BEYOND THE NUMBERS

IRS Funding Cuts Likely Mean More Tax-Credit Errors

Even as the Treasury Department’s Inspector General noted a significant overpayment rate in the refundable part of the Child Tax Credit (CTC) this week, lawmakers chose — in the pending 2015 government funding agreement — to weaken the IRS’s ability to reduce errors in this credit and other parts of the tax code by once again cutting IRS funding to enforce and ensure compliance with the tax rules. And, while lawmakers such as Senator Orrin Hatch (R-UT), the Senate Finance Committee’s top Republican, assailed the IRS for failing to address the errors, the Treasury and IRS have recommended a series of measures to Congress to reduce errors in the tax credits and other parts of the tax code — and Congress has failed to act on them (except for one very small measure included in the 2015 funding agreement).

Errors in the CTC and the Earned Income Tax Credit (EITC) — another working-family tax credit — need to be reduced (as do errors related to small businesses and various other groups of tax filers). But the debate around this issue often is misleading and ignores three significant points:

1. Most overpayments result from unintentional errors, not fraud. IRS studies indicate that the majority of EITC errors stem from the interaction between the credit’s complex rules and complicated family and child-rearing arrangements, not fraud. The EITC has very strict rules over who can claim a child, for example, which often trip up separated or divorced couples or three-generation families. The CTC eligibility rules are similar. Moreover, overclaims in these tax credits account for a small share of the tax compliance gap. Underreporting of business income alone accounted for $122 billion of the $450 billion tax gap in 2006, the latest year for which such data are available.

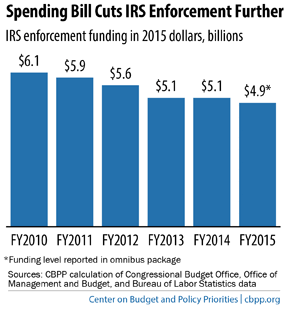

2. IRS funding cuts have weakened tax enforcement. The IRS’s budget has taken repeated hits in recent years and will shrink further under the fiscal year 2015 budget agreement, falling to its lowest inflation-adjusted level since 2000. Funding for IRS enforcement has been hit particularly hard; its 2015 funding level under the agreement is 20 percent below the 2010 level, adjusted for inflation. Yet the number of tax returns filed has grown significantly over the same period, and the IRS received substantial new responsibilities related to the Foreign Account Tax Compliance Act and the Affordable Care Act.

Because of these cuts, the IRS lacks the resources to pursue a substantial share of the questionable EITC and CTC claims that it identifies or to improve enforcement of other parts of the tax code. For example, the IRS can use data matching and other techniques to identify questionable claims on tax returns related to the tax credits, but it cannot pursue many of those claims further because it lacks the staff resources to do so. Due to budget cuts, the number of IRS staff devoted to enforcement has dropped by 15 percent since 2010.

3. Congress has failed to act on proposals designed to lower error rates. The year-end funding bill requires people who prepare their own returns to answer due diligence questions when claiming refundable tax credits, a useful but small measure. But Congress has ignored an array of other, more significant proposals from the Treasury and the IRS (most of which are in the President’s fiscal year 2015 budget) to reduce errors in these credits. These include:

- Giving the IRS the statutory authority to require paid tax preparers to demonstrate basic competence in the rules governing these credits and other basic tax matters. The Treasury has found very high EITC error rates among returns filed by certain types of paid preparers (e.g., those who aren’t lawyers, CPAs, enrolled agents, or affiliated with a national tax preparation firm). These preparers do not need to get any training whatsoever or demonstrate basic competence in the tax rules, a factor that contributes to tax-credit errors.

- Requiring employers and other third parties to send the IRS information such as W-2’s and 1099’s earlier in the year to help it detect erroneous or fraudulent claims before it pays them.

- Requiring paid return preparers to follow due diligence requirements in determining eligibility for the CTC, as they already must do for the EITC.

Senator Hatch said this week that “[t]he IRS’s inability to properly administer these refundable tax credits fails American taxpayers.” In reality, it’s Congress that has failed American taxpayers by not giving the IRS what it needs to enforce the tax code.