BEYOND THE NUMBERS

Marketplace Premiums Are In Line With Employer Premiums — and Would Be on Track to Stay That Way Absent Sabotage

Far from reaching “levels that nobody thought even possible,” as President Trump claimed recently , premiums in the Affordable Care Act (ACA) marketplaces are roughly in line with those for employer coverage, an Urban Institute study finds. And they’d be on track to stay that way, according to a new analysis by actuaries at Oliver Wyman — if the Trump Administration weren’t sabotaging the marketplaces. In fact, Oliver Wyman attributes two-thirds of projected 2018 marketplace rate increases to sabotage.

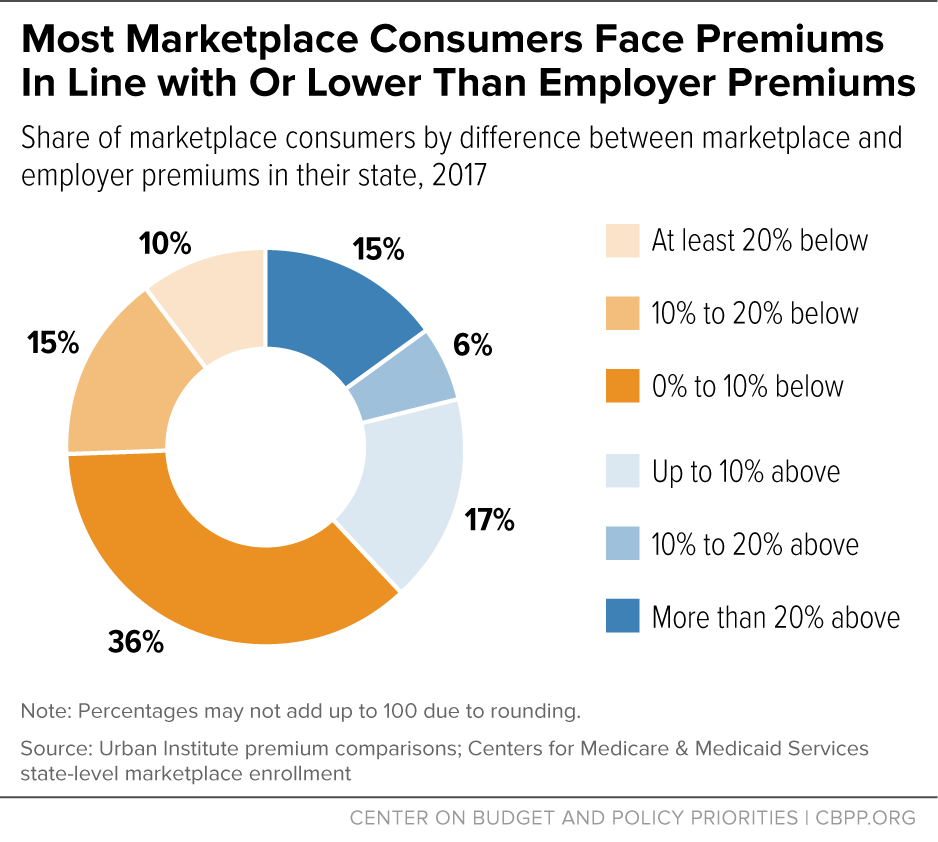

The Urban Institute study compares 2017 benchmark marketplace premiums with average premiums for people with employer-sponsored coverage, taking into account the differences in enrollee age mix and plan generosity. (As the study explains, benchmark premiums, which are used as the basis for the ACA’s premium tax credits, are likely a good proxy for average marketplace premiums.) As the first chart below shows, 61 percent of marketplace consumers live in states where marketplace premiums are equal to or lower than average employer premiums, and another 17 percent live in states where marketplace premiums are no more than 10 percent higher than employer premiums. Not surprisingly, some states whose marketplaces have experienced particular challenges — such as Alaska and Tennessee — have marketplace premiums well above employer premiums. But conversely, marketplace rates in 12 states (Indiana, Kentucky, Massachusetts, Michigan, New Hampshire, New Jersey, New Mexico, Ohio, Rhode Island, Texas, Washington, and the District of Columbia) are at least 15 percent below employer rates.

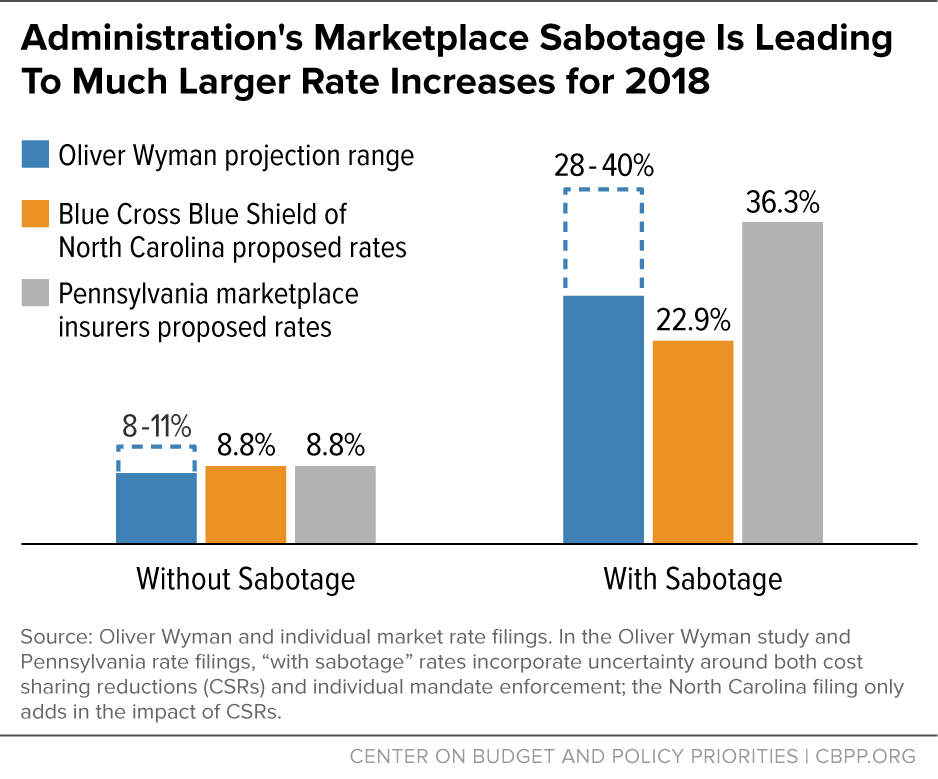

The Oliver Wyman analysis estimates 2018 marketplace rate increases, with and without uncertainty about policy changes. It concludes that, absent policy changes and uncertainty, marketplace premiums would grow roughly with “medical trend,” which Oliver Wyman estimates at 5 to 8 percent. Medical trend refers to the system-wide growth of per-enrollee health care costs, and so premium growth in line with medical trend would keep marketplace premiums in line with employer premiums next year.

Instead, however, Oliver Wyman projects that marketplace premiums will rise by 28 to 40 percent in 2018. The bulk of the difference reflects uncertainty about whether the Trump Administration will continue reimbursing insurers for cost-sharing reductions (CSRs) and enforcing the ACA’s individual mandate that individuals have health insurance or pay a penalty. Specifically, Oliver Wyman expects insurers to add 11 to 20 percent to premiums to account for the risk that the Trump Administration will withhold CSR payments, as it has repeatedly threatened to do, and another 9 percent to premiums to account for the risk that the Administration won’t enforce the mandate. (Oliver Wyman also expects the end of a one-year moratorium on the federal health insurance tax to add 3 percent to rates.) The analysis concludes, “more than two-thirds of [2018] increases will be related to the uncertainty around CSR payments and the individual mandate.”

Oliver Wyman’s assessment is consistent with other recent studies and with insurers’ preliminary rate filings. For example, Standard and Poor’s and the Kaiser Family Foundation have found that insurers nationwide improved their individual market financial performance in 2016, putting them on track to break even or make a profit this year. All else equal, that would mean lower premium increases going forward. And in states where insurers have submitted two sets of proposed rate increases for 2018 — with and without uncertainty around CSRs and the individual mandate — these proposed rates are in line with the Oliver Wyman projections, as the second chart shows.

With more rate filing deadlines approaching over the next few weeks, President Trump and congressional Republicans will likely keep citing marketplace premiums as justification for repealing the ACA. But with marketplace premiums in line with employer premiums in most of the country — and poised to remain so if not for policy uncertainty — it’s clear that the marketplaces aren’t structurally flawed or incapable of attracting a balanced risk pool. The most important thing policymakers could do to stabilize the ACA marketplaces is to stop sabotaging them.