BEYOND THE NUMBERS

How Would the Chained CPI Affect Social Security Benefits?

Most future Social Security beneficiaries would experience a benefit cut averaging about 2 percent over the course of their retirement from the President’s proposal to adopt the chained Consumer Price Index (CPI) for computing Social Security’s cost-of-living adjustments, our brief report explains:

- For beneficiaries receiving an average benefit, the reduction would average 1-2 percent.

- For beneficiaries receiving smaller-than-average benefits, the reduction would be smaller, likely in the 0.5 percent to 1.5 percent range — except for beneficiaries poor enough to qualify also for Supplemental Security Income (SSI), who would be held harmless.

- For beneficiaries receiving higher-than-average benefits, the reduction would be larger, averaging 2 percent or slightly more.

The proposal includes features to mitigate its effects on low-income and older beneficiaries: a benefit “bump” that phases in gradually between ages 76 and 85 (as well as a second increase between ages 95 and 104). It also exempts means-tested programs — notably SSI for very poor seniors and people with disabilities — from the switch to the chained CPI.

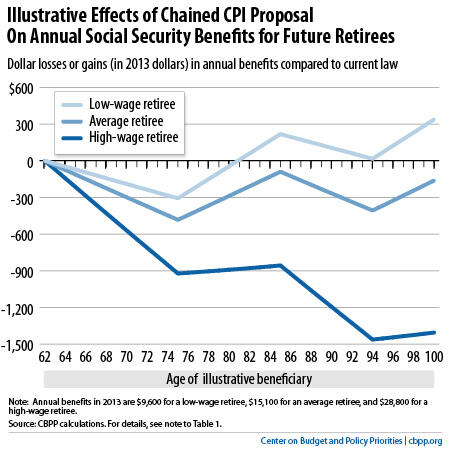

The graph shows how the proposal would affect three illustrative future retirees. Shifting to the chained CPI would reduce annual cost-of-living adjustments (COLAs) by about 0.25 percentage points a year for all three, according to Congressional Budget Office projections.

The cumulative impact of this reduction would grow over time but would be offset by the benefit bumps beginning in a recipient’s 70s and 90s.

Current beneficiaries would suffer smaller losses than future beneficiaries at any given age. Current beneficiaries now 69 or older receiving an average benefit would receive lower benefits than under current law for the first ten years, but generally would receive higher benefits than under current law in years after that. After 15 years, the cumulative change in benefits for the average current beneficiary would be near zero. Current beneficiaries receiving smaller-than-average benefits would come out ahead if they lived more than ten or 15 years.