A Majority of States Have Now Adopted a Key Corporate Tax Reform — “Combined Reporting”

A growing number of states are adopting a major reform in their corporate income taxes long advocated by state tax experts: “combined reporting.” With the recent enactment of combined reporting legislation in Wisconsin, 23 of the 45 states with corporate income and similar business taxes have implemented this critical policy.

Most large multistate corporations are composed of a “parent” corporation and a number of “subsidiary” corporations owned by the parent. Combined reporting essentially treats the parent and most subsidiaries as one corporation for state income tax purposes. Their nationwide profits are combined — that is, added together — and the state then taxes a share of that combined income. The share is calculated by a formula that takes into account the corporate group’s level of activity in the state as compared to its activity in other states.

By requiring corporate parents and subsidiaries to add their profits together, combined reporting states are able to nullify a variety of tax-avoidance strategies large multistate corporations have devised to artificially move profits out of the states in which they are earned and into states in which they will be taxed at lower rates — or not at all. These strategies cost the non-combined reporting states billions of dollars of lost corporate income tax revenue they need to finance essential public services, like education and health care. Households and small businesses, which do not have the opportunities or resources to engage in interstate income-shifting, end up paying higher taxes than necessary to make up for the taxes that large corporations are able to avoid.

Growing Consideration of Combined Reporting

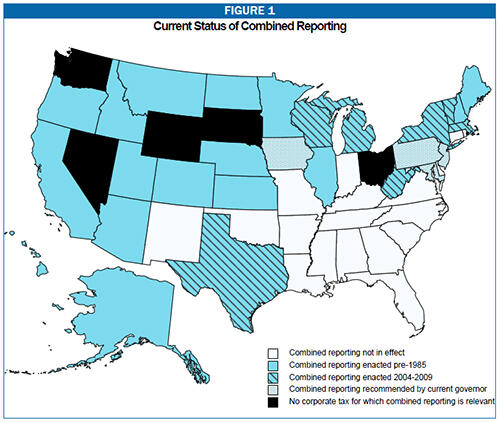

Sixteen states — slightly more than one third of the states with corporate income taxes — have mandated and successfully used combined reporting for decades. (See Figure 1.) Until recently, however, that group had not expanded at all — not even after the U.S. Supreme Court ruled in 1983 that combined reporting was a fair and constitutional method of taxing multinational (and, by extension, multistate) corporations.

That inertia is now being overcome. Seven states have enacted combined reporting legislation since 2004, and serious consideration of combined reporting is occurring in a number of other states:

- In 2004, Vermont became the first state in more than 20 years to adopt combined reporting, effective in 2006.

- In adopting a new general business tax in 2006 to substitute for its corporate income tax, Texas also mandated combined reporting (effective 2008). Although the new tax differs in significant ways from a traditional income tax, the decision to require combined reporting was based on the same basic understanding that underlies the inclusion of combined reporting in state corporate income tax structures — that failure to do so would have given corporations free rein to artificially shift taxable income out of the state.

- In March 2007, West Virginia adopted combined reporting, effective with the 2009 tax year.

- As part of the state budget bill approved in April 2007, New York required combined reporting, retroactive to the beginning of 2007.

- In July 2007, Michigan Governor Jennifer Granholm signed into law a new “Michigan Business Tax” to replace the state’s former “Single Business Tax.” The new tax is a hybrid tax on corporate gross receipts and corporate profits and mandates the use of combined reporting.

- Massachusetts enacted combined reporting in May 2008 at the recommendation of Governor Deval Patrick, retroactive to the beginning of that year.

- Finally, Wisconsin Governor Jim Doyle signed Senate Bill 62 on February 19, 2009, implementing combined reporting retroactively on January 1, 2009.

There has also been serious discussion or consideration of combined reporting in a number of other states in recent years:

- Four current Governors — Jon Corzine of New Jersey, Chet Culver of Iowa, Martin O’Malley of Maryland, and Ed Rendell of Pennsylvania — have sponsored combined reporting legislation or expressed support for it. [1]

- The 2003 Blue Ribbon Tax Reform Commission in New Mexico recommended that the state adopt combined reporting. [2]

- In a November 2003 report, the Florida Senate Committee on Finance and Taxation wrote: “There are several changes in the Florida Income Tax Code that the legislature should consider to prevent further erosion from tax avoidance strategies by corporations that are taxable under current law: 1. Adopt combined reporting to nullify the use of passive investment companies and other corporate tax avoidance strategies. . . .” [3]

- In January 2007, the North Carolina Revenue Laws Committee formally recommended to the incoming legislature that the state adopt combined reporting legislation; the committee recently reaffirmed its support for combined reporting. [4]

- Combined reporting bills have been introduced in numerous states in 2008 and 2009, including Connecticut, Florida, Missouri, New Mexico, North Carolina, Pennsylvania, Rhode Island, and Tennessee.

State Corporate Tax Experts and Newspaper Editorial Boards Support Combined Reporting

In giving serious consideration to combined reporting, states are following advice long offered by state corporate tax policy experts. For example:

- Economist Charles McLure, Deputy Assistant Secretary of the Treasury Department in the Reagan Administration, has written: “Failure to require unitary combination is an open invitation to tax avoidance. (Or — to the extent transfer prices are misstated — is it tax evasion?) The advent of electronic commerce exacerbates the potential problems of economic interdependence and manipulation of transfer prices.” [5]

- In a recent paper, GeorgeWashingtonUniversity professors David Brunori and Joseph J. Cordes wrote: “Our research shows that requiring combined reporting would help the corporate income tax become a more significant source of revenue. . . The combined reporting requirement would severely limit the ability of corporations to use tax planning techniques such as creating nowhere income and establishing passive investment companies to avoid state corporate tax liability. . . .” [6]

- In an article in the prestigious National Tax Journal, Economists William F. Fox, Matthew N. Murray, and LeAnn Luna wrote: “[W]e argue for combined reporting in all states. This conclusion is based in part on economic considerations that are independent of any tax planning opportunities, such as the practical problems associated with measuring economies of scope across related firms. But combined reporting can also lessen tax planning distortions based only on corporate form that waste resources through avoidance and government oversight activities.” [7]

Major newspapers have also editorialized in support of combined reporting. For example:

- The Tampa Tribune wrote: “Florida allows multistate businesses to shelter Florida income in other states. This makes the effective income-tax rate on small Florida businesses higher than the rate paid by corporations sheltering income elsewhere. A company can reduceits tax bill by paying rent to an out-of-state subsidiary. Or it might send profits, on paper, out of state to pay itself for its own patents and trademarks. Rep. Dan Geller, a Miami Beach Democrat, says closing the loophole with a technique called ‘combined reporting’ would raise $365 million a year. Many other states already use the approach, so technical and constitutional issues have been ironed out. . . [I]t is neither good politics nor smart economics to charge Florida businesses more [tax] than is charged the interstate rivals who already enjoy economies of scale.” [8]

- According to the Des Moines Register: “The appropriate tax rate of business certainly is debatable, but everyone should agree those companies should pay the full taxes they owe, and multistate corporations shouldn’t have a tax advantage over wholly local corporations. Last year [former Governor] Vilsack proposed combined reporting to lawmakers, but it didn’t get anywhere. . . . That’s unfortunate. . . . Ensuring taxes are collected by closing a loophole that’s unfair to Iowa-based businesses should be a bipartisan no-brainer.” [9]

Corporate Tax Shelters and the Need for Combined Reporting

Renewed discussion of combined reporting was sparked approximately a decade ago by a rash of court cases in which non-combined reporting states sought to nullify an abusive corporate tax shelter to which they are vulnerable. That tax shelter is frequently referred to as the “Delaware Trademark Holding Company” or “Passive Investment Company” (PIC). It is based on a corporation’s transferring ownership of its trademarks and patents to a subsidiary corporation located in a state that does not tax royalties, interest, or similar types of “intangible income,” such as Delaware and Nevada. Profits of the operational part of a business that otherwise would be taxable by the state(s) in which the company is located are siphoned out of such states by having the tax-haven subsidiary charge a royalty to the rest of the business for the use of the trademark or patent. The royalty is a deductible expense for the corporation paying it, and so reduces the amount of profit such a corporation has in the states in which it does business and is taxable. Moreover, the profits of the Passive Investment Company often are loaned back to the rest of the corporation, and a secondary siphoning of income occurs through the payment of deductible interest on the loan. Of course, the royalties and interest received by the PIC are not taxed; Delaware has a special income tax exemption for corporations whose activities are limited to owning and collecting income from intangible assets, and Nevada does not have a corporate income tax at all.

Combined reporting nullifies the PIC tax shelter because the profits of the subsidiary are added to the profits of the operational part(s) of the corporate group. The PIC remains in existence and the royalty payments continue to be made to the PIC, but the tax benefit of shifting profits to the PIC are eliminated by the combination.

Rather than adopt combined reporting, some states attempted to attack PICs in more limited ways. Some tried to impose their corporate income taxes on the out-of-state PICs directly, and others enacted laws disallowing the deduction of royalty and interest payments to the PICs. A widely-discussed front-page article in the Wall Street Journal in February 2007, however, underscored the need to take a comprehensive rather than piecemeal approach to the corporate tax avoidance strategies to which non-combined reporting states are vulnerable. [10]

The article discussed a tax shelter established by Wal-Mart that is analogous to the PIC but that would not be nullified by the targeted anti-PIC legislation that some states enacted. Indeed, the article revealed that Wal-Mart set up this shelter, known as a “captive Real Estate Investment Trust” (REIT), at approximately the same time it was liquidating its conventional PIC (perhaps because PICs had become a red flag for state auditors). Wal-Mart transferred ownership of all its stores to its REIT subsidiary, and the stores paid tax-deductible rent to the REIT for use of the buildings they occupied. As with royalty payments for the use of trademarks, the rent payments had the effect of reducing taxable profits of the stores and shifting the profits to the REIT. Virtually all states effectively treat the REIT as a tax-exempt entity — just as the federal government does. And the other Wal-Mart subsidiary that owned the REIT was only taxable in the state in which it was based, so the states where Wal-Mart’s stores were located couldn’t reach the REIT’s profits when those were passed on in the form of dividends to the REIT’s owner, either.

The Wal-Mart REIT example suggests that the comprehensive solution of combined reporting is a much better way for states to shore-up their corporate income taxes than narrower, case-by-case attacks on specific tax shelters, for at least four reasons:

- Highly-skilled and highly-compensated tax attorneys and accountants are likely to remain at least one step ahead of under-staffed state revenue departments in devising new mechanisms multistate corporations can use to minimize their state income taxes in non-combined reporting states. For example, a recent newsletter from the BDO Seidman accounting firm that discussed a (rare) New YorkState court victory against a PIC assured its clients that:

“BDO Seidman can facilitate the replacement of your current Delaware Holding Company with state tax reducing strategies to fit naturally around your business operations. Examples of BDO Seidman’s most popular state tax reducing strategies include:

- 197 Strategy,

- Embedded Royalty Company, and

- Effective Use of Transfer Pricing.” [11]

- It is labor-intensive, time-consuming, and costly for states to address these problems on a case-by-case basis. For example, after the Wisconsin legislature rejected the 1999 call by former Governor Tommy Thompson to mandate combined reporting, the state revenue department was compelled to engage in a four-year-long process of auditing and then negotiating individual agreements with 175 banks to stop tax avoidance based on the use of PICs located in Nevada.[12]

- Some of the laws aimed at nullifying specific tax shelters that non-combined reporting states are vulnerable to may be subject to legal challenge. Numerous articles have been written by corporate tax attorneys advising their clients how to attack these laws on the grounds that they discriminate against interstate commerce; a challenge to Alabama’s law is currently on appeal to the U.S. Supreme Court. [13] In contrast, the legality of combined reporting has been upheld twice by the Court.[14]

- Perhaps most importantly, there are several tax-avoidance strategies that have been widely adopted by major multistate corporations that cannot be effectively countered through any policy other than combined reporting. [15]

The corporate income taxes of states that do not mandate combined reporting are fundamentally flawed because they permit intra-corporate transactions to affect how much income tax a corporation owes to a particular state. Attacking specific tax shelters that exploit this flaw is akin to treating the symptoms of a disease rather than the underlying defect that causes it.

Combined Reporting Is Primarily About Fairness, Not Revenue

The primary goal of combined reporting is to create a level playing field for all businesses. It seeks to ensure that large multistate corporations cannot end up paying income tax at a lower effective tax rate than small businesses by subdividing themselves into separate corporations and then manipulating transactions within the overall corporate group.

Because such manipulations appear to be widespread and because combined reporting nullifies their tax effects, most states that have studied the fiscal impact of combined reporting have concluded that its adoption would raise some additional revenue. In states that need new revenue sources, requiring combined reporting could certainly make a modest contribution toward that objective. Most states that have prepared estimates conclude that the adoption of combined reporting would increase corporate income tax receipts on the order of 10 to 25 percent.

If a state is considering combined reporting at a time when it does not need additional revenue, and if it wishes to maintain the current balance of taxes between businesses and households, it can use the revenue gained from combined reporting to make offsetting changes in other business tax provisions to ensure that the overall impact is revenue neutral. Even if other business tax changes are made to keep combined reporting revenue-neutral in the short run, its adoption will help to preserve the long-run revenue-generating capacity of the corporate income tax by nullifying a wide variety of corporate tax-avoidance techniques.

Combined Reporting and State Economic Development

As is often the case when changes in tax policy are proposed that would have the effect of increasing tax payments by some businesses, state consideration of combined reporting has elicited warnings from corporate interests that implementing the policy will harm the economic prospects of any state doing so.

In fact, combined reporting states are well-represented among the most economically-successful states in the country. Between 1990 and 2007 — a period roughly spanning the two business cycles preceding the current recession — only eight states that levy corporate income taxes managed to achieve net positive growth in manufacturing employment. Seven of those eight states — Arizona, Idaho, Kansas, Montana, Nebraska, North Dakota, and Utah — had combined reporting in effect throughout the period. The next two best-performing states, Oregon and Minnesota, each of which had roughly flat manufacturing employment during that period, were also combined-reporting states. All other states lost manufacturing jobs, and a majority of them did not require combined reporting. [16]

Three recent studies examined the location decisions of the largest manufacturing corporations in Iowa, North Carolina, and Wisconsin — each of which was considering the adoption of combined reporting when the studies were conducted. [17] All three studies found that the large majority of these companies maintained facilities in numerous combined reporting states and were therefore unquestionably subject to corporate income taxation in those states. If these businesses did not shun existing combined reporting states as locations for their facilities, there is no reason to think they would shun states implementing combined reporting in the future.

California is the state that has used combined reporting the longest and enforces it most aggressively, but this was not a barrier to the birth of Silicon Valley in the 1990s. The presence of combined reporting has not been a barrier to Intel Corporation’s maintenance of its headquarters in California and its decision to place the bulk of its expensive chip fabrication plants in Oregon, Arizona, and Colorado — all combined reporting states. Such anecdotes and the data on manufacturing employment and facility location decisions cited above suggest that the burden of proof ought to lie with combined reporting opponents to demonstrate that the policy has a negative impact on state economic growth.

Total state and local taxes paid by corporations represent approximately two and one-half percent of their expenses on average, and the state corporate income tax represents on average less than ten percent of that two and one-half percent. [18] A state’s decision to adopt combined reporting increases that small corporate tax load only slightly. The potential influence on corporate location decisions of state corporate tax policies is simply overwhelmed in most cases by interstate differences in labor, energy, and transportation costs, which comprise a much greater share of corporate costs than state corporate income taxes do and often vary more among the states than effective rates of corporate taxation. It comes as no surprise, then, that a recent study by economists Robert Tannenwald and George Plesko, which measured interstate differences in overall state and local tax costs for corporations in a particularly rigorous way, found that there was not a statistically-significant (inverse) correlation between those costs and state success in attracting business investment. [19] In other words, higher state and local business taxes did not impede business investment.

Making the Transition to Combined Reporting

A state’s adoption of combined reporting is a significant change in corporate tax policy, and therefore it necessitates some effort to educate state personnel and taxpayers alike in the ways in which it differs from the “separate entity” approach to corporate taxation that still prevails in slightly less than half the states.[20] Fortunately, assistance is available from the Multistate Tax Commission to states that wish to make the change to combined reporting. The MTC is an organization of state revenue departments whose members include most of the existing combined reporting states. In recent years, the MTC has promulgated a model statute for the implementation of combined reporting and a model regulation spelling out in considerable detail which corporate subsidiaries do and do not constitute parts of a “unitary business” that therefore must be included in a combined report. [21] The MTC also has a staff of corporate income tax auditors who audit large multistate corporations on behalf of numerous states simultaneously. They are quite familiar with auditing under combined reporting regimes. A state new to combined reporting could supplement its auditing efforts with MTC auditors as its audit staff familiarizes itself with the new approach. States do not need to be members of the MTC to participate in its Joint Audit Program.

Conclusion

That the number of combined reporting states has increased almost 50 percent in the last five years is compelling evidence that awareness of the need to reform state corporate tax structures is growing. As policymakers in non-combined reporting states ponder their states’ ongoing vulnerability to a variety of aggressive corporate tax shelters — such as Wal-Mart’s “captive REIT” — and objectively examine the decades-long experience of 16 states with this policy, the movement toward combined reporting seems likely to continue.

End Notes

[1] On October 16, 2008, New Jersey Governor Corzine presented the “New Jersey Economic Assistance and Recovery Plan” to a joint session of the state legislature. Materials released at that time stated: “Governor Corzine is directing the Treasurer to immediately engage with major corporate business taxpayers to develop an appropriate strategy to move towards the so-called “single sales factor” method of tax liability computation and towards adoption of Unitary Combined Reporting.” See: “Long Term Solutions,” available at www.state.nj.us/governor/home/media_long.html.

As did his predecessor, Iowa Governor Chet Culver included recommendations for the adoption of combined reporting in both his FY08 and FY09 budgets. In the face of legislative resistance, however, he did not include the proposal in his FY10 budget package.

Maryland Governor Martin O’Malley proposed the enactment of combined reporting legislation as part of a budget-balancing plan submitted to the legislature during an October 2007 special session. The Maryland House of Delegates approved the proposal but the Senate did not concur. Instead, the legislature enacted legislation mandating that corporations prepare a “pro-forma” corporate tax return calculating their tax liability on the basis of combined reporting and establishing a Business Tax Reform Commission. That commission will get underway in 2009.

In February 2005, Pennsylvania Governor Ed Rendell proposed state adoption of combined reporting as part of his FY06 budget package. He has continued to press for the adoption of combined reporting since that time, although the legislature has not acted. In this year’s budget address he stated: “I welcome any revenue enhancement proposals made by any member of the Legislature. Among some of the ideas that have been shared with me are, for example, amendments that close the enormous tax loopholes that exist for companies located outside the state who do business here. . . . These are good ideas and if the Legislature puts them or others on the table I will consider them.” In a Februry 27, 2009 letter to the editor of the Philadelphia Inquirer, he wrote: “In my budget speech, I said I would be willing to consider other revenue enhancements, such as adopting combined reporting for businesses, if sent to me by legislative leaders.”

[2] New Mexico Blue Ribbon Tax Reform Commission, table of recommendations, available at legis.state.nm.us/LCS/bluetaxdocs/BRTRCTableofRecommendations.pdf.

[3] Florida Senate Committee on Finance and Taxation, Why Did Florida’s Corporate Income Tax Revenue Fall While Corporate Profits Rose? Available at www.flsenate.gov/data/Publications/2004/Senate/reports/interim_reports/pdf/2004-137ft.pdf.

[4] See: North Carolina Revenue Laws Study Committee, “Report to the 2009 General Assembly of North Carolina 2009 Session,” pp. 49-50.

[5] Charles E. McLure, “The Nuttiness of State and Local Taxes and the Nuttiness of Responses Thereto,” State Tax Notes, September 11, 2002, p. 851.

[6] David Brunori and Joseph J. Cordes, “The State Corporate Income Tax: Recent Trends for a Troubled Tax,” unpublished paper submitted to the American Institute of Tax Policy, August 15, 2005.

[7] William F. Fox, Matthew N. Murray, and LeAnn Luna, “How Should a Subnational Corporate Income Tax on Multistate Businesses Be Structured?” National Tax Journal, March 2005.

[8] “Tax Phobia in Tallahassee Protects Huge, Unfair Loopholes,” Tampa Tribune, April 11, 2008.

[9] “First, Close Loopholes,” Des Moines Register, February 20, 2004.

[10] Jesse Drucker, “Wal-mart Cuts Taxes by Paying Rent to Itself,” Wall Street Journal, February 1, 2007.

[11] BDO Seidman, LLP, State Tax Alert, May 2005.

[12] Paul Gores, “Bankers Fear Doyle Cold Shoulder, Some Still Smarting Over Tax Shelter Issue,” Milwaukee Journal Sentinel, November 15, 2006.

[13] See, for example: Thomas H. Steele and Pilar M. Sansone, “Surveying Constitutional Theories for Challenges to Add Back Statutes,” web site of the Morrison and Foerster law firm, February 23, 2005. A friend-of-the-court brief filed by the Council on State Taxation (an organization representing large multistate corporations on state tax matters) arguing that the Alabama statute disallowing deductions for royalties paid to PICs is unconstitutional is available at www.cost.org/WorkArea/DownloadAsset.aspx?id=72430.

[14] The cases were Container Corporation of America v.California Franchise Tax Board (1983) andBarclays Bank v. California Franchise Tax Board (1994).

[15] See: Michael Mazerov, “State Corporate Tax Shelters and the Need for ‘Combined Reporting’,” Center on Budget and Policy Priorities, October 2007, available at https://www.cbpp.org/10-26-07sfp.pdf.

[16] See: Michael Mazerov, “Most Large North Carolina Manufacturers Are Already Subject to ‘Combined Reporting’ in Other States,” Center on Budget and Policy Priorities, January 2008, Table 1, p. 6. Available at https://www.cbpp.org/sites/default/files/atoms/files/1-15-09sfp.pdf.

[17] See the study cited in Note 16. See also: Michael Mazerov, “Almost All Large Iowa Manufacturers Are Already Subject to ‘Combined Reporting’ in Other States; Fears of Job Flight from Reducing Corporate Tax Avoidance Are Unwarranted,” Center on Budget and Policy Priorities, April 2008, available at www.cbpp.org/4-3-08sfp.pdf. See also: Jack Norman, “Combined Reporting: How Closing Corporate Loopholes Benefits Wisconsin,” Institute for Wisconsin’s Future, February 2009, available at www.wisconsinsfuture.org/publications/taxes/ IWF_combined%20reporting_Feb09.pdf.

[18] See the source cited in Note 16, Endnote 9.

[19] George A. Plesko and Robert Tannenwald, Measuring the Incentive Effects of State Tax Policies Toward Capital Investment , Federal Reserve Bank of Boston Working Paper 01-4, December 3, 2001.

[20] The key differences between combined reporting and the “separate entity” approach to state corporate income taxation are discussed in Appendix B of Michael Mazerov, State Corporate Tax Disclosure: The Next Step in Corporate Income Tax Reform , February 2007. Available at https://www.cbpp.org/sites/default/files/atoms/files/2-13-07sfp.pdf .

[21] The MTC’s model combined reporting statute is available at www.mtc.gov/uploadedFiles/ Multistate_Tax_Commission/Uniformity/Uniformity_Projects/A_-_Z/Combined%20Reporting%20-%20FINAL%20version.pdf. The MTC’s model definition of a “unitary business” for combined reporting purposes is available on pp. 5-14 of the following document www.mtc.gov/uploadedFiles/ Multistate_Tax_Commission/Uniformity/Uniformity_Projects/A_-_Z/AllocationandApportionmentReg.pdf.

More from the Authors