What the President’s Budget Shows about the Administration’s Priorities

The Administration’s new budget is, at bottom, a statement about national priorities. This budget’s priorities are clear: the budget features cuts in scores of programs that middle- and low-income families rely on, alongside large additional tax cuts for those at the top of the income spectrum who have benefited the most from the tax cuts already enacted.

The consequences of the tax cuts enacted in 2001 and 2003 are becoming more apparent, as the Administration responds to continuing high deficits not by reassessing any of the tax cuts that have contributed substantially to the deficits, but by proposing new tax cuts, along with substantial cuts in many domestic programs that have contributed little or nothing to the return of deficits.

- The budget includes $214 billion in cuts in domestic discretionary programs (non-entitlement programs other than those related to the Department of Defense, international affairs, or homeland security) over the next five years, with the cuts reaching $66 billion — or 16 percent — by 2010. [1]

- The budget includes $138 billion in reductions in mandatory programs (excluding the effects on outlays of the tax legislation proposed in the budget) over 10 years, including cuts in Medicaid, the food stamp program, and child care assistance for low-income working families. Figures in the budget show that child care assistance would be ended for 300,000 low-income children by 2009. The food stamp cut would terminate food stamp aid for approximately 300,000 low income people, most of whom are members of low-income working families with children. The $45 billion in reduced Medicaid funding for states over ten years almost certainly would cause many states to cut their Medicaid programs, increasing the ranks of the uninsured.

- The budget proposes new tax cuts (including extending expiring tax cuts) that will reduce revenues by almost $130 billion over five years and $1.4 trillion over ten years, a figure that rises to $1.6 trillion when the added interest payments on the debt are taken into account. (All estimates of tax cuts in this paper include the effects on outlays of changes in tax law.

- Despite cuts to scores of domestic programs, the Administration’s budget increases rather than decreases the deficit over the next five years. As shown by its own figures, the effect of the Administration’s budget is to increase total deficits over the next five years from $1.364 trillion to $1.393 trillion. (This is so even though the budget fails to include the funding that will be required beyond the upcoming supplemental to fund the war in Iraq and Afghanistan or the cost of extending relief from the Alternative Minimum Tax beyond 2005.) The major reason that the President’s budget increases deficits over the next five years is that tax cuts and increases in defense and homeland security spending increase cost more than the proposed cuts in domestic programs save.

The most appropriate way to view the proposed budget cuts is not as a means of reducing the deficit, but as a way to offset a modest part of the increase in the deficit that has resulted from the tax cuts already enacted since 2001 and proposed in this budget.

- In 2006, the cost of the tax cuts already enacted since 2001, plus those proposed in this budget, would be $193 billion (without interest payments).

- The $18 billion in domestic program reductions proposed for 2006 in the budget would simply keep the tax cuts from increasing the deficit to a greater degree.

The budget also is misleading in some key respects. It omits such things as the cost of future funding for the war in Iraq and the cost of the President’s Social Security proposal. The budget also includes a major new tax cut that the Congressional Research Service has said eventually would cost $300 billion to $500 billion over ten years, but the budget uses a timing gimmick so that this tax cut would save money in the first five years and the large long-term costs of the tax cut are thereby hidden from view. The years in which the tax cut would swell the deficit would be outside the Administration’s “budget window.”

The budget also fails to show how much the Administration proposes to provide for individual discretionary programs — such as education programs, veterans’ health care, environmental protection, and many programs that serve the needs of low-income Americans — in years after 2006. No President’s budget has failed to provide detailed information about proposed discretionary funding beyond the coming year since at least 1989 (and backup materials from whatever Administration was then in office provided that information for a number of years before that).

The omission of this information is serious, because the budget proposes to set caps on discretionary spending for each year through 2010. The Administration is proposing caps that would require large cuts in discretionary programs, while withholding information on the cuts that it envisions proposing in particular programs to comply with these austere caps.

The Administration also proposes a new budget rule apparently intended to make it appear that there is no cost to extending the tax cuts. Under this rule, legislation to extend tax cuts would be treated as if such an extension had already been enacted. When the Office of Management and Budget and the Congressional Budget Office are asked to provide estimates of legislation to extend tax cuts or make them permanent, they would be required to produce estimates showing the costs to be “zero.” This proposal is highly significant, as it would exempt legislation to extend tax cuts from any sort of Congressional budget enforcement.

Budget Shows Unbalanced Priorities

The President’s budget calls for significant cuts in a number of programs that provide key supports and services to low- and middle-income Americans at the same time that it proposes more tax cuts that would go overwhelmingly to the most well-off Americans. The budget also proposes cuts in funding for many other important activities of the federal government.

The budget proposes the cuts in programs for low-income Americans despite the fact that the number of Americans living in poverty went up for the third straight year in 2003, the share of total income that goes to the bottom two-fifths of households has fallen to one of its lowest levels since the end of World War II, and the number of people lacking health insurance rose in 2003 to the highest level on record. Sizeable reductions in programs for low-income families would exacerbate these trends.

Medicaid Proposals

For instance, the budget proposes to cut Medicaid by $45 billion over the next 10 years. (The budget shows proposed cuts in mandatory programs for 10 years although it only gives budget discretionary spending and budget totals for five years.) To evaluate some of the specific Medicaid cut proposals, more detail from the Administration is needed. While various of the Medicaid proposals appear to warrant consideration, reducing the federal funding provided to states for Medicaid when the number of the uninsured is rising and states are encountering increasing difficulty paying their share of Medicaid costs would almost certainly push states to squeeze Medicaid programs in ways that would further increase the numbers of uninsured children, parents, elderly, and people with disabilities. It would make more sense to retain and use any savings from reasonable reform proposals within Medicaid to help states meet the challenges of rising health care costs and increases in Medicaid enrollment that are stemming from the erosion of employer-based coverage. That would help states minimize increases in the number of people without access to health care.

In short, the approach to Medicaid that the budget takes — siphoning badly needed federal funding from hard-pressed state Medicaid programs — would weaken the health care safety net for some of the nation’s most needy and vulnerable people. It may be noted that when it comes to taxes, the Administration takes a decidedly different approach — savings from the small number of revenue-raising proposals included in the budget are not used to reduce the deficit, but instead effectively pay for a very small share of the large cost of the Administration’s tax-cuts proposals.

Other Domestic Program Reductions

The budget also proposes cuts in mandatory spending for programs such as food stamps. Food stamp benefits would be cut by $1.1 billion over 10 years by terminating approximately 300,000 people from the program. The budget freezes child care funding for five years; the budget acknowledges this will cause the termination of assistance for 300,000 low-income children by 2009.

The budget also calls for substantial cuts in domestic programs funded through annual appropriations (so-called discretionary programs). Overall, the budget proposes a 4.9 percent, or $18 billion, real (after inflation) cut in funding in 2006 for domestic discretionary programs — that is, programs not related to the Department of Defense, international affairs, or homeland security. [2] (The budget proposes to increase real funding for the Department of Defense — excluding funds for the war in Iraq and Afghanistan — by 2 percent, or $8 billion, and for homeland security by 1.1 percent, or less than $1 billion.) By 2010, the last year for which the budget provides any information on proposed discretionary spending, domestic discretionary spending security would be cut by $66 billion, or 16 percent, after taking inflation into account.

Costs of the Tax-Cut Proposals

In contrast to these cuts in domestic programs, the budget proposes new tax cuts (including making expiring tax cuts permanent) that will cost $129 billion over the next five years (2006-2010) and $1.4 trillion over 10 years (2006-2015), excluding interest costs. [3] When the tax cuts already enacted since 2001 also are taken into account, the cost of President Bush’s tax cuts totals $1.06 trillion in 2006 through 2010 and $2.45 trillion in 2006 through 2015. (This does not include any cost for alternative minimum tax relief. The budget does not propose to extend temporarily the AMT relief that expires at the end of 2005. According to the Congressional Budget Office, providing AMT relief could cost close to $700 billion over 10 years.)

| Cost of Tax Cuts | ||

| 2006-2010 | 2006-2015 | |

| Tax-cut proposals:b | ||

| Extend 2001 and 2003 tax cuts | 53 | 1,134 |

| New tax cuts proposed in budget (net) | 50 | 198 |

| Extend expiring provisions | 26 | 73 |

| Subtotal, proposed tax cuts | 129 | 1,405 |

| Tax cuts enacted since 2001c | 928 | 1,048 |

| Total, proposed and enacted tax cuts | 1,058 | 2,453 |

| Note: | ||

| AMT relief left out of the budgetd | 202 | 692 |

| Total, tax cuts with AMT relief | 1,259 | 3,145 |

| a Includes the effects on outlays of changes in tax law. | ||

The real impact of the President’s tax cuts is much larger than these numbers indicate, both because the tax cuts will not be fully in effect until 2010 when the estate tax is repealed and because two new tax cut proposals related to savings accounts are built around a timing gimmick — they increase revenues in the first five years but lose very large amounts in subsequent decades. In the first 10 years when all the tax cuts proposed in the budget are fully effective — 2010 through 2019 — they would cost $2.6 trillion. In 2018 alone — the year that the Administration implies Social Security will be in crisis because it will pay out $23 billion more in benefits than it will receive in revenues — the tax cuts would cost $323 billion.

The benefits of these very expensive tax cuts would go overwhelmingly to the most well-off Americans. According to the highly-regarded Tax Policy Center of the Urban Institute and the Brookings Institution, more than 70 percent of the benefits of the President’s tax cuts enacted in 2001 and 2003 (and proposed in last year’s budget) would go to the 20 percent of taxpayers with the highest incomes, and more than 25 percent of the tax-cut benefits would go to the top one percent.

Despite the Administration’s argument that cuts in a very wide swath of domestic programs are necessary to reduce the deficit, the Administration is unwilling to consider scaling back any tax cuts for the most well-off Americans. It is unwilling even to forgo two tax cuts for the highest-income households that were enacted in 2001 but have not yet gone into effect. Those cuts involve the repeal of two provisions enacted in 1990 as part of the deficit reduction package negotiated by then-President George H.W. Bush and Congressional leaders. The provisions in question phase out the benefits of personal exemptions and some itemized deductions for taxpayers at high income levels. The tax bill enacted in 2001 repealed these two provisions, with repeal being phased in starting in 2006 and repeal fully in effect in 2010.

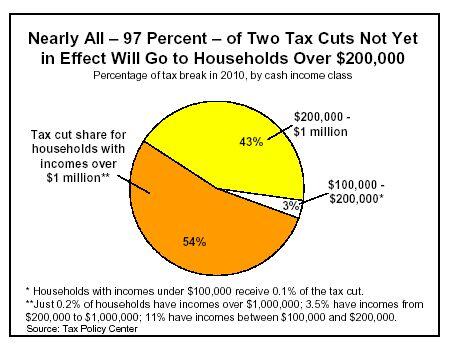

According to the TaxPolicyCenter, 54 percent of the tax-cut benefits from repeal of these provisions would go to households with incomes ofmore than $1 million a year — the top 0.2 percent of households. [4] In 2010, repeal of these provisions would reduce the taxes of households in this income bracket by more than $19,000, on average. This will be in addition to the average tax cut of $133,000 that households with incomes over $1 million will get from the other provisions of the 2001 and 2003 tax cuts.

Another 43 percent of the tax-cut benefits from repeal of these two provisions would go to the 3.5 percent of households with incomes between $200,000 and $1 million. Thus, 97 percent of the benefit of repealing these two tax provisions will go to the 3.7 percent of households with incomes exceeding $200,000. Virtually none of the tax-cut benefits will flow to families with incomes under $100,000.

According to the Joint Committee on Taxation, these two provisions will reduce revenues by $9 billion in 2010, rising to $16 billion in 2015. The ten-year cost of these provisions when they are fully in effect (2010 through 2019) would be $146 billion, not counting the added interest payments on the debt, and about $200 billion including the interest payments. The Administration’s priorities thus are shown by a budget that proposes to cut $214 billion from domestic discretionary programs over 5 years in the name of deficit reduction, but is unwilling to forgo tax cuts that have not yet taken effect and that will bring the benefits of the President’s tax cuts to $152,000, on average, by 2010 for taxpayers with incomes of more than $1 million.

Costly New Tax Cut for High-income Households

Indeed the budget not only retains these tax cuts but adds a costly new upper-income tax cut on top. The budget proposes, as it did last year, to allow households to place $5,000 per family member each year in tax-sheltered “Lifetime Savings Accounts;” earnings on the accounts would be tax free and withdrawals from the accounts also would be tax free. In addition, households could place another $5,000 each for a taxpayer and her or her spouse into a tax-sheltered “Retirement Savings Account” each year. These RSAs would replace IRAs, but the income limits on who can use IRAs would be eliminated. A very wealthy couple with two children would be able to shift $30,000 every year from taxable investment accounts to tax sheltered LSAs and RSAs.

Analysis by the UrbanInstitute-BrookingsTaxPolicyCenter has shown that virtually none of the new tax benefits from these new savings accounts would go to families with incomes under $100,000, as the new accounts would not meaningfully expand tax incentives they already have. The TaxPolicyCenter found that virtually all of the new tax-cut benefits would go to high-income households, which would generally shift assets to the new tax-sheltered accounts (rather than increase their savings) to take advantage of the new tax break.

The proposal also would be extremely expensive. It is designed with the use of timing gimmicks so it saves money over the first five years. But it loses massive amounts of revenue after that. The TaxPolicyCenter has estimated that the proposal ultimately would cost the equivalent of more than $35 billion a year and warned: “The revenue losses explode just as the baby boomers start to retire and the budget situation turns really bleak.”[5] The TaxPolicyCenter found that over the next 75 years, the impact of this proposal on the budget would be equivalent to increasing the long-term Social Security deficit by more than one-third.

What Caused Deficits to Return?

Despite claims that the main culprit in this fiscal deterioration is “runaway domestic spending” or growth in entitlement spending, the primary reason for the change from surplus in 2000 to the deficit in 2005 is lagging revenues. In 2000, the surplus equaled 2.4 percent of GDP. For 2005, CBO projects the deficit will equal 3.3 percent of GDP (including CBO’s estimate of new funding for the Iraq war). This is a negative swing in the nation’s fiscal position of 5.7 percent of GDP. During this period, revenues declined from 20.9 percent of GDP in 2000 to a projected 16.8 percent of GDP in 2005, a drop of 4.0 percent of GDP. Thus, 71 percent of the downturn in the fiscal situation since 2000 (some 4.0 percent of GDP of the total deterioration of 5.7 percent of GDP) is attributable to the drop in revenues.

Moreover, revenues in 2005 will be lower as a share of GDP than in any year in the 1960s, the 1970s, the 1980s, or the 1990s. By contrast, total spending is projected to be 20.1 percent of GDP in 2005 (including CBO’s estimate of new funding for the Iraq war), up 1.6 percent of GDP from 2000 but lower than in any year from 1975 to 1996.

Similarly, data CBO released last month show that increases in domestic discretionary and entitlement spending account for only about one-seventh — 15 percent — of the cost of legislation enacted since January 2001. Tax cuts account for 48 percent of the cost of that legislation — more than three times as much — with the remaining 37 percent attributable to increased funding for defense, homeland security, and international affairs. These data also make clear that the cost of the legislation enacted since January 2001, which totals $539 billion in fiscal year 2005 including interest, far exceeds the projected deficit for this year.

Despite the fact that increased spending for domestic programs has played only a small role in the return to deficits since President Bush took office, the President’s budget puts virtually the entire burden for deficit reduction on these programs.

An analysis of the proposal that the Congressional Research Service conducted last year reached similar conclusions. CRS estimated that the costs of the proposal ultimately would reach the equivalent today of $300 billion to $500 billion over ten years. [6]

Lack of Attention to Tax Compliance

The Administration also seems unwilling to consider, as a way to reduce the deficit, tax compliance and reform measures that could raise a significant amount of revenues. The staff of the Joint Committee on Taxation (JCT) issued a report in January detailing more than 70 steps that could be taken to improve tax compliance, make the tax code more consistent, and close loopholes. The Joint Committee estimated these steps could save about $400 billion over the next 10 years. In contrast, the budget offers only modest tax compliance measures, which would save only a few billion dollars over 10 years.

The Administration’s priorities thus seem clear. The Administration seeks deficit reduction through cuts in large numbers of domestic programs — including cuts in programs that millions of working-poor families with children, low-income elderly and disabled people, and other less fortunate Americans rely on — rather than pursuing an approach that puts all parts of the budget on the table, including highly regressive tax cuts that have not yet been implemented, and that includes efforts to shrink the deficit by attacking tax avoidance and wasteful tax loopholes.

The Budget is Not Open and Honest About the Full Consequences of Its Fiscal Policies

The budget appears to be designed to obscure some of the effects of the policies the Administration is proposing. It is constructed in a way that conceals the fiscal effects of various Administration proposals that would increase the deficit, as well as the consequences of various cuts in domestic programs proposed as a means to deal with the deficit.

- The budget only covers five years, not the ten years that had become customary before President Bush took office. (Ten-year numbers are provided for the cost of proposed tax and entitlement changes, but no information is provided about discretionary spending, total spending, total revenues, or deficits or debt for years beyond 2010.)

- This allows the budget to show the deficit being cut in half from its 2004 level by 2009 without showing the increase in deficits that would occur under the President’s policies in the years after 2010. In particular, covering only the next five years hides the effects on the deficit of the President’s proposed tax cuts, which will mushroom in cost from $39 billion in 2010 to $159 billion in 2011 and $287 in 2015, if the tax cuts are extended.

- The budget also leaves out all of the costs of funding military operations in Iraq and Afghanistan and the global war on terrorism that will be incurred after the $80 billion the Administration has requested for 2005 is exhausted. CBO estimates these additional costs could total around $350 billion over the next 10 years (excluding interest payments on the debt), assuming an eventual phasedown of U.S. activities in Iraq and Afghanistan.

- The budget also leaves out the cost over the next 10 years of reforming the alternative minimum tax (AMT) so it will not increasingly affect middle-income taxpayers. The President’s budget does not propose to extend the current temporary AMT fix, which expires in 2005. According to CBO, extending AMT relief through 2015 could cost nearly $700 billion over 10 years (excluding interest).

Finally, the cost of the President’s proposal to divert Social Security payroll taxes to establish private accounts is not included in the budget. That proposal would add more than $750 billion in deficits and debt in 2006 through 2015, according to the White House, although that number is misleadingly low. It is misleading because the President’s plan would not begin to take effect until 2009 and eligibility for the accounts would be phased in over three years. Over the first ten years that the plan actually would be in effect (2009-18), it would add about $1.4 trillion to the debt. Over the next ten years (2019- 28), it would add about $3.5 trillion more to the debt. All told, the plan would add $4.9 trillion (14 percent of GDP in 2028) to the debt over its first 20 years.

It also may be noted that a principal reason the Administration cites for providing only a five-year budget is that estimates of the budget beyond the fifth year are too uncertain. Yet the Administration contends that the traditional 75-year test of solvency used by the Social Security actuaries and most social insurance experts is not long enough and that Social Security solvency must be measured into eternity. The Administration believes that estimates of the effects of Social Security reform proposals should be made not just for the next five years, not just for the next 10 years, and not just for the next 75 years, but into the “infinite horizon.” The Administration also proposes that 75-year cost estimates be required for major entitlement legislation — and that such legislation be deficit-neutral over 75 years — but tax bills would only have to be scored for five years and would not have to be paid for. The Administration does not explain how those infinite or 75-year estimates will provide a sounder and more reliable basis for decision-making than estimates for 2011 of federal revenues, federal spending, the deficit, and the cost of extending the tax cuts — estimates that the Administration declines to provide on the grounds that they are too uncertain.

End Notes

[1] Unless otherwise noted, all estimates in this analysis are based on Administration estimates or data.

[2] It also should be noted that for purposes of this analysis, this part of the budget includes programs outside of the Defense Department that are considered part of the defense budget function, such as atomic energy programs of the Energy Department. The OMB documents provide budget details in a way that necessitates such an approach.

[3] The Administration estimates that making the tax cuts enacted in 2001 and 2003 permanent will cost $1.1 trillion in 2006 through 2015. CBO estimates that extending those tax cuts will cost $1.3 trillion. Under CBO’s estimates, when interest costs and the cost of the portion of AMT reform attributable to the President’s tax cuts are added in, the total cost of extending the tax cuts reaches $2.1 trillion. See Joel Friedman, Ruth Carlitz, and David Kamin, “Extending the Tax Cuts Would Cost $2.1 Trillion Through 2015,” Center on Budget and Policy Priorities, Revised February 9, 2005.

[4] In its analyses, the TaxPolicyCenter examines the effects of the tax cuts on different “tax units.” These “tax units” include individuals and married couples who file income tax returns, as well as those who do not file (primarily because their incomes are below the minimum threshold for filing). As shorthand, this report uses the term “households” instead of “tax units.”

These TPC distribution estimates reflect the assumption that provisions expiring before 2010, such as the capital gains and dividend tax cuts and relief from the Alternative Minimum Tax, will be extended through 2010. Without this assumption, the degree to which these tax cuts are concentrated on those with the highest incomes would be even greater.

[5] Leonard Burman, William G. Gale, and Peter R. Orszag, “Key Thoughts on RSAs and LSAs,” Urban Institute-BrookingsInstitutionTaxPolicyCenter, February 4, 2004. The analysis finds that the cost of the proposal after 25 years would be 0.3 percent of GDP.

[6] Jane Gravelle and Maxim Shevedov, Congressional Research Service, “Proposed Savings Accounts: Economic and Budgetary Effect,” February 13, 2004.

More from the Authors

Areas of Expertise