.8 percent between the fourth quarter of 2009 and the fourth quarter of 2010 and by 2.0 percent between the fourth quarters of 2010 and 2011. With economic growth so slow, the unemployment rate would remain above 8 percent until 2012 and above 6 percent until 2014. Since CBO completed that forecast, the economic data released have been weaker than the agency had expected, so if CBO was redoing the forecast today, it would project slightly slower growth in the near term.[16]

Indeed, private forecasters are revising down their forecasts. For example, the National Association of Business Economists (NABE) Outlook Panel cut its growth predictions for 2010 and 2011 in its latest report, issued October 11. Summarizing the reasons, NABE President-elect Richard Wobbekind, said, “This summer’s slowdown has exposed the economy’s sensitivity to wealth losses, the unwinding of debt, and the reductions in economic stimulus” (emphasis added).[17]

Goldman-Sachs (GS) raised a red flag in July when it asked whether we had seen “the end of stimulus,” as Congress enacted the extension of UI benefits only through November 30 and failed to renew subsidized COBRA health insurance benefits for unemployed workers, the additional $25 per week of UI benefits enacted in the Recovery Act, or the tax deductibility of UI benefits. Seeing a waning taste for additional stimulus among policymakers, GS said,

We are therefore removing from our estimates an assumption of further fiscal stimulus beyond the policies in law (including this week’s unemployment extension), though we continue to expect extension of most of the expiring 2001/2003 tax cuts.This adds almost a full percentage point to the drag on growth from Q4 2010 to Q4 2011 to what we had already estimated (emphasis added). [18]

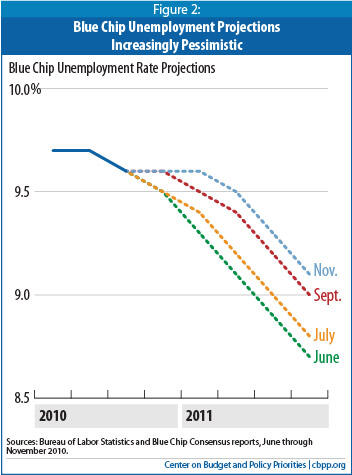

Other forecasters seem to be catching up with GS’s assessment. Growing pessimism over the economic outlook is clearly evident in the evolution of the Blue Chip consensus forecast for the unemployment rate in 2010-2011 (see Figure 2). Whereas in June, the Blue Chip consensus expected the unemployment rate to decline steadily to under 9 percent by the fourth quarter of 2011, by October the consensus forecast envisioned less progress and an unemployment rate that remained above 9 percent through the end of 2011.

The Case for More Stimulus Remains Strong

Forecasters and monetary policymakers recognize that a strong economic recovery remains elusive, that there is still tremendous economic slack (a gap between what the economy would be capable of producing with low unemployment and high industrial capacity utilization and what it is actually producing because demand is so weak), and that further economic stimulus such as that provided by federal emergency UI benefits would increase economic activity and reduce unemployment. As CBO director Elmendorf said in his recent testimony,

The weak demand for goods and services…is the primary constraint on economic recovery…Policymakers cannot reverse all of the effects of the housing and credit boom, the subsequent bust and financial crisis, and the deep recession. However, in CBO’s judgment, there are both monetary and fiscal policy options that, if applied at a sufficient scale, would increase output and employment during the next few years. [19]

Elmendorf acknowledged that the fiscal options would add to the budget deficit and that the long-term budget outlook is grim under current policies, but he then explained:

Despite that grim picture, there is no intrinsic contradiction between providing additional fiscal stimulus today, while the unemployment rate is high and many factories and offices are underused, and imposing fiscal restraint several years from now, when output and employment will probably be close to their potential.[20]

Recent remarks by William C. Dudley, President of the New York Federal Reserve Bank and Vice Chairman of the Federal Reserve’s policy setting Federal Open Market Committee (FOMC), are also of note. Dudley offered the following assessment of the economy and monetary policy:

The deep recession that ended in June 2009 has been followed by a very tepid recovery. Economic activity has grown—but only slowly from levels far below the productive capacity of the economy… Viewed through the lens of the Federal Reserve’s dual mandate—the pursuit of the highest level of employment consistent with price stability, the current situation is wholly unsatisfactory. Given the outlook that the upturn appears likely to strengthen only gradually, it will likely be several years before employment and inflation return to levels consistent with the Federal Reserve’s dual mandate.

…

We [the Federal Reserve] have tools that can provide additional stimulus at costs that do not appear to be prohibitive …..Thus, I conclude that further action is likely to be warranted unless the economic outlook evolves in a way that makes me more confident that we will see better outcomes for both employment and inflation before too long.[21]

In its monetary policy announcement November 3, the Fed announced that it was time to put the tools Dudley was talking about to use. These tools are not the standard ones of monetary policy, which involve reducing the federal funds rate (the short-term interest rate the Fed can control directly) to make money and credit more available and indirectly lower the real (inflation-adjusted) longer-term interest rates that affect business investment, housing, and other interest-sensitive spending. That option is not available now because short-term interest rates are effectively zero and cannot be pushed lower. Meanwhile, declining inflation is pushing real interest rates higher.

Under these circumstances, the Fed has had to resort to nonconventional policies to stimulate economic activity, as Fed Chairman Bernanke has explained in recent speeches.[22] These include clear communication about the Fed’s objective of keeping interest rates low for an extended period and so-called “quantitative easing” (trying to lower long-term rates directly by purchasing long-term securities). To that end, the Fed committed to buying $600 billion of longer-term Treasury securities, thereby hoping to push down long-term interest rates directly.

The Fed is travelling in somewhat uncharted waters in pursuing these policies, and the uncertainties are greater than those associated with conventional monetary policy conducted in normal economic circumstances. There is legitimate debate over how effective the Fed’s new actions will be. One problem is that businesses are already sitting on piles of cash, and it is questionable how much of a deterrent current borrowing costs really represent to new investment. Weak demand seems a more likely suspect. As CBO acknowledges, however, “there seems little reason to doubt that asset purchases in sufficient volume would encourage spending—although that volume might be quite large.”[23]

This brings us back to fiscal policy. In the current environment, Federal Reserve monetary policy is limited in what it can do, which indicates that fiscal policy measures to boost the economy are called for, as well. There currently is a misguided debate over whether such measurers (increases in government spending or tax cuts) can be effective at stimulating economic activity. House Minority Leader John Boehner has contended, for example, that “excessive government spending is crowding out the private economy.”[24]

Such a view defies basic economics: This is not 1999-2000 when the economy was operating at very low levels of unemployment, increases in government spending or tax cuts might — if enacted — contribute to overheating the economy, and the Fed most likely would have responded to deficit-financed spending increases or tax cuts by raising interest rates to maintain a non-inflationary level of economic activity. This is 2010, when there is very high unemployment, significant economic slack, very low inflation, and the Fed wants to see a higher level of economic activity (and is concerned about falling — not rising — inflation). Concern now about government spending causing the economy to overheat seems irrational.

Mr. Boehner’s argument reflects the view of critics of fiscal stimulus who claim that “Congress cannot create new purchasing power out of thin air.”[25] That claim is too simplistic under ordinary circumstances, and it is acutely wrong under current circumstances. When there is substantial economic slack in the economy, inflation is lower than the Fed wants it to be and monetary policy is constrained by the “zero lower bound” on the Fed’s interest rate target (i.e., by the fact that when interest rates hit zero, the Fed cannot lower them further using conventional monetary policy tools in order to boost a weak economy ), then deficit-financed government expenditures — and tax cuts aimed at low- and middle-income taxpayers who are likely to spend rather than save a high proportion of additional disposable income they receive — can be highly effective at stimulating new economic activity and creating jobs.[26] Those are exactly the conditions we face now.

The Fed has already acted to stimulate the economy, and it could definitely use some help on the fiscal side. Chairman Bernanke has been circumspect and not commented directly on fiscal policy.[27] According to former Federal Reserve governor Lawrence H. Meyer, however, “Bernanke has said that fiscal stimulus, accommodated by the Fed, is the single most powerful action the government can take for lowering the unemployment rate, when short-term rates are already at zero.”[28] And as the analyses by both CBO and Moody’s indicate, renewing federal emergency UI benefits is at the top of the list for effective actions to do just that.

What’s at Stake for the Budget

The federal UI program currently costs in the neighborhood of $6 to $7 billion a month, and the cost will come down automatically as the economy improves and the unemployment rate drops. So the cost of extending the program for another year would most likely be less than $80 billion and possibly substantially less.[29] Lawmakers might want to have the number of weeks of emergency benefits available shrink automatically as the economy improves, which would further reduce the program’s cost. But terminating the program now or in the next few months, without regard to economic conditions, would be a serious mistake that would weaken the economic recovery.

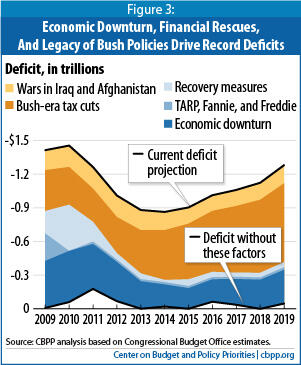

Ending the program also would do almost nothing to improve the long-term budget outlook. As earlier CBPP analyses have shown, the combined cost of the measures the federal government has undertaken to combat the financial meltdown and the recession (including the emergency UI program) will only modestly increase budget deficits over the 2009-2019 period as a whole, with much of the impact occurring in the early years (see Figure 3) [30] — and these measures are only a minimal contributor to our long-term fiscal problems.

Maintaining federal emergency UI benefits for the next 12 months would cost only a small fraction of the cost of these earlier measures and have no noticeable effect on the long-term budget gap, because the program is temporary. Instead, as is well documented, the major driver of the long-term budget gap is the relentless, ongoing rise in health care costs throughout the U.S health care system, which pushes up costs for Medicare and Medicaid.[31]

Emergency UI benefits will affect the long-term budget outlook only to the degree that they increase the national debt and thus the cost of interest payments on the debt. And the interest in future years on the cost of 12 months of federal emergency UI benefits now is tiny; it represents barely a blip on the long-term budget gap.

Some policymakers insist that Congress offset the costs of renewing emergency UI benefits to avoid making the deficit problem worse. From the standpoint of stimulating the economy, however, it would be counterproductive to enact offsets that would take purchasing power out of the economy at the same time that the economy needs the injection of purchasing power that emergency UI benefits provide. Ideally, policymakers would offset the near-term cost of temporary measures like UI benefits with savings that would take effect in years after the economy has recovered so that projected longer-term deficits do not rise by any amount at all. Finding politically feasible “offsets” for the UI legislation that is critically needed now is likely to be difficult and time-consuming, however, and may prove impossible. Should that be the case, it would be better to continue federal emergency UI benefits even without offsets than to let them expire when the economy remains weak, since the immediate damage that would come to the economy would be substantial while long-term fiscal impact of continuing those benefits for a year would be barely noticeable. [32]

Conclusion

It will be unprecedented if Congress allows the federal emergency unemployment insurance benefits program to expire at the end of November or renews the program for just a few months when the unemployment rate remains near 10 percent. That program is providing valuable income support to unemployed workers struggling to find work in a very harsh labor market where job opportunities are scarce. It is also providing valuable support to an economic recovery struggling to gain traction. Without the spending supported by federal unemployment insurance benefits, businesses would experience weaker sales and be less inclined to expand and create jobs.

Congress has provided emergency UI benefits in every major recession since the 1950s and has kept that emergency program in place until the economy was back on track and job prospects were improving. In all previous cases, the unemployment rate was 7.2 percent or lower when the program expired. It is 9.6 percent now and showing no signs of coming down quickly. Continuing the program for another year will provide substantial benefits to both unemployed workers and the economy — and it will do so without endangering efforts to achieve longer-term fiscal balance.

| Appendix Maximum Weeks of Unemployment Insurance and Number of People Affected if Federal Benefits Expire, By State | ||

| State | Weeks of Benefits Available if Federal Benefits Expire | Total Number of Workers Affected in December |

| Alabama | 26 | 26,900 |

| Alaska | 46 | 0 |

| Arizona | 26 | 52,600 |

| Arkansas | 26 | 7,900 |

| California | 26 | 410,700 |

| Colorado | 26 | 41,000 |

| Connecticut | 46 | 0 |

| Delaware | 26 | 6,800 |

| District of Columbia | 26 | 8,000 |

| Florida | 26 | 107,500 |

| Georgia | 26 | 90,000 |

| Hawaii | 26 | 3,400 |

| Idaho | 26 | 15,200 |

| Illinois | 26 | 127,800 |

| Indiana | 26 | 66,800 |

| Iowa | 26 | 8,700 |

| Kansas | 39 | 0 |

| Kentucky | 26 | 33,000 |

| Louisiana | 26 | 10,800 |

| Maine | 26 | 6,800 |

| Maryland | 26 | 13,900 |

| Massachusetts | 30 | 52,500 |

| Michigan* | 26 | 91,700 |

| Minnesota | 39 | 0 |

| Mississippi | 26 | 9,300 |

| Missouri | 26 | 44,900 |

| Montana | 28 | 4,000 |

| Nebraska | 26 | 3,800 |

| Nevada | 26 | 38,000 |

| New Hampshire | 26 | 2,000 |

| New Jersey | 46 | 0 |

| New Mexico | 46 | 2,200 |

| New York | 26 | 160,300 |

| North Carolina | 46 | 0 |

| North Dakota | 26 | 800 |

| Ohio | 26 | 88,500 |

| Oklahoma | 26 | 7,600 |

| Oregon | 46 | 7,400 |

| Pennsylvania | 26 | 133,100 |

| Rhode Island | 46 | 3,000 |

| South Carolina | 26 | 44,200 |

| South Dakota | 26 | 400 |

| Tennessee | 26 | 57,400 |

| Texas | 26 | 127,900 |

| Utah | 26 | 6,500 |

| Vermont | 26 | 1,600 |

| Virginia | 26 | 30,900 |

| Washington | 46 | 0 |

| West Virginia | 26 | 11,000 |

| Wisconsin | 26 | 44,100 |

| Wyoming | 26 | 2,000 |

| UNITED STATES | 2,013,100 | |

| Note: Massachusetts and Montana offer 30 and 28 weeks respectively through their regular state UI programs. Four states that will continue to have Extended Benefits (EB) programs in place will have a small number of exhaustees in December because a number of workers were moved onto EB when the federal program lapsed in June and July and have thus exhausted all benefits available through the program (CT, NM, OR, RI). *Because of an anomaly in Michigan's law, the state will cover workers through January 1st. Sources: CBPP for weeks available, based on information from Department of Labor; National Employment Law Project for number of workers who will lose benefits, published in "Out in the Cold for the Holidays," October 27, 2010: http://www.nelp.org/page/-/UI/2010/november.extension.report.pdf?nocdn=1. | ||

End Notes

[1] All states are required to provide EB when a special measure of unemployment called the insured unemployment rate (IUR) is above a certain threshold, but the IUR threshold in question is typically associated with an extremely high regular unemployment rate that few states reach, even in downturns as severe as the current one. States are allowed, at their discretion, to adopt an optional trigger under which EB benefits are paid to long-term unemployed workers in their state if unemployment hits a level that is high, but not as high as the rate at which a state’s participation in EB becomes mandatory. When full federal funding of EB became available under ARRA, many more states adopted this optional trigger, but those states revert to the higher mandatory threshold when full federal funding ceases to be available.

[2] EUC provides 20 weeks of Tier 1 benefits and 14 weeks of Tier 2 benefits in all states; it provides 13 weeks of Tier 3 benefits in states with unemployment rates of at least 6 percent and 6 weeks of Tier 4 benefits in states with unemployment rates of at least 8.5 percent. See Center on Budget and Policy Priorities, “Policy Basics: How Many Weeks of Unemployment Compensation Are Available?” Updated October 25, 2010.

[3] Christine Riordan, et al., “Out in the Cold for the Holidays: Federal Jobless Benefits Will Be Cut Off for Two Million Workers in December—800,000 Immediately—If Congress Fails to Renew the Emergency Program,” National Employment Law Project Briefing Paper, Revised October 27, 2010. http://nelp.3cdn.net/20ce94b316693432d4_41m6ivi1o.pdf

[4] See Chad Stone, “Cold Turkey — and Cold Holidays — for the Unemployed,” Center on Budget and Policy Priorities, October 25, 2010.

[5] No new recipients were enrolled in the Federal Supplemental Compensation Program after March 1985. The program phased out for existing recipients from April through June of that year.

[6] Lawrence F. Katz, “Long-Term Unemployment in the Great Recession,” testimony before the Joint Economic Committee, U.S. Congress, April 29, 2010, pp. 4-5. http://jec.senate.gov/public/index.cfm?a=Files.Serve&File_id=e1cc2c23-dc6f-4871-a26a-fda9bd32fb7e . For a concise summary of this testimony and other recent research see Joint Economic Committee, “Does Unemployment Insurance Inhibit Job Search?” July 2010. http://jec.senate.gov/public/?a=Files.Serve&File_id=935ec1e7-45a0-461f-a265-bbba6d6d11de

[7] Raj Chetty, “Moral Hazard vs. Liquidity and Optimal Unemployment Insurance,” NBER Working Paper No. 13967, April 2008.

[8] Raj Chetty, “Should Unemployment Benefits Be Extended? An Economic Framework and Empirical Evidence,” presentation before the Economic Policy Institute, May 28, 2010. http://epi.3cdn.net/d5a99f04921083739f_t7m6bxpa7.pdf

[9] Bernanke, “Monetary Policy Objectives and Tools in a Low Inflation Economy,” op. cit.

[10] Congressional Budget Office, “Policies for Increasing Economic Growth and Employment in 2010 and 2011,” January 2010, Table 1, p. 18.

[11] Specifically, CBO estimates that a dollar spent on additional aid to unemployed workers in 2010 would result in an increase in GDP in 2015 of between $0.70 and $1.90; it estimates that a million dollars spent in 2010 would produce between 8 and 19 person-years of full-time-equivalent employment in 2010-2011.

[12] $78 billion would produce between 624,000 and 1.5 million person-years of full-time-equivalent employment, based on CBO’s range of 8 to 19 person years per million dollars of spending. Given the Fed’s intention to keep interest rates as low as possible for a significant period of time, the number of jobs created is likely to be toward the high side of this range.

[13] There is no official cost estimate for a one-year extension of federal emergency UI benefits. Depending on a number of factors, including how much improvements in the economy might reduce the number of recipients, the budgetary cost could be lower than the $75 to $80 billion assumed in the text.

[14] Michael Leachman, “New CBO Report Finds Up to 3.3 Million People Owe Their Jobs to the Recovery Act,” Center on Budget and Policy Priorities, August 24, 2010; Alan S. Blinder and Mark Zandi, “How the Great Recession Was Brought to an End,” July 27, 2010, http://www.dismal.com/mark-zandi/documents/End-of-Great-Recession.pdf .

[15] See Carmen Reinhart and Kenneth Rogoff, “The Aftermath of Financial Crises,” American Economic Review, vol. 99, no. 2 (May 2009), pp. 466–472.

[16] Douglas W. Elmendorf, Director, Congressional Budget Office, “The Economic Outlook and Fiscal Choices,” testimony before the Committee on the Budget, United States Senate, September 28, 2010, http://www.cbo.gov/ftpdocs/118xx/doc11874/09-28-EconomicOutlook_Testimony.pdf .

[17] National Association of Business Economists, “Growth Projections Marked Down – Higher Unemployment and Lower Inflation,” NABE Outlook, October 2010, public summary, http://www.nabe.com/publib/macsum.html.

[18] Goldman Sachs, “U.S. Daily: The End of the Road for Fiscal Stimulus? (Phillips)”Goldman Sachs Global ECS U.S. Research, July 20,2010.

[19] Elmendorf, op. cit.

[20] Ibid .

[21] William C. Dudley, “The Outlook, Policy Choices and Our Mandate,” Remarks at the at the Society of American Business Editors and Writers Fall Conference, City University of New York, Graduate School of Journalism, New York City, October 1, 2010. http://www.newyorkfed.org/newsevents/speeches/2010/dud101001.html .

[22] See Ben Bernanke, " The Economic Outlook and Monetary Policy," speech delivered at "Macroeconomic Challenges: The Decade Ahead," a symposium sponsored by the Federal Reserve Bank of Kansas City, held in Jackson Hole, Wyo., August 26-28, 2010 and more recently Ben Bernanke, “Monetary Policy Objectives and Tools in a Low-Inflation Environment,” speech delivered at the Revisiting Monetary Policy in a Low-Inflation Environment Conference, Federal Reserve Bank of Boston, Boston, Massachusetts, October 15, 2010.

[23] Elmendorf, op. cit.

[24] See, James R. Horney and Robert Greenstein, “Boehner Proposal Would Cut Non-Security Discretionary Programs 21 Percent, The Deepest Such Cut in Recent U.S. History,” Center on Budget and Policy Priorities, revised September 15, 2010, p.3.

[25] For a vigorous statement of the anti-stimulus argument, see Brian Riedl, “Why Government Spending Does Not Stimulate Economic Growth: Answering the Critics,” The Heritage Foundation, January 5, 2010. But as Riedl acknowledges, the Fed can fund new spending by “printing new money” as long as businesses respond to the new demand as being real and not inflationary, which is exactly today’s circumstances.

[26] For a technical discussion, see Michael Woodford, “Simple Analytics of the Government Expenditure Multiplier,” June 13, 2010. http://www.columbia.edu/~mw2230/G_ASSA.pdf.

[27] See Sewell Chan, “Bernanke’s Reluctance to Speak Out Rankles Some,” New York Times, October 28, 2010.

[28] Quoted in David E. Sanger and Sewell Chan, “Fed to Spend $600 billion to Speed Up Recovery,” New York Times, November 3, 2010.

[29] As mentioned in footnote 13, there is no official cost estimate for extending the program.

[30] Kathy Ruffing and James R. Horney, “Critics Still Wrong on What’s Driving Deficits in Coming Years,” Center on Budget and Policy Priorities,” updated June 28, 2010.

[31] See “Testimony of Robert Greenstein, Executive Director and Jim Horney, Director of Federal Fiscal Policy before the Commission on Fiscal Responsibility and Reform,” Center on Budget and Policy Priorities, June 30, 2010, and Paul N. Van de Water, “Federal Spending Target of 21 Percent of GDP Not Appropriate Benchmark for Deficit-Reduction Efforts,” Center on Budget and Policy Priorities, July 28, 2010.

[32] See James R. Horney and Chad Stone, “Don't Let the Ideal Prevent the Necessary: Why Offsets Are Not Needed for Temporary Economic Recovery Legislation,” Center on Budget and Policy Priorities, March 3, 2010.

More from the Authors

Areas of Expertise