BEYOND THE NUMBERS

It’s Time to Fix the Broken Mortgage Interest Tax Break

The mortgage interest deduction is one of the largest federal tax expenditures — it costs the federal government about $70 billion a year — yet it appears to do little to achieve the goal of expanding homeownership. This tax break needs reform, as we explain in a new paper.

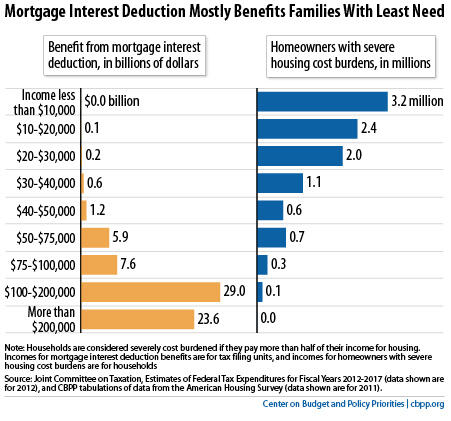

The bulk of the deduction’s benefits go to higher-income households who generally could afford a home without assistance: in 2012, 77 percent of the benefits went to homeowners with incomes above $100,000. Meanwhile, the deduction provides little benefit to the middle- and lower-income families who are most likely to struggle to afford homeownership (see chart) — and no benefit at all to more than a third of homeowners with mortgages.

Three major bipartisan panels have proposed converting the deduction to a credit and lowering the maximum amount of interest that it covers. These reforms would be major improvements over current law and would generate significant additional revenue.

- A mortgage interest credit would provide more help than today’s deduction to most middle- and lower-income homeowners with mortgages, while trimming subsidies for upper-income owners. As a result, it would likely do more than the existing deduction to help families that would otherwise struggle to afford the costs of homeownership.

- Unlike simply eliminating or scaling back the deduction, which some fear would undermine the housing recovery, replacing the deduction with a credit would make a major overall drop in housing prices unlikely. The credit would replace much of the deduction’s overall dollar value and would subsidize more households to purchase homes than the existing deduction. Congress could further reduce the risk of market disruption by phasing reforms in gradually.

- The proposed reforms could raise substantial added revenue — about $200 billion over ten years, under one version — and thereby contribute to a balanced deficit-reduction package. Policymakers could also use part of the savings (once deficit-reduction goals have been met) to address a portion of the large unmet need for assistance among renters at the lower end of the income scale. For example, the new renters’ tax credit that CBPP has proposed, if capped at $5 billion per year, would substantially reduce housing cost burdens and the risk of homelessness and other serious hardship for 1.2 million low-income renter households.

Click here to read the full paper.